dartmonkey

-

Posts

642 -

Joined

-

Last visited

-

Days Won

3

Content Type

Profiles

Forums

Events

Everything posted by dartmonkey

-

That all makes sense, but when they say 'FFH currently trades at 1.1x [book]', it looks like they mean it currently trades at 1.1x their estimate of year-end book value, right? Or maybe that is now 1.2x, given the share price rise today.

-

I’m sure you meant book value will be $1,400-1,450 USD by the end of the year, not CAD. $1,450 USD *1.38 CAD/USD * 1.5 = C$3001.5

-

I think the correct approach is to be agnostic about how the market will react to what may be an optically bad earnings report. As an example, just remember how we expected that inclusion in the S&P TSX 60 would drive FFH's share price out of the range of buybacks - it has done nothing of the sort. In retrospect, the market was probably already expecting the news of the inclusion, sooner or later, and it was probably already priced in. Now we are expecting share price declines in Fairfax's public holdings, slightly lower interest income, and the beginnings of a soft inisurance market, and that is probably all true, but that is probably why the share price has been stagnant. If the Q1 report is just a little less awful than we are expecting, the share price might actually rise. I'm not going to second guess the market... I'm confident this investment will do very well in the next few years, but I have no idea about the next few days.

-

It's not crazy to pencil in a bad year for a company like Fairfax with supercat exposure, but sticking it in 2028 seems pretty arbitrary. If you're going to model in that bad year, it would make more sense to see what the effect would be of one very bad reinsurance year in 10 years. Berkshire, for instance, had a year with a 115% CR (everyone knows what year), and given the fact that their average CR from 2000 to 2024 was 97.7%, that wiped out about 6 years of underwriting gains. Fairfax has a much bigger insurance float than Berkshire. More relevant would be knowing how much each company writes in reinsurance; Berkshire has reduced its exposure, Fairfax I don't know. But anyways, in a very bad year, like the one Horne thinks we will have in 2028, earnings will be low, but that hardly justifies a valuation that bakes that in as though it were a normal year for Fairfax.

-

It is good for everyone's health to see the bright side and stay positive !!! But for anyone who can only be happy if the share price is going up, the share price actually is up about 10%, both FFH and FRFHF, since a year ago, not counting the $15 dividend, so although we have been spoiled by 33% annualized price increases over the last 5 years, the price is not completely unchanged. If it is still at C$2364 by mid-June, then we could gripe that the price is unchanged over a year, or we could be happy that there are 5% less shares outstanding!

-

I'm struggling to understand how there is any economic difference between holding the TRSs with the current number of shares versus selling the TRS investment and repurchasing an equivalent number of shares with the proceeds (apart from taxes on capital gains or possible differences in how insurance regulators consider the TRSs.) If they have enough capital to buy stock on the open market, and they are limited as to how much they can buy, either because they don't want to move the price, or because they are capped at a certain percentage of shares, then I can understand holding on to the TRSs AND buying back shares. But I don't think either of those restraints applies: their NCIB allows them to buy up to 2.187m shares this year and they have never come close to buying that many shares in a year, and the average volume of shares traded is 77,000 a day, so their typical rate of up to a million shares a year, or 4,000 a day, is not high enough to materially move the market. My understanding (correct me if I'm wrong) is that buying the TRSs and buying stock are economically equivalent - in both cases, every $1 the stock moves up is $1 more in the pockets of the company. So apart from tax and regulatory consequences, if they sell a TRS on one share and use the proceeds to buy back one share, they have exactly the same return on capital going forward as if they had not sold the TRS and not bought the extra share. Whoever their counterpary on the TRSs is is effectively short FFH, and has probably hedged that position by holding an equivalent number of shares. Why not just simplify for both parties and sell the TRS in exchange for the shares held by the counterparty?

-

Not in the sense of capital gains, but there is a 2% tax on share repurchases in Canada.

-

We've discussed this frequently here and I don't think any of us really knows the pros and cons of selling this very profitable position and repurchasing an equivalent number of shares. The relevant questions, AFAICT, are tax (selling now would probably mean a big tax bill), regulatory treatment in terms of capital requirements, and volatility (if there were to be a big stockmarket drop that included FFH shares, this would hit then just when they might want some liquidity. My conclusion is that we amateurs can't really know, and I have no doubt that management will make the right decision after weighing the above considerations. In the meantime, we can either treat the TRS's as just another investment, or we can back it out the holding and reduce the share count as if the shares had been retired.

-

As I pointed out, dividends is a terrible use of capital given that Prem's goal is to internally compound book value @15%. I would rather Fairfax buys back stock with all the excess capital that can't be invested internally as long it trades below intrinsic value. My previous post referred to "return on incremental dollar" which you seem to have missed. So we are on the same page. However I would note that Prem's stated goal is 15% return on incremental dollars retained. I think you give too little credit to Berkshire & Buffett. I don't believe Buffett ever wanted to grow Berkshire's asset base at the expense of growing per share intrinsic value. If you even causally read past Berkshire annual reports, you would notice that Buffett almost always referred to maximizing per share intrinsic value. Yes, Buffett said all this forever, but he didn’t repurchase shares, until recently, so I think it’s fair to judge him based on what he did, not what he said. Watsa bought back 1/4 of Fairfax’s shares in the last 5 years, starting when it was the size of Berkshire in about 1980-1985. Berkshire started doing buybacks in 2011, so Fairfax has a head start of 20-25 years. With both companies doubling their value every 4 years or so, that means Fairfax started when it was about 2^5 or 2^6 times smaller, i.e. 32-64 times smaller. I think that gives Fairfax both a longer runway and, to the extent that shares remain cheap, an advantage in securing great per share returns.

-

Yes. At that valuation (328 Rs/share) it would mean we go from a 2720 crore INR stake ($291m) to a 3720 crore INR stake ($399m), putting it ahead of CSB bank as #3 investment, after the Bangalore investment ($2187m at year end) and IIFL Finance ($438m). Nice result so far, cost basis $51m in 2015.

-

I think your thinking is correct but it is difficult to say what Berkshire's market cap would have been under current accounting rules without doing a lot more analysis. The important thing is that it was bigget than Fairfax (adjusting for ionflation) in 1993 and may have already been bigger by 1991 or 1992. So Berkshire has about a 34-35 year headstart on Fairfax. And as you and hoodlum have pointed out, Fairfax will not grow as fast as Berkshire if it spends a significant part of its earnings on buybacks, so hopefully we will have considerably more than 35 years before Fairfax reaches Berkshire's current size. Of course, there's no guarantee that Fairfax will continue to have the opportunity of buying back shares at such low prices, but so far, so good.

-

We have talked about this before, but I looked up what year Berkshire was about the same market cap as Fairfax, and it is roughly at the end of 1995, when Berkshire had a US$38b market cap like Fairfax today. If you adjust for inflation, $38b in 2025 is the equivalent of about $17.5b back in 1995, so we need to go a bit farther back. At the end of 1992, Berkshire had a market cap of about $14b, a little smaller than Fairfax's present value adjusted for 129% inflation isnce then, but by the end of 1993, it was about $30b, as new accounting rules meant that the stock positions were marked to market. So Fairfax is very roughly Berkshire's size around the beginning of 1992, or 34 years ago. My hope is that Fairfax will buy back enough shares to materially slow its growth, so that it retains its ability to invest widely; Berkshire started far too late, in retrospect, despite his admiration for Henry Singleton and his share repurchases: https://www.google.com/search?q=buffett+on+henry+singleton&oq=buffett+on+henry+singleton&gs_lcrp=EgZjaHJvbWUyBggAEEUYOTIICAEQABgWGB4yBwgCEAAY7wUyBwgDEAAY7wUyBwgEEAAY7wUyBwgFEAAY7wUyBwgGEAAY7wXSAQkxMDA1MWowajeoAgCwAgA&sourceid=chrome&ie=UTF-8#fpstate=ive&vld=cid:7c22ca26,vid:ePg5JxYChgE,st:0

-

Any thoughts on why Berkshire has never owned shares of Fairfax? It would seem like a natural fit, and big enough to move the needle (a little) even for Berkshire. Why buy Chubb when they could buy Fairfax at a lower multiple?

-

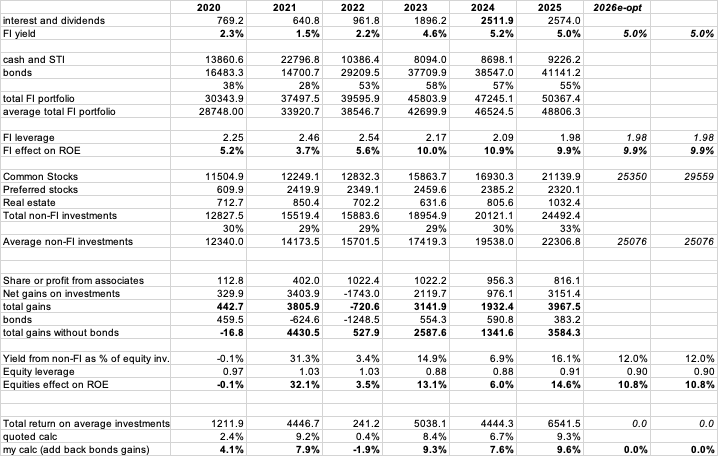

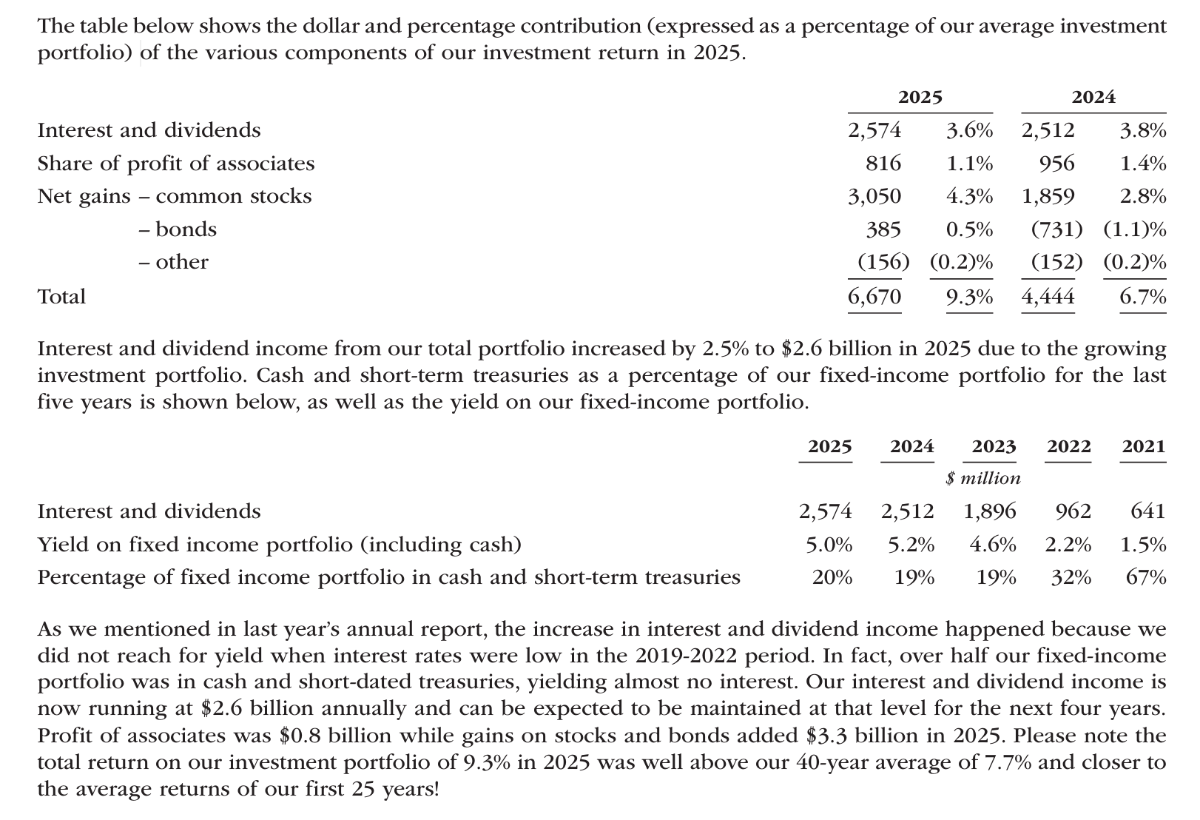

Interest and dividends are from non-consolidated and non-equity method accounted holdings as well as fixed income investment. Fixed income interest is calculated as coupon rate times par value. Yes, that's what I thought. That means that line is not helpful in trying to tease out valuations for fixed income investments separately from equities, since it includes returns from some of each. In the end, I just used the 5.0% rate the company reported (2025 AR, p.18 or p.222), multiplied by the 2.01x leverage (the size of cash and short-term investments and bonds ($51,501.0m), divided by average total equity for the year ($24,621.2m).

-

The fees are based on the increase in book value per share over a 5% annual non-compounded hurdle, calculated at the end of each three-year period. The three 3 year periods so far ended at the end of 2017, 2020 and most recently 2023, with the next one at the end of 2026. At the end of 2023, book value was $21.85, and it was $22.94 at the end of 2025 (the most recent published report; Q1 2026 should come out in about 2 weeks.) If the performance fee were to have been calculated for the end of 2025 instead of the end of 2026, my understanding is that it would be based on the 2023 high-water mark, i.e the $21.85 end of 2023 book value on which the previous performance fee was calculated, plus 2 more years of the 5% 'non-compounded' hurdle rate, which I think means just 5% of the original $10 issue price, or 2*$0.50. That would put the high-water mark at $22.85, meaning that there would be a tiny performance fee based on the difference between the highwater mark of $22.85 and the new book value of $22.94, and in fact, this amount is accrued in FIH's books, even if it is not yet paid out. The Sanmar loss will of course be reflected in the updated book value. By the end of 2025, FIH carried their 37% stake of Sanmar shares at $101.6m, a $115.5m loss from its original value (along with $134.9m in realized gains from its Sanmar bonds.) The sale at $27m would mean they will have lost an additional ~$89m, or $0.66 per FIH share, which, all other things being equal, would push down their book by about $0.55 post tax, or from $22.94 to $22.39, meaning there would be no performance fee, based on the high-water mark of at $22.85. Of course, all other things are not equal, and it is likely that by the end of 2026, book value will have increased again, for instance from a revaluing of the Anchorage stake. Meanwhile, the high-water mark will have increased by another $0.50, to $23.85, and we will see if book value has increased enough to trigger another performance fee. But in any case, the Sanmar loss will eventually be reflected in the performance fee, decreasing it by about 20% of the $0.55 per share loss, or $0.11 per share. So, yes, the Sanmar loss will in effect trigger a reduction in the performance fee from what it would have been without the loss, and it should be accrued to the books in the Q1 report, even if there is no immediate cash payment from FFH back to FIH.

-

Makes a lot of sense. Or maybe just split the FIH stock into an Anchorage part and a 'rest of FIH' part, by sending out an Anchorage stock dividend to FIH shareholders. I doubt it's going to happen, but it might resolve a lot of the insatisfaction.

-

Well said!! I don’t think it’s well said at all. There’s nothing they have done with Fairfax India that in any way contradicts their claims to integrity, in my opinion. The share price has been a disappointment, but that’s not their fault. The incentive fees based on book value were clearly explained at the outset and have been followed - in fact , if anything, they have low-balled the book value on the assets that are not marked to market, reducing the fees. I invested a higher percentage of my own assets in this investment than I should have, but I have only myself to blame for that. I hope the share price catches up to fair value, and I expect the Anchorage IPO will do a lot of the work here. In a few days or a few years we will wake up to a share price of $40 and wonder what happened, and this talk of a ‘black mark on their reputation will look as silly as I think it is.

-

Fair enough not 0, 3-4% but a meaningfully lower return than buying back your stock at <10x earnings Edited 50 minutes ago by djokovic1 Say they get 3.7% (the 1-month, 3-month and one-year Treasury rate). Then pay 20% income tax, so it's 2.96%. Inflation in the USA is 2.4%. So investing in short-term treasuries is a good way of not LOSING money, but it's only a 0.6% real return, so thinking about it as zero is pretty close.

-

petec said: I don't think that's accurate. If you don't know why it's cheap, I am not sure that you really know that it is cheap. There are two kinds of 'why it's cheap'. The kind of 'why it's cheap' that value investors care about, is, it's cheap because it trades for 8x last year's earnings in a market that is trading at 25x, I think the earnings are sustainable and will even grow, so that's why I am saying it's cheap. The kind of 'why it's cheap' that a 'quality investor' might use is "it's cheap because, duh, it's an insurance company, it has no moat, it shorted tech companies and bought Blackberry. So a value investor can perfectly well say "I think it's cheap, but I don't know why", meaning that they don't know why the market is giving them such a low offer but they have good reasons to think it's cheap, so it will do well in the long run, even if they don't see any way out of the low multiples.

-

Yes, the behaviour is similar but the timing and the pricing are very different. Buffett keeps gobs of cash on the sidelines, like you, but he doesn't seem to ever deploy it, since the stockmarket drops we have experienced in the last 20 years don't seem to take us into what he considers bargain territory. Perhaps this is the curse of being 95 years old and having known times when stocks got really, really cheap compared to today's prices. You on the other hand are prepared to go from 30% to 90% invested after the S&P 500 is down just 7% from its all-time high, or down 5% from the end of 2025, or up 15% from a year ago, however you want to think about it. This seems to me almost indistinguishable from fully invested. I am in a similar position, fully invested right now. I guess if the market drops by 40% this year, Buffett will have the last laugh, but he sure has been waiting a long, long time to be right.

-

I do use earnings of $3584.3m (was 3584.2 a typo or maybe I have a typo somewhere? I have $3,967.5 total gains, and subtract off 2025's $383.2m in bonds gains) in the numerator. In the denominator, it seems to me more logical to use the average non-fixed income portfolio for 2025, not the beginning of the year and not the end of the year, so I just use the straight average of end of 2024 and end of 2025. For common stocks, that would be $16,930m and $21,139m, but since I really just want to separate out fixed income (cash, cash equivalents, short-term investments and bonds) from the rest, I also lumped in preferred stocks and real estate along with common stocks, and took the average of these values at the end of 2024 and the end of 2025, so I ended up getting $22,306.8m as my denominator, for a return of $3584.3m/$22,306.8m = 16.1% for non-FI for 2025. The average for the last six years was 12.0%. It's a work in progress, but I'm getting there...

-

I actually used the average of year-end 2024 and year-end 2025 as the denominator, which I call “year average fixed income portfolio”, but you are right, 2025 year-end value is not relevant.

-

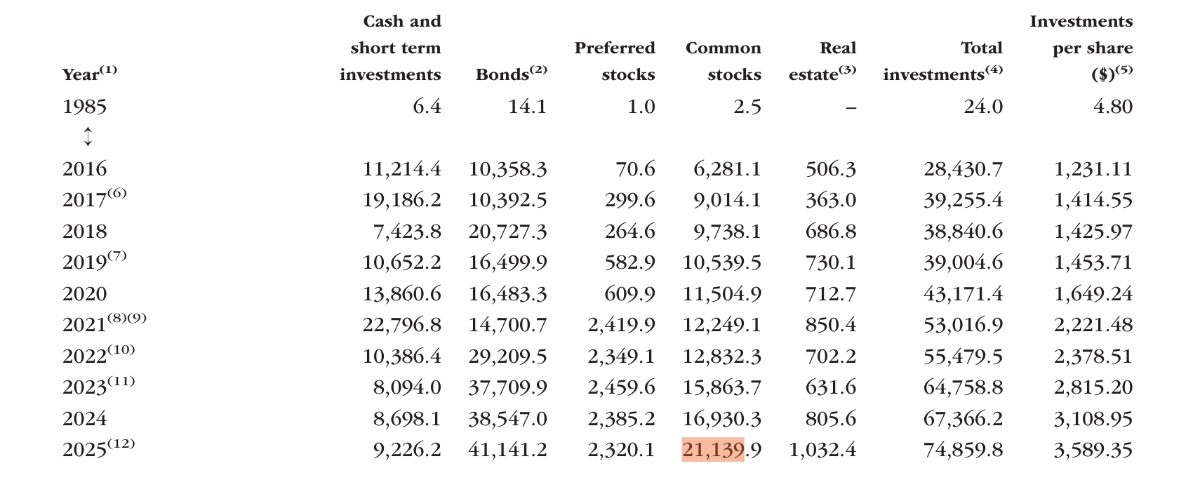

First of all, you are looking at the wrong year: last year was 2025, not 2024, and the equivalent numbers for carrying value and market value are up to $20.5b and $23.6b, iin the table on p.16 But I actually used another table, giving the carrying values of common stocks, on p.179 (of the 2025 AR): Thinking about this further, (a) I don't know why the two numbers, $21,139.9b and $20.5b, are not the same, and (b) Since I am interested in separating invesment results into fixed income and non-fixed income, I really should be adding the returns from preferred stocks and real estate, not just common stocks. I'm just not sure that the line item 'interest and dividends' only pertains to fixed income interest and dividends; does anyone know? For that matter, some of the common stocks issue dividends, too, so if they are included in 'interest and dividends' (for instance, as below), I don't know how I can isolate fixed income, except by using their yield on fixed income (5.0% last year) and estimating how much that represents, based on the size of the fixed income portfolio. If anyone has any thoughts about this, they would be welcome. Here's the extract from p.17 whose wording makes me feel that when they refer to interest and dividends, they are just talking about fixed income dividends, not common stock dividends:

-

I never understood this expression, "you can't have your cake and eat it too", because of course you can have your cake and then eat it. What you can't do is eat it, and then still have it. So the original English expression, "you can't eat your cake and have it too*" makes more sense than the inverted North American one that I and probably most of us grew up with. In Fairfax's case, of course, you can eat half your cake and keep the other half, with no contradiction, and that seems like a great compromise. They accomodate their investing partners that wanted more that wanted more shares, while taking some money off the table which will be useful for buybacks (Safety will probably correct me and say that most of it willl stay in the subsidiaries; Gemini tells me that "The holding is primarily managed through Fairfax's investment affiliates"; but I guess some of this could be dividended up to the holding company...) But at the same time, they keep some cake for later by keeping a big share in a company that is performing well... ======= Interersting fact: The Unabomber was in part caught because his brother David, who read his manifesto, recognized what he thought was "a weird version of the common idiom 'you can’t have your cake and eat it too!'—both Ted Kaczynski and the Unabomber inverted it into 'you can’t eat your cake and have it too.' In fact, the Unabomber was just using the more logical, original version of the expression, but this was unusual enough for an American for David to suspect that the Unabomber was his brother Ted.

-

I think this is a good point, and it illustrates how we will go astray if we look at, say, the 10 biggest Fairfax investments today and how they have done (survivorship bias), vs looking at the 10 biggest Fairfax investment 10 years ago and seeing how they have done going forward.