shalab

-

Posts

1,157 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Posts posted by shalab

-

-

CBO expects rate hikes this year and economic growth of 2.3%.

-

One would have thought Pakistan is a basket case and a terrorist den. Its GDP is around 1% of US GDP in USD terms. It has a population of about 220mm, about 2/3rd US population and about 30% more land area than Texas.

However, the stock return(s) point to something else - looks like it did very well and one of the best performing stocks after 9/11.

https://www.theglobaleconomy.com/Pakistan/Stock_market_return/

US investors can invest in it using the PAK ETF.

It also did mcuh better than India.

cheers!

Shalab

-

While I agree with you that US economy is healthy, Fed definitely has the power to damage it. The press did its job in pressuring them and it resulted in them leaking a story to WSJ about quantitative tightening. Wall street liked the leaked message on Friday.

BTW - I believe Elon Musk/Tesla have added tremendous value to the US and also to the world. I have no opinion on Tesla as an investment but I met an investment manager that has met Musk and invested in Tesla. Their opinion - "don't bet against Elon Musk".

...

My point, WPRT was a shit company. The US economy is quite healthy. Fluctuations can occur, that are quite material in terms of impacting the value of ones investment, and driven by nothing but sentiment. It’s easier to swim with the current, rather than against it. One just needs to find the current. Who cares how long Jerome Powell needs to chase his own tail...

Amen

Forget what they say, just see what they do.

-

Thank you John Hjorth

I went through the bank data you shared - thank you for sharing. The bank share prices were lower at the end of 2018 compared to 2017 - the main reason being people are concerned about 2019. That to me would be one material change. Then there is the housing prices, lack of inflation and emerging market impact and overall less business activity.

I am curious to know what would constitute material change from your perspective?

Thank you, shalab,

Your last post puts more shades on your line of thinking. [still : To me, nothing material changed here, so far.]

Wikipedia : Flexibility (personality).

-

May be not damage, they might have created an opportunity. I deployed a bunch of funds in December and got high quality names for low prices.

First Powell said the rates are a long way from neutral when he didnt even know what neutral is:

Then he said a bunch of things that caused the market to nose dive

https://finance.yahoo.com/news/powell-said-seems-troubling-markets-181403220.html

Then in January he comes out and says he learned China is slowing down from Apple release. All along he has been saying that China is doing great and global economy is great. Then IMF comes out and lowers global growth forecasts.

This guy is Fed Chair for crying out loud - even a casual person looking at newspapers (unless it is all fake news)can see what is going on. He should have more data and insights than an orangutan reading newspapers.

What damage?Since shalab posted, I have had exactly the same line of thinking as Spekulatius. Maybe I'm more or less blind, but - for sure - I can't see it. I may be in need of a cane of the blind, though. The number of yellow rings here locally goes from one to three, as I understand things. I think two rings is for the user where the spouse/partner is still beautiful, despite it was so ages ago, while three rings is when you're blind.

Right now, I'm spending time to counter my blindness by thinking about position sizing for the Big Four US banks.

-

It looks like the fed chair goofed up big time - they are trying to undo the damage

https://www.wsj.com/articles/feds-patience-buys-breathing-room-for-asian-economies-11548393287

-

-

cigarbutt - I don't understand the last statement. Can you please explain in more detail?

Let us say carried value is 45B, current market value is 100B and retained earnings are 30B.

Book value would be 75B actual value would be 130B.

If one uses the morningstar P/B methodology, the fair value would be 105B.

The actual value would be 130B and the gap is around 24% - it doesnt seem miniscule to me.

However the above methodology is fraught with errors as the retained earnings may have been used to buy other businesses. Meanwhile the valuation of other businesses have also changed as many of them are growing at double digit clip.

My problem with the P/B valuators is that they will never apply this to comparable businesses. They won't apply it to UNP (P/B 5.66), Hershey (P/B 18.37), AMZN (P/B 21.20), PGR (P/B 3.31) or even MKL (P/B 1.52)

Here's a blog post with a look back on the BNSF acquisition almost 10 years ago. He's taken out over $30 Billion in tax free cash distributions (not including BNSF tax payments to parent).

https://berkshirebuffettandbeyond.com/2019/01/15/10-years-since-bnsf/

...

The point being that there is a growing gap between book value and intrinsic value but taking into account retained earnings makes the size of this gap relatively small.

-

Congrats - indeed experience of a life time! I can totally see how service would be in a different league compared to USA and Canada. The highest I have paid for a hotel is around $400/day on biz trip and had no time to check out different aspects of the property. I stayed at a top hotel in Thailand for a few days and it was a very different (in a nice way) experience as well.

Rambagh palace hotel:

Leela palace hotel:

Very useful insights - thanks for sharing!

Looks like the places you stayed are the top two for luxurious experience in India. https://traveljee.com/destination/asia/india-asia/most-expensive-hotels-in-india/

We stayed at four of the top ten...also Taj Palace Mumbai and Oberoi Mumbai. The Oberoi Mumbai was not part of the tour, but I stayed a couple of extra days in Mumbai and added it. Extraordinary hotels, but the service put them all over the top. You have very nice hotels in the U.S., but the service is nothing like what we experienced in India! Cheers!

-

Wally Weitz on Berkshire, if you add share buy-backs, it will add anywhere from 1-5% returns on top of the 7-10%.

Our largest stock holding is Berkshire Hathaway (BRK.A, BRK.B), and we are pretty sure Warren Buffett manages it just as he would if it were private. It holds a portfolio of marketable securities (which we are happy to own), dozens of operating businesses, and (at 9/30/18) cash equal to over $40 per B share. Berkshire companies and securities generate billions of dollars a year in excess cash, and the insurance companies provide a growing pool (currently over $100 billion) of virtually free float (premium money collected but not yet used to pay claims). This cash is reinvested in the business or used to make acquisitions.

We believe that Berkshire is currently selling below its intrinsic value per share and that its value will grow by 7-10% per year on average for many years to come. Drilling into the underlying businesses and investments, we like what we own. Its fortress balance sheet, its diversified portfolio of businesses, and above all, its culture of disciplined capital allocation should make it a solid core holding well beyond Warren's tenure. The stock price will fluctuate with the market and with Berkshire-related headlines, but we would expect its price to reflect its intrinsic-value growth over time.

May the sentiment “cheap but not that cheap “ prevail until they buy back $100 B + worth.

There’s an interesting topic on why value investing doesn’t seem to work anymore. BRK itself being a value play is a more interesting topic. Or most boring

It will be very interesting to see what they have done with the $100 billion in cash in Q4.

I think the most likely meaningful stock purchases are JPM and AAPL (however, the downside with Apple is it is already such a large part of BRK that it now influences the price of BRK; i am sure Buffett does not want the price of BRK to be too closely tied to fortunes of AAPL).

An update of buybacks will also be good.

If it has simply grown by another $7-8 billion (with no meaningful purchases) that will be disappointing. Although i think it is fair to say winter is coming and stocks and businesses will likely be going on sale at some point in the next 12-24 months (perhaps fire sale).

Today is actually the first day this year, that I visited Semper Augustus Investments Group LLC, to see if there were new Berkshire related client letters available since last years release. [Answer : No.]

Earlier years, Mr. Bloomstran released the client letters in the first half of February - at least before the 13-F/HR 20XXQ4 was released from Berkshire. Personally, I speculate it won't be so this year, because of the changes - partly actual and partly expected - in the 2018H2 Berkshire portfolio, because just about everybody expects Berkshire has been on a shopping spree in 2018Q4. [ : - ) ]

-

I am a Prem and FRFHF fan. I made money in FRFHF and ORH (when it went private). I bought Thomas Cook India at 196 INR last year. I follow all their investments India, Canada and the US.

However, I liquidated my FRFHF positions recently and went into Berkshire.

The reasons are as follows:

1. FRFHF transparency (or lack thereof) - in BRK case, we clearly know how much is needed for insurance ops and how much isn't. We also know headquarters gets 400 MM of cash per week to invest in anyway they like. This translates to 21B per year. Apple drop is likely temporary and BRK will make 750MM per year from dividends increasing every year with their Q3 position. I even bought apple when it dropped to 140s.

In FRFHF case, I don't believe their insurance operations are as sound - this is likely one of the reasons for hedges. Parsad suggested this a while back. So it is not clear how much cash is available to invest freely.

2. Berkshire investing FRFHF cash:

It is not clear how much cash is available to invest - they have issued shares to raise money for acquisition(s). Parsad suggested in one of the threads on FRFHF to reduce leverage. They haven't done that. They also run hedge funds in India and Africa and pocket fees. Where are the best ideas - is it in FRFHF or in the hedge fund? One of the suggestions by SD (which made the most sense) was that they are getting the next generation setup in the family business. Many people go to FRFHF annual meeting spending a bunch of money. Nothing of substance comes out either about the company or about its direction.

I believe there are better options available right now than FRFHF.

Shalab,

First of all I have benefitted from your work here....thank you. I believe you discovered the share awards which I have a big problem with.

I see you on the Berkshire thread which is excellent discussing the value of the holdings and $100b cash....Berkshire holdings were decimated in the fourth quarter. Mr. Buffett has a$20b limit for holding cash.

So Buffett has $80b cash on a $500b market cap...and many are excited about his buys despite Apples massive losses as well as others.

My questions to you are

1. Are Prem and HW actually that bad that with $20b+ in cash on a $12b market cap and minimal losses in the fourth quarter in comparison to Berkshire....that you doubt they benefit from the opportunity less than Berkshire did?

2. What is Fairfax worth if Mr. Buffett is running the investment portfolio?

-

Let us bring back Geico with 30 B valuation as opposed to 50B - Buffett has said that 20B is the emergency cash that is needed to run all the insurance ops.

BNSF - 100B

Manufacturing and service - 150B

BH Energy - 60B

Total: 310 B

net value 205B - 310 B = -105B

Geico => 30B

net value = -135 B

You get financial products and other operating insurance subs for free.

-

What you are saying is absolutely right - I like USA the best when it comes to the stock market - the managements are generally shareholder friendly and very efficient. It doesn't hurt that USA has some of the best companies on the planet. E.g:, Japan has several successful companies but several investors have written about their experiences there - stakeholders other than shareholders are given priority.

India's commercial and court system are borrowed from Britain. So they are similar to the US in many respects. People should see better returns in India compared to some of the other "emerging" markets. E.g:, there is a reason why many RE companies in Hong Kong trade for low valuations - fraud is rampant. This problem of dishonest promoters also exists in India, out of the 6000 companies listed in the exchange, only about a 1000 or so are investable.

Here is the story from one of the super investors for reference:

Dazel - my estimate is that FRFHF has ~10% exposure to India. It is definitely huge compared to FAANGM's exposure to India. However, even old economy companies like BTI, CL, PG, UN have more exposure to India than FAANGM.

One can open a brokerage account in India (it is quite a hassle, time consuming but can be done), it will allow one to buy public companies in India. I expect Indian economy to grow to 5.5 trillion USD by 2030. At the same time US economy should be around 30-35 trillion USD. Canada would probably be at 2.5 trillion While India will do very well, the USA will also do well.

High GMp growth does not necessarily mean a strong stock performance. China for example still has high GNP growth, but a very poor stock performance for many years now. There are numerous other examples. I believe stock market performance depends much more on how this GNP growth is achieved and profitability metrics than the actual GNP growth

-

Ok - remove Geico. Add manufacturing and service - 10 B income with 15% growth. Put a multiple of 15 on pre-tax earning (after tax 19) - market value 150B.

So - we do the same calculation without Geico.

BNSF - 100B

Manufacturing and service - 150B

BH Energy - 60B

Total: 310 B

net value 205B - 310 B = -105B

This is not counting Q4 which I expect Q4 to generate another 7-8B in cash.

WEB and Munger do buyback at 207. It is safe to say no one understands BRKA valuation better than these two gentlemen. My son and I did some calculations last week, looks cheap even today.

market cap: 500B

Look through stock portfolio (Q3): 180 B

Cash and short term: 115 B

net value: 205 B.

BNSF: 100B (comp UNP)

Geico: 50 B (comp PGR)

Berkshire energy: 60 B (comp Duke energy)

Total: 210 B

Net value: -5 B

Remaining businesses are for free.

You are double counting geico cash and investments. Cheap, but not that cheap.

-

WEB and Munger do buyback at 207. It is safe to say no one understands BRKA valuation better than these two gentlemen. My son and I did some calculations last week, looks cheap even today.

market cap: 500B

Look through stock portfolio (Q3): 180 B

Cash and short term: 115 B

net value: 205 B.

BNSF: 100B (comp UNP)

Geico: 50 B (comp PGR)

Berkshire energy: 60 B (comp Duke energy)

Total: 210 B

Net value: -5 B

Remaining businesses are for free.

Why do you all think that BRK has not enjoyed a bit of a pop in 2019 like the S&P and other indexes have?

Is it that there has not been enough news flow specific to BRK, or do you think everyone is still worried about the investment holdings of AAPL going down in the portfolio?

Here are my guesses for BRK underperformance YTD:

1.) AAPL and financials big price decline in Q4 and upcoming substantial hit to Berkshire BV when year end results are reported in Feb. Headline will be ugly.

2.) AAPL profit warning (caused immediate decline in BRK) and concern about AAPL results going forward and potential impact on Berkshire BV.

3.) flight to safety reversing: as thepupil mentioned, BRK dramatically outperformed in the Dec panic, and now it is underperforming as investors shift to riskier stocks.

The good news:

1.) since the start of the year, financials are on fire and we all know they are twice the size of AAPL in the BRK portfolio.

2.) AAPL, re-priced in the portfolio at $155, is now cheapish. It could go a little lower but the big decline is behind us. At some point in the next year or two Apple will launch a must have phone and when they do sales and profit will hit new records and the company will be valued over a billion $. At $155 this is a great long term hold for BRK. Having said that, i do think 2019 could be a very difficult year for Apple. China may be a big problem, and may persist for a year or two. And the current lineup of iPhone’s looks uninspiring with the result that people will hold on to their current phone a little longer on average (which will impact unit sales and profits. Fortunately, Apple does have a pretty good track record of recognizing mistakes with the iPhone lineup and making the proper course corrections the following year.

3.) at the end of Q3 BRK had $100 billion in cash. BRK bought $25 billion in stocks in Q3. With the decline in stocks in Q4 i would expect more than $25 billion in new stock purchases in Q4. Perhaps big additions to APPL, JPM etc. If so, this will meaningfully increase earnings power of company.

4.) BRK buying back its own stock: I expect more commentary from Buffett about this in this years annual letter. Given the size of APPL and financials, and the investment portfolio in general, we could see large swings in BV from quarter to quarter. Buffett has his own idea of intrinsic value of BRK and it obviously doesnot swing so dramatically quarter to quarter. Perhaps we will see BRK buy back its own stock at 1.4x BV when it feels the stock portfolio is being undervalued by Mr Market (resulting in BV being understated).

5.) as the US banks have communicated, the US consumer and economy continues to perform well. We can expect the Berkshire op co’s to report very strong results.

6.) tax reform: BRK was one of the big winners and the benefits of tax reform will continue into future years. The stock price today is trading close to where it was trading in Nov of 2017 when tax reform was being discussed. Bottom line is it does not look to me like Mr Market Is valuing Berkshire higher even though its future after tax earnings will be much higher as a result of tax reform.

7.) long term bond yields look like they have peaked and may be headed lower. All things being equal this will allow for a higher PE to be attached to stocks (in general).

8.) as volatility returns to the market, Mr Market may start to value ‘stalwart’ (bond like) stocks like BRK a little higher.

9.) insider buying: $20 million purchase by Jain in Dec likely around $192 is encouraging.

BRK looks attractively priced at current levels. I buy it in place of holding a bond. When it runs up 5-7% i am happy to sell. Rinse and repeat.

-

Dazel - my estimate is that FRFHF has ~10% exposure to India. It is definitely huge compared to FAANGM's exposure to India. However, even old economy companies like BTI, CL, PG, UN have more exposure to India than FAANGM.

One can open a brokerage account in India (it is quite a hassle, time consuming but can be done), it will allow one to buy public companies in India. I expect Indian economy to grow to 5.5 trillion USD by 2030. At the same time US economy should be around 30-35 trillion USD. Canada would probably be at 2.5 trillion While India will do very well, the USA will also do well.

Shalab,

Totally agree....Fairfax India and others are a better bet for sure if you are India focused. $20trillion @2% vs $2.7t that will double likely every 6 or 7 years....is the place to be. Many better opportunities in India and those with feet on the ground would blow away Fairfax or any other investment vehicle.

Fairfax gives you exposure to India and particular in the private market they are integrated in the financial system there and will get a lot more opportunities than others because of the trust they have earned there. But as you say being able to play in all of the other world economies is very important ...No one else really gives you that optionality that I see with direct exposure to India of “some” scale. If there is someone I would be very interested in them as an investment.

Ironically, Thomas Cook India has been a home run that Hamblin Watsa do not get much credit for...in the equities poor performance hit they are taking publically. What have you done for me lately prevails and that is fair after some of the big stumbles.

Ie Apple and Amazon are growing massively in India but will not even move the needle to their world incomes.

-

Dazel, hope FRFHF works out for you.

US is a 20.5 trillion economy. India is at 2.7 trillion. Canada is at 1.7 trillion or so. FRFHF market cap is 13 billion. There are many opportunities in the market some of which will undoubtedly be better than FRFHF.

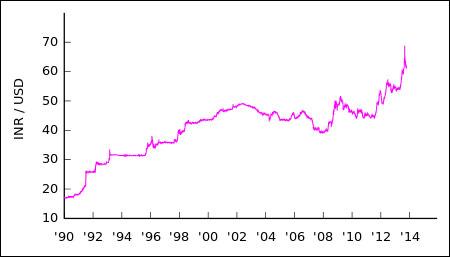

One can simply buy ThomasCook India and bypass the overhead of owning FRFHF. Even better, one can buy businesses with better prospects in India. Note that ThomasCook India has been flat since 2015 in Rupee terms and doesnt pay much of a dividend. The indian rupee has declined against USD at the same time.

"-Fairfax followers are as bearish as I have seen since 2003."

Seriously?

Back then it traded well well below book value and it is not the case these days. Now they need to generate earnings at a reasonable ROE to justify trading above book and to move up.

Cardboard

-

Very useful insights - thanks for sharing!

Looks like the places you stayed are the top two for luxurious experience in India. https://traveljee.com/destination/asia/india-asia/most-expensive-hotels-in-india/

-

Dont think it works for USA based investors.

Here is one idea if you are ok with cigarette companies. BTI (British American Tobacco) which owns close to 30% of ITC (India) looks cheap and sports 8%+ dividend yield. ITC has branched off from tobacco and is in the hospitality business. 1/5 of BTI valuation is covered by its ITC stake.

In what about investing in Indian mutual funds?

Franklin India Prima had 19.75% CAGR over 22 years:

Even after adjusting for Indian Rupees weakening agains USD it's not too bad:

https://im.rediff.com/money/2016/sep/19graph-rs.jpg

-

One can open a trading account - as Guy Spier mentioned, it can take a while to open one. It took two years for him and it took a while for me. I went through tradeplusonline.com. They offer excellent customer service and the process went quickly once I went with them.

http://www.nriinvestindia.com/qfi.html

http://investindia.kotak.com/qualified-foreign-investor

https://www.tradeplusonline.com/

Also - when investing in India, be careful. Here is the story of one super investor who lost money and is complaining to SEBI (SEC of India).

Another thing to be aware of is that India's inflation rate is around 7-8% - whereas USA inflation rate is around 2% or lower. So one should expect currency depreciation over time in India.

-

-

Starting a thread to discuss investing ideas in India

Pabrai and Spier on India:

FANGM doing well in India:

Looks like FANGM is doing well in India:

Google:

https://entrackr.com/2018/10/google-india-revenue-profit/

FB:

Netflix:

Apple:

https://yourstory.com/2018/10/apple-india-profit-grows-140-percent/

Microsoft:

Amazon:

https://inc42.com/buzz/amazon-india-revenue/

India ETFs and mutual funds for USA investors:

https://money.usnews.com/funds/search?category=india-equity&etfs=true&mutual-funds=true

-

Looks like there won't be a hike immediately:

Hope so - but looking at comments from others - it looks like the Fed may still raise rates

Cleveland Fed:

https://www.cnbc.com/2019/01/04/feds-mester-says-if-inflation-doesnt-rise-fed-could-stop-hikes.html

"If we don't see inflation picking up and we see the labor market staying reasonably strong from where we are now, that may tell us we're not neutral."

Cramer thinks Fed has outdated models and I tend to agree:

https://www.cnbc.com/2019/01/04/cramer-fed-will-hike-rates-until-there-are-firing-and-layoffs.html

CNBC's Jim Cramer argued Friday that the Federal Reserve's policies are severely outdated, and said the central bank won't stop its rate-hike policy until Americans suffer from "firings and layoffs."

Ah... the guy woke-up!

Cardboard

-

Six of my family members (other than myself) and several friends are investing in BRK.B in this way - buy or save money to buy 1-2 brk.b share every paycheck for atleast 50 brkb every year. We are comfortable to have up to 50% of our assets in brk.b

Please take the poll. And please feel free to comment the way you like.

Gross position defined as if you use leverage.

{kind=link}

POLL: Fed and interest rates

in General Discussion

Posted

Thanks - looks like the Fed did the right thing finally.

https://www.cnbc.com/2019/01/30/fed-leaves-rates-unchanged.html

I expect the USA GDP to be close to or cross 22 trillion at the end of 2019. Let us see how it goes. It was 20.66 trillion at the end of Q3. I expect it to hit ~21 trillion at the end of 2018.