All Activity

- Past hour

-

-

-

-

Buffett/Berkshire - general news

ValueMaven replied to fareastwarriors's topic in Berkshire Hathaway

Wow. Really interesting. The last few moves have been awesome...high quality companies in depressed industries: OxyChem, Taylor, and now another homebuilder -

Cato Institute: World Hyperinflations

-

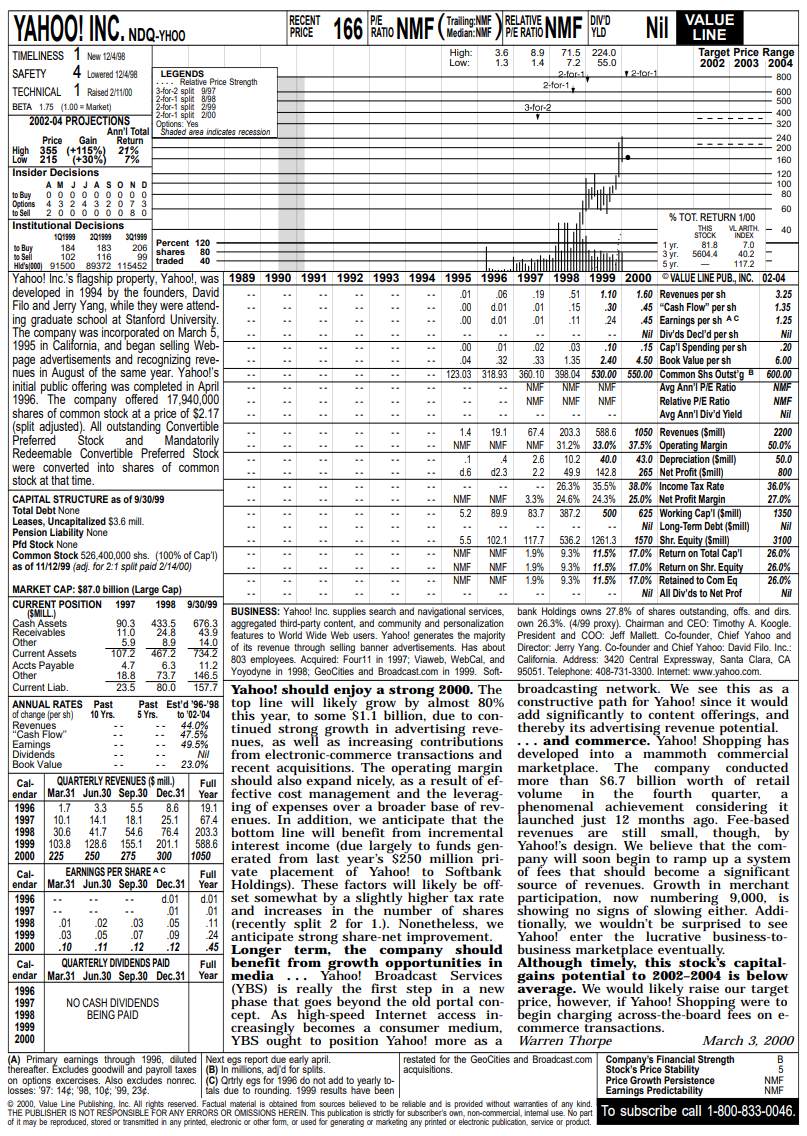

I figured out how to get ahold of some and thought they were cool. 2008 - Washington Mutual.pdf 2008 - Lehman Brothers.pdf 2008 - Freddie Mac.pdf 2008 - Fannie Mae.pdf 2008 - Countrywide Financial.pdf 2008 - American International Group.pdf 2002 - Yahoo!.pdf 2001 - eToys.pdf 2001 - Enron.pdf 2000 - Yahoo!.pdf 2000 - Cisco Systems.pdf 2000 - Amazon.com.pdf

-

Sure but it would give a certain short seller another opportunity or at least something to think about - especially if they still hold the same beliefs about the company. Just thinking out loud - you guys are great and help crystalize these issues.

-

They will get more creative. Yes, the TRS trick could always be used again.

-

They will get more creative.

-

You might have a higher return hurdle than they have. To me it easily clears their 15% return hurdle.

-

Can't really speak to UA and Andrew Peller b/c admittedly don't follow those industries and candidly don't understand what Fairfax management sees there. So to answer your question, would probably prefer Fairfax buybacks to THOSE investments (little as I know or care about either). And b/c of your point that dividends are and can be sent by insurance subs to holding company, not sure it matters specifically which is buying what - they're all part of Fairfax Financial. The point I was trying to make is that Buffett passed on repurchasing BRK shares at times when the stock traded at and below BV, i.e., ridiculously cheap - for reasons I could never understand. Fairfax is not at such a price, though it is cheap enough for me to have purchased shares this year at various times. But it raises the thought that what if Fairfax repurchases its limit of stock for the year and then the stock price craters to BV or below?

-

I don’t think they want to sacrifice the 3:1 investments to equity leverage. I’m very happy for that. They are turning over the portfolio which allows them to keep making new investments. The risk/reward buying FFH is better than anything else they could buy.

-

The $1.7b they have spent on share repurchases is a big investment, and I agree that it is reasonable to ask whether they didn't have other, better opportunities. I wouldn't want them to buy back shares if it meant they couldn't take out minority holdings like Allied. But how would you compare buying more Fairfax to buying Under Armour, for instance, or buying wine producer Andrew Peller? I have SafetyinNumbers on the conscience, and I am imagining him saying, right now, that we are failing to make the distinction between the insurance companies (who are buying Peller and UA) and Fairfax the holding company, buying Allied and doing repurchases. But to some extent, the insurance subs could be buying more things like Peller and UA instead of sending dividends to the holding company to repurchase shares and buy out preferred shares and buy out the minority interest in Allied. So it may be fair to compare acquisitions, whatever level they are at. I for one think that Fairfax repurchases are a very sensible investment, and if they can't sensibly expand their insurance holdings, I would just as soon see them repurchasing rather than increasing the dividend or, like Berkshire, just holding onto a mountain of cash. And I like to see them stay small and nimble, like Berkshire was at an equivalent point in its trajectory. By my calculation, that would be in 1992, when Berkshire had a market cap of $15b, which would be the equivalent of Fairfax's current market cap of $35 in 2026 dollars. I expect Fairfax will keep growing, but I selfishly want it to stay under $100b for the foreseeable future, and not get to Berkshire's $1.1t where small opportunities like the $1.4b Fairfax paid for Eurobank in 2014 don't move the needle.

-

I thought your reasoning was correct, then it occurred to me that, if they're bumping up against the 10% limit, they might not want to close the positions, because they don't have the capacity available to buy back the shares. In that scenario, if you pretend the TRS is approximately like a buy back if you squint, then the volume of shares the company can acquire through the combo of a maximum 10% buyback and maintaining the TRS is effectively higher than the combo of a maximum 10% buyback and closing the TRS (while being unable to buy back shares equivalent to the TRS because of the 10% limit.)

- Today

-

I think this is a good way to think about it. The TRS position is basically leverage on their own shares. Fortunately, they are in a strong enough cash and leverage position that the volatility can be handled without too much problems. They also bought so low that the likelihood of needing to pay on them for further drops was remote. At least we can say that in retrospect. Does anyone know the run rate cost on keeping this position going? I guess the only other thing to consider is that if the share price does fall, they have to pay up cash to Settle, at the same time that it would be opportune to buy back their shares as well. I'm sure they have a good strategy around this investment, and we will realize what it was in due course.

-

You may be right. Perhaps I'm viewing the issue more as a Berkshire shareholder with a younger Buffett at the helm. They are different companies and different management teams. Gotta always keep that in mind.

-

Not really, unlike what you are implying, what I was saying is if they cash out the gains on the TRS and simultaneously buy back the shares when they are priced lower, you'd actually be gaining from the increase in share price. The only thing you would be locking in is the lower taxes. That's a subtle difference.

-

But equally it's better for continuing shareholders and best when done sooner than later. Berkshire has been sitting on $150B plus for over four years now. They've just let the cash pile up, keeping it in treasuries, etc. While I realize that gives them optionality; the share price has gone from roughly 300 to 500 during this time. There's no way they generated anything close to that return in cash. And what's worse they would still have had $180 billion if they just bought back their own shares at that time and we know raising capital would never have been an issue for them with their AAA rating. So, I don't think it's good or bad. I think it all just depends on the share price compared to the intrinsic value. And like you said when the share price is low, the alternatives perhaps look less appealing. Fairfax is what they know better than any other external investment they will make, I believe it should serve as the benchmark hurdle on which all other investments they make should be judged. As we saw with the Brit acquisition, Allied world acquisition, and many others over the last decade when the right opportunity comes they're willing to buy, even at the expense of temporarily diluting their share count, or partially monetizing their subs, presumably because even though their shares themselves maybe undervalued, they felt certain that what they were buying was even more undervalued and strategically important. That's exactly the type of capital allocation thinking that you would want as a long-term shareholder.

-

For me, the question is what they are spending it on. Ironically, as a long time Berkshire shareholder, I felt the exact opposite way when Buffett completely shunned share buybacks, particularly during the dot com era and during the financial crisis though Buffett was understandably concerned more with the latter. I guess my feeling is share buybacks should be a tool and are more appropriate for larger, more mature companies. Truly hope they don't try to buy back 10% of the company each year for lack of other ideas.

-

The share count is shrinking, the balance sheet is still growing. They are spending < earnings on buybacks.

-

This would be by the September renewal. They can reup then albeit on the lower float size. I think about it on a calendar year basis b/c of the disclosure around dividend capacity for the insurance subsidiaries. On that basis it’s $1.7b so far this year. I think they have $700m-1.3b left which should be enough to buy the 700k shares. They could always get more creative if those are easy to buy.

-

maybe hedge with assets uncorrelated. or avoid bubble sectors.

-

Good question. I'm old enough to have been through a number of downturns, beginning in Oct. 1987 (though admittedly didn't have much back then). Never felt the need to hedge b/c always felt the asset mix was appropriate and had sufficient income coming in, which is probably the main point.

-

@Red Lion You are right, 3% is excessive. 1% might work if the hedge can throw cash to be invested as market goes down. "Maybe 10-15% tops to avoid selling during a protracted down market." - This sounds about right to ride out downturn. @73 Reds DCA works well if downturns happen early in career. In my case, annual additions are getting small relative to portfolio. The critical thing seems to have enough cash cushion to avoid selling during multi-year down markets like 2000-2003. A more general question - why would anyone hedge? Is it to manage short-term risks?

-

Fairfax is but a tiny fraction of Berkshire's total market cap. When Berkshire was the size of Fairfax, no one was even considering the possibility that Berkshire would outgrow its investment possibilities (I don't think they have even today). And when Berkshire was worth just shy of $40 billion, that same $40 billion was worth a lot more. No question, share buybacks are fine if they are the best investment available to management at the time. My question always is whether that is the case. Because of Berkshire's size, that question is more easily answered in favor of Berkshire. Fairfax still has a lot of growth ahead and shrinking the balance sheet to such a large extent at this stage gives me pause.

-

That‘s an interesting observation, and another accounting difference between share repurchases and the TRS, since swings in share price don’t affect earnings if they have bought back shares but do affect earnings and book value if they have established TRS instead. This means that the TRS might tend to increase volatility, which is just what we should want, given the fact that Fairfax takes advantage of low share prices to repurchase more shares. Share repurchase limit is 10% of float, or 2.1m shares, yes, thanks for the correction. That means they still have about 0.7m shares they can repurchase this year. If they have spent $2.8b on shares this year, maybe they will get to about $3.7b by September, reducing share count by a stunning 10%, but also preventing them from getting that much bigger. For comparison, they had record profit of $4.8b last year, and paid out about $300m in dividends in January. Yes they have sold some equities (Orla, Poseidon and Eurolife) but they can also buy back Allied and preferred shares, so altogether, 2026 will be a year where they will have postponed their growth in market capitalization, allowing them to remain that much longer in the sweet spot where they are big, but not so big that small investments stop moving the needle, a problem that Berkshire has run into by not paying dividends and only repurchasing small numbers of shares. There‘s a lot to be happy about with Fairfax in 2026, despite (and, to some extent, because of) the lull in its share price.