WFF

-

Posts

138 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Posts posted by WFF

-

-

13 hours ago, tnp20 said:

@WFF

Care to share your thesis on 1658.HK ? I am curious ....I kind of came across this today via a different route.

I am looking at Ping An after a recent sell off and remembered some mention of Li Lu/Himalaya possibly owning it. I look at the 2021 Annual report for Ping An to see if he owned it but it does not show up, its possible that Ping An is so big that he is not a top 10 shareholder (usually they list only top 10 in the annual reports).

However, he did get listed as a 6% holder on the Postal Savings bank of China annual report (2020 and 2021). He seems to have increased the stake slightly from 2020 to 2021 and ofcourse the recent slide has me curious.

Is the slide purely due to this mortgage non-payment issues ? Its hard to believe such a huge drop over some $20M HKD exposure...would appreciate your thoughts.

The largest retail bank, with lowest cost of deposit with no legacy loan issue. It used to be a deposit bank that doesn’t make any loans, usually to support government infrastructure. The market that it service has a high moat, people that are getting wealthier would likely continue to bank with PSBC (because it is in lower tiers and it doesn’t make much sense to build a branch). The amount they make align with the big 4 banks, due to agency fees paid to the Postal Service. However, a clause should be activated in the next 12 months ( my estimate) to re-rate the agency fee downward, powering its earnings. The stock trades already at 5x P/E, about a 6% dividend, with higher loan provisions then it’s counterparts. All stack to the upside I think.

The sell off consist mainly recession fears in China, the zero-covid policy is causing great economic harm and thus far there hasn’t been much relaxing of the policy. The second, is the housing/mortgage concerns that started last year, the fear is developers failing, and people not paying their mortgages.

This for PSBC is overblown, their biggest loan is to the railway (which I believe is like 20-30%), the developers exposure is minimal and haven’t dug deeper into the mortgages but I venture these are related to unfinished homes by the developers not regular home mortgages. But since they don’t have big exposure to developers, I am deducing that exposure to unfinished homes are limited as well, they are usually done in conjunction, and are given special access to mortgages as part of their agreement with developers.

In all, the bank is still trying to boost its lending, especially to the sannong and green initiatives as promoted by common prosperity. The declining environment might actually decrease overall risk for us as it goes on sale, but also for the bank, as they are underwriting for assets that are deflated.

-

bought me some 1658:hk under 5 HKD. Hopefully Mr. Market continues to discount the merchandise today

-

BAC, Sold Oxy 55 Puts expiring 7/15 for 0.45.

-

Added some more BAC. Might pick up some more 01658:hk especially if it breaches 5 HKD mark.

-

2 hours ago, Pessoa said:

You added twice, eh?

actually three times. Added more again. The first time was a starter and as it dropped I just kept adding. Probably a 5% position this far.

-

Added to JOE.

-

Added to JOE.

-

Bought JOE, BRKB, MU, DIS, PARA, BAC.

-

Added to PYCO, AIV, FRPH

-

On 4/2/2022 at 9:46 AM, WFF said:

PCYO, recycling some APTS proceeds that are now over the line.

Same old same old. This time picked up some BAC and AIV.

-

On 4/2/2022 at 9:46 AM, WFF said:

PCYO, recycling some APTS proceeds that are now over the line.

Same trade. Plus picked up some BAC

-

A quick search: scott.kirby@united.com

The fastest would probably be mileageplus@united.com if you are a member.

-

PCYO, recycling some APTS proceeds that are now over the line.

-

Picked up some BAC.

-

1 hour ago, NnnnotSoSmart said:

Am guessing the mystery buy(s):

1. 1658.HK - Li Lu is a substantial shareholder and could of influence Charlie. Plus the share price did trade around the prices Li Lu bought for Himalaya

2. 700.HK - Charlie has spoken in the past about how well Tencent has done with Weixin/WeChat. Given his stake in Baba wouldn’t be surprised if he starts to buy Tencent, as spin-offs and valuations are attractive.

Anyone done any detective work?

-

Added to FRPH.

-

FRPH, AIV calls

-

FRPH. Thanks for the sale Mr. Market

-

1658.HK

-

1 hour ago, NnnnotSoSmart said:

Not sure. I use TIKR to look for foreign holdings.

BYD HK(211) is the only foreign stock I see listed for Himalaya Capital Management LLC Investments

https://app.tikr.com/investor?id=5057306933&ref=gb181q

They also own quite a bit of PSBC 01658.hk. Found it on a filing with HKEX. If someone know a place, please share.

-

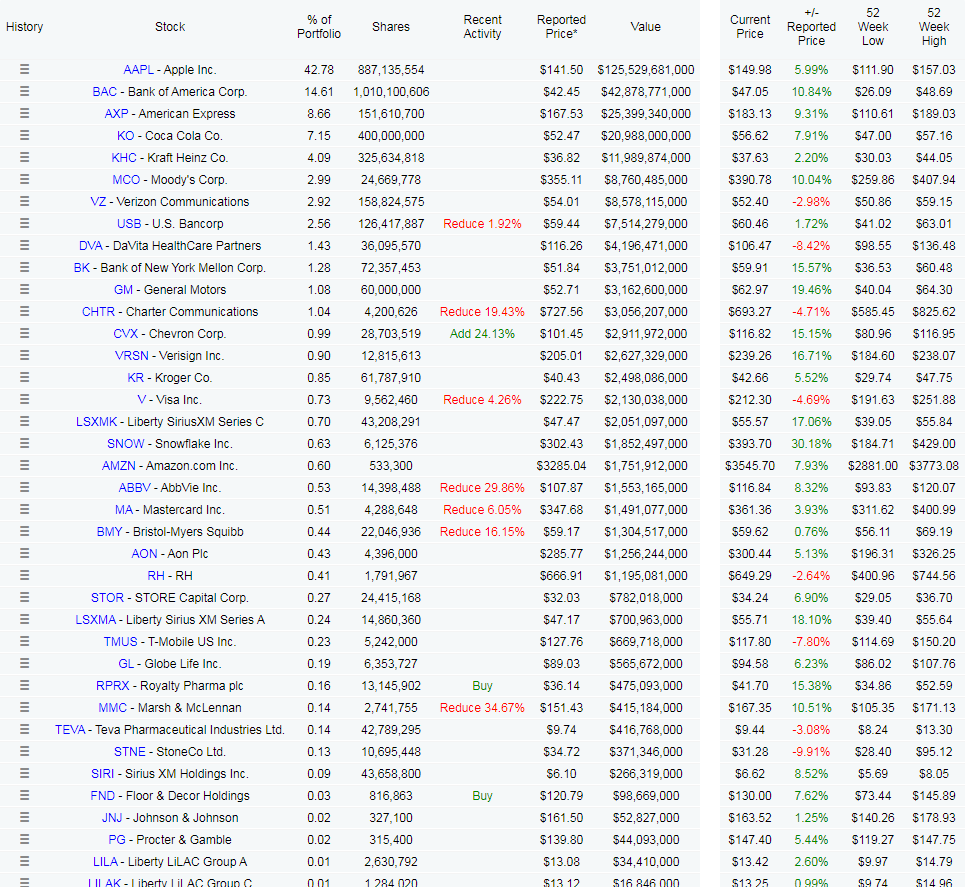

https://www.dataroma.com/m/holdings.php?m=BRK

Latest changes is out:

Add: CVX

New: RPRX (475m position) , FND (98.7m)

Reduce: USB, CHTR, V, ABBV, MA, BMY, MMC

Seems like Todd or Ted purchases.

-

-

Bought some APTS April 10 Calls

-

Free commission has allowed me to:

1. Purchase positions in small lots, usually averaging downwards vs buying up my entire position in one go.

2. Allow me to reinvest dividends at a time of my choosing vs scrip dividend

3. Similar to the above, buying a stater position to do additional research (owner notification mentality)

What are you buying today?

in General Discussion

Posted

Added to 1658.HK PSBC. If it keeps dropping, it is on track to be my largest position.