anders

-

Posts

108 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by anders

-

racemize..I do care about my mistakes, thx for telling me.. peter.. you are right, I should have been more informative of the purpose.. The write up was quite quickly done and basically ment to illustrate the business from a helicopter view perspective.. the first stage in the process if you like; to get an idea about the business and to bring up potential risk vs. the upside to the surface.. Next stage would be deeper and include segment analysis, isolating advantages, info from competitors, catalyst etc.. I know a lot of the boardmembers have BAC in the portfolio. Would be interesting to find out how much of your time you spend on each case before buying it..?? Apart from the write up, I have red the quarterly reports, went deeper into the business structure, thought I had a sense of where the business is going and bought a part of it.. But would this be enough to justify my purchase?? Am I really speculating in belief that I am investing..?? ??? I am quite worried about Grahams warning, and looking back, when I started, I was just lucky, riding the bull wave in equities.. I understand the exponential learning curve, reading reports on same company for years and suddenly the correct price appears.. but Im still in the beginning of that curve (couple of years on it) so am a little bit afraid of having a high opportunity cost.. Rgds

-

.. don't hesitate to let me know what you think of it, good and bad criticism is equally welcome.. BANK_OF_AMERICA.docx

-

"Voluntary" what does it mean... and CDS contracts doesn't get written down since it would be voluntary.. but if a creditor is using CDS to hedge and decides not to participate, then he would still hold his original debt claim and CDS hedge..? Banks must now set aside 9% of funds -- or put in another way, raise 106 Billion euros in coming 8 months.. how are they going to be able to achieve that without going to the equity market..? The Governments, but where are those money going to come from since ECB wont print money..? How long before other troubled nations start to ask for cuts..Why should the top-performers in Ireland pay dearly while demonstrators in Greece get the easy way out..? Furthermore, they don't actually put in money into the pot but instead lever the EFSF 4x-5x.. If Europe doesn't get actual economic growth, this solution is just a massive SIV with levered risk.. I don't get it.. ???

-

Everything I See Says "No Double-Dip" In Near Future

anders replied to Parsad's topic in General Discussion

So, what really is a recession..? ??? I know about the theory and NBER data, but I believe the one that makes most sense to me is the one the Buffett once stated in an interview.. (cant remember which one).. He said in some sort that as long as the people are poorer today than yesterday -- we still are in a recession.. ---- In a CNBC interview 30/9-11, andrew asks WB if the US is going into another recession and Buffett's reply: Oh, we're not. We're not going— I think it's very, very unlikely we'll go back into a recession. We're coming out of a recession and what we've been doing it since 2009, and a great majority of our businesses are going to be earning more money than they did last year and the year before. ---- Below represents Real GDP per Capita in the United States: 2007-01-01 48532 2008-01-01 47923 2009-01-01 45854 2010-01-01 46844 2011-E 48067 So, in my opinion, USA will not be going back into a recession simply because we are still coming out of it.. ::) Thoughts? -

Will The Real Value Investor Please Stand Up

anders replied to moore_capital54's topic in General Discussion

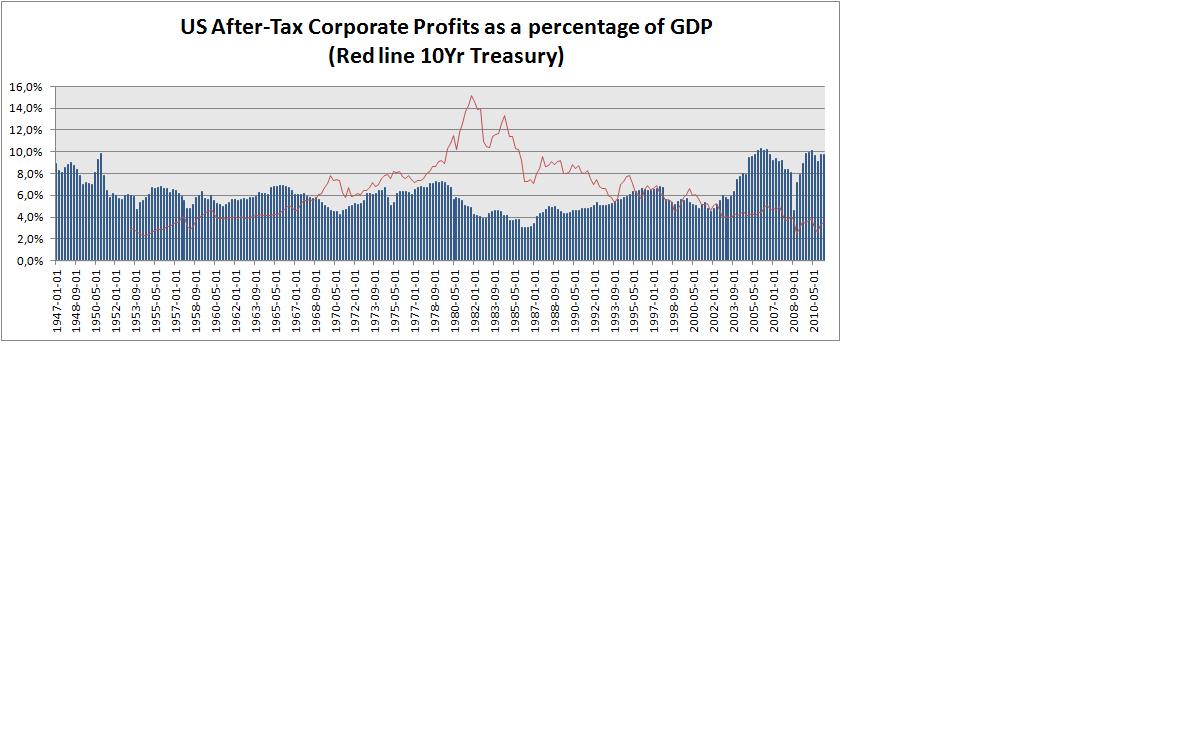

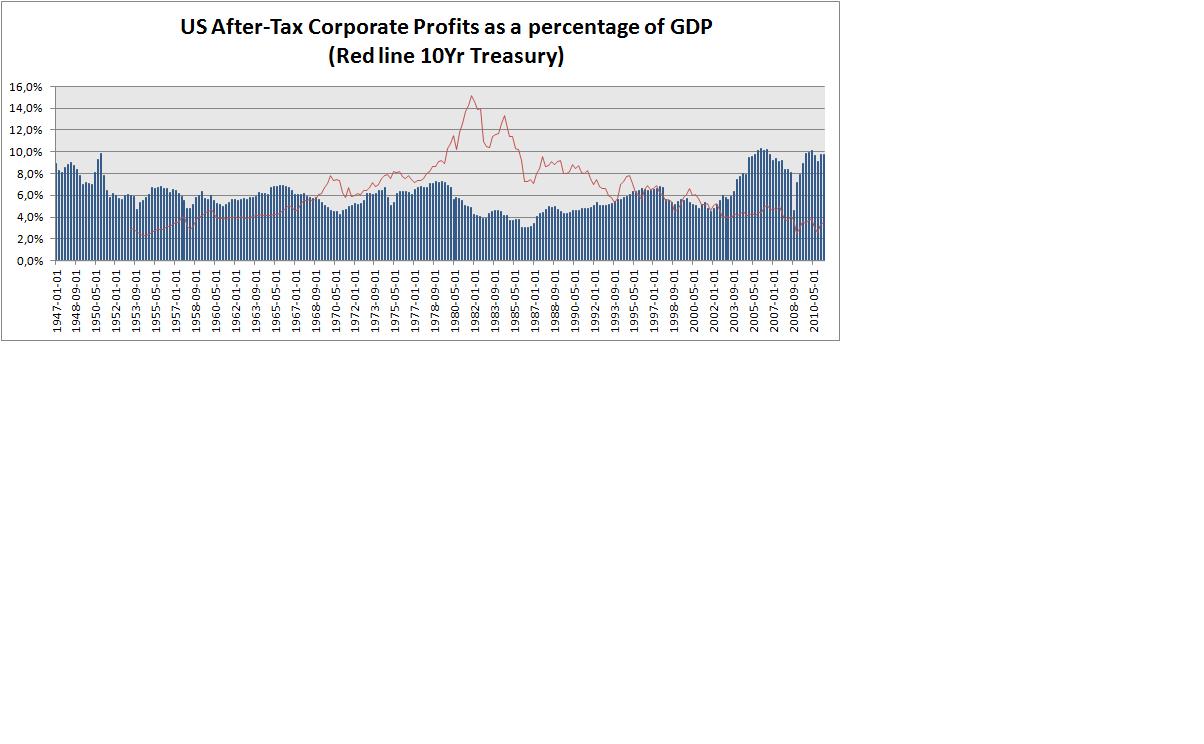

So yes, what is the cost of capital..? I have never quite been able to understand the concept.. and never meet anyone that could explain the term without mention some cost of equity based formula, wacc, etc.. To quote Charlie Munger "it's only fair, if you are going to use the cost of capital, to say what it is".. Another quote at BRK annual meeting "Charlie and I have not the faintest idea what our cost of capital is and we think the whole concept is fairly crazy, frankly, but it's something you learn in business school and you have to be able to answer it, or you don't get out of business school... But I've never seen a cost of capital that makes sense to me" - Warren Buffett ;) About the Margins, Ive attached a small graph i made.. As per 2011-04-01 the after tax profit/gdp was 9.8% compared with historical average since 1947 at 6.1%. If you go further back to 1929 to date, they typically range between 4-6%.. I don't know when the margins will start regress to the mean.. but one thing to remember is that we are talking about AFTER TAX here and there is still no political action like a move to raise corporate taxes.. which evidently starts to become an reality with people demonstrating in the street.. With a current portion of 10% of US GDP going to shareholders, the labor component share of GDP has fallen, and I am not sure how long this could progress in this economic environment we are having without becoming a political issue, it wouldn't surprise me if it comes up during the next election.. not to forget, the US budget deficit is around 10.8% of GDP..! Corporate taxes used to be over 50%, now a lot of companies are paying in the low 30s.. Another part of the equation is the delevering process. If you look at some companies i.e. apple, the profit is estimated to rise in a higher rate than sales which indicates a margin increase! ??? The consuming makes up around 70% of US GDP, how can margins stay at levels when that 70% starts saving more..? This cannot last, the profits wont't stay at 10% much longer.. I dont think market is cheap.. I would say its currently fairly-to modestly overvalued with quite a big risk in contraction of margins.. and if that happens then the multiples would still be over 20x and if history rhymes they could very well come down under 10x.. that is an additional -50% downturn from here.. Im not saying this is going to happen, but this is perhaps why PremW choose to hedge up 90% of the portfolio until the picture clarifies..? People delevering their personal balance sheet, potential rise in corporate taxes, overall corporate financial leverage coming down, potential higher inflation,.. it doesn't look good for the ROE in the Corporate America.. Any thoughts.? with regards to Richard Feynman's first principle "that you must not fool yourself, and you are the easiest person to fool" - I would love if someone could break down all my arguments ::) Rgds,

-

Gold Price is Now Higher Than Inflation Adjusted 1980 Price

anders replied to Parsad's topic in General Discussion

@ eric50 My way of looking at the miners is to calculate TOTAL cash cost.. I think you get a much better insight of the valuation.. @ ericopoly Well.. yes.. same with all businesses, a t-shirt should be priced higher than same amount cotton in the field.. but I don't think you can find out an answer on how much an irrational market should discount a product.. only your own preference for the rate of interest that makes you indifferent between present and future dollars would give the answer.. Rgds, -

Gold Price is Now Higher Than Inflation Adjusted 1980 Price

anders replied to Parsad's topic in General Discussion

I agree, the spread is crazy.. I bought the miners last year to get exposure and to have something to calculate.. Can't do it with pure gold.. However, recently switched my gold positions to financials instead since the risk/reward is better here.. And the gold has started to go into the parabolic phase, which makes it more difficult.. However, I am a believer in gold and will probably buy some back when the hick-up arrives, I think it will go pass 2000 next year, and continue to up to maybe 5000 by the end of the bear market 2014.. And silver.. I believe will go pass the $100 mark.. Watched a clip on j.rogers.. apparently, all the managers he spoke with, about 90% of them never purchased gold.. he said that when the opposite occurs, that is the time to become bearish.. For those who don't understand why gold will continue to rise in price as long as the Fed continues to debase the currency, should read what Bernanke wrote himself 2002.. (the reason why he is called helicopter ben).. http://www.federalreserve.gov/boarddocs/speeches/2002/20021121/default.htm Further, Ben's special field while studying was the great depression.. He wont let the country slip into deflation, meaning continuously adding credit to the financial system thereby increasing the monetary base... I'm simplifying of course but all comes down to increasing consumption to increase growth.. that's the US model.. And what happens when you increase consumption.. ::) As a sidenote, I saw a clip about Friedman there he states that Keynes warned about exaggerating his principles.. which is happening now, so there is a probability of high inflation when the pendulum start to move towards growth and lower unemployment.. I agree of what buffett is saying about gold, I also rather own the farmland and exxon mobiles.. and c.munger when he says that for gold to rise even more, then the world need to become more afraid next year.. and that is pretty hard to predict.. But as long as USA choose to debase their currency, one should have a gold-bullet in the portfolio.. :) Rgds, -

@ Harry, You seem to be a smart guy and Im sure you will find prosperity and success in your life.. There is one thing though that many quants in finance tend to forget.. or choose to ignore.. Quantum Finance is not the same as Quantum Physics -- very important point. If you work within the field of physics and one morning you come up with a theory, there might be a chance in hell that you are actually correct. This since physics is governed by laws and math. In quantum finance, these laws cannot become true since human behavior is part of the equation, and you will never be able to calculate the natural instincts of human beings.. An example, if you go in to a store and buy a bottle of coca cola, it will cost you a dollar. If a computer do the same it will cost a dollar. However, if you come into the store to buy 100 bottles, you might want to discuss a discount and pay 99 or 95 dollars. But your computer will be programmed to purchase it for 100. This since programmed mathematical equations are linear -- and the world of business is not.. But hey, "techniques shrouded in mystery clearly have value to the purveyor of investment advice. After all, what witch doctor has ever achieved fame and fortune by simply advising 'Take two aspirins'?" -- I took that one from Warren Buffett ;) My two cents,

-

So, during 02-08 period they paid out a total of approx $10.36 to shareholders... and now they need to pay approx $7 the coming 7 years to justify current level of price of the warrants.. ??? oh, I don't know...the seven good and the seven lean years comes into mind..

-

Many thanks :) So the question comes down to the dividend planning.. more than $7 from jan 2012 - jan 2019.. = undervalued.. less = overvalued.. give or take.. I know Im being lazy here but does anyone know the average payout ratio for BAC ?

-

I know many of you bought BAC warrants.. Im thinking of switching my common to the warrants but get confused on current market pricing.. Based on B&S formula, I get that the warrants should trade in the range of $2.15-$2.35..? instead of the current $4 ??? Warren buffett got 700m with strike just above $7.14.. the value on 25th aug were approx $5.49 per warrant.. B&S formula indicate a fair value more like $4.5 for his warrants.. Are BAC warrants mispriced in the market? do they trade with a premium? What am I missing? Grateful for an answer,

-

Many thanks, I also believe one should pay attention to what corporate leaders say to get clarity.. (the good persons that is ;)) Another example is Wall-Mart CEO Bill Simon about inflation -- "We're seeing cost increases starting to come through at a pretty rapid rate.".. http://www.usatoday.com/money/industries/retail/2011-03-30-wal-mart-ceo-expects-inflation_N.htm

-

I like to invest from a 'businessman perspective'... I think the quote below explains my point: WEB -- "There is no distinction in our minds between growth and value. Every stock is a value stock to us. The potential growth of the company is simply one factor that we consider." Munger chimed in: "All intelligent investing is value investing." Rgds,

-

Buffett said BAC deal is reminiscent of his youth. GEICO & AmEx

anders replied to claphands22's topic in Berkshire Hathaway

Quick also pointed out that "he thinks Wells and Bank of America have two best deposit franchises in the United States".. ::) -

Basel III requires 8% Minimum Total Capital plus conservation buffer 2013.. Then 10.5% as of 1 january 2019

-

Thanks for a great discussion, munger, moore, parsad and others.. Im learning a tonne! :) My reasoning on BAC, As far as I know, WEB first step in his investing process is -- what is the odds that this business is subject to any catastrophy risk..? If there is any such risk, he simply says no. (WEB rule nr 1 -- dont loose money, rule nr 2 -- dont forget rule nr 1). Brk lending 5B to BAC means exposure and, it is therefore logical to assume no catastrophy risk involved in the investment. Sure the preferred is superior than common, but its very junior and according to my knowledge, none of the preferred shareholders got any back from financial bankrupties such as Northern Rock, Bear Sterns, Lehman. I have 60k common BAC shares @ little under 9. I dont know what the price will be tomorrow, next week or next year. All I know is that the market has gone up over time and, will probably continue doing so in the future. (extrapolate curve on DJIA and we are at 2m in 2100 ::)) I believe that the economy in USA will recover at some point and BAC should benefit from that growth. Quite simply, Im trying to buy a systemically integrated part of USA when others are fearful.. "and if a business does well, the stock eventually follows"..

-

Thank you for sharing parsad :D

-

Agree, Have no cash left though.. bought a lot of bac and c.. Honestly, Im fearful now, forced myself to buy.. Im reminded of 2008, I got in after half the yearly downturn and came out bleeding.. :-\

-

I dont think it is that easy.. I look for companies with a competitive advantage and believe that the durability of that advantage derives from the strength & growth of the moat... the building blocks of the moat/competitive advantage being porters five forces.. I believe that it wasnt until 'buying wonderful businesses at a fair price' that buffett increased his focus on the moat.. so for smaller companies it is much more difficult to find wonderful businesses with a moat since they really havent yet developed into one... One reason I believe buffett not invests in tech is because he can not determine the future of the moat.. e.i. low entry barrier into high-tech since thousands of students trying to make services better, faster and cheaper.. coca cola is so much easier, "give me 100B and tell me to compete against coke and I say it can not be done" - WB.. All porters forces in coke are so extremely high that no company would make the effort to compete (except giants like pepsi).. its throwing money away.. virgin coke anyone? Charlie munger stated that google has the biggest moat he has ever seen.. b/c of mindshare which I believe is final destination for building a moat.. but mindshare still depends on the durability of the competitive advantages.. how did apple grow and fall then rise again..? The business must start out with certain characteristics that enables it to build strong barriers before competitors enters the arena.. I believe you can find these characteristics in all levels of market cap and in all levels of industry.. I recommend reading books about entrepreneurs.. e.i. Sam Walton.. He opened his first store in newport, arkansas.. I you can understand how he created the company coupled with the situation and place at that time, I believe you are on the right track for understanding how great moats are created.. how wonderful businesses are created.. Regards,

-

# Link01 # RRJ Thanks for great feedback and response. From a helicopter view perspective, according to PRC budget plan, china's total production and sales of new energy vehicles will reach 500 million in 2020 with hybrid vehicle annual sales of more than 50%. 2011-2020 the PRC will grant subsidies to individuals purchasing new energy vehicles of RMB 3000 per kWh for new energy vehicles; the maximum amount for plug-in hybrid automobiles will be RMB 50,000 per unit and RMB 60,000 per unit for pure electric vehicles (BYD E6). Corporate sales of new energy vehicles and key parts of the VAT rate was adjusted to 13%. R&D within this field will be 100% deductible. Moreover, PRC plans to implement mandatory new energy vehicle purchases in all levels of government and public bodies (BYD K9 electric Bus). Talk about tailwind :D Buying into the company today gives approximately the same multiple levels of MidAmerican's rights issue purchase in September 2008. Regardless of speculation or investment, I believe this one is a keeper and would gladly see the price drop further and, if Munger's consideration of W.Chuan-Fu to be a mixture of T.Edison and J.Welch holds true -- then this story will surely be one of the great ones.

-

Another thing...Why is BYD referred to as a speculation ?? :-\ The company does provide cash flow.. it shouldn't be categorized under the greater fool theory..

-

BYD @28.6 is in HKD so converted the price to RMB to meet the figures in their report.. and, it's for 2011.. the multiples are for 2011, based on revenues of approx 52B RMB with profit margin 8%.. (which might be optimistic).. ::) When I speak about the business itself I mean what multiples you are paying for the operating business, excluding the balance sheet.. Take Bunge, you buy the company @ capital funds.. (equity excluding intangibles) so essentially, you get the operating business for free.. if you were a buyout company you would look at enterprise value..

-

Well.. yes.. but, total revenue increased 18% yoy.. I wrote 'the biggest cause' ..Sure they did not deliver the forecast which is always painful for the stock.. In my mind, you need to create revenue before the costs and, by selling first and buying after the company can let revenues control the cost level that is acceptable for the company.. So raising the sales target to maybe 700'000 vehicles doesn't necessarily mean that Wang Chuan-Fu thought: "well we have a target on 700'000 and therefore we will increase the cost with 77% to meet that target".. but rather longterm we need to expand the business and therefore we need to increase our sales and distribution channels. Sure the gross margin was hurt by the forecast but the profit margin decline I believe was due to other factors. :)

-

-

# treasurehunt, Thank you for your insight, I believe you are right with auto sales, I am optimistic about BYD to reach 600t vehicles, but not unrealistic... but lets not forget that 'handheld components' stands for 44% of revenue and increasing, so even if not meeting target in auto segment, they should come out ok on top line. About margins.. I believe you have a point that the price cuts will hurt the margin, but less then many anticipate. The larger cuts are for G3 and F6 model which might very well increase in sales in same proportion, but who knows? But one thing is clear, the biggest cause of the drop in margin 2010 was not drop in sales but due to increased effort in sales channels and distribution -- a 77% cost increase. I don't believe BYD will repeat that increase.