crs223

-

Posts

636 -

Joined

-

Last visited

-

Days Won

2

Content Type

Profiles

Forums

Events

Posts posted by crs223

-

-

$4.4B in repurchases in Q1 (0.66% of outstanding shares). This was a good quarter for repurchases. Apr 1 - Apr 25, BRK repurchased an additional $150M (0.02%).

-

3 hours ago, treasurehunt said:

I guess the evidence is that PGR had a combined ratio of 96% for 2022, while GEICO had a combined ratio of 104.8%. Since auto insurance is mostly a short-tail business, the combined ratio is probably a good indication of underwriting quality.

PGR's combined ratio did rise to 99% in Q1 2023 though.

Thank you! — That makes complete sense.

-

1 hour ago, longterminvestor said:

I would tend to agree with you if

FYI it’s impossible to agree with me… I’m not smart enough to have any opinion, I just wanted to understand your logic.

My understanding: Progressive has a new technology for pricing insurance which dictates lower premiums. GEICO, without this tech and without lowering premiums, is losing market share to Progressive. Progressive is very intelligent and therefore is not underpricing their product.

-

16 minutes ago, longterminvestor said:

No, I am not saying GEICO is mis-pricing product. I am saying GEICO has to increase the price of their product due to the type of drivers they are now getting due to Progressive getting/retaining better Drivers. And GEICO has always won business on price alone, no other value proposition they offer - they are the low cost provider. Where as Progressive allows independent agents to package the Progressive Auto with other lines of business.

Progressive policy count/premium volume is growing and GEICO is shrinking as previously evidenced with financials and slides.

Thank you. Perhaps Progressive’s price is too low, as in my $1 example above? Why do you dismiss this possibility? (I just want to understand your logic, I don’t have an opinion.)

-

On 4/17/2023 at 8:55 PM, longterminvestor said:

Match rate to risk. I believe GEICO is getting the more risky drivers and has to price for that risk. If Progressive is attracting more good insureds defined as people who are generally safer and ultimately file less claims, their individual premium charged will actually go down over time (Progressive calls this their "Discount Loyalty Program" or something like that) but more policies in force means Progressive is growing top line. Conversely, GEICO is taking on clients who potentially could file more claims (the ones Progressive doesn't want), their rate charged needs to be higher. GEICO is not "raising rate/premium for raising sake". The premium is up for the individual policy because they are taking on an insured that is less predictable and the margin of safety needs to be included in the rate making formula - this is pure Buffett. However top line is shrinking because they are losing long time customers.

GEICO's entire premise is price, auto insurance is a commodity - policies are basically the same at personal auto level and loyalty comes with with getting best price - compete on price. And very clearly, they are losing on price, and they are losing the better risks on price. This is my point.

GEICO barely puts out anything public as granular as you are asking for. Here are the Numbers the way I see them:

GEICO premium 2020- $34,928B, 2021 - $38,395B, and 2022 - $39,107B - thats a 12% growth rate from 2020-2022

Progressive personal lines premium 2020- $32,620B, 2021 - $35,373B, and 2022 - $37,880B - thats a 16% growth rate from 2020-2022

Comping off 2020 with COVID skews numbers but its what I had infront of me - if you have more questions I can dig some more. This is just the way I see it, I hope I am wrong for Berkshire, I hope they are figuring this out. Just concerning how poorly Progressive is LAPPING GEICO.

And Progressives number for Q1 YOY are at a 22% growth rate. GEICO has not published Q1. BUT premium written for GIECO in Q4 2022 YOY was actually down, less than last year, premium is shrinking, another way to call that is negative growth.

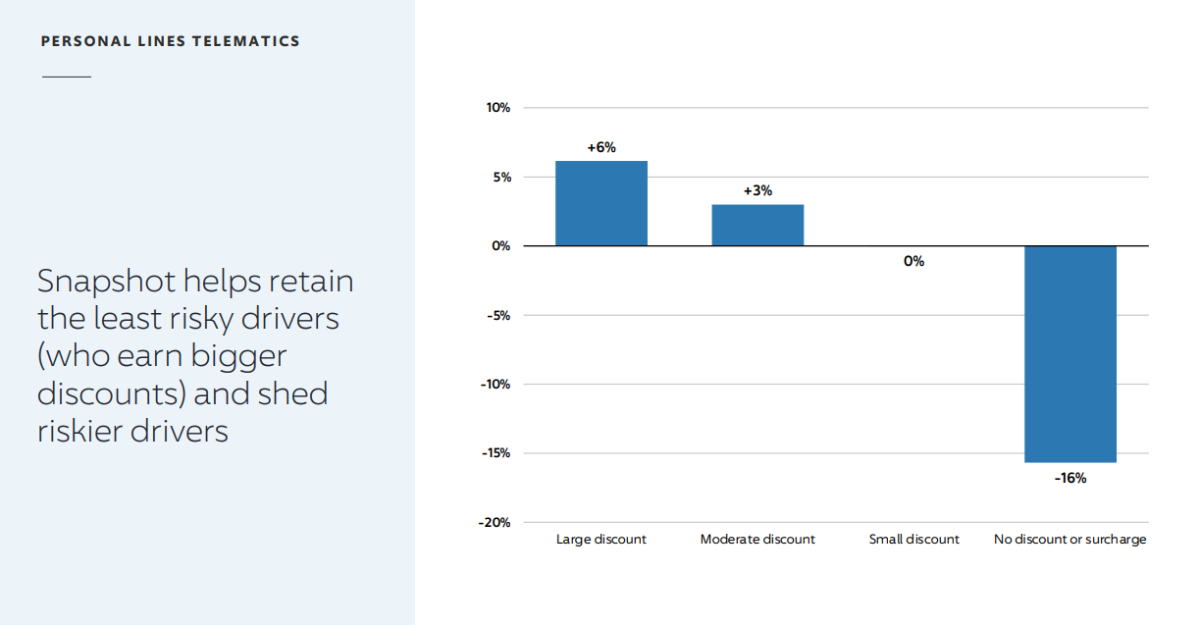

see slide deck from Progressive regarding attracting/retaining better drivers, this is public information:

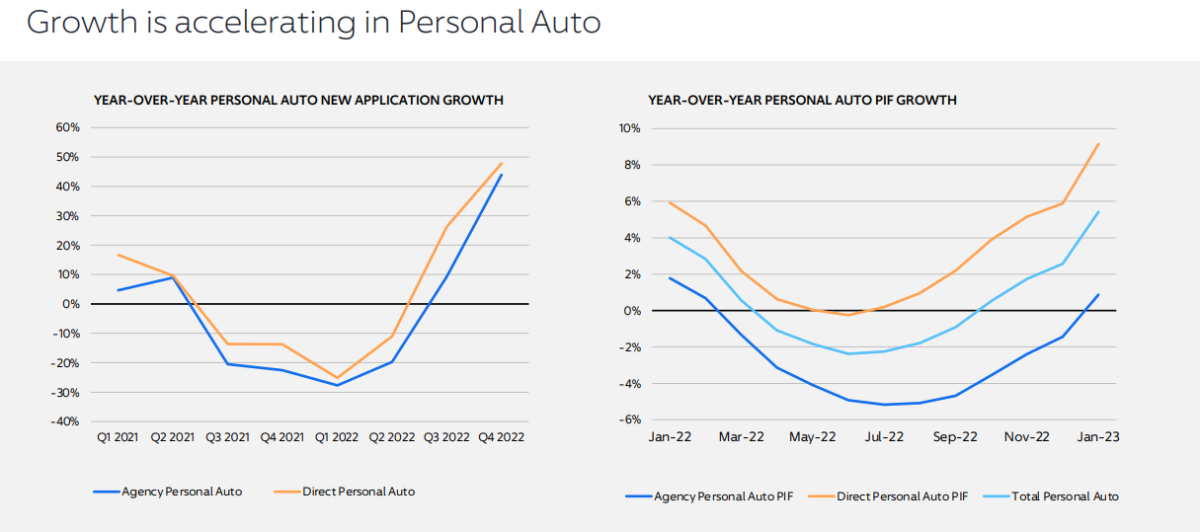

see slide deck regarding Progressive premium growth:

been busy with my day job, sorry for the late reply. Insurance in Florida is going nutty.

I believe you are saying "because good drivers are moving to Progressive, therefore GEICO is mis-pricing their product".

I could charge $1 for unlimited auto coverage. GEICO would lose all customers to me -- doesn't mean that GEICO is mis-pricing.

Q: What evidence do we have that Progressive is right and GEICO is wrong?

I'm not saying that GEICO is correct -- I have no idea -- I'm just trying to understand how the forum concluded that GEICO is mis-pricing their product.

-

2 hours ago, Luca said:

Nowhere did i say ,,to the moon,, or that i have no idea what they are doing...the reality is that amazon developed like it is due to their spawning and investing engine. Nick Sleep identified that early and its a different business now than it was 10 years ago. I wouldnt be surprised if we see a lot of new things and changes in perspective in amazon in another 10 years.

You did not say “to the moon”. You said you weren’t sure if it would double or triple.

You didn’t say “don’t know what they are doing”, you said that “we don’t know what they will create”.

I’m very sorry and I apologize. I am completely in the wrong and i will be more careful not to make such flippant comments in the future.

-

1

1

-

-

3 hours ago, Luca said:

Well, you read what you want to read. I never said i have no idea what they do, the current businesses are quite clear and understandable. The spawning engine on the other hand is kicking but we dont know what it will pop out, past performance showed that they have a good hand for it. Amazons financials are difficult to understand, they dont tell us how many millions were put in projects that didnt end up giving returns and how many millions lead to significant returns. AWS is an example of that spawning engine working very well. I also never said they are going to the ,,moon,, (again thats what you probably want to read). Amazon could very well be a 2x-3x over a decade. Its an incredible business...thats not the moon. Perhaps you have any other input than unnecessary noise. Your reply made me smile.

Im not saying anything about amazon or your investing prowess. Furthermore, I don’t have anything useful whatsoever to add on the subject.

I just thought it was amusing the way the sentences were structured. That’s all I meant.

-

2 hours ago, Luca said:

Wdym?

I thought you were describing a fraud — but then I realized you were bullish.

I read it as “I have no idea what they do, and they don’t tell us anything in their financials. But they are going to the moon!”.

-

9 hours ago, Luca said:

…which we dont know what it will create … we dont know the return on invested capital … statements dont reveal exactly whats going on …

Sorry but this just made me smile…

-

12 hours ago, backtothebeach said:

All 4 hours of the recent CNBC interview are now on Squawkpod.

That was great, thank you.

I loved hearing so much from Greg. Nice to know he's the "enforcer" for WEB. WEB had a great point: where else do you have an officer buying $100M of stock with his own money and no discount/grants/options. I love being a shareholder in BRK.

This one surprised me, particularly given the conversation around this site a year ago (which came from BRK letters from the early 80s): inflation is not that bad for auto insurers. BRK is not going to write a 20 year auto policy. They write 6 month policies and they can crank up the price pretty quickly. They'd write 15 day policies if inflation got up high enough! Inflation is not special risk to insurers... they just adjust the price as needed. "I don't wish it on anyone, but you could argue inflation is good for insurance because you get much bigger premiums on much bigger coverages". "over time, autos have gotten safer, accidents per 100 miles driven has gone down, but price for auto insurance has gone up 30-40x".

-

2 hours ago, Xerxes said:

Anybody knows how to watch this live without any of that CNBC PRO firewall

EDIT: i would be surprised if Buffett does not push CNBC to make this available pronto without the firewall. He is all about democratizing access to his point of views without hurdles. But would prefer to watch live.

... you can sign up for a free trial week of YoutubeTV and watch it on the CNBC channel.

I assumed we could watch it for free on CNBC but you've got me thinking otherwise now... how frustrating.

-

35 minutes ago, changegonnacome said:

SPY heading back to ~4100

How’d you pick 4100?

-

54 minutes ago, Spekulatius said:

I used to read ZH and John Mauldins newsletter starting in 2008 or so. They both sound clever, but if you go down these rabbit holes they are digging you end up wasting a lot of time and even worse, probably lose a lot of money just through opportunity cost if you actually start to believe the financial doomsday porn they are writing.

In my opinion, it's important to have some basic media hygiene in terms of what you are consuming. While it is probably a good idea to look at some alternative news sources from time to time, but if you start to dig into these fringe newsources there is a good chance you start to convert your thinking into conspiracy mush where Occam's razor has no chance to cut through any more.

@Spekulatius your entire post is brilliant, but the best two words are “sound clever”.

An inexperienced but moderately smart person will be drawn to a logically consistent “doom porn” article such as “US is printing; countries that print fail; therefore US will fail.”

There is an equally clever story that takes far more effort to digest: The Intelligent Investor by Graham.

Path of least resistance leads well meaning people to the story that is easy to digest.

For me the first dose of “antidote” came from Buffett’s article on gold.

Druckenmiller provides a good booster (me summarizing): “I’ve always been naturally bearish… but I can only make money being bullish.”

https://fortune.com/2012/02/09/warren-buffett-why-stocks-beat-gold-and-bonds/amp/

ZH is terrible for society — not because of Russia, or politics… but because it’s a doom narrative that “sounds clever”. In a cult like way it teaches that all other media outlets are full of shit and only it can be trusted to deliver the truth. I hope that our educational system can teach kids about bias in the media and understanding the agenda of a source. will be important going forward….

-

1 hour ago, Gregmal said:

But rule of thumb with stocks, people, life, etc, at least for me, is if you truly know and are comfortable with

No, this doesn’t work. When an intelligent person is getting started with investing reads ZH… that person “truly knows and is comfortable with” (your words) the system is corrupt and collapse is imminent.

-

2 minutes ago, Gregmal said:

Pitch fear? Those folks think theyre being prudent, conservative and responsible

Brilliant. I was personally screwed by this… i became “prudent, conservative, and fearful” in 2007. In 2009 I thought i was the smartest man in the universe and remained fearful until i finally got back in during COVID. Dutifully reading ZH every day. What a waste.

-

If Fed raises rates, ZH headline says “Fed Hell-Bent on Tanking Market”

If Fed lowers rates, ZH says “Fed Money Printing Will Destroy Society”

If Fed keeps rates same, ZH headline reads “Fed Refuses to Acknowledge Lurking Danger”

ZH is a waste of time.

-

5 hours ago, MCR said:

Here you go...

thank you!

-

1 hour ago, Parsad said:

Investor's have a lack of knowledge when it comes to how underlying securities work and what outlier events could cause to happen to security classes. Cheers!

Sorry but I don’t think I understand your point. Are you saying:

“People are foolish to move money out of 0.1% bank accounts and into 4% money market funds because risk/reward is bad”?

-

i emailed the CNBC marketing person and got two indecipherable responses to this question:

We know that CNBC “streams” the meeting on their “website”.

Q: Does CNBC broadcast the meeting on their TV channel?

… I’m preparing a watch party at my house …

-

2 hours ago, Xerxes said:

This is the first time I have seen that the "Cheers!" is not on a new line

Gotcha !

I once saw a cheers-less post. Gregmal was being disciplined over in the Disney thread…

-

2

2

-

-

26 minutes ago, Luca said:

I love Prosus, constellation software looks super expensive at first glance? What's the thesis here? 20-30% annual growth for the next years? They need to triple earnings to be valued at almost 25x. Don't see how this is an interesting business at that price.

I was really just reminding myself that I want to look into PRX and CSU as trustworthy allocators. I’m not interested in paying a high P/E.

-

46 minutes ago, RedLion said:

It worries me that everyone is so confident that there will never be anything to worry about at Berkshire.I’d prefer to own a less worrisome company than BRK. What do you recommend?

-

I don’t know what exactly is a cannibal, but BRK is not indiscriminately buying back stock. Only when it’s cheap. And from looking at the month-to-month purchases, “cheap” is not just about the stock price. WEB must be considering the changing intrinsic value and/or opportunity cost of spending that money.

Re BRK CAGRs, for me it’s about trust first and CAGR second. Right or wrong, I completely trust BRK to do the right thing for me while I’m at work, sleeping, market crashing, or rallying.

My preference would be to find a company/fund just as trustworthy but 1,000 times smaller (more CAGRs). But until that happens I’m with BRK.

Based on recommendations here (thank you) I’ll be watching Prosus and Constellation.

-

50% BRK

30% Privately Held

12% BABA

3% iBonds

3% S&P500

1% SAVE (formerly ATCO)

1% Cash

"Private" is the S-corp I work for. No debt, 9% FCF, essentially all of which is paid out as a divi, growing since I started 22 years ago at 10% CAGR.

Market downturns bring me joy -- BRK's brains and cash do all the work. I'd love to find a smaller company that give me the same joy.

I'm not interested in buying any individual stock that BRK could conceivably buy... rather just put that money into BRK and let them figure it out. I should roll SAVE into BRK.

I'm open to a BABA alternative. Ideally something with good FCF, that BRK would never buy, that will profit if US grows dumber than the rest of the world over the next 20 years.

-

1

-

US Regional bank stocks - PNC Financial, TFS - Truist, USB- USB Bank, MTB - M&T Bank etc

in General Discussion

Posted

How exactly do I quickly get my funds out of my bank using the website?

Can you guys “wire” funds from the website? (I cannot)

I can perform an ACH… but AFAIK that is technically the same as writing a check (which i can do without internet).