All Activity

- Past hour

-

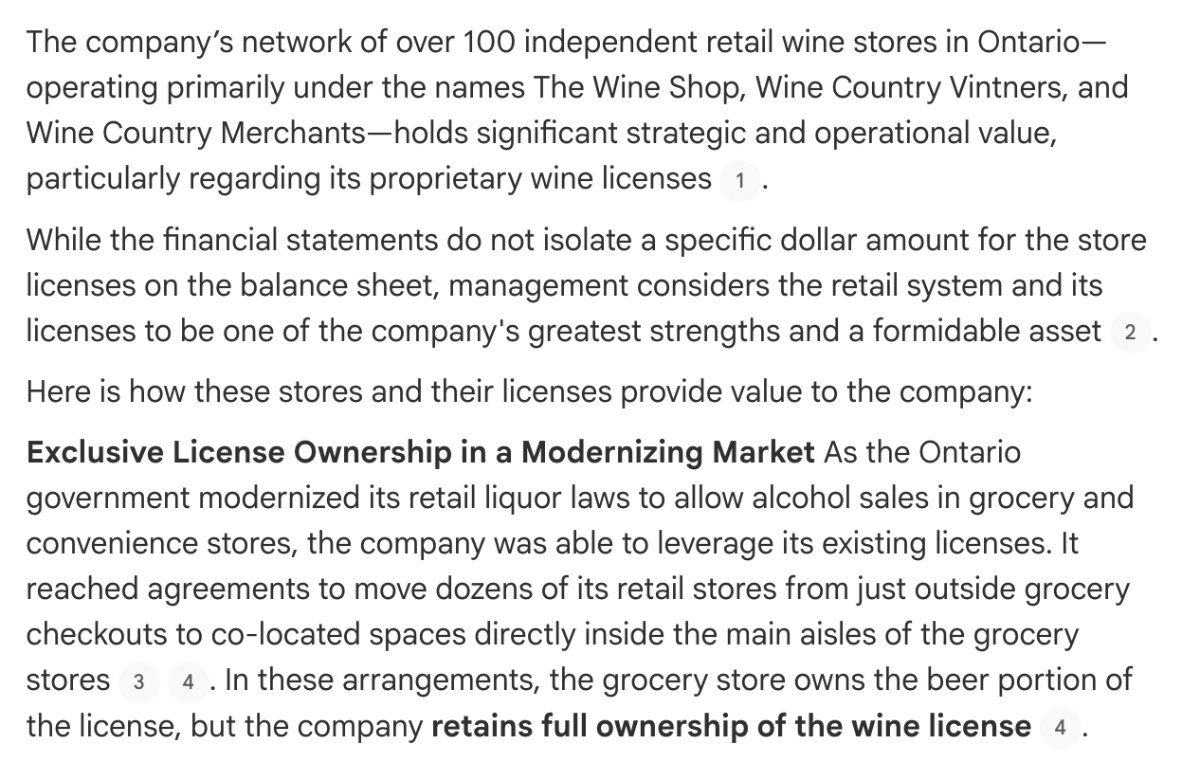

Another important thing is the retail wine store licenses the company owns.

-

S&P500 total return has been ~12.7% since 2018. Fairfax’s equity portfolio has smoked that return over the same timeframe. Especially if you calculate Fairfax’s CAGR using carrying value (which is comically low) and include FFH-TRS (which has a very low cost basis). The problem is people do not appear to want to follow the math… (in fairness, it is complicated to calculate).

-

Yes, no argument. But to play devil's advocate, stock indices have done extraordinarily well since 2018 too. Not to suggest they invest in broad equity indices but there a lot of public companies that have done very well.

-

The construction project for a developer at Port Moody Winery would be in the range of $800- $900M CAD per John Peller (Prior CEO). See transcript from their 2023-11 call. Now, where Real Estate is currently in Canada it might not be Viable, but definitely worth a lot in the right hands over time.

-

A: CAGR = 25% (I think that is in the ballpark for both holdings) I think Fairfax has been doing quite well since 2018 with their equity portfolio. Short answer: they are wired the way they are wired. These days, I like it. I don’t always understand it. But I didn’t like/understand the Stelco purchase - and I was the idiot. My focus these days with Fairfax is results - how are the individual positions performing and, more importantly, how is the total portfolio performing. Over the past 5 years they have been hitting the ball out of the park - so I am a happy camper. PS: they did load up on ‘quality’ big caps coming out the the Great Financial Crisis. Their problem was they had to sell them too early to cover losses from the equity hedges/shorts. Its not like they have never done it before.

-

I'm curious why you say this. At the time there were large protests against the regime, and the regime there is bad for both the Iranian people and the rest of the world. To my way of thinking at the time, there was maybe a 50% chance of the Iranian people enacting their own regime change, and it was also unclear if Iran could potentially close the strait against the USA's military might. And, it distracted Trump, preventing him from attacking his allies. So to me, it looked like a reasonable bet at the time. What, at the time, made you think that it was an obvious foolish thing to do? Did you just have a different estimate of the probability of positive regime change, or were more confident than me about Iran's ability to control the strait?

-

I wrote about it on X

-

Sure they've done well (you can answer the question more precisely, LOL). Your point about spreading themselves too thin in 2014-2017 explains a lot. But there have been some excellent stocks bantered about on this forum over the years that would seem to fit in their wheelhouse that require no involvement on their part at all, yet with rare exception they often take the more difficult path. Not a criticism, just a question as to why.

-

I don’t think they are averse. I think they go to where they see the most value. Here is a question for you. The two biggest investments they made in 2018 were Seaspan and Stelco. What is/was the return (CAGR) each of these investments generated since then?

- Today

-

One of these times, he ain't gonna be able to get out. And we'll all be standing there right beside him.

-

Steps of success according to Trump: Step 1: Create an unnecessary problem that has the potential to cause chaos Step 2: Work yourself to the brink of said chaos, terrifying the entire world in the process Step 3: TACO right before chaos is unleashed Step 4: Announce complete and total victory while rejoicing in the fanfare of your brainless supporters Step 5: Repeat

-

Munger: "I think Berkshire is sort of a temple of rationality. What's really admired around Berkshire is somebody who sees it the way it is. Wouldn't you agree with that Warren? More than anything, more than energy, more than..." Buffett: "You better see it the way it is."

-

Lots of folks rushing to dance on Trump's deal here.....obviously IMO i think it was foolish to do what he did re: attacking Iran in the first place and things will have to be conceded at the negotiating table here because whatever way you slice it Iran has cards and leverage it can trade.....but if you take that out of the mix here I will say one thing I'm not sure many of our recent President's having got themselves into a mess like this would have the gumption to steam roll the neocons in their own party, ignore the naysayers from the left all while Israel/Bibi/AIPAC launched a relentless campaign to scupper and talk down the deal and Trump via sheer force of personality is steamrolling them all into it here whether they like it or not......as I said lesser Presidents would have doubled/tripled down by now in Middle East hoping to please the usual D.C. stakeholders and Trump is telling them to go sing.

-

Interesting observations and history lesson. Why do you think that after 2017 they still remain averse to most well-followed, larger public equities which require no active management?

-

Grand Old Perverts Bunch of rapists and closet cases.

-

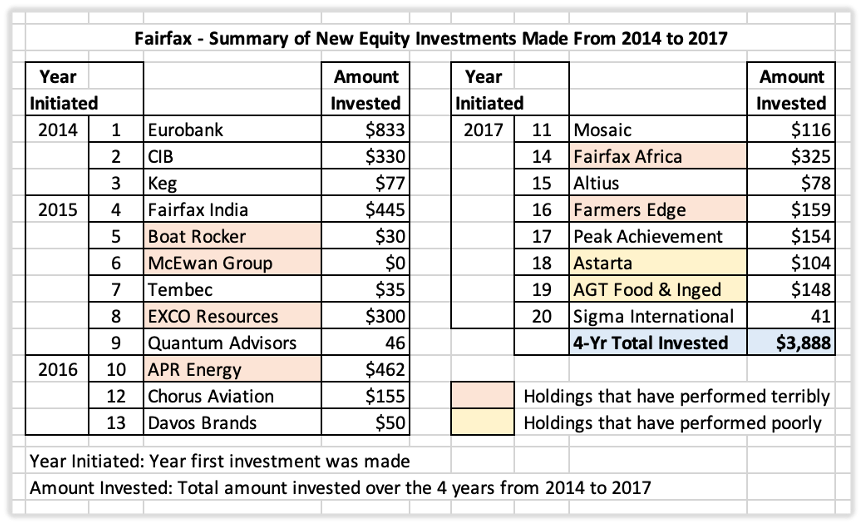

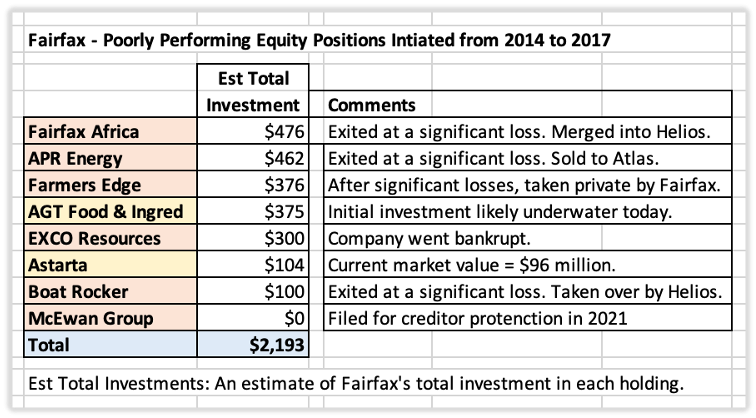

A Review of 2014 to 2017: Old Fairfax – Too Many “Chronically-Leaking Boats” This article #3 in my historical review of some of Fairfax's investments. “My conclusion from my own experiences and from much observation of other businesses is that a good managerial record (measured by economic returns) is far more a function of what business boat you get into than it is of how effectively you row… Should you find yourself in a chronically-leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.” – Warren Buffett – Berkshire Hathaway 1985AR Fairfax defines value investing as purchasing securities at prices below intrinsic value while maintaining a margin of safety. The approach is explicitly long term and places unusual emphasis on downside protection and the avoidance of permanent capital loss. From 2014 to 2017, Fairfax doubled the size of its insurance business through aggressive international expansion. As a result, the company's investment portfolio grew significantly. Fairfax also expanded its equity holdings. During this four-year period, it established approximately 20 new positions and invested roughly $3.9 billion. The results were mixed. A number of investments performed well. Unfortunately, many did not. New Purchases: Too Many Clunkers Over the years, Fairfax invested approximately $2.2 billion in eight companies that would go on to produce disappointing results. Two investments largely went nowhere: Astarta AGT Food and Ingredients While neither investment resulted in a significant loss of capital, both generated little return for shareholders over a decade. The opportunity cost was substantial. Capital tied up in stagnant investments cannot be deployed into better opportunities. Six other investments performed much worse: Fairfax Africa EXCO Resources APR Energy Farmers Edge Boat Rocker McEwan Group These investments resulted in significant capital losses. Given Fairfax's emphasis on downside protection and avoiding permanent capital loss, the results were particularly disappointing. What Was the Problem? The problem was not that Fairfax had losing investments. Every investor has losers. The problem was that too many investments shared the same weaknesses. A pattern emerged across many of the holdings: Weak management Weak balance sheets Weak profitability Many suffered from all three. From 2014 to 2017, Fairfax accumulated too many businesses that could fairly be described as chronically-leaking boats. The Overall Portfolio Was Getting Worse The problem extended beyond the new purchases. At the same time Fairfax was making these investments, its equity hedges were forcing the company to sell some of its strongest holdings. Several existing investments were also struggling, including BlackBerry, Resolute Forest Products and Recipe. Fairfax was selling some of its better businesses while adding a number of weaker ones. The overall quality of the equity portfolio was deteriorating. Why This Was a Problem for Fairfax Weak businesses tend to share two characteristics. First, they often consume capital. Companies with weak economics frequently require additional investment simply to survive. Second, they demand management attention. Turnarounds are rarely passive investments. Neither was a good fit for Fairfax. Years of losses from the equity hedges had already reduced financial flexibility. At the same time, Fairfax operated with a highly decentralized structure and a lean head office. The company was not built to oversee numerous troubled businesses simultaneously. As business performance deteriorated, many investments required additional capital and more management attention. The situation became increasingly difficult to manage. The Real Lesson In hindsight, the issue was not bad luck. The issue was process. Fairfax's investment framework had drifted too far toward lower-quality businesses at precisely the time the company needed to move in the opposite direction. “Time is the enemy of the terrible company.” Many of the companies Fairfax was buying required additional capital, intensive oversight and successful turnarounds to generate acceptable returns. Those requirements were increasingly at odds with Fairfax's decentralized operating model and lean corporate structure. The result was a growing mismatch between the businesses Fairfax was buying and the organization Fairfax had become. Fairfax eventually recognized the problem and adjusted its approach. The result was the birth of what I like to call New Fairfax. That article - the last in our series - will be out tomorrow.

-

Make it 3

-

Sure thing @Blake - do you approve of topless trannies running around the White House lawn? Is that dignified enough for you?

-

Yeah, was kind of thinking the same thing.

-

this narrative of Prem supposedly making capital allocation decisions for philanthropic reasons is tired.

-

Why are all you Trumpies so ferociously obsessed with trans people? I feel like I could count on two hands how many I've seen in my entire life. I'm starting to realize that much of human behavior is actually inverse to itself: extreme arrogance masking insecurity, anger veiling fear, that sort of thing. Why then are some of you so fixated on trans people? Is there something you would like to share with the class @cubsfan?

-

In Trump world, any level of taxation is basically socialism at the same time that spending $10 trillion on defense is essential and "You better not touch my Social Security money."

-

Can I please see this propaganda?

-

Hmmm... let me meet somewhere in the middle with the Trump bunch. I personally don't like Platner and think it's kind of crazy that the Democrats are championing someone who had a totenkopf tattoo and espouses antisemitic content. Now then, is it crazy that I also don't approve of having a felon as our president? How about not supporting a man who instigated his followers into storming the U.S. Capitol building? Am I crazy for thinking that Trump blowing out budget deficits isn't good for the long-term health of our economy? Here I go trying to bang my head against the wall again.

-

Charles is actually doing a great job as a King. He had lots of time to prepare.