maplevalue

-

Posts

282 -

Joined

-

Last visited

-

Days Won

2

Content Type

Profiles

Forums

Events

Posts posted by maplevalue

-

-

This Week in Virology 762 - SARS-CoV-2 origins with Robert Garry

I don't necessarily agree with the conclusions of the people in the podcast (particular with respect to CCP obfuscation), but still an interesting discussion with some Professors from Tulane and Columbia. They are fairly dismissive of the lab leak hypothesis. -

7 minutes ago, Parsad said:

- The virus came out of a lab, but the conspiracy theorists said let's not wait for evidence.

Which is it...do we base decisions on evidence or speculation?

As value investors, you invest based on evidence or fundamentals. As a speculator, you invest based on speculation.

In the face of uncertainty one should base their decisions probabilistically.

The probability a novel coronavirus was the result of a lab escape, given it emerged a couple hundred metres from a lab which was conducting research to create novel coronaviruses, and given China has a history of lab escapes for the original SARS, is non-trivial and hence the lab-escape theory should always have been taken seriously.

-

started position in Morguard North American Residential REIT (MRG.UN)

-

Many big name investors sit on investment committees for non-profits they are passionate about. A good way to be connected with a non-profit, contribute your skillset, and also gives you confidence when you give money it is being managed responsibly.

-

16 minutes ago, muscleman said:

Does anyone know any historical examples of similar irresponsible actions like this? I would like to study those cases.

Not an exact comparison, but there is this gem from May 17 2007

Quote"Federal Reserve Chairman Ben Bernanke said Thursday that he didn't believe the growing number of mortgage defaults would seriously harm the economy"

https://www.cnbc.com/id/18718555 -

Quote

A McDonald's restaurant in Florida is paying job applicants $50 for turning up to an interview amid struggles to hire new employees. The franchise owner, Blake Casper, who has 60 McDonald's restaurants in the Tampa, Florida area, told Insider that a general manager gave him the idea for the interview reward after telling them to "do whatever you need to do" to hire workers. Casper he believes it is difficult to hire workers at the moment due to the number of businesses reopening and hiring, alongside enhanced unemployment benefits.

...

Casper also said he is considering raising starting wages to attract more employees. The McDonald's restaurant currently pays $12 an hour, which is $3 above Florida's minimum wage, but he is considering increasing the wage to $13.https://www.newsweek.com/mcdonalds-restaurant-offers-job-applicants-50-turn-interview-1585692

-

On 4/20/2021 at 9:33 AM, wabuffo said:

Some of you may say - "well by buying 40% of that issue, the BoC helped the Federal Govt get that low rate on the other 60%. That is false. Federal govt's spend first, creating financial assets in the private sector banking system. The debt issuance (as I've explained before) is just a bank reserve maintenance function and not actual borrowing.

Central bank policy makes no sense to me.

wabuffo

Thank you for this comment and it led me to look more into the mechanics of how BoC QE is operating. One question I had, which you may know the answer to. So the BoC currently remits its earnings to the Federal Treasury. I am just thinking about a situation where if interest rates rose, the value of the bonds fell and interest expense on reserves increases, the BoC could run at a loss one year. Does the govt need to write a cheque to the BoC in this scenario? Or could the BoC just run a negative equity position (it's all funny money anyways).

-

With respect to government spending I think the comparison to the World Wars is weak at best (in terms of the necessity of the spending).

One of the things that will be interesting is the future political will across the country to impose higher taxes to pay for the COVID response. Income taxes were introduced around WWI and made permanent after WWII. For me I can see how Canadians would have come to accept income taxes as an acceptable price to pay to put an end to Nazism. But with COVID related government spending there has been such incredible waste and misallocation of resources (e.g. self-employed people getting CRB who claimed negligible net income in 2019, Chinese state-owned companies accessing the wage subsidy, Leon's Furniture getting the wage subsidy and then paying out special dividends, WE Charity fiasco) that I believe a large part of the electorate will be unwilling to accept higher taxes.

All of this probably points to a continued period of endless QE/zero interest rates forever.

-

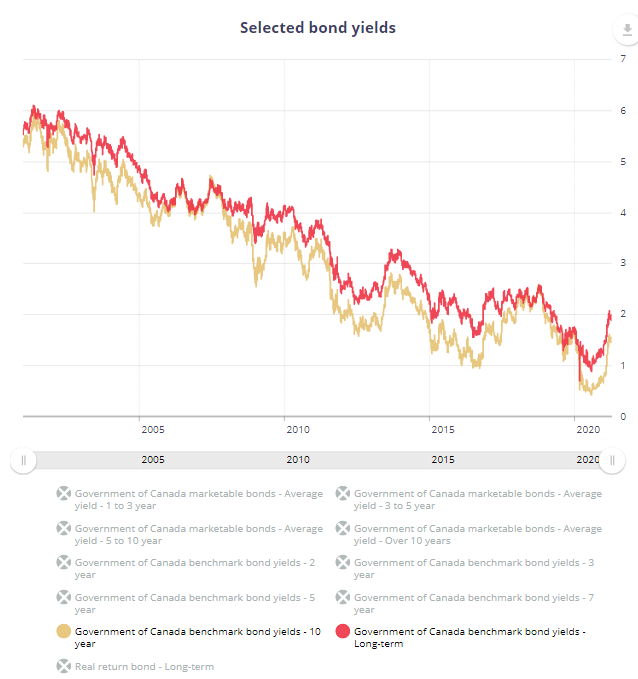

Also to put into context what is happening, in 2020-2021 GoC issued 267bn short-term bonds (2yr/3yr/5yr) 107bn long-term (10yr/30yr), 2021-2022 they will issue 160bn short-term 121bn long-term (and keep TBills about the same). Relative to keeping proportions the same it means they are issuing an 'extra' 38bn long-term debt. Now one can compare this 38bn to the total size of the debt outstanding (par value) right now:

- TBills: 218bn

- Under 1yr (excluding TBills): 104bn

- 1yr-5yr: 442bn

- 5yr-10yr: 120bn

- 10yr+: 166bn

So while they are extending the term of the debt, it really pales in comparison to what is currently outstanding, particularly the 764bn maturing in under 5yrs. Better hope rates are low forever!

-

43 minutes ago, SharperDingaan said:

Media will focus on the spend. The real benefit is the planned change to the debt maturity profile - rolling out to 10yr and 50yr terms. Very likely as $CAD bonds, with inflation driven rate escalaors and reduced taxation depending on the type of bond (green) and term (infrastructue). Very elegant, very smart, very BoC alumni.

Two comments on this.

First on the debt maturity profile. 10yr/30yr yields are already back towards pre-COVID levels so while it is nice to see the extended issuance, the attractiveness is not what it once was. Also, the long end of the curve is less influenced by central bank policy so issuing more can 'move the market'. I believe last year Canada was thinking of having more long-end issuance but did not because of possible market impact. Canada is a small open economy and investors do not view CAD debt in the same way as UST's so this shift to long term issuance could push rates higher (who really wants to buy 30yr debt at 2% in the midst of a massive economic rebound?), and is hence not the 'free lunch' it is being marketed as.

Second, I view the green bond as a waste of everyone's time. It's not clear to me that that this will trade at a lower yield (i.e. savings for government) than standard issue Government of Canada bonds, and there are also likely to be a bunch of costs related to setting up the program.

-

TVO Interview with Federal MP Adam Vaughn - What Should the Government Do About Housing?

Absolutely terrific interview to understand the mindset of politicians in Ottawa about house prices, and the lack of political will to do anything about it. Basically says we cannot have a 10% correction in house prices, even after a 20%-30% runup, because we need to "protect the investments Canadians have made in their homes". -

Quote

A clause in Rogers’ 128-page takeover offer has hedge funds eyeing big gains from Shaw’s preferred shares

Specifically, the document stated Rogers can force Shaw to redeem $300-million worth of preferred shares on June 30, for $25 each. In return, Rogers pledged it will pay Shaw $120-million if the Calgary-based company redeems its preferred shares, and the takeover doesn’t close next year. That payment would be in addition to the $1.2-billion break fee Rogers will hand to Shaw if the deal falls apart.

From Rogers’s point of view, getting Shaw to buy back its own preferred shares is good housekeeping, according to one hedge fund manager who owns the securities. (The Globe and Mail is not identifying the source because they are not authorized to speak publicly about the fund’s holdings.) These Shaw shares are only redeemable once every five years. If Rogers misses this opportunity, it will be forced to keep paying out cash dividends until 2026. Rogers would rather use that money to pay down debt, or fund 5G networks.However, there’s a significant gap between where Shaw preferred shares have traded since the takeover was announced – around $21 each – and the $25 a share the company would pay out at the end of June if it chooses to redeem. Wasps at picnics have nothing on merger arbitrage funds that smell a 15-per-cent-plus return in less than three months. This is becoming a popular trade.

A clause in Rogers’ 128-page takeover offer has hedge funds eyeing big gains from Shaw’s preferred shares - Globe and Mail

-

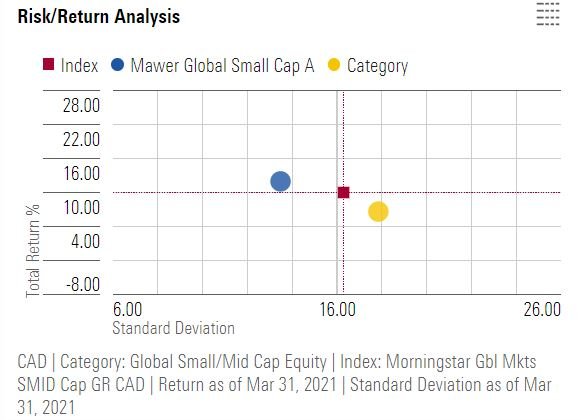

No thoughts on that particular fund, but worth looking at some of the Mawer funds. Risk-adjusted returns fairly strong (Global Small Cap fund risk/return analysis from Morningstar below). Can invest as a Canadian, and can invest direct with them for lower MERs (fund I mentioned is 1.76% MER). Does not resemble the index very much.

-

Some similar comments from Prem Watsa in Fairfax Financials most recent annual report https://s1.q4cdn.com/579586326/files/doc_financials/2020/q4/WEBSITE-Fairfax-Financial's-2020-Annual-Report.pdf

... companies that have survived for over 100 years have four characteristics:

1. They are sensitive to the business environment, so that they always provide outstanding customer service.

2. They have a strong culture - a strong sense of identity that encompasses not only the employees but also the community and everyone they deal with. Managers are chosen from the inside and considered stewards of the enterprise.

3. They are decentralized, refraining from centralized control.

4. They are conservatively financed, recognizing the advantage of having spare cash in the kitty.

-

FFH, have been growing more comfortable with the name and prefer it over the indices in what is today a very uncertain investing environment.

-

Message on TD Online Broker Today

"We are currently experiencing issues with order entry. You will not be able to edit or cancel orders submitted. You may also experience delays receiving fill reports in your Order Status. Please use caution when placing your orders; they may have been filled.

We are investigating the issue and working to restore service as soon as possible."

!

-

There was a good post by VC Sam Altman on inflation, sorry no link, where he suggests what is in store is faster deflation of anything depending on labor and inflation on anything otherwise supply constrained , basically equities, land, certain commodities.

I agree with this wholeheartedly.

It is amazing how frequently one reads about new labour saving technology (take a look at this video on autonomous fruit picking which looks like it is out of The Jetsons

). I think we have almost become numb to how fast technology is advancing. -

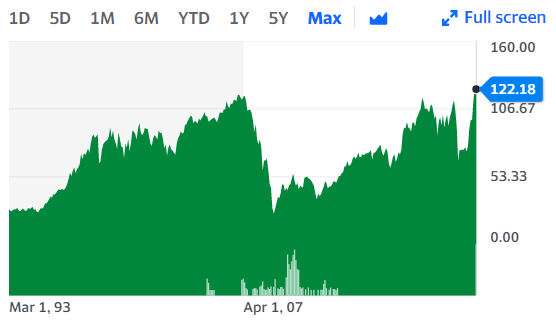

What kind of companies would you say would benefit from an interest rate increase?

One obvious one is banks/insurers.

The KBW Bank Index only recently exceeded its pre-GFC high (chart below https://finance.yahoo.com/quote/%5Ebkx/)

-

clearly permanent loss of cash purchasing power can't be good for savers, rich or poor.

why do nations and people accept it ? why wouldn't they just not spend or lock their money away even if it earns little ? isn't there a human tendency toward deflation as a protection of one's savings? or is the issue that the vast majority of people have no money at all so any handout or income, inflated or otherwise, is better than nothing?

Why do people accept it? Because of the money illusion (https://en.wikipedia.org/wiki/Money_illusion) where most people think in nominal, rather than real terms. Inflation of 2% is small enough that most people barely notice it, and do not adjust their behavior much (i.e. still treat cash as a fine asset to hold).

Why do governments accept it? Because the government can use it as a hidden tax on individuals. It's no surprise that when government deficits are large the same governments manipulate interest rates so that the real interest rate is negative (right now in the US the short term real rate is deeply negative, 10yr real interest rate is -0.60%).

From a fairness standpoint it is very unfair to individuals who are not financially sophisticated, since these individuals would tend to have large amounts of cash or GICs. The rich largely avoid the negative effects of inflation as they tend to own things like equities which fare relatively better during inflations.

-

This is exactly what concerns me--that inflation will not be something that occurs gradually, but in a highly nonlinear fashion that is "unpredictable", black swan like. A lot of economic phenomena occur like this thanks to lots of interconnectedness and feedback loops existing in our modern system.

I say it's better to prepare for it than to ignore the risk due to extreme asset price sensitivity to rates at these levels.

Agree with you here. One interesting thing to think about is that in response to a rapidly changing economic situation in 2020, the Fed conducted monetary policy in an 'emergency' fashion (i.e. inter-meeting cuts, cuts larger than 25bps). Given the nature of the COVID shock, and the potential for inflation dynamics to rapidly change in 2021/2022, it is not too crazy to think about the possibility they need to react in an emergency fashion to raise rates.

Probably a low-probability event, but given it is not priced in at all it's interesting to think about.

-

It’s astonishing how nonlinear the trend gets as you get down closer to zero rates: interest rate sensitivity of asset prices becomes very high in the regions closer to zero.

Yes, and closely connected to the big risk that exists in the market. 10yr risk free rate of ~1% vs. a pre-GFC 10yr risk free rate at 4%+ has wildly different implications for where the broad indices trade. Ultimately it will be driven by the inflation outlook, and with the financial markets increasingly divorced from the real economy the assumption of a continued Fed put is a dangerous one.

With this risk out there makes sense to stay defensive a be less sensitive to what the performance of the index is.

-

Seems pretty reasonable that there will be some inflationary pressures as the economy fully re-opens, but to project that as a new long-term trend seems a bit premature.

Right. I don't get it. We didn't have 6% inflation before covid, so what has changed?

What has clearly changed is the attitude of governments, and the general population, towards running large budget deficits. To take the example of Canada, the Federal Government ran a $400bn deficit in 2020 (16% of GDP vs. 4% in 2009), and has not produced a budget in two years. This government now has a ~50% of winning a majority this spring (if an election is called), and there is very little appetite for austerity.

One of the 'classic' causes of inflation is the government printing money since desired spending > taxes. The political dynamics around deficit spending ('build back better') are likely to be very different post-lockdown vs. post GFC so the low inflation experience of the 2010's is unlikely to be repeated.

Deficit source: https://tradingeconomics.com/canada/government-budget

-

I don't know if it is easily quantifiable, but it seems like our heavily financialized economy is responsible for a good portion of GDP instead of actual productivity increases or exports.

In 2017 1 of every 50 dollars of Canadian GDP came from real estate transaction fees!

Source: https://www.cbc.ca/news/business/real-estate-fees-home-sales-1.4226630

-

If inflation is at 6% for a sustained amount of time central banks will have to decide between

1. Keep low rates while letting inflation run at 5-10% for a few years to decrease the real value of debts while the general populace grumbles (much like Canadians have grumbled about higher real estate) but asset owners do well.

2. Raising rates in a meaningful fashion, leading to the collapse of the entire financial system and bankruptcy of the governments that appoint central bank chiefs.

My money would be on 1 being the more likely outcome.

Fed can't keep the rates low

in General Discussion

Posted

Financial repression at it's finest. Cash is trash!