dwy000

-

Posts

2,323 -

Joined

-

Last visited

-

Days Won

2

Content Type

Profiles

Forums

Events

Posts posted by dwy000

-

-

2 hours ago, Gregmal said:

In general? Imagine being in Ukraine or America or any country for that matter, and some politician picks a fight or gets involved in a war and now YOU have to pay the price for them? Or go to jail? Fuck that. I mean I’d be cool saying, “if you voted for XYZ and XYZ gets you into a war it’s mandatory you fight”…but don’t make problems I didn’t ask for my problems. Let alone let them dictate my freedoms. And no, I don’t need a politician or media outlet to tell me whether or not my freedom is at risk by the “war”.

You could make the same argument as a young Russian man. At least Ukraine can argue defense of the nation as a rationale. Not sure how a Russian justifies it.

-

Iran stating matter is concluded now. We'll that was quick. Glad it didn't escalate.

-

25 minutes ago, scorpioncapital said:

The FTC is even going after money losing or precarious companies. Look at irobot merger fail. Stock from 50 to 8. Or grail by illumina the company doesn't even have a product yet. Meanwhile some drug companies are allowed. It's scary as it seems almost random?

it wasn't the FTC that killed iRobot it was the European regulators.

-

It used to be more useful when unrealized gains and losses didn't flow thru income statement but got reported on balance sheet at fair market value (so stmt of comprehensive income bridged the gap). Now that the unrealized gains/losses do go thru income statement it really has less value.

If I recall, Buffett had a good discussion of its use years ago but I can't recall if it was one of the Berkshire letters or something else.

-

1 hour ago, Jaygo said:

I own GFL. I bought the ipo and have been moderately impressed with the industry. There is an incredible economy of scale because of landfill locations. Somewhat similar to concrete and asphalt plants.

You basically have an oligopoly in every market. You rarely see all the big players in a single market. It is 2 big boys and some independent feeder fish in major markets so the pricing seems rational.

I owned wcn before and moved my shares into gfl looking for more upside.

I originally bought wcn because of Michael Larson who manages bill gates money. That guy seems to identify industry economic improvements early and has owned republic for a long time.

A new avenue for GFL has been collecting biogas from the landfills and it may well prove to be an excellent bump to revenues from what was a waste byproduct previously.

I don’t expect any grand slams out of it but could definitely see the industry doing better than the market average.

I owned GFL for a while but moved it over to WM. While GFL is ambitious and aggressive I just couldn't get comfortable with a management so intensely focused on the market and their stock price. Not only did they give quarterly projections and annual projections but they'd give 2 year EPS outlooks. And the price increases they would push thru made for some unhappy customers.

The companies I've done best on are the ones that focus on their customers first and let the stock price take care of itself. And I just couldn't see that at GFL. I'm sure it will do great and I will regret that decision but it always made me a bit nervous.

-

I've used buyers agents when changing cities or if we didn't have time to do a proper search. But there is absolutely zero chance they are earning anywhere near the 2-3% that they end up getting. I get it for sellers who can actually put in a lot of work. But even then, in a hot market the agent can earn a massive commission for a listing that might last a week or two.

What I'd really love is a commission schedule that goes up as the price goes up. For a $1m property, a trained chimp could sell it for $750k whereas a really good agent is the one who gets you $1.1m. I'd give 1-1.5% on the easy part and then increasing to pay them like 5% above a certain threshold.

-

There are different kinds of float that would have different values. Insurance companies float is a reserve for "what if" whereas a subscription business needs that float to cover the cogs over the life of the subscription. Then there's subscriptions without a defined product delivery schedule - like Amazon Prime. You can also consider companies like Costco and Dell to have massive float in that they have negative working capital.

Id just value FCF but be very careful because for those with negative working capital or subscriptions, if growth turns flat or negative for a while you could have a really large outflow required (well beyond the revenue decline) and they need to be able to fund it.

-

40 minutes ago, longterminvestor said:

Seems like the voting machine is alive and well while the weighing machine is colleting dust with this name. Just trying to learn and be an active investor doing the work. Writing it out helps me frame in my head and challenges me to find clarity. Anonymously sharing my work is easy however I would let my mouth run with confidence on this name with management if they ever showed up on my doorstep. Just can't get my financial mind around BRP.

Just listened to the call. Boy it's tough to wade through the cash vs adjusted numbers.

FYI, on the broker compensation, a portion of the earnouts from businesses acquired were allocated by the sellers to people who were not "selling shareholders" (sounds like the owners gave a portion of the earnout to the rainmakers who otherwise weren't actually shareholders). As a result, they had to reallocate a portion of the earnout payments into compensation and that drove the number up to the very high levels you pointed out. It's why EBITDA margins were similar despite the higher comp number.

They still have a massive amount of earnout to pay during 1Q. They've sold the wholesale business to help fund it ($34m rev business with $5 EBITDA that they sold for $59m cash)

Free cash flow from operations is forecast at $165-195m for full year 2024. That will all go to earnouts I guess but those should largely be done in 2024.

-

Works great for happy hour.

-

37 minutes ago, Eng12345 said:

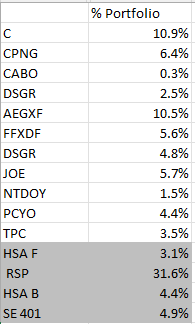

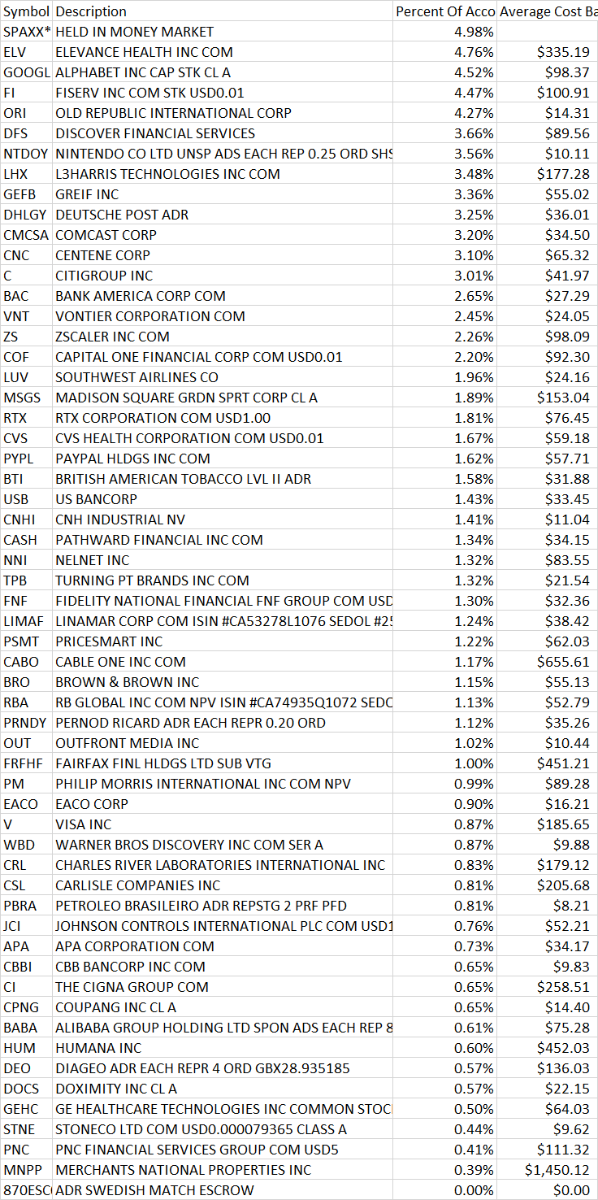

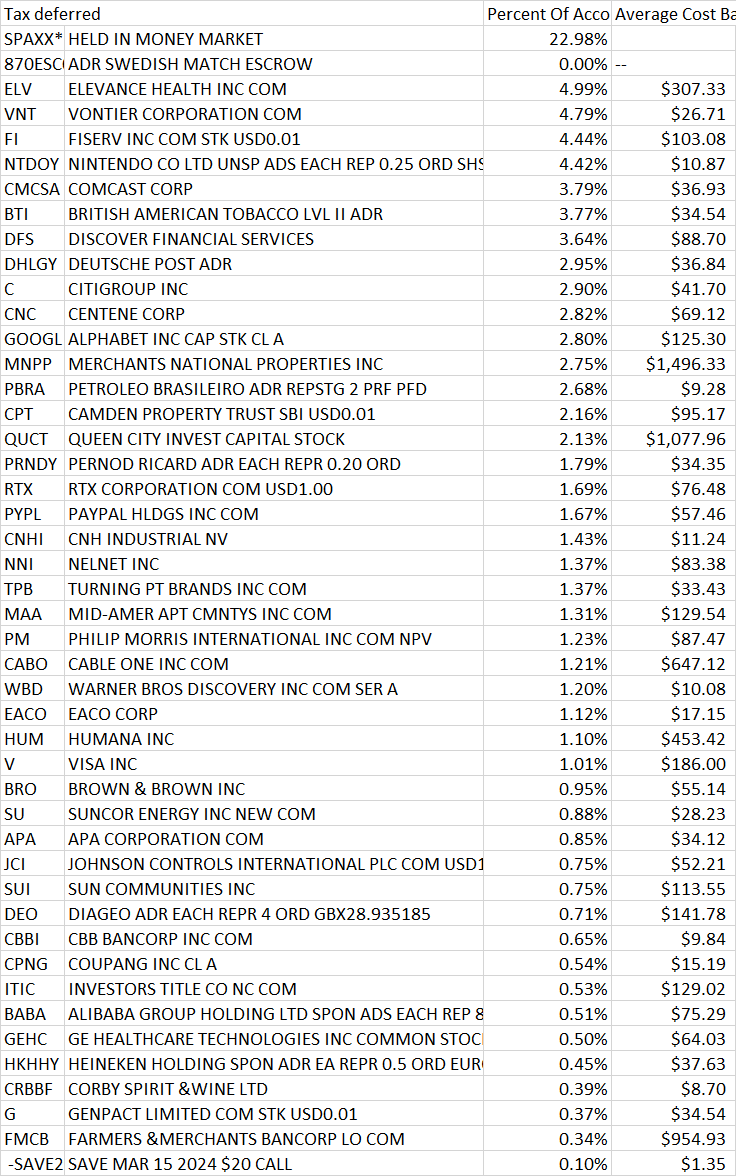

This was a good exercise in forcing myself to build out my spreadsheet...realizing I'm not nearly as concentrated as I like to think I am. The last 4 lines are general index funds or dry powder waiting.

Just FYI, you have DSGR in there twice.

-

Starter position in SBAC

-

5 minutes ago, thepupil said:

as an interesting data point, my parents church had an annual budget shortfall of $100K as donations did not come in as expected.

they dropped their windstorm coverage ($100K of $120K / yr total insurance premium) in order to meet the budget and plan to forego coverage indefinitely.

I'm sure there's a relevant bible verse to share here, but I guess I didn't pay enough attention growing up...

That must be why it's referred to as an Act From God.

-

20 minutes ago, Haryana said:

Comparison value is very logical like we would do with an index. Nothing to do with looking backward or forward.

I am actually boosting Buffett's Berkshire as a benchmark. However, I understand if it appears offensive.

This may be sensitive issue and hurt public sentiments as the masses are programmed with {Buffett == Oracle}.

What is an Oracle anyway? A more technologically advanced translation of the word Prophet?

You may still participate in the chart game by ignoring the red line at bottom and just focus on the blue line above.

Im still confused. What are we trying to accomplish with random comparisons looking backward?

-

4 hours ago, Haryana said:

Not arbitrary, that date is the maximum starting point from when that stock in the original question has data from.

But what's the value of the comparison? Looking backwards for charts that beat Berkshire is pretty easy. Are you saying these stocks will do well going forward? If so why? As Buffett says, the rearview mirror is always clearer than the windscreen.

-

58 minutes ago, CorpRaider said:

Comcast

that's 2 days in a row. You must have quite the position at this point.

-

After 14 years of stop/start/stop/start in the fiber business it looks like Google is throwing in the towel and seeking external funding for Google Fiber.

-

1 hour ago, KJP said:

What is the incremental OpEx/SG&A after a new subscriber connects? Assuming this is just broadband, and not video, it should be very low. So, incremental operating margin, which is probably the best way to assess incremental new build CapEx, is likely much higher than 20%. Also, 60% gross margin on broadband seems low. Tucows claims much higher. See slide 25: https://ir.tucows.com/wp-content/uploads/2023-Q3-TCX-results-investor-deck.pdf Put those two things together and you'll get much higher (claimed) margins. See slide 26.

I do want to note that I've never been able to reconcile that slide (which they've long had in their presentations) with the segment numbers. The CapEx/passing in the segment financials always seems higher than what they put on that slide. [The slide is showing cost per passing, not cost per subscriber, and doesn't include the cost of the drop to the house of a new subscriber.]

I also agree with you that there are other costs besides CapEx that must be incurred to get the system to steady state/50% penetration (marketing, etc.) so the EBITDA losses should be included, not just the CapEx, when looking at returns on capital.

I was just back-of-the-enveloping it so you're probably right on some of these. The 60% gross margin is what they're currently reporting (3Q23) and gibes with the low end of the slide deck (p 26).

Like you, I also struggle to reconcile their numbers. They literally state in their quarterly KPI page (footnote 2) that they have spent $329m in capex and acquisitions (net of writeoffs) to date and yet they only have 114.5k passings. That's $2900 per passing and yet their investor deck says their cost to build is $1650 per address. It's a huge difference. Likewise, where they get $1000 annual gross margin per subscriber is beyond me - especially when the same page says they're charging $89/mo. Even at 75% margin that implies they're charging $111/mo for every single sub which seems ridiculously high, especially if you need to get to 50% uptake.

These business plans always look like they were drawn up by an investment banker trying to sell the deal. The reality never comes close to the plan and the only number that is higher than expected is the spend. But mgmt can't now say they were wrong so they keep expanding and say it's not wrong, just delayed.

-

Other than BOC's numbers the other one you can use to measure is Tucows (Ting Fiber). They're pretty similar in that they go into very small, newer communities (often new builds). The actual returns are still TBD because they generally assume a very strong level of uptake and pricing that takes years to normalize. They often also don't take into account the response from incumbents (if there are any) with promo pricing and retention offers that were never factored into the planning models. I haven't seen any that have hit their projections or have turned cash flow positive to the level where you can judge long term capital returns.

Edit - I took a quick look at Tucows. Thru 3Q they state they have invested $329m of capex in the biz since 2015 (this includes a couple small acqns). For just the past 3 yrs they will have EBITDA losses of another $80m or so. Haven't looked further back. So all in, they're about $425-450m of spend. Right now they have 41k subs. Let's say they can get that up to 60k on the current builds. They seem to charge about $100/mo with 60% gross margins.

$450m of spend for 60k subs is about $7100/subscriber. At 20% op margin that's $240/yr which is a 3.4% ROIC.

-

Does this even work anymore? It seems the value was there because very few were willing to put in the effort to page through S&P manuals or go through the balance sheets of 1000 microchips.

But now that anyone can run a NCAV screener or sign up to a dozen services that filter and recommend this stuff a lot of the juice is gone. Especially when you have to find 25 of them at a time to make it work out on a portfolio basis over the longer term.

-

1 hour ago, Spekulatius said:

Wow, that's a lot of positions!! How do you find time to keep track of 40 positions plus do research for new ones?

-

How do you put a calculated or intrinsic value on it? If you have no basis for why it will go up or down or whether it's overpriced or undervalued, how is it anything other than gambling?

-

18 hours ago, backtothebeach said:

Regarding book keeping: I calculate monthly returns looking at the month-end values of my portfolio. The YTD or annual return is the monthly return compounded.

If I take out money I try to do it at the beginning or end of the month and subtract it from the starting value or add it back to the ending value of that month. It would be the opposite for inflows. Example: Let's say I start with 110k, and take out 10k on one of the first days of the month, I just pretend I started the month with 100k.

Or, with a lot of inflows or outflows you can net them out and adjust the starting and ending balance by half the value.

Nothing too fancy, everything else would be too much work for negligible extra precision.

thanks for all the feedback on this. I do a weekly calculation which for me is a compromise between accuracy and effort. I started monthly originally but I found it to actually be a meaningful difference if you got a really strong market movement that month. In an extreme month (like a March 2020 say) the difference between using the start of the month value vs. end of the month value when adding/subtracting to the portfolio can move the needle quite a bit. But it's a lot of work to do more and it doesn't really matter much at the end of the day.

-

There's a decent discussion about the company, the product and the stock itself in the Investment Ideas section.

-

21 hours ago, KPO said:

It looks like Lowe’s buyback is mostly debt financed as their debt has more than doubled to -$36B in the last four years. That said, the other Loews decreased their share count by about a third and paid down a third of their debt over the same period.

Oracle is similar. From 2011 to 2022 they retired almost half their shares (5.15b shares OS down to 2.7b shares). Over the same period LTD went from $13.5bn to $86.4bn (although that includes buying Cerner for $30bn and NetSuite for $9bn).

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

in General Discussion

Posted

BRP going off this morning. Not entirely sure why - the results were good but not that good. The overhang of debt ($1.3bn) and contingent payouts ($225m - all current) are going to be a drag for a while. They were able to fund it all by selling a business for $56m during the quarter.