KFS

-

Posts

179 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Posts posted by KFS

-

-

31 minutes ago, KFS said:

Another video interview of Carson Block discussing the MW short.....

Fairfax Financial: The Oracle of Nothing - Zer0esTV: Video channel for short sellers

Block compares Go Digit to Lemonade to illustrate his assumption that Digit's market value has obviously plummeted "into the toilet" over the last few years. Lol.

-

Another video interview of Carson Block discussing the MW short.....

Fairfax Financial: The Oracle of Nothing - Zer0esTV: Video channel for short sellers

-

3 hours ago, MMM20 said:

This is where the tyranny of the book value people gets ridiculous. I can personally come up with twice his 18% number in fair value over carrying value and show that book value is at least 18% understated. He ignores the fact that cash flow has exploded 3-4x structurally higher over the past few years and that the stock is now trading at 6-8x those cash flows. All of the historical transactions can be explained by the fact that they were short on cash for a few years... but they're not anymore. The irony is he nailed the GE comparison... in the Danaher / Culp era. Decentralization, quality upgrades, massive turnaround, and now a well-run cash machine.

Well said. Even there is merit to certain "accounting gimmicks" in the MW report, the impact feels pretty silly and pointless in the overall picture. Even if you discount the book by 30%, it is still trading cheaper than peers.

And then you have other items like the big pet insurance sale ($1.4 billion in 2022 ??) that seemingly came out of nowhere. If anything, Fairfax might have been guilty of understating itself.

Consider incentives/behaviors. In 2020, Prem stepped in with his own money and purchased a whopping $150 million worth of shares during the fear and uncertainty of covid. He knew the intrinsic value of the business. FFH has made significant buybacks. Since the recent runup in stock price, Prem hasn't sold any shares, the company hasn't issued shares, and they still hold the TRS position. This would be very weird behavior for a company that is allegedly desperately trying to overstate its value via "gonzo-mode financial engineering."

The cash flow is what matters to me. With the amount of cash that will be gushing into FFH over the next few years, it would be pretty entertaining to watch the stock drop 30% only for the company to jump in with monster buybacks. One can dream.

-

On 1/26/2024 at 8:15 PM, Blugolds11 said:

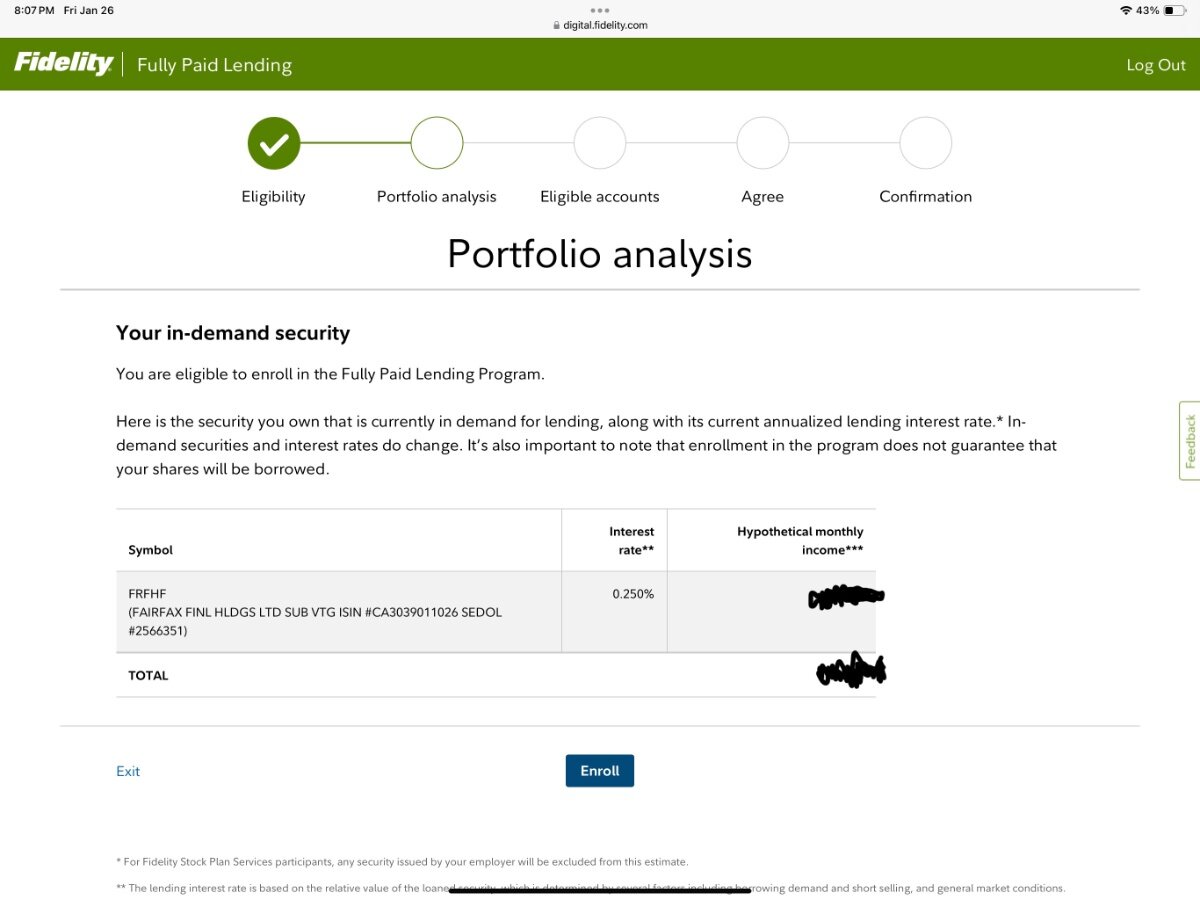

Logged into my Fidelity account and saw something at the top of the screen telling me that I am eligible for additional income by lending shares of a security. Happened to be Fairfax…Anyone else see this?

I didnt enroll, but have never seen that before….thoughts? Not necessarily as to if I should, but why they are doing it? Due to daily volume?

I've received the same notification from Fidelity. 0.25% obviously isn't much, but could amount to a couple hundred extra bucks per month if you have significant holdings. What exactly is the downside to enrolling? (If there is one.) Is this easy money with no downside?

-

3 hours ago, Haryana said:

FRFHF touches US $ 1000

Last updated: Jan 24, 2024, 11:35 AM ETSource: QuoteMediaOpen993.81Day High/Low1,000.00/987.00Half way there!

.... Take my hand and we'll make it I swear!

-

-

5 minutes ago, MMM20 said:

Shareholders hadn't completely thrown in the towel yet.

Narrative follows price.

Right-- That was kind of my point. These specific items are important to a degree, but overall investor sentiment is the driver.

-

12 hours ago, Parsad said:

For FFH to earn the premium on P/B, they need to keep more cash at the holdco level, increase the investment grade to at least "A" and add more quality...I reiterate...quality operating businesses. Much of the non-insurance operating businesses they own are not 2 times book operating businesses, nor do they fully own or control many.

FFH had a P/B of >1.2 as recently as 2018. It's not clear to me that any of the items above were fundamentally better for FFH at that time. Curious how one would explain this.

-

+31% USD

--- Long FRFHF throughout the year and added opportunistically. (Cheers, @Viking)

--- Long BRK

—- Smallish positions of Fairfax India and MKL

--- At various times during the year, short MSTR, AMC, GME, and TSLA (both directly and/or via puts).

-

23 hours ago, Viking said:

Well time to get the bubbly out this weekend for Fairfax shareholders. Why? Christmas has come early. Fairfax’s stock price has hit a new all time high today in Canadian dollar terms of $791.93 (markets haven’t closed). The previous all time high had been C788.88 on June 15, 2018. Congratulations to shareholders… it is always nice when a plan comes together! A few of us backed up the truck late in Oct/Nov of 2020 at under C$400 which has been a double in a little over 2 years. Not too shabby.

But the story gets even better. Trading today around C$790, Fairfax is still wicked cheap. My guess is ‘normalized’ earnings for Fairfax is north of US$100/share, or C$135/share. So the stock is trading at PE multiple of less than 6. Moving forward i think Fairfax should be able to deliver 20% to 25% returns per year for at least the next couple of years driven primarily by earnings growth and also a little multiple expansion. (I also expect the stock to continue to have lots of volatility… as per usual.)

The quality of my estimated C$135/share in earnings is very high: primarily coming from Interest and dividend income and underwriting profit. I also expect Fairfax to be very aggressive on the stock buyback front over the next year, taking out at least 1 million shares (perhaps 2 million) and this is NOT built into my earnings estimate. Other catalysts would be a Digit IPO or more asset monetizations like we saw in 2022 with pet insurance and Resolute Forest Products.

Congrats Viking and thank you for the excellent analysis on this company over the past few years. I seriously can thank you and others enough (glider, petec, etc.) for all the work you guys have done and shared on this board. I had been a quiet reader of this board for several years, and made a huge purchase of FFH during covid, shortly after Prem's large personal purchase of the stock, and made an additional large investment earlier this year. At this stage, Fairfax has had a meaningful impact on my personal financial situation and has probably shaved several years off my expected retirement plans... (I do not have an ultra-high income -- a 36 year old chemical engineer working in operations at a nuclear power plant.) Fairfax has "accidentally" grown to about 66% of my overall portfolio. Normally, I would rebalance to reduce the risk of being so far overweight in one security, and I may still do that only as a matter of principle, but given the future prospects and intrinsic value of the company relative to the (still low) stock price, I could just as easily stick with the full position for now... I think we are just getting warmed up, and I'm very much looking forward to what the next few years will bring.

-

Yeah, I'm on board and will contact them as well. I've been pretty tempted lately to pull some money out of Vanguard just to be able to buy additional FRFHF...... I imagine if enough people threaten to pull money off their system they'll hopefully do something about it.

-

Excellent, thanks.

-

6 minutes ago, TwoCitiesCapital said:

The only reason for the correlation is b/c people expect higher rates to result in higher income. But that's only true if you invest the cash into higher rates. Fairfax didn't do that last time we went through the cycle and rates were significantly higher than they are today.

I don't have a ton of confidence they're gonna put a ton of cash to work with rates even lower than prior opportunities they've passed on. Seems like the market agrees which is why the correlation broke down. We learned from history.

If interest rates go to 5%, I'll eat my words. But I'm highly skeptical that the 10-year gets sustainably above 2.5% for more than a 3-6 month period and it's not clear that Fairfax will put it's cash to work until rates get well above the 3.25% that was passed on in 2018.

Forward rate curve is already inverted for 2s-10s suggesting potential for another recession within 12-18 months. There's a very real possibility we sit on cash and miss it again.

Fair point. I guess I tend to assume Bradstreet & gang would be able to make some intelligent decisions if/when the opportunities arise, but of course you may be right.

-

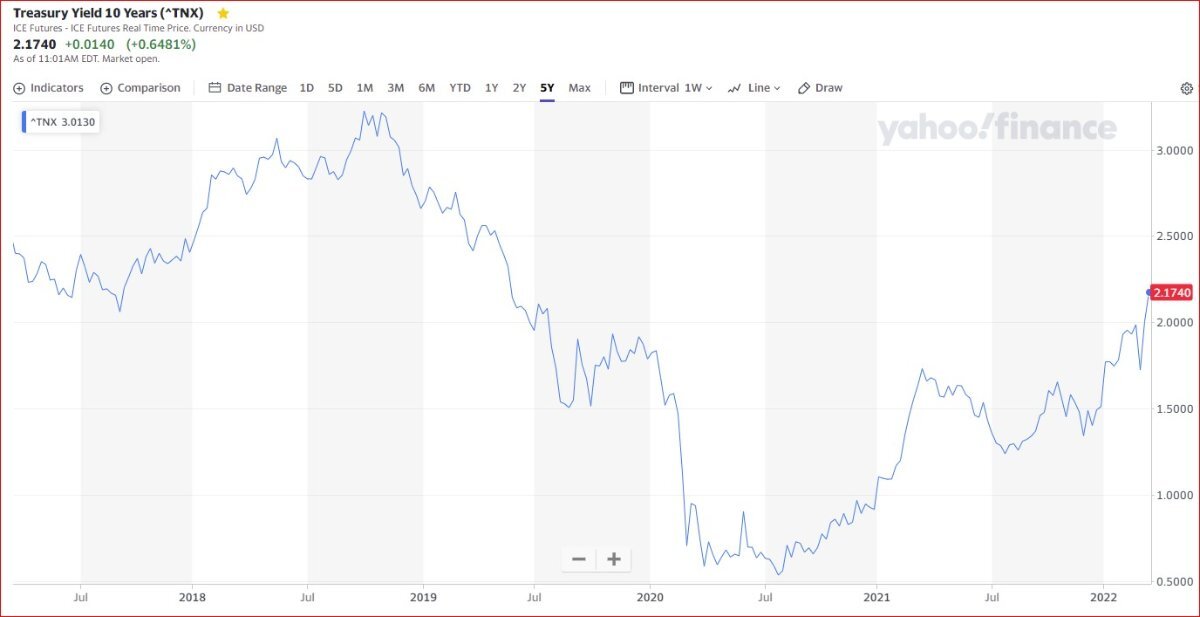

There are obviously many factors impacting Fairfax's stock price as discussed endlessly on this board, but I think it’s worth remembering FFH’s price/book ratio over the past several years -- like many insurance companies -- has been fairly well correlated with interest rates as you can see in the two 5-year charts below.

Just looking at some random data points over the past 5 years:

P/B 10-year %

July 2017 1.15 2.30%

August 2018 1.20 2.95%

October 2018 1.25 3.15%

August 2019 1.03 1.80%

Feb 2020 1.00 1.50% (just prior to covid crash)

April 2020 0.70 0.65% (just after covid crash)

August 2021 0.86 1.28%

March 2022 (today) 0.76 2.16%

Today, with the recent increase in rates, it sure seems FFH stock has not responded in the typical way…. As perhaps other factors are weighing heavily on the stock, or the market is simply asleep in failing to acknowledge this rise and the impact it could have on the company’s earning potential. Today the 10-year yield is at 2.16% and rising, and yet the P/B is lagging behind, still ~0.76. FFH’s insurance business/float has increased quite dramatically over the past few years, and one would expect rates to be an even stronger factor going forward, yet here we are. Like I said, there are obviously many other things affecting the stock as you all know, but I think it’s worth being aware of this historical relationship vs. the apparent lapse today...

-

1 hour ago, longterminvestor said:

Found this audio and transcript regarding Financial Crisis Inquiry Commission interview of Mr. Buffett. Audio below and transcript attached.

http://fcic.law.stanford.edu/interviews/view/19

2010-05-26-Transcript-of-Interview-With-Warren.pdf 210.82 kB · 3 downloads

This is a gem. Thank you for sharing.

-

23 minutes ago, Thrifty3000 said:

I have a friend whose mom has boxes of Beanie Babies sitting in an attic that originally cost something like $16,000. Every time I see her mom I have the smart assed thought to ask how many divvies those babies paid out last quarter. I refrain.

LOL. One of my favorites is this picture of a couple in divorce court dividing up their collection of beanie babies one by one, ~1999.

-

9 hours ago, Thrifty3000 said:

Don’t forget the impending crypto bust that will happen as soon as the greatest greater fool has placed their bet - and the crypto cult finally figures out how to discount all future cryptocurrency dividends to the present.Agreed. I tend to include all crypto in the meme/bubble basket which I'm sure will be unpopular with some people here. I have a very small position on MSTR puts.... if (when) bitcoin drops below ~30k, this turd is toast.

-

1 hour ago, Spekulatius said:

Anyone here also thinks that 2023 may be the year of recession? I think even Elon Musk tweeted a similar take. By 2023, the stimulus money hoard that is saved up will be burned and the inflation will start to eat seriously into the buying power.

Is this the real reason Musk has been selling his TSLA shares?? lol.

-

1 hour ago, Viking said:

My read is what the Fed does matters to financial markets. Monetary policy has never been as stimulative as it has been over the past 22 months. We have also had unprecedented fiscal stimulus (government spending/direct transfers to people) over the past 22 months.

Asset prices (stocks and real estate) the past 22 months have ripped higher. My guess is the unprecedented monetary and fiscal stimulus was a factor driving asset prices higher.

As of today we KNOW the fiscal stimulus is largely done. And the monetary stimulus will be quickly reversed starting Jan 1. End taper first (Q1). Then higher Fed funds rates (starting March?). Then shrink Fed balance sheet (2H 2021?).

If all the stimulus (monetary and fiscal) helped spike asset prices higher it makes sense to me that when it is withdrawn that will have a negative impact on asset prices. I just have no idea what the magnitude will be… Or how it will play out…

This

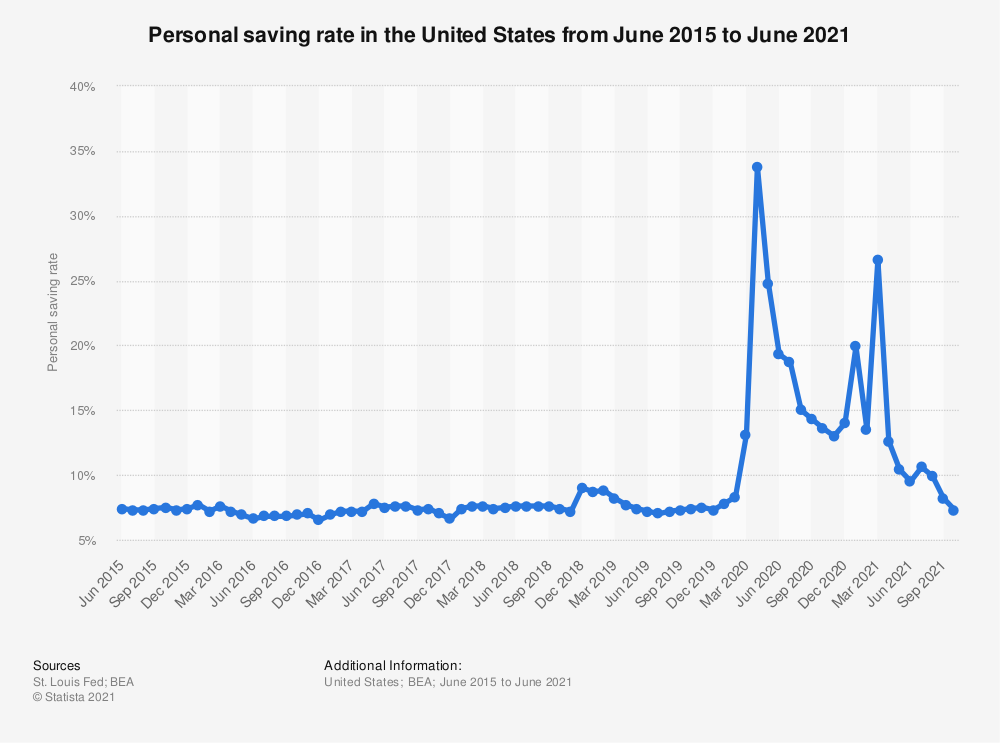

One of the most under-appreciated facts IMO has been the surge of the personal savings rate that resulted from huge amounts of stimulus. The chart below aligns shockingly well with the meme/bubble era over the past 22 months. The savings rate finally returned to normal level around October 2021 to a rate consistent with the pre-covid stimulus era. As you said, we know the stimulus is done, and policy will begin to reverse as the Fed has made very clear recently with persistent inflation as the driving factor. No idea how or when it plays out, but it seems hard to imagine that the meme/bubble and other stocks which rocketed due to stimulus will not be impacted by the reversal of the very thing that drove them up in the first place.

source: • U.S.: personal saving rate monthly 2021 | Statista

-

Very good (IMO) interview with Jim Chanos... Discussion of parallels with dot-com bubble, discusson of crypto, inflation, etc.

-

18 hours ago, mjm said:

anyone receive an offer from their brokerage for the FFH dutch auction? nothing from Fidelity.

Yes, Vanguard (FRFHF) on 12/3.

-

Insightful as always - thanks Viking.

-

2 hours ago, Spekulatius said:

I don’t think it is likely that FFH’s discount to NAV will close, the complexity and the fact that it is an controlled entity will make sure of that, even if performance improves (which is the bet that we are making). I can see this going to 1x book perhaps, but quite frankly, I don’t see this going to 1.3x book for a long time.

This is more of a reversal to the mean stock than a LTBH compounder for sure.

FFH was trading at about 1.2 - 1.3x book as recently as October 2018. Looks like 1.3x was roughly average in 2016 and 2017 and during those years it was not any less complex or any less of a "controlled entity" so I don't see how this alone explains anything.

-

Fairfax 2024

in Fairfax Financial

Posted

Fairly certain this fellow is a regular on this board. Well done.

It's completely incorrect to associate growth in Fairfax with book value adjustment: expert - Video - BNN (bnnbloomberg.ca)