allnatural

-

Posts

374 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Posts posted by allnatural

-

-

That's the opinion yes. Not sure if fairholme argued for direct as well but their focus for now seems to be on the derivative claims where remedy could lead to write down of senior pfds.

-

9 minutes ago, MrSwankyPants said:

I'm so confused after listening to this. Can someone refresh me what case this is and where it's on appeal from? Too many cases, too many judges...I'm loosing track!

The appeal is from the court of federal claims. Shareholders are claiming that the NWS was violation of the 5th amendment for the taking of private property for public use without just compensation (the recent Collins decision affirmed the the NWS action by the FHFA is a government action taken for public benefit). Even if the NWS was allowed under HERA (like Collins ruled), you still have to give compensation for the takings. The original ruling by Judge Sweeney allowed the derivative claims to move forward and dismissed the direct claims. This oral argument was related to the appeal of both of those decisions. Should have a decision in the next 6 months. If shareholders survive the derivative claims we will move to trial.

-

1 hour ago, TwoCitiesCapital said:

Thanks for posting. Not an expert myself in these legal arguments/analysis, but certainly sounded like the judges were VERY skeptical of the gov'ts framing and POV and less so of Fairholme's lawyers.

Would also add that Fairholmes lawyers just sounded more impressive because they spoke with confidence and didn't stumble all over themselves like the govt's guy was doing. Not that it ultimately matters, but perceptions like that can sway lesser people - maybe it can sway a judge.

Keep in mind the only claims we want surviving is Fairholme's derivative claims (where the remedy would flow to the GSEs aka existing shareholders) vs all the other shareholders lawyers were arguing for direct claims (where the remedy would flow to shareholders who owned stock on day of NWS).

The judges were very harsh re: direct claims (i think these all get dismissed / affirm Sweeney's ruling), but when it was the governments turn to speak they were tough on the lawyer re: derivative claim as they didn't seem to bite that there wasn't a conflict of interest if only the FHFA could ever sue the FHFA re: derivative claims.

Of the 4 derivative claims being argued for, based off oral arguments today, I think the judges will reverse and dismiss all but the first one.

• Just Compensation Under the Fifth Amendment for the Taking of Private Property for Public Use

• Illegal Exaction Under the Fifth Amendment

• Breach of Fiduciary Duty

• Breach of Implied-in-Fact Contract Between the United States and the Companies

-

Don't see any new language/commentary re: exiting conservatorship (or not).

-

-

If anyone managed to pick the bottom this week (I was not), they would already be up ~30% in a few days time for FNMAS/FMCKJ. Not bad for dead money.

-

-

18 hours ago, Wiggins said:

thank you this is an excellent resource

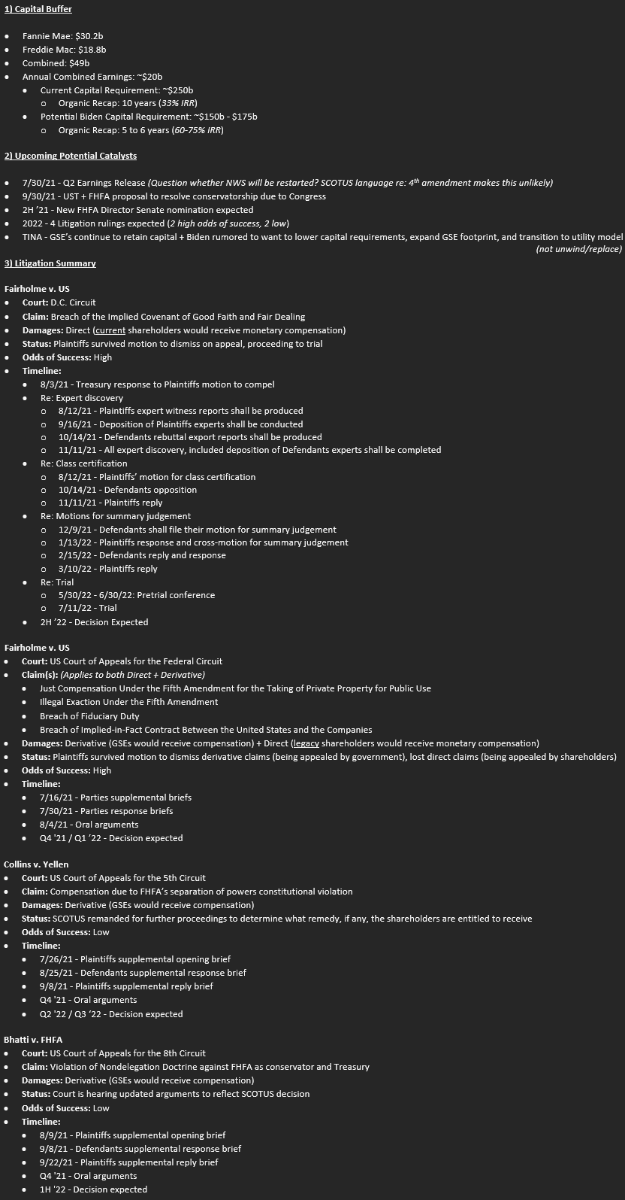

Updated w/ more details + some personal commentary

-

Some upcoming catalysts/events to keep an eye out over the next year including litigation timeline:

-

20 hours ago, orthopa said:

Im no lawyer so Im happy to have other opinions but the most recent SCOTUS was a statutory ruling. They plainly interpreted HERA. Lamberth agreed already that the APA avenue was a no go but other claims are proceeding. Can SCOTUS rule HERA says FHFA can do what is best for itself but not honor a contract? Can FHFA do what it wants but still have to pay for property taken? I guess we will see if we get that far.

FWIW both Lambert and Sweeney ruled in favor of shareholders while explicitly saying that the government didn't violate the APA (agreeing w/ SCOTUS) re: the NWS but that doesn't help them in the contractual or takings context.

-

https://www.politico.com/news/2021/07/05/biden-housing-dilemma-low-income-497921

“Top Democrats are calling on Biden to quickly name a permanent leader — a position that Senate Banking Chair Sherrod Brown's spokesperson said is “vital to the administration’s goals of building an equitable economy and must be filled quickly.”

“Our housing finance system remains in urgent need of reform,” said Sen. Pat Toomey of Pennsylvania, the top Republican on the Senate Banking Committee. “I look forward to working with the next FHFA director to enact legislation that finally addresses the flaws in the structure of the housing finance system, ends the conservatorships, and protects taxpayers against future bailouts.”

“Van Tol is already trying to warn the administration against nominating two prominent housing experts — Mark Zandi, chief economist of Moody’s Analytics, and Jim Parrott, a former Obama White House economic adviser. He objects to their support for earlier housing finance reform proposals that envisioned revoking Fannie and Freddie’s government charters, voiding their affordable-housing obligations as a result. ... “I’d be very disappointed if the administration tapped someone who was wedded to the failed ideas of the past,” Van Tol said.”

-

It seems like your concern is addressed in Section A of page 26 "HERA does not require dismissal of Plaintiffs' implied covenant claims" that even if shareholders should have expected the government via HERA/FHFA to act in its own best interest, shareholders contract breach takes place in the fact that the GSEs themselves (whom PFD shareholders are contracted with) breached our contracts as they accepted these terms in exchange for nothing.

-

5 hours ago, Sunrider said:

The way I read it is that the rights travel with the securities, but not necessarily what should be deemed 'fair' and 'reasonable expectations' ... i.e. those might be different for those who bought prior to NWS and those who bought after ... in other words, no question that prefs have liquidation preference, etc., but whether a shareholder who bought post NWS could've reasonably expected that the liquidation preference is worth >0 is a question he left open.

if you read that differently, could you please point to where Lambeth addresses the point in the way you interpret it?

Thank you.

Christian

This is a direct quote from David Thompson after the ruling was released:

"... And a couple of things are significant on page 17 of Judge Lamberth's ruling he holds that the claims travel with the security. That's a point we had briefed. The Delaware law is uniform on that point saying that is what happens but still, there had been a gray area there so that was important that current holders owned these claims not people who owned it before..."

-

1 hour ago, Sunrider said:

Well, sadly, 10 years later, we now should update the title of this thread to '15 or 16 baggers', which is what some of the prefs now trade at. This one hurt.

I've re-read the delawarebay paper, and the Lamberth opinion ... main worry is

(a) question about whether not only the rights to liquidation preference and dividends travel with the shares but also the expectation of fair dealing (as plaintiffs will be able to show that GSEs were about to be profitable and as a matter of record did not receive anything new in return for the NSW). -> My brain has trouble thinking of how this might practically work if they were divorced, but then again it seems that judges have now split hairs so fine they could circumcise a mosquito.

(b) Sweeney seemed to be balanced and didn't take too much of the government's BS ... not clear what to make of the new judge ... and there seems to be a leaning towards the government once these guys are in the seat, irrespective of what their views were previously.

(c) whether this admin is genuinely interested in getting the GSEs off the government's books (so to speak). If so, then they will work towards recap. If not, they may simply want to speculate that the next crisis requiring a bailout may be a problem for the next guy/girl in the role.

I am tempted to average down, but I am aware that I may just be blinded by commitment bias and the (so far) stupid belief that the land of liberty will eventually conclude that if this all stands, property rights don't matter, and will therefore correct this. Perhaps that is pure naiveté.

On the other hand, one should evaluate investments based on what they offer today. FNMAH at 1.68 is about 1:15. The fact that the total investment IRR after such a long time would be pedestrian doesn't matter, it's a sunk cost. Giving it 3 more years and making 15x does look attractive compared to everything else, but I am genuinely wondering whether this is the right mental model for such a binary situation.

Input welcome.

All valid points / concerns. Re claims traveling in the Lamberth case, he ruled that they indeed do travel.

-

28 minutes ago, orthopa said:

Do you have readily accesible links to that lamberth stuff? Is it just in the court filings? Not sure I read that before.

https://www.govinfo.gov/content/pkg/USCOURTS-dcd-1_13-cv-01053/pdf/USCOURTS-dcd-1_13-cv-01053-1.pdf

See page 14 section B for the relevant section. The government tried to file for a motion for rehearing after this decision came out which Lamberth promptly rejected as well. Section A of page 26 explains that even with todays confirmation from SCOTUS that HERA allows FHFA to act in its own best interest (the "death knell" in the SCOTUS APA claim), shareholders still win.

-

Tough day for shareholders / rule of law. What value is left if any is left in the preferred shares?

1) Biden Admin optionality: Word is that the Biden admin is against the high capital requirements and footprint shrinking set by Calabria. Why do capital requirements even matter if they are stuck in perpetual conservatorship? Biden will shortly nominate a replacement and that replacement will share his views on the future of housing finance reform (could be bullish or more of the same aka nothing).

2) SCOTUS remand for relief: Based off the ruling today, very low likelihood shareholders see any relief here.

3) Lambert/contracts case: Probably shareholders best shot at short-term relief in litigation. Set for trial in ~9 months from today. Lamberth already ruled in favor of shareholders that the government allegedly violated our contractual rights with the NWS (whether the NWS is legal or not is irrelevant to his analysis). The crux of his ruling was that no shareholder could have ever expected at a time when the GSEs were about to hit record profitability, for the government to come in and to arrange the contracts so they take everything for themselves while zeroing out the shareholders in exchange for NOTHING. He then went on to list all the facts to support this view. Damages/relief would potentially entail PAR+ interest in damages in the form of a direct monetary check to shareholders.

4) Takings case: Another good shot on goal but I think its at least 1-2 years away.

5) TINA: As always, GSEs are more stable / reformed than ever before and have ~$40-50b of retained capital on their books. I don't think unwind/replace is a real risk here but being stuck in limbo may be. TINA provides shareholders a perpetual call option either way.

Add it all up and you get ~10% of PAR for FNMAS.

-

-

3 SCOTUS rulings today, all from 2020. Only 1 remains from 2020 (Collins)... tick tock

-

40 minutes ago, Castanza said:

So the Collins case is delayed 45 days to see what SCOTUS rules? Are we expecting a ruling before 45 days? Or is this a minimum before another extension needs to be filed?

You mean the Lamberth trial is delayed 45 days. Expecting Collins ruling by the end of the month (possibly tomorrow).

-

17 hours ago, TwoCitiesCapital said:

If no Opinions are scheduled for May/June, does that mean this is dead in the water for at least another two months? Or does the calendar get updated with some frequency to suggest we might have a response sooner?

The calendar gets updated week of, to announce opinion dates. So expect no opinions this week, but nothing to read into for rest of May. June 30th is latest (57 days remaining and counting).

-

Collins APA = Derivative

Collins Constitutional = Derivative

Court of Federal Claims Takings = Derivative

Lamberth Contractual Claims = Direct

-

??? "Mnuchin said that case and other issues must be resolved before Fannie and Freddie could raise capital in private markets,"

-

Re: Collins you have it backwards. There are 2 scenarios here:

1) Collins case is dropped (as a result of PSPA amendment and/or settlement). Calabria's job would be safe until this issue is re-litigated by Biden back to SCOTUS (probably sometime in 2022 as it would have to make its way through the DC circuit first).

2) Collins case isn't dropped (no PSPA/settlement). Calabria will be removable by Biden as soon as the Collins ruling is released (May-June).

As you can see the Admin and Calabria have a large incentive to get rid of the Collins case during the lame duck. Regardless, the earliest Calabria gets removed is May/June, and potentially into 2022 if the Collins case goes away shortly (by giving shareholders the remedy they desire via a PSPA amendment).

They waited until the last possible day for the letter agreement. January is likely the decision point on whether a 4th amendment occurs.

From commentary on this board it appears the Collins case probably needs to go ahead on Dec 9 to avoid a quick firing of Calabria at will soon after Biden's inauguration.

-

Doubtful because if shareholders win the APA claim in SCOTUS, it would be because the judges ruled that NWS violated HERA as it didnt follow the duties of a conservator. A potential 4th amendment does follow HERA as it would be trying to restore the GSEs to safety and soundness (the opposite of the NWS).

I got that same feeling. Trying to set the narrative of exactly that

right. Ackerman is too much of a tool not to be used as a tool by C/Mn.

the collins reply brief was due 11/23, filed 11/19. you almost never see an early filing. https://www.supremecourt.gov/DocketPDF/19/19-422/161278/20201119155421721_11-19-20%20Collins%20Merits%20Reply.pdf

The article was certainly a trial ballon. This has been telegraphed for essentially years now so not sure why the MBS market would be suprised by this. I dont have access to an instrument to tell by pricing or otherwise if they were or will be "surpised" but I doubt that to be the case. Apparently Sherrod Brown has come out and said he thinks Mnuchin is the worst Treasury Secretary of all time so he wont lose any friends there by doing the PSPA.

Calabria has said that the lawsuits go away with the 4 PSPA and with the timing here that very likely maybe the case. For optics there may not be a "settlement" as much as plaintiffs drop the case no? It would be in their best interest depending what's in the 4th PSPA to preserve Calabria for as long as possible and let his removal play out through the legal system.

Someone please tell me if Im off on this but once there is a 4th PSPA within 30 days FHFA should request recap plan. FnF then have 45 days to respond and in turn FHFA has 60 days to approve. So we are looking out no further then 4.5 months from the PSPA amendment to know the final fate of the Jr Preferred. Hopefully sooner as one has to imagine JPM and MS have been sitting on plans for months and just tweaked it Wednesday night.

Worst case by middle of Q2 2021 we should finally know our fate.

there may very well be some kabuki theater with this process, no settlement (for optics) but T going to scotus and saying collins is moot because 4th A...and if it is to be moot, Ps need to get everything they are asking for...or maybe there is some backchanneling so that Ps will agree case is moot if 4th A does X, but there won't be a formal settlement agreement with Ps. once a 4thA is agreed to by fhfa and T, then yes fhfa can immediately ask for CRPs, which can be a part of a consent decree.

If the SCOTUS case is not ended, one way or the other, and it is decided that the 3rd amendment needs to be overturned, can someone hostile to GSE recap come along and use the exact same legal arguments to overturn a 4th amendment?

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

in General Discussion

Posted · Edited by allnatural

Lamberth is my favorite case as well (and much closer to ultimate resolution than the takings case).. Although i'm very curious to see how the Collins remand plays out based off the last briefing (especially since its back in the en banc hands with all 16 judges who have shown willingness to rule for shareholders already).