allnatural

-

Posts

374 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by allnatural

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

FHFA's fiscal year (FY) ends on Sept 30. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

It also states that "FHFA plans to finalize the rule in the first quarter of FY 2021." Q1 FY 2021 = Q4 2020 (now) -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

Bold assumption by Tim Howard: -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

Assuming the final PSPA is similar to what Phillips had in mind and discussed earlier in the year. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

Bloomberg article titled "Fannie-Freddie Plan Could Face Race to Finish After Biden’s Win" this morning reported that a 4th amendment has been in the works for months now. "To avoid that outcome, shareholders’ fervent hope is that Mnuchin and Calabria before Jan. 20 come to terms on an amendment to Fannie’s and Freddie’s bailout agreements that Biden can’t unwind. Such an amendment could reduce the government’s massive stake in the companies, making it easier for shareholders to see a higher value on their own stock. Officials at the FHFA and Treasury Department have been working on such an amendment for months, said a person familiar with the matter, and long have been in agreement on some of the issues that such an amendment would contain." -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

I think ACG is putting the settlement window out to June simply bc it lines up with the latest SCOTUS has to rule on the Collins case. But you would think if they have conviction of a 4th amendment in Q4, that 4th amendment would decide the final treatment of the snr pfds. Theoretically if a 4th amendment includes writing down the snr pfds and a tax credit for the excess payments, the government doesnt need to engage with or "settle" anything with shareholders. They are simply giving them the remedy shareholder desired and would have the result of making the Collins case irrelevant. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

rolg, if they find that CID was ratified, doesnt that mean that the CID action survives? if not why even bother remanding it and just say the CID action is void. the way i read the backwards looking remedy portion is that this all comes down to whether the challenged action (NWS in our case) was ratified or not by the new director. if it wasnt, it gets voided. did calabria ever ratify the NWS, not one sweep was made under his watch. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

No because a a pspa amendment converting the current $250b credit line to a catastrophic paid for backstop will act as an explicit backstop. What else would you want to see if you are a credit agency. Doesnt require congress and this option is highlighted in the admin GSE plan from last year. Those whalen arguments indicate that none of this is at it seems. There's no way each one has not been carefully considered by Calabria and Mnuchin, especially Mnuchin, and plans are in place to address them. That said, I'm backing off my opinion of no more govt backing because it doesn't seem possible after reading his comments about it. So, regarding that govt backing, to every comment made by anyone against 4%, I think one very simple question by Congress must be affirmed: "Would these capital requirements assured no bailouts 12 years ago?". That's mandatory, no support without it. FnF have tanked since that pdf. I wonder if that's the issue, that this all can't be done without congress, and fear of Trump losing. Of course. Whalen is a douche and has been self serving an a big bank propagandist the whole time. He just cares about what pertains to him. You think Calabria will spend 2 minutes on his concerns after how he and Dave Stevens acted regarding the forbearance issues? There will be a fee paid for support to treasury which with the amount of capital they will have more then enough. There is nothing congress can do to stop recap now....and why would they? FnF need to come out of conservatorship. He may be a douche but his thoughts on FnF's credit rating being lowered and costs increased seems logical to me. So if FnF need, at the very least, another strong implicit guarantee, won't that require Congress' support? -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

Something to keep in mind, Watt's capital proposal allowed loan loss reserves to count as statutory capital. So the $4.1b of loan loss allowance put in place by FNMA today for Corona (which assumes 15% forbearance) should still ultimately count as capital if Calabria doesn't change that. From Watt's proposal: "Total capital, using the statutory definition, means the sum of the following: (1) Core capital of an Enterprise; (2) a general allowance for foreclosure losses, which (i) shall include an allowance for portfolio mortgage losses, non-reimbursable foreclosure costs on government claims, and an allowance for liabilities reflected on the balance sheet for the Enterprise for estimated foreclosure losses on mortgage-backed securities" -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

The more options you give homeowners, the better chances to get back into good status from forbearance to avoid delinquencies. Seems like there is a lot of mixed info out there. I've basically only heard forbearance for the 3-month term afterwhich an extension of mortgage modification could be requested. As for as when the forbearance is due, I've read a ton of articles that say either at the end of the 3-month period and a ton of articles that say they tack an additional 3-months onto your mortgage. I've also read a ton of articles where consumers are being told both of those things by their banks depending on who they're talking to. It really doesn't seem like ANYONE knows when the money will be due to be repaid at this point, but I imagine there will be some clarity once they've had some time. For an example, see this article from the WSJ https://www.wsj.com/articles/getting-a-mortgage-payment-break-isnt-the-boon-many-expected-11587634200 https://nationalmortgageprofessional.com/news/74667/lump-repayment-required-loans-forbearance Seems there are multiple options for repayment available to confirming mortgages and lump sum payment is not being required. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

Seems like Calabria and Mnuchin are on the same page regarding servicers. (Bloomberg) --Treasury Secretary Steven Mnuchin said the U.S. has no current plans to create a Federal Reserve facility to inject funding into non-bank mortgage servicers, as recent government moves will help the firms get through the risk of millions of borrowers missing their mortgage payments. Mnuchin pointed to Ginnie Mae’s decision last month to facilitate payments to mortgage bondholders themselves, thus covering an obligation that would have fallen on servicers. That combined with steps taken this week by the Federal Housing Finance Agency, which regulates mortgage giants Fannie Mae and Freddie Mac, will “deal with liquidity concerns,” he said in a Bloomberg News interview on Thursday. “We’re not looking at a Fed facility for this at this time,” Mnuchin said. “The moves that both regulators have just taken are more than sufficient to create liquidity.” The Treasury Secretary and other government officials have been under pressure to bail out servicers, companies that collect monthly payments from borrowers and then funnel money to investors in securities made up of home loans. The firms are still obligated to pay bondholders even if homeowners go into forbearance, prompting the industry to argue that thinly-capitalized nonbank servicers could go under if swaths of borrowers stop paying. Mortgage lenders have argued that such a scenario could trigger the collapse of the U.S. housing market. Despite that concern, Mnuchin said the firms do not pose a systemic risk to the financial system. The FHFA tried to ease strains on servicers Wednesday by announcing that it would allow Fannie and Freddie to buy new loans that have just entered forbearance. It also said that servicers handling Fannie-backed loans would only have to facilitate borrowers’ missed payments to bond investors for four months, bringing it in-line with Freddie. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

Layton also fails to recognize the big bang moment for GSEs isnt a "BIG IPO" but actually the 4th amendment which shouldnt be delayed more than a few months at best (unless lockdown situation gets much worse). -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

According to T. Howard, FNMA was already on the hook after 3-4 months (we know FMCC was after 4 months), so i'm not sure how this policy diverges from that. jtimothyhoward MARCH 24, 2020 AT 10:25 AM "... A former Fannie Mae colleague wrote to remind me that under most of Fannie’s servicing arrangements servicers ARE required to advance the first 3 or 4 months’ missed payments, although they then are reimbursed for those advances so that Fannie ultimately bears the cost." jtimothyhoward MARCH 26, 2020 AT 12:46 PM "The problem for servicers is that even though they ultimately get reimbursed for the monthly payments they are required to advance for 3 to 4 months on Fannie or Freddie-guaranteed MBS, many likely will have neither the capital nor the liquidity to be able to make these advances in the volumes that may be required." -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

Keep in mind that prior to today's FHFA press release, the GSEs were ALREADY on the hook for making the MBS payments after 4 months. Calabria even highlighted this in the press release, "Today's instruction establishes a four-month advance obligation limit for Fannie Mae scheduled servicing for loans and servicers which is consistent with the current policy at Freddie Mac." I know Tim Howard was saying 3-4 months as well a few weeks back. Servicers were never on the hook past 4 months to begin with. It seems like this is an "optical" win for MBS at best, but what did they actually get out of this that was different before today? In reality no policy was actually changed other than Calabria reiterating the GSEs responsibilities after 4 months. GSEs also bot themselves 6-12 months (depending on length of forbearance) by keeping the forbearance loans in the GSEs MBS pool. At the end of the 6-12 months we will know how much % of the forbearance loans translates to default events and thats the only time the GSEs will really start to take some losses. Keep in mind the average LTV @ FNMA is 57% and FMCC is 60%. Home prices would have to sharply correct by >20%+ before home owners start getting wiped out / defaulting. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

The article reads stale / like a rehash of the original article that said everyone was waiting for FHFA to signoff and Calabria surprisingly put his foot down. I imagine this headline is just referencing that event. Calabrias approval (which has been pending for 2-3 weeks now?) won't come bc he already decided on what is his duties as conservator are. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

I think we would all love (unless you own common) for the Treasury to write a $125b check to the GSEs and simply convert their senior pfds to common, bypass an IPO all together, and slowly do secondary offerings on their snr pfd common + warrant stake over the coming years. It just seems a much more palatable solution is to write down the senior pfds to zero, and give the GSEs a "future tax (or commitment fee) credit" of ~$30b that can be deemed capital for balance sheet purposes. Zero $ out of pocket. Regardless of how much money the government is dishing out right now, I would think writing a $125b cash check would be difficult in any environment (vs the alternative of zero $ outflow). But I hope you turn out correct! -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

Dream case hypothetical- Calabria: "I am happy to help the servicers, but i need capital in order to do so. How about we write down the snr pfds and give the GSEs a tax credit for the overpayment of $25-$30b, that gets the GSEs to ~$50b of combined capital to start." This is what ACG was alluding to on their recent call. Admin definitely has cover to pull this off (saving housing market), and I imagine this compromise works for MBA (historically anti-recap) as they will get their liquidity wish for servicers. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

"But i think at the end of the day if we're through the worst of the virus in the next, another 6 to 8 weeks, then i think we still see a large equity raise by the enterprises in 2021." Also mentioned there are a number of things they need to put in place prior to that (i'm assuming that includes the capital rule and PSPA amendment) -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

https://www.cnbc.com/video/2020/04/01/fhfa-director-approximately-700000-mortgage-loans-could-need-forbearance.html -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

Calabria was on CNBC this morning. Will post clip when link is available. On exiting conservatorship: "Modest delay in my opinion" ... "could put off exit by a couple of months" , still see's initial equity raise by 2021, fannie and freddie need to be strengthened. He also reiterated that that he expects the take rate on the GSEs forbearance program by May to be 3-5% (currently seeing 1-2%) so doesnt expect much stress yet, can handle 2-3 months if people start going back to work after a few months, if lasts 6+ months and people stillunemployed and 25-30% take rate it will see stress the system. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

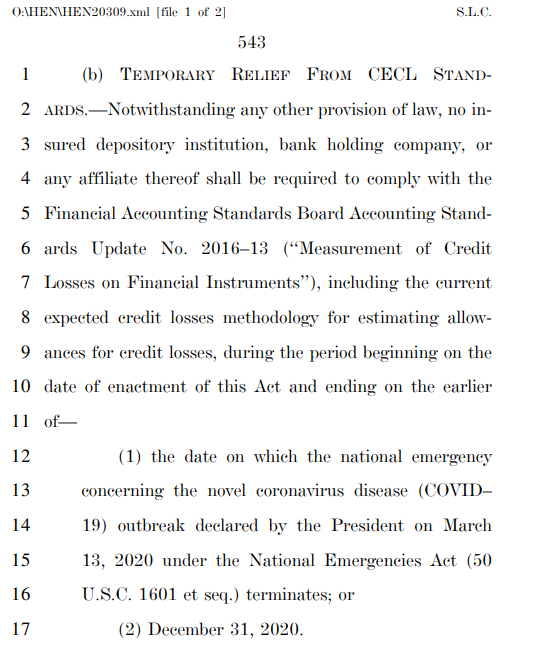

1) The CARES act delayed CECL until end of the crisis at the very least (or end of year, whatever comes first), FHFA still hasnt delayed it for 2 years like banks (TBD). 2) Mortgage servicers only have to front 3-4 months worth of payments I believe, then GSEs are on the hook after that, which they can borrow at close to 0% rates to pay the MBS investors like TH pointed out so non-issue until those loans turn delinquent. I have been thinking about GSE loss reserve creation over the next couple of Qs. first, a big benefit is CECL "mitigation" (an overused term) for 2 years. big plus for B/S optics. second, how much of the "forbearance" amounts are reserved against? ie do the GSEs simply assume that the forbearance amount will be paid and the deferral is simply a restructuring of the mortgage terms, so no loss reserve creation? rolg asked Tim Howard this and his reply was essentially a question of conservatism/judgment. there is a big difference imo between nonpayment due to by a federally mandated forbearance, and an obligor's default in payment. while GSEs do have to make payments to mbs pools in place of mortgagor payments, these are borrowed at extremely low interest rate cost, so not a big delta arising from that The FhFa hasn't yet delayed cecl for the GSEs, unless I missed something. Also are you sure about your last sentence? Do the GSEs have to pay before they are delinquent? Aren't the mortgage servicers at risk here, and why they are asking for the [100?]bn facility? -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

From a sell-side note today. "Forbearance kicking the credit loss can down the road? The forbearance program announced by the FHFA essentially would allow the GSEs to defer the recognition of losses on mortgages guaranteed by the GSEs for the next 12 months if the borrowers can verbally confirm financial hardship or health-related impacts. We believe this program could significantly reduce the near-term loss recognition across all agency-backed mortgages, including potential losses on credit-risk transfer (CRT) investments that are widely owned by hybrid mortgage REITs facing significant MTM risk." -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

CECL delay included in bill. see attached. Lets hope for a quick recovery then, will probably depend heavily on when economy gets opened back up. Getting them out by 2021, 2022 was always the plan from a 100% out of conservatorship standpoint if the ACG timeline was to be believed. From a preferred stand point as Midas mentioned what really is needed is a PSAP amendment to get rid of the Srs. Even if the economy stresses FnF I think that should still be on the table and the legal story continues as well. Realistically capital cant be raised until early 2021 so out of conservatorship in 2021 maybe even a stretch, but by then Preferred should have been dealt with or their fate should be determined. the big issue for GSEs will be CECL accounting adoption. that will give rise to large credit reserves being established. anyone know if the bill delays CECL?

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

From Bloomberg: *CALABRIA: CRISIS DOESN'T YET AFFECT FANNIE-FREDDIE TIMELINE *CALABRIA: GSES WILL BE STRESSED IF CRISIS EXCEEDS TWO MONTHS He also mentioned he still expects to get them out by 2021, 2022 (im assuming this means the IPO but was pretty vague this time around). -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

allnatural replied to twacowfca's topic in General Discussion

I imagine anything that removes snr pfds from cap structure would result in extremely bullish action for jr pfds which turn to snr. Anyone else think the GSEs are going to profit handsomely on providing liquidity today as they are increasing the size of their internal portfolio at record wide spreads which should revert back once (if) this all cools down over next 3-6 months? They could theoretically be buying the lows right now. I wonder how prefs would trade in that scenario given the current market and many other equities depressed in price.