BG2008

-

Posts

3,145 -

Joined

-

Last visited

-

Days Won

1

Content Type

Profiles

Forums

Events

Everything posted by BG2008

-

Does anyone know why Valuewalk is so Spammy lately? I get 2-3 e-mails a week from them and frankly the content is more along the line of Cryptocurrency and No Fail "5 Year" retirement plan. What happened?

-

Speaking to start-up hedge funds - what to look out for

BG2008 replied to tol1's topic in General Discussion

I think the most important thing is qualitative and character related. I am assuming that you are considering joining a start up fund in a role of co-founder, partner #1-5, or as a primarily asset raiser. In case these are correct assumptions, I would suggest that you try to figure out the following: 1) Who are you getting in bed with? Is the guy/gal someone that you would let your wife and kid manage money with in case you got hit by a bus. If the answer is absolutely yes, great. If the answer is no or maybe, you're probably better off not going forward and I can save you a lot of time. Keep in mind, there are two aspects to this. One is the your perception of the person's ability to compound capital on a risk adjusted basis over a long period. The second part maybe more important, the person's character. There are a lot of people who will pass the first test by a mile, but I will not partner with them due to the second part. If they are the takers type in the classic taker, giver, and matcher examples, I would suggest that you back away. A taker will try to take something from you at every opportunity. 2) What is your role? Will you be co-portfolio managers? If yes, I would recommend you stop. The track record of Co-Portfolio managers is terrible. I guess it's because the fund eventually run into performance issues. Then the finger pointing starts. If you are the sole CIO, then you look in the mirror and you said, I screwed up, let's regroup and move on. Investment by committee is usually a terrible idea. This doesn't mean that you can't let your trusted friends smell test your ideas. I actually endorse smell test by your friends. Typically roles where your function is vastly different than your partner tend to work better. For example, your partner does all the capital allocation and you bring the fund raising capabilities. Those relationships tend to be healthier and enduring. The only example of co-portfolio manager that seems to have endured and prospered is Scoggin Capital Management. 3) How will you guys pay bills? What about the most basic research items like travel and subscriptions etc. What is the AUM at launch date? Do you have W-2 wages now? Just understand that you maybe going from a stable paying job to something that is likely bootstrapping. You generally need $10-20mm of AUM to kind of pay for expenses and pay yourself a living wage assuming you guys actually charge a management fee. This is lesser of an issue if you guys have a good chunk of savings yourself. I think if you are very passionate, this is lesser of an issue. I think item 1) and 2) are deal breakers. Item 3) is more along of the line of how willing am I to live below my means for an extended period of time. 4) Follow the the advice others have mentioned. Once you're past 3) I think you're good to follow the process and line of questions that a job seeker at a HF would consider. -

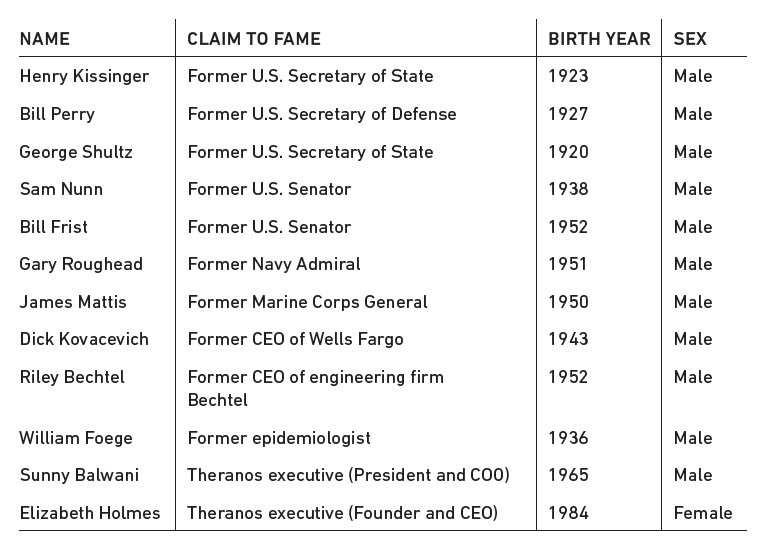

I wonder what would've happened if they had a woman on the BOD. Maybe another female would've smelled the bullshit? That's a pretty crazy BOD of who's who.

-

There's a big difference between selling a future dream/vision and lying about past and present facts. I think that's where Theranos crossed the line. If you read SEC's complaint, they highlight multiple instances of egregiously false statements originating from the top, just to keep the story alive. Theranos went beyond simply "highlighting the amazing stuff." It began fabricating facts that it knew didn't exist. For instance, Holmes told that Theranos’ technology had been deployed by the DOD in Afghanistan when that was never the case. I don't know if Bezos ever made factually incorrect claim, that he knew was false, to raise capital. Such lies are not the same as consistently overestimating future production levels because investors treat, or should treat, a statement of fact issued by a company differently than forward looking projections. There's a HUGE difference between saying "our company has $1B cash on the balance sheet today" VS "We predict our company will have $1B cash on the balance sheet by next year." I think the only reason Theranos' BoD were such accomplished heavy weights (that had nothing to do with the medical field) was to keep the story alive and to fly under the radar for as long as possible while arousing minimal suspicion. Textbook definition of a "con artist." Lie about the future - No biggie Lie about the past - Jail Time Likely

-

Tilson's latest intrinsic value on BRK as at 27 Feb 2018

BG2008 replied to kiwing100's topic in Berkshire Hathaway

Is the intrinsic value increase of 6% appropriate? It seems like it should be higher from my experience (assuming no market collapse which will drag the equity portfolio down significantly). -

Thanks for the note. I'll reach out to Gio

-

"If you're going to somewhere like Naples, then you do want to be a bit more careful than Milan." - Could you elaborate on this? Could you elaborate on the pick pocketing? Ways to lower the chance? I've gotten my stuff stolen in Spain before. It's annoying because you have to get new Drivers License, CC, etc. Anything else I should be aware of? Generally, we're doing a Milan, Venice, Rome, and Florence trip I want to clarify and give a perspective on my question. If I had a good friend booking a flight to NYC and they said that they were about to book an Airbnb in East New York and will take the subway to Manhattan. I would tell them "hold on a minute." I would also tell them don't make eye contact with people asking for money. Once you make eye contact, they know they've got you. I have no idea what it is like in Europe. As a value investor, I am just trying to do the best for my family with the research and risk mitigation etc. In short, I don't want to book a nice AirBnb in the European equivalent of "East New York." Yes, there are more No-Go Zones in the US.

-

What about GE? Yes, there's a lot of issues. But they tend to be #1 or 2 in most of their product categories. Clearly Immelt has been a waste of space for the last 15-20 years. I remember him speaking to my Mech/Aero engineering class at Cornell in the early 2000s. I always felt that Welch's shoes were too big to fill. Maybe 3G's strategy may actually work at GE by streamlining that business.

-

Well, it is the most important investment.

-

I think telling your wife that the ROI on renovation is low is a mistake to start out with. Unless your wife has drank the value investing cool aid like all of us on this board, reasoning with her from a ROI perspective is setting yourself up for disappointment. I would never lease a Acura MDX myself. I think an Acura TL with totally fine despite having a newborn. But the Mrs. wants to be able to take one car to go to dinner with the in-laws. In a happy marriage, you're not going to get everything right. But the major things are important. They go something like this: 1) Happy wife 2) Agree on same values - savings, kids, tight family etc 3) Don't do crazy things - bet the farm on whatever crazy investments is I think your objective should be to understand why your wife want it. If she cooks a lot and wants a nice kitchen so that you can have your close friends and family over for memorable dinners and gatherings, that ROI is actually much higher than whatever hard numbers you can measure. If you just can't afford the project, be honest and upfront. Just make sure she's not going to change her mind and want something else. I also think you'll have a better chance of talking your wife out of the project if you genuinely paid attention to why she wants the project. Remember, Buffet paid $30,000 cash for his house and never regretted it. BRK.B has done 2,400,000% since 1965. So if you viewed it from that perspective, it can get depressing. If the grand wizard thinks it's okay, then I think it's alright. 10 years ago, I would've been more ROI focused. Now that I have a newborn, I understand why you want to buy into a nice neighborhood etc.

-

I have read in the news about European No-Go Zones where the police cannot enter certain areas or regions without backup. Do such a zone really exist? Have they gotten worse after the recent migrant crisis? If one is concerned about safety for his family while traveling aboard, what is the best way to avoid this? I know we have quite a bit of a European constituent on this board. Please share your experiences. If you have details on Italy, it would be greatly appreciated.

-

Companies -truly long term focused not managing to quarter results?

BG2008 replied to Nell-e's topic in General Discussion

I think a lot of the returns for Vornado is due to the unique circumstances of NYC getting safer, interest rate going from 8-10% to sub 3%, the kale eating crowd crowding into NYC, coupled with a land constraint location. I know a lot of people who have levered returns in the 20s range who simply bought property in a fringe area in NYC and sat on it for 20-30 years. They don't speak any English and had no formal education. So, his track record has to be valued in that light. Pupil - send me a PM. Let's chat offline. There's no agenda on my part to keep crapping on your ideas. I've seen a crazy cycles in 08 and 09 when SLG traded from over $100 to under $10. I have a tendency to nitpick. It's probably because I am a grumpy old man who has failed to keep up with time. -

Companies -truly long term focused not managing to quarter results?

BG2008 replied to Nell-e's topic in General Discussion

FRP Holdings - Over 20% family ownership LAACZ - 70% family ownership There are very few followers of these two companies. You basically own a bunch of real estate in the private market alongside the family at a big discount to liquidation value. They behave like how a wealthy family would with regard to their real estate portfolio. There aren't a ton of people following them. So there is no management to quarterly results. -

"Measured against interest rates, stocks actually are on the cheap side compared to historic valuations," Buffett told CNBC on Monday. "But the risk always is interest rates go up, and that brings stocks down." Feb. 27, 2017

-

I believe either the XIV or SVXY will go into auto-redemption mode after a 80%+ drop in a day? Does after-market movement count? Can you explain the mechanics a bit more?

-

I forgot to mention that having control is very real unless you know that the CEO and Chairman have aligned interest.

-

I've written a bit about my experience in the last 10-15 years about figuring out "paying up for quality". In short, the NYC and CA assets are higher on the quality spectrum and they rightfully deserve a lower cap rate. Although, I disagree that you should pay 2% for anything. 4% is on the expensive side of reasonable for CA in my humble opinion. Often time when you buy a high yield in the middle of lower, you're paying for the long term lease, you're not paying for the dirt and the replacement value. If the existing tenant leaves upon lease maturity, you oftentimes can't get a similar tenant. This is especially true in a smaller market where your building maybe 5% of the market. I personally think that interest rate risk is very real. Assume you have a REIT that is 50% LTV, due to low interest rates, it trades at a 4% dividend yield. Bc of higher rates, people demand a 5% yield. Two things will happen, first the cost of debt capital will go up when the debt matures. Second, people now demand a higher dividend yield. Third, the bank may want to maintain a 50% LTV but the value of the assets have moved against the REIT. So, the REIT may have to put up more capital. All of these factors makes levered REITs a really good investment when interest rates drop but terrible one when rates increase. I am convince that this applies for companies trading at 20 P/FCF with substantial debt on them as well. Unless you're a REIT that can grow out of these issues, you're going to have some tough going ahead. We own FRPH and we know that FRPH will face some cap rate expansion headwind, but the FFO will be minimally impacted due to higher interest rate cost. We own some LAACOs as well. It is a severely under followed and under discussed name in Southern California and San Diego trading at 7.5-8.0% cap rate plus a free Downtown LA building. The amount of debt is roughly $50mm versus a private market value that is in the 6-700mm range. Just to walk through that 50% LTV REIT excercise (this exercise applies to privately owned assets as well) - F $1.0 bn asset with 50% LTV with 6% cap rate $60mm in NOI less $10mm in G&A equates to $50mm in EBITDA $500mm of debt at 4% equates to $20mm of interest expense This equates to roughly $30mm of FFO and we assume 80% payout which equates to $24mm at 4% dividend yields a market cap of $600mm Now that interest rate is 1% higher Still $50mm of EBITDA because the assets still generate the same cashflow $500mm of debt at 5% equates to $25mm of interest expenese This equates to roughly $25mm of FFO and we still assume 80% payout which equates to $20mm at a 5% dividend yields a market cap of $400mm This is how a 50% LTV REIT can logically lose 33% of its value in a 1% movement in interest rate. This is also the reason why I've avoided RE companies with a lot of leverage. FRPH and LAACO both have leverage below 10% of their private market value. FRPH has non-recourse leverage at one of its multi-family building in DC, but that's a 10 year fixed mortgage. So we view that a little differently. We've held a lot of cash because in a world where 3-4% interest rate is normal and cap rates in the 3-5% is normal for certain type of assets, a 100 bps movement is seismic. This applies to both real estate and anything that trades at 20x FCF or higher.

-

If anyone has resources on specialty chemicals, I would love primers, newsletters, etc. If anyone here works in the field or knows someone who work in the field, I would not mind directly compensating or donating to a charity for your time in helping me understand the barriers to entry, pricing power, and long term trends of this industry. The specialty chemicals involves specialty refined products such as lubricating oil, Waxes, Petrolatum, Solvents, branded synthetic lubricants etc. I also think that this forum we should utilize the industry expertise of this forum more. I'm a real estate guy in case anyone wants to chat about that.

-

I know a lot of people here have looked at retail real estate, i.e. Seritage, Macy's, mall REITs, etc. You absolutely should subscribe to Shopping Center Smart Brief. I don't read it everyday, but it has articles on turn around, deals, developments etc. It's a fantastic resource if you own any these names. Although, I don't own any of these names myself because 1) I once worked on a $400mm sell side deal for three regional malls and they have all turned the keys back to the bank 2) I lost money in Macy's 3) I watched Sears from the sideline and can't believe how much of a time drain and brain damage that would've been had I own it

-

I stand corrected about the yield. I think that the purpose of owning treasuries is that you want to own the treasuries not some ETF that can potentially trade at crazy discount/premium to NAV in a 2008/2009 scenario. The decision is really between holding cash vs holding 2 year treasuries. Thanks for the input everyone and I would encourage anyone who holds a substantial amount of cash to look into owning 2 year treasuries. I think the treasuries will have substantial liquidity and will likely do their job in case we get another 08/09 situation.

-

#1 - yes, but I have only bought long duration zeroes... was easy though. #2 - I think you just buy the cheapest... they are probably are within rounding, so look to the lowest spreads... #3 - What is TPA? bond appreciation/discount is accreted to income on 1099's I believe... so it's all interest. #4 - Correct... #3 - TPA is my third party fund admin. Does IB generate a bond appreciation/discount in the 1099?? I guess you don't have to calculate that manually? #4 - Is the amount of taxes on the interest calculated by your broker via the 1099? How is the interest known?

-

VGSH yields 1.1%, if you buy the 2 year treasury, it yields close to 2%. I'm more confident that I can sell my 2% 2 year treasury in case shit hits the fan than I can sell VGSH at $60 or whatever it trades at. I'm also more confident that the 2 year treasury will trade at close to a 2% yield or even lower in case shit hits the fan. I think that the ETF could trade all over the place.

-

2 Year US Treasuries is now trading at about 2% which I think is quite high and everyone who hold cash should own 2 year treasuries IMO. If the market crashes, and somehow it trades to a 3% yield, you'll likely have a shorter duration at a lower yield. Treasuries are large and liquid so there's no worry really. My question really revolves around the mechanics of owning treasuries. 1) Has anyone bought them from IB? 2) Any thoughts on whether to buy a zero with 2 year maturity with different coupons? 3) Is everything considered interest, price appreciation and coupons? Has your TPA been helpful? 4) I've heard that if you own Zeros, you still have to pay taxes even if you have not received any coupons. Thoughts? I think it's kind of crazy that 10 years are trading at about 2.5% and 2 years are trading at 2.0%. They say that every time the yield curve starts flattening there's a recession that comes after that. https://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=yield

-

This is a hunch. I think that Amazon wind up in the DC Metro area as 3 of the 20 locations are on this final 20 list. It's DC, Montgomery County, MD and Northern VA. If you put these locations on the map, it is clear that they are all adjacent to each other. Bezos also owns the Washington Post. DC is the political center as there are more chatter now that Amazon may face anti-trust or break up risk. Just seem like it makes sense. There are a lot of locations in NV and Montgomery that has vacancy issues because the shift is to DC. Amazon can probably take 5mm sqft of space without any issue.

-

2017 S&P 500 Total Return 21.8% Vs Implied Return from Tax Cut

BG2008 replied to BG2008's topic in General Discussion

No political agenda here. I'm the chump who got left in the dust in 2017 with my large cash holdings. So trying to reason and learn from my mistake that's all. I would say that not all companies deserve to be 21% higher because the ones with no moat don't deserve to trade higher.