redskin

-

Posts

226 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Posts posted by redskin

-

-

7 hours ago, Xerxes said:

showing off from my new book.

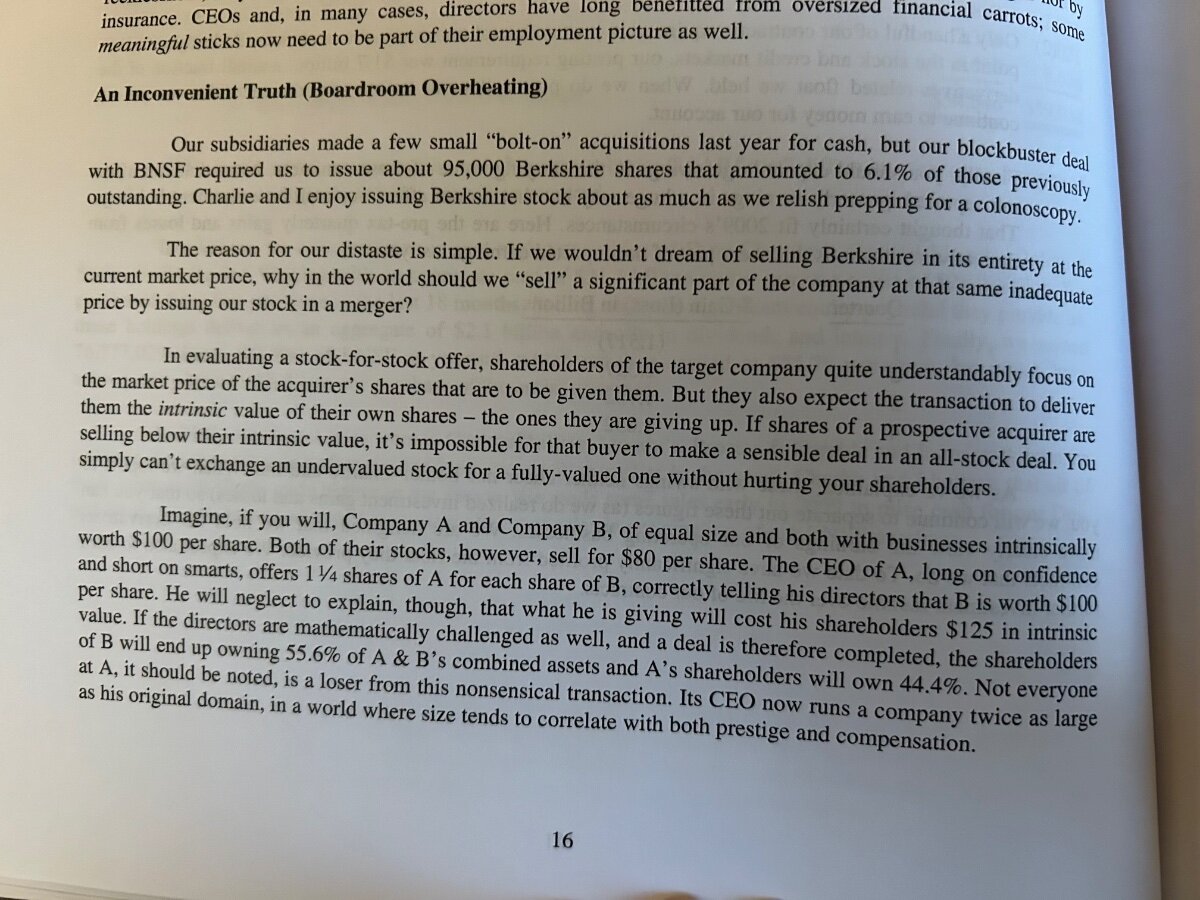

Excerpt from 2009, 2010 and 2011 letters on BNSF.

$22B in cash + 6% of the company

Excluding the stake they already had.

Did Berkshire gave away too much by issuing away 6% of Berkshire. That is $54 billion on a market cap of $900 billion todays price.

So it looks like it was worth giving up the 6%

-

On 2/25/2024 at 10:38 PM, gfp said:

He has received his entire cost basis back in dividends and retains an extremely profitable, durable enterprise that has comparable valuations (UNP = $155 Billion, replacement cost ~$500 Billion ??) that are favorable and the "capital eating enterprise" continues to pay out several billions of cash every year in tax free dividends to the owner. I think it was a once in a lifetime opportunity to buy an irreplaceable productive asset that is almost impossible to buy out of the public markets. He was pretty psyched.

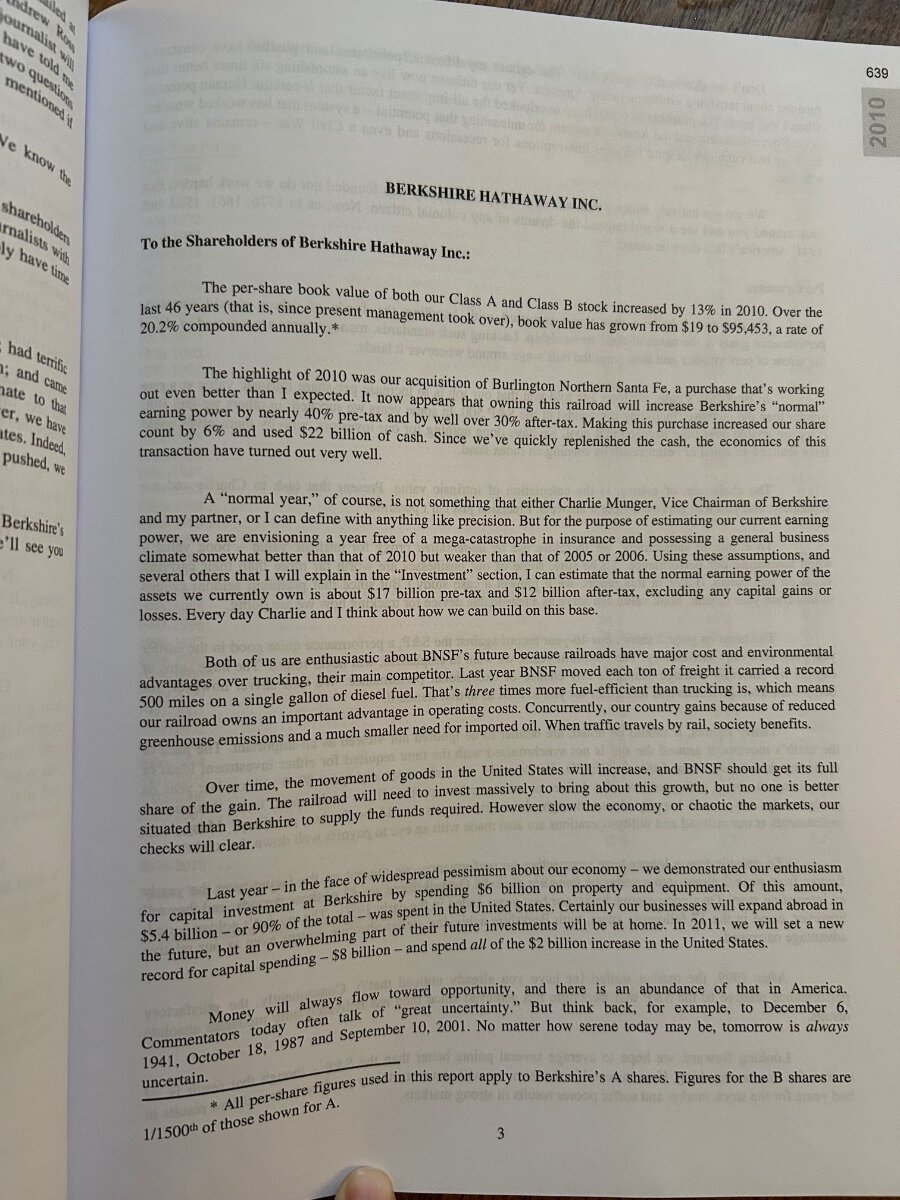

Berkshire has received $53.68 billion in dividends from BNSF since its purchase in 2009. Did he pay $34B for it?

-

On 10/11/2023 at 12:08 AM, schin said:

Articles about his HF performance

https://www.ctinsider.com/business/article/Who-is-this-Todd-Combs-anyway-747167.php

I remember Warren Buffett saying that both Ted and Todd have been underperforming the S&P in their portfolio over the past few years.

If you listen to the video, Todd has strong opinions about GEICO and Progressive. Essentially, they will be investing more in technologies as their IT is antiquated. I have friends that work there and it's definitely outdated. We'll see if he can add value to GEICO. He was hired for his investment prowess -- less see if he can reinvigorate GEICO on the operational side.

The Forbes article gives his performance from 2006 through 2009. He was up 35% over that period. The S&P 500 total return over the same period was -2.6%. I don't understand how they could be critical?

-

On 3/25/2023 at 2:35 PM, John Hjorth said:

With all respect and politiliness, we don't need - blank - links to substack items here on CoBF. What we may demand is your personal comments to such, expressing your opinion at the matters at hand.

Otherwise, we all drown in posts here on CoBF about etc. how many shares has Mr. Abel acquired this week et. al.- or what do I know.

In short, please put our own personal angles to your postings to spice things up, and those will be met by a lot constructive interaction.

I appreciated the link. There were some articles or information I didn't see. I liked the summary.

-

6 hours ago, yesman182 said:

I agree.

I have a dumb questions to play devils advocate. I understand Ally is a bank, but is it a bank because it keeps deposits or because it issues loans. Could Berkshire buy Ally and then sell the online bank and CC business and brokerage business, while retaining the insurance and loan book and the ability to generate more loans using Berkshires Capital? What would another bank pay for $150 Billion in 90% insured deposits at a time like this?

I know nothing about Ally, but you mention $150 billion in deposits. I assume those deposits are funding their loans. Berkshire would need to fund the loans if they sell the deposits. If you assume a bank can earn 1% ROA, they could make $1.5 billion on those deposits. Maybe a 10 multiple ($15B)? I would assume a lower multiple as you don't know if you will retain all of the deposits.

-

1 hour ago, cubsfan said:

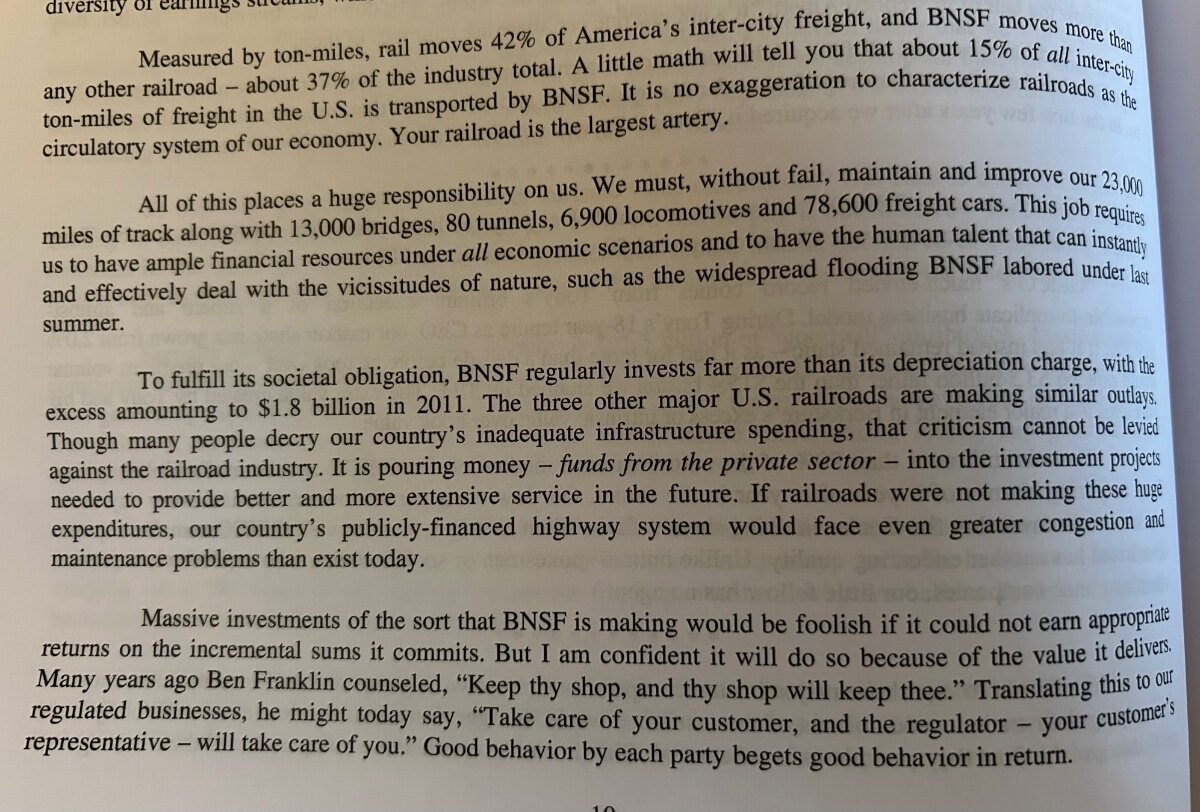

GFP - If I remember correctly, early on, BNSF went into large capital expense mode for rail maintenance, tunnel expansion, etc - before and right after the Berkshire acquisition. Do you see this subsiding, and is that the reason for the large cash distributions? Just trying to understand whether the other railroads have really been cutting corners and paying for it now - ie., Norfolk..

BNSF has distributed $50.58 billion to Berkshire since it was purchased in 2009.

-

On 7/8/2022 at 7:11 PM, Blugolds11 said:

Buffett knew the moat and knew the business very well. I dont know where you got the above quote comping it to HD...but at one time remember HD bikes were selling for over MSRP before owners even took delivery, they were selling their spot in line for profit. So everything has its heyday.

Since the quote calls the company something that appeals to "boomers" did the author go on to recommend AMC, GME or BTC holdings to a solid reliable and predictable investment that has been around for 100 years.

Regardless, See's has been a solid investment for BRK, the investment has already paid off and IMO anything now is icing on the cake.

https://news.yahoo.com/sees-candies-record-quarter-170456133.html

He recognized that See’s had 3 distinct advantages:

- It possessed a strong built-in customer loyalty moat

- Its product was so good that customers would tolerate price hikes

- It required very little operating capital

In 1982, Buffett was offered $125m for See’s — 5x the $25m he’d paid for it just 10 years earlier, or a 20% compound annual growth rate. He passed, opting to let the company slowly chug along.

Buffett’s rejection of the $125m offer would turn out to be a smart move.

Since 1972, the company has given Berkshire Hathaway well over $2B in income. That’s a return of more than 8k%, or 160%+ per year.

Over the same time period, the small operation required only $32m in capital to run. “Modest physical growth,” wrote Buffett in 2007, had led to “immodest financial growth.”

See’s provided Berkshire Hathaway with a reliable stream of capital that it used to buy into other attractive businesses.

In the late 1980s, he used See’s profits to buy Coca-Cola shares, which are now collectively worth more than $25B.

Today, See’s Candies sell for $22.50 per pound — about double the 1972 price, after adjusting for inflation — but its customers have remained loyal."

As to if the company was publicly traded would anybody own it...that all depends on the price you give for the value you get...just like anything else and at .1% of BRK holdings there are better things to spend time contemplating with regard to BRK IMO.

Well said...

-

6 hours ago, Spekulatius said:

Earnings were a bit ho-hum. As @gfp predicted, Geico‘s underwriting didn’t look great and neither did the rest of the insurance. Of course insurance underwriting always is lumpy. Actually, the biggest (but also immaterial ) surprise was that McLane had a small loss. I thought this business should have rebounded, but I guess they could not pass on the cost increases.

Thats purchase from Walmart many years ago did not work out well overall, I think.

What was the price they paid for McClane?

-

On 6/15/2021 at 9:04 AM, thepupil said:

I pulled Berkshire's annual for year ended 1998, when 10 yr treasuries yielded 6% and were very much positive / real. Berkshire was running very low duration back then too. Buffett has always had the 70's seared in his mind and seems to have been on the wrong side of the long duration trade for decades. I am not saying he is wrong. I think the cash / very ST FI makes sense in the context of the rest of his portfolio. But I don't think Berkshire is positioned any differently today than 5,10,20+ years ago.

So I think his strategy is consistent. Run an overcapitalized insurance company. Don't take (much, if any) duration/credit risk. Own equities. I don't think it has to do with the current inflationary trends of 2021.

-

I'm having a tough time finding anything cheaper and safer than WFC..

-

He bought about 15% of the average daily volume.

-

There is some evidence that there might have been a decent amount of buybacks in Q2 - https://finance.yahoo.com/news/buffetts-berkshire-hathaway-reduces-share-160700854.html . 19,000 A shares is a decent buyback and above my diminished expectations after the AGM but I would have really liked 20-30 billion dollars of them at these really low prices.

I'm calculating BRK repurchased 23,744.4 class A shares equivalent as follows:

- On Feb 13, 2020, BRK had 700,395 Class A and 1,385,994,959 Class B shares outstanding, adding up to a total of 1,624,393 Class A equivalent shares. See https://www.berkshirehathaway.com/2019ar/2019ar.pdf.

- On July 7, 2020, Buffett owned 248,734 Class A and 10,188 Class B shares, adding up to a total of 248,740.792 Class A equivalent shares. His total economic share in BRK was 15.54%. This puts total Class A equivalent shares of BRK to be 248,740.792/0.1554 = 1,600,648.597. See https://www.sec.gov/Archives/edgar/data/315090/000119312520189490/d936378dsc13da.htm

- 1,624,393 - 1,600,648.597 = 23,744.4 class A equivalent shares repurchased

There were 1,620,023 class A equivalent according to the 1st quarter 10-Q. About 19,300 this quarter.

- On Feb 13, 2020, BRK had 700,395 Class A and 1,385,994,959 Class B shares outstanding, adding up to a total of 1,624,393 Class A equivalent shares. See https://www.berkshirehathaway.com/2019ar/2019ar.pdf.

-

He sold $6 billion of equities in April.

-

I emailed Carol Loomis asking if Warren would be taking questions from shareholders. She responded with the following...

Yes, he is--though the number of questions probably will be shorter than in previous years.

-

Has anyone heard what the format will be for the annual meeting? Will Warren be fielding questions from the journalists or analysts?

-

The new control regulations are delayed for 6 months. I was thinking we'd start to see BRK increase its bank holdings after this was implemented.

-

He's talked in past meetings about the potential for very large investments in the utility. He reiterated in the letter that they could take on projects requiring investments for as much as $100b. In 2019, they invested $4.5b in excess of depreciation charges in the utility.

-

-

Has anyone heard any updates on this proposal?

Personally, I'll second redskin's question whole-hearted. I can't remember the sources any longer, and I've got no time to dig them up [perhaps it was actually posted by a fellow CoBF on here], but if I remember correctly, Berkshire has asked for permission not to reduce its position in BAC below 10 percent, while it continues to reduce its position in WFC.

Please correct me if I'm wrong, and if I'm not wrong [i may be], what do you get out that? I mean, perhaps, with regard to the forced WFC selling at Berkshire, it may be considered at Berkshire's convenience in the situation. [No kick-a** one-liners from Mr. Buffett nor Mr. Munger for years about WFC being a "good bank" - perhaps for a reason.]

Looks like they finalized the rule change. It is effective April 30th.

https://www.federalreserve.gov/newsevents/pressreleases/bcreg20200130a.htm

-

Has anyone heard any updates on this proposal?

-

Nice update on your line of thinking, which has been consistent.

Accepting the possibility that you may be right to "outsource", to some degree, the timing of investments (which really is not timing but sticking to internal yardsticks by Mr. Buffett {and IMO not thumb-sucking as implied by the Wedgewood move}), a potential weakness of the model may be that the IV floor that you describe may move down, as perceived by the markets, when fat pitches come along, given how progressively correlated BRK has become in downturns (typical time to use the elephant gun) and given BRK's relatively high exposure to financials.

As John Hjorth alludes to above, BRK is built to last but a question remains: is the relative advantage for BRK in downturns and the ensuing recoveries sufficient, on a relative basis?

If the buybacks become truly significant, the IV/BV ratio would narrow somewhat, but otherwise (as is likely to persist for some years) I'd imagine that there are still quite a lot of people willing to pay 120% of BV, and probably also 125% of BV in normal circumstances, which acts as something of a backstop.

They might adjust last-reported BV down a little in the event of a market crash.

Certainly, if markets plummet, Berkshire is likely to fall too, by a somewhat similar amount, such that the perceived risk-adjusted returns are commensurate for all stocks.

However, 'somewhat similar' may still be less than the general market, which could be pegged to a few reasons:

1. If it was trading at the bottom of its range before the crash (e.g. P/BV < 1.30) as it is now, it likely to fall a little less .

2. It is seen as more defensive (i.e. lower risk, meaning lower business risk as well as lower 'beta' for those who subscribe to EMH or CAPM), hence on a risk-adjusted basis it ought to fall a little less. Some of the optionality of Berkshire's assumed ability to invest its excess cash profitably when markets are down is then priced in when markets fall markedly, reducing how much it falls compared to the wider market.

3. The stock portfolio of Berkshire might well fall less than the market because it's also relatively defensive. And even if the Berkshire portfolio experiences a 20% pre-tax decline, this $42 billion reduction in market value is only about 10.6% of Berkshire's Book Value, and after applying 21% deferred tax reduction to the unrealized capital loss, BV would only reduce by 8.4%. This would be partially offset by operating earnings too.

I would expect most things to decline in market panics, Berkshire included, and for Berkshire to gain IV and increase leverage by spending that float-funded cash hoard at such times if it can deploy capital, even if it that value might be hidden for a few years. I would not expect Berkshire to fall more than the general market, but not an awful lot less than it either (unless it was highly priced going prior to the crash, of course)

I don't try to side-step market crashes, aiming to remain fully invested as I would expect the compounding I'd miss out on by predicting the crash too often and too early to exceed the losses I'd avoid by going to cash.

If purchases are made above book value and below intrinsic value, the gap between book and intrinsic value will actually widen.

-

Berkshire Hathaway Energy is the only subsidiary I know of where you can see the valuation that Buffett places on it. Since Walter Scott is a minority shareholder and he periodically sells his shares to Berkshire Hathaway Energy, those transactions are reported in the Berkshire Hathaway Energy filings. Scott's last reported sale was in Q1 2019. He sold 447,712 shares for $293mm ($654 per share). This transaction values BHE at approximately $50 billion.

Transactions in previous years suggest the following per share values....

2018 $602

2017 $542

2015 $480

2013 $350

2010 $225

2009 $210

He purchased MidAmerican for $35/share in 1999. This equates to an annual rate of return of close to 16%.

-

I think some British papers are massaging the headline to cater to a local audience. Buffett gave his standard response "we will be happy to buy outside the US" and obviously being the FT, the questioner made it more specific and he obviously obliged.

In the past one of the issues Buffett has pointed out in the UK is that the reporting threshold for ownership positions here is 3% and he has said in the past this is a issue since they like to take large positions and this would alert others prematurely but he considers this a jurisdiction he understands well.

On another note, I don't see Rolls Royce as a viable candidate. Currently it is a well known brand but not a great business with zero growth, loads of debt, highly variable earnings and high capital intensity.

it has a 3 part business strategy that includes the phrase "transform the business". If that does not keep Buffett away I'm not sure what will. It may be a good cigarbutt candidate though but Buffett doesn't do that anymore.

I think Buffett would be more interested in buying a private European business or a public European company in whole which would avoid the % restrictions.

-

Berkshire's cost basis in 'Banks, Insurance, Financials' increased by $15 billion in Q3. $5-6 billion can be attributed to the increased stake in BAC. Will be interesting to see the additions he made.

Berkshire Hathaway Annual Meeting 2024

in Berkshire Hathaway

Posted

Does anyone know where to find the podcast with the Pilot CEO that Warren and Greg mentioned?