mattee2264

-

Posts

786 -

Joined

-

Last visited

-

Days Won

7

Content Type

Profiles

Forums

Events

Everything posted by mattee2264

-

Funny that the Fed Put has morphed into the Fed Call. Markets close to ATHs and Powell comes out and congratulates himself on beating inflation and says rate cuts are now on the table and don't worry guys inflation will be back on target in 2026.

-

Fed has just confirmed with their dot plot that they expect three rate cuts in 2024. And Powell also said that a recession is not necessary to start cutting rates. Market got it exactly right that Powell was just posturing to try and restore what little credibility the Fed has. Now it is election year he will give markets and the US government what they want.

-

Something fishy about the Fed signalling rate cuts during an election year when core PCE is still twice the target rate. Wasn't it just two weeks ago that Powell told the market not to speculate about rate cuts. Then lo and behold the Fed confirm that rate cuts are now on the table. Irony is that by promising rate cuts within the next year that is going to discourage consumer and investment spending because why borrow now when you can borrow a year later at much cheaper rates?

-

I think it depends on how much resolve the Fed has to get inflation back to 2%. They are using the lag factor as an excuse to pause. And jaw boning about how their stance is restrictive. But if they were less political they would admit that the massive fiscal deficits are completely dominating the impact of rate increases and most of the decreases in inflation to date have very little to do with them and more to do with supply chain issues easing, commodity prices falling, and companies reaching the limits of their ability to price gouge consumers. They are also ignoring the massive loosening of financial conditions as a result of the market recovering most of its 2022 losses and long term bond yields sliding. It would also not surprise me at all if the economic data that the Fed is "dependent" on is very manipulated. It is a typical trick. Report strong headline data. Then in later quarters quietly revise it downwards. Some evidence of that already in the jobs data. And there is a massive divergence between GDP and GDI. So with all this smoke and mirrors it is difficult to tell how strong and resilient the economy really is. And that seems to be the basis for the soft landing optimism. The economy has been strong and resilient avoiding recession in spite of an aggressive tightening cycle. Inflation has pretty much fallen in a straight line and is heading back to target. And non-inflationary growth will allow the Fed to cut rates. So you end up with a Goldilocks scenario in which 2024 EPS will be higher and 2024 interest rates will be lower. And AI optimism is an added kicker. So little wonder you are getting SPY 5000 and even SPY 6000 market calls.

-

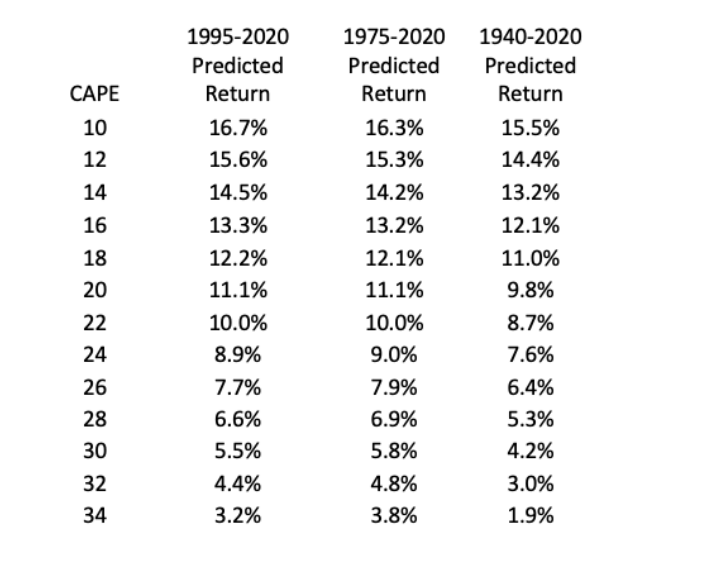

Shiller PE is being distorted by Mag7 because if you apply a 10 year earnings average to high growth stocks it is always going to result in a very high number. The same kind of thing happened in the late 90s when the Shiller PE topped out above 40. And all the Shiller PE is supposed to do is predict 10 year returns. If history is a guide then with the Shiller PE around 30 you can expect 10 year returns of around 5-6% per annum. That is still better than you can get on a long bond. The table below is quite instructive. But it is also a bit deceptive. Because it shows returns from your starting point. It doesn't show the dilution in returns from selling at some earlier point and sitting out of the market for several years waiting for the predicted return to increase.

-

Above is a very valid point. You can improve near term results by cutting costs, capex, research spend etc. But the risk is that by doing so you will fall behind and in a winner takes all dynamic that is a risk you cannot afford to take so it makes business sense to err on the side of overinvestment and overstaffing and make sure staff are paid enough that they aren't tempted to jump ship and join a competitor.

-

Lying requires the ability to distinguish truths from falsehoods and deliberately choose the falsehood. AI is not capable of that. What it is capable of which makes it unreliable and dangerous is making incorrect statements with a lot of conviction. And as anyone with a basic grounding of human psychology will understand that when someone sounds very confident when giving a response they are often believed. In fact politicians make a career out of that ability. AI also has a massive halo effect so people will probably find out the hard way that it is not always reliable and has major limitations.

-

It is tough really. Most value investing theory is based on reversion to the mean. As Graham loved to quote ""Many shall be restored that are now fallen, and many shall fall that are now in honour". There are also a lot of outdated academic studies showing that buying glamour stocks is a losing proposition so there is a natural reaction to shun popular stocks that everyone seems to own. But with more and more of consumer and business wallet share going towards e-commerce/digital advertising/cloud/AI those are tailwinds that are very favourable for Big Tech and very unfavourable for everyone else. And therefore anyone without at least a market weight in Big Tech risks getting left behind. Especially if AI lives up to the hype and extends their growth runway another decade. Valuation risk is clearly higher than previous years. You are paying about double the market multiple. On the other hand mega caps traded at much higher multiples at the heydays of the Nifty Fifty and dot com bubbles. Competitive risk is possibly lower than previous episodes because most of them have incredibly strong moats and each technological advance seems to reinforce them with AI likely to be no different at least in terms of its current limited possible applications. Tesla and Nvidia have technological leads which historically are difficult to maintain but in the meantime they can build their mind share so even when viable alternatives arrive people may still go with Tesla and Nvidia. Probably the greatest competitive risk is that as their markets overlap more and more competition between themselves intensifies driving down margins and returns. But historically with new technologies especially those that can capture the imagination the way AI can then there is a risk of new competition from upstarts who have little trouble attracting money from venture capitalists and the speculative public. And long dominance and technological leadership didn't save IBM, Intel or Polaroid from being disrupted by emergent technologies. Execution risk is there especially with AI requiring huge investments with uncertain returns. But in general their core businesses are well managed. Cyclical risk is probably underestimated. They haven't been tested by a proper recession. The COVID episode was brief and it soon became clear they were major beneficiaries. But historically advertising, semiconductors, consumer goods, cars, even IT have not been immune to the economic cycle. And until AI hype took over investors were most unkind to the contrast between 2021 and 2022 results the latter weighed down by inflation and a slowing economy. But so long as the US government continues to spend trillions and companies are reluctant to fire staff the US can probably avoid a severe recession. And bizarrely if economic growth did strengthen and was accompanied by higher interest rates it might encourage a rotation out of tech and into more cyclical/value names. So to some extent Big Tech do rely on a goldilocks not too hot not too cold economy. They did badly in the fire stage and might do equally badly in the ice stage. Regulatory risk is hard to call. Regulation has been pretty soft and done little to prevent acquisitions that have enhanced tech dominance. But it is not unforeseeable that regulators would want to put roadblocks in the way of AI advancements. Geopolitical risks might also exist if they make it difficult for global domination to persist and makes it more difficult for them to operate in certain markets. And probably some other risks that haven't occurred to me.

-

https://futurism.com/economist-ai-doomed-bubble Article above pours a bit of cold water on some of the hype. Basic criticism is that LLMs learned to write before they learned how to think and while they can string words together in convincing ways they have no idea what the words mean and are unable to use common sense, wisdom or logical reasoning to distinguish truth from falsehood. And as a result they are unreliable. And dangerously so because they are programmed to sound so confident and convincing. In another essay Smith and Funk recall the "Eliza effect" a 1960s computer program that caricatured a psychiatrist and convinced many users that the program had human-like intelligence and emotions. And we are vulnerable to this illusion because of our inclination to anthropomorphize. So in many ways Chat GPT and the like are just another example of pseudo intelligence. It reminds me a little of well of the way that parents have a tendency to extrapolate thinking just because their kid does something semi-intelligent he will grow up to be a genius. In the same way the argument seems to be "Well it is 2023 and already these AI models can write college-grade essays and do high school math. So by the end of the decade AI will be capable of doing most jobs better than humans with unimaginable productivity benefits" But the history of AI shows that what tends to happen is that a brick wall is reached and then there is an AI winter that can span decades. And the scary thing is that because of FOMO Big Tech companies not to mention all the VC funds and so on are going to invest billions and billions with very uncertain returns. Perhaps they will make money out of it at least in the early days because if enough consumers and companies believe in AI they will want to buy the AI products even if they aren't really that game-changing and prove to be unreliable. And the illusion is very strong. But the problem with fads is that while you might buy a fad product once, you aren't likely to be a repeat buyer, and to justify the massive investment it needs to become a recurring revenue stream.

-

Amazing really especially when you compare to the sums spent during the GFC. Fiscal policy also operates with some lags so I think the cumulative spend since the pandemic has played a massive role in keeping the US economy from falling back into recession and has clearly dominated the impact of monetary policy tightening except for very interest rate sensitive sectors. Obviously becoming less productive as even without a decrease in spending more of the spending will go on interest payments rather than handouts. Long term also pretty scary especially as if AI fulfils its promise there is going to be a massive amount of structural unemployment and global corporations are a lot harder to tax than individuals.

-

Trust is probably going to be a big deal. Especially for businesses who are going to place a lot of reliance on the output of AI applications. And Big Tech are going to want to include in their ecosystem and integrate with their other service offerings to increase the likelihood you'd pick their product. Where markets could have got it very wrong is overestimating the short term revenue opportunity. Especially when you consider how massive revenues of Mag7 companies already are. And that to some extent that AI market is going to be shared between them and possibly some start ups as well as if AI becomes very bubbly everyone and anyone will be able to secure funding.

-

I'm inclined to stay in short term bonds. While inflation will probably continue to come down I would expect the yield curve to steepen especially as concerns over US government debt begin to build.

-

Companies only cut prices if they think that failing to do so is going to mean unsold inventory. So while good for inflation, bad for corporate profits and employment.

-

Mag7 does seem like the no-brainer way to play the AI revolution. Deep pockets, cashflows from core businesses to invest in research and hiring the best human capital, existing capabilities in things like machine learning, automation, coding and so on. And with antitrust laws so weak they can buy out any emergent competitors. It reminds me a little of cloud. With the benefit of foresight an investor would have realised that cloud was a fantastic money maker that companies like Amazon, Google and Microsoft were well placed to exploit. And at the time these companies were under-priced because the potential of cloud was not reflected in their price. As a counter example though historically incumbent firms such as IBM at the dawn of the PC age and Microsoft in the Internet Age had deep pockets but new firms emerged and captured a lot of the value creation. And to some degree new technologies involved some creative destruction cannibalising to some extent the old technologies. And clearly AI prospects are to some extent priced in with Nvidia an extreme example and probably to justify Tesla's crazy valuation you are also betting they make a lot of money through AI rather than selling cars. But then again in the Dot Com Bubble mega-caps got up to 60-70-80x earnings or more. And so if the AI bubble really takes off then Mag7 could easily quintuple over the next 5-10 years. So Mag 7 doubling YTD coming off a severe tech bear market is nothing and if AI can fulfil its early promise and Mag7 are the winners then still a lot of money to be made. The issues I see are that: a) AI is going to require a lot of investment. Returns could be quite far in the future. And there might be an incentive to prioritise short term commercial applications that are more incremental than transformative in nature. And while that would reduce the investment required it would also reduce the value creation. And because core businesses are so profitable and capital light if the economics are inferior that is going to show up in the numbers and disappoint investors. b) Establishing a moat in a new technology takes time so there is vulnerability to creative destruction and while deep pockets give an advantage it does not guarantee success. After all most of the Mag 7 emerged from nowhere and most of the mega-cap techs of the dot com boom are either gone or are insignificant players. Even within the Mag7 there will be winners and losers as they are competing with each other. c) AI is going to be something that governments are going to want to regulate. It is a threat to jobs which can disrupt the social order and put pressure on government budgets. It can also lead to the spread of disinformation. Currently attempts to regulate Big Tech have been pretty pathetic. But AI is going to increase incentives to do so.

-

Cost of living crisis is starting to ease. I'm also seeing grocery prices starting to fall. And energy prices have fallen as well. Even rents are starting to come down a little. So this is a positive. Although some of the additional funds available will be used to replenish savings or pay down credit card bills and other debt. And to the extent that consumers did take on additional debt to survive the cost of living crisis they will need to service that debt at still very high interest rates. And spending power might also come down because consumers have probably exhausted by now any excess savings built up over the pandemic so are limited to what is available from their income after taxes, debt service etc. We are at full employment and there are some indicators that labour markets are starting to weaken and that is going to have a negative impact on consumer spending. And most recent real consumer spending growth was 2.4% which is going to be a hard comparative figure to match. And in nominal terms with inflation coming down as well nominal spending growth will almost certainly be lower and that will have a negative impact on nominal corporate earnings. Although agree that absent a massive increase in unemployment it is difficult to imagine consumer spending falling off a cliff and that increases the chances of a soft landing. Agree that multi-trillion dollar deficits are also going to be very supportive to the economy. It is a very underestimated factor and probably explains a lot of the comparative strength of the US economy compared to the ROW. And in an election year they are going to continue. Not so convinced about cost cuts. Over the last year or two cost cutting supported earnings growth even as revenue growth softened. But as most of the easy efficiencies have probably been achieved by now further cost cuts will be more difficult and may require reductions in headcount which is a negative factor for the overall economy and therefore corporate earnings generally. And again comparatives will be tough because in 2022 and 2023 earnings benefited from cost cuts and revenues held up better than expected because the economy avoided recession. If there is some kind of soft landing next year it will mean even weaker revenue growth and absent major cost cuts that is going to mean much lower earnings growth than in previous years and we have all seen that the stock market punishes that harshly.

-

Central banks have always been terrified of deflation. That is why you have a 2% target and not a 0% target. So yeah if we undershoot the inflation target rates will quickly come down. I cannot imagine the Fed blithely saying "Oh the deflation is transitory so we will wait and see what happens". Other thing that probably isn't generally realised is that both fiscal and monetary policy operate with lags. So today's rapidly disappearing inflation was caused by yesterday's stimulus. And today's contractionary monetary policy and less effective fiscal policy (no longer giving direct stimmies) could be tomorrow's deflation. Deflation clearly isn't good at all for government and private sector debt even if it does make it cheaper to service. I also think that data will get revised and indicate that the economy isn't as healthy as recent figures suggest and while the Fed is still worrying about inflation the market has probably correctly realised that interest rates are heading lower but perhaps will be taken by surprise if we do fall into a recession that is deeper and longer than expected.

-

Might be worth resurrecting this thread given that WMT made a point of using the "D" word and there are some signs of emerging weakness in US labour markets as well and the full impact of monetary policy is also likely to be felt in the coming months and already we are starting to see rising credit card delinquencies and defaults and bankruptcies. And a lot of inflation was driven by food and energy prices which are falling. Already in groceries I am starting to see lower food prices. There will be a lot of discounting in the holiday season as well. Rents are also starting to fall. And it is pretty clear that a lot of companies were quite opportunistic in putting through large price increases and got away with it because the economy held up pretty well and labour markets were tight and consumers had a lot of excess savings from the pandemic and it takes time to change your spending habits. If sales start to fall they will come under pressure to reduce prices. Deflation is still very unusual and there are still inflationary pressures in the economy coming from fiscal profligacy and union wage bargaining and resource shortages. But these are unusual times and a deflationary bust probably has some probability higher than zero. Thoughts?

-

An index that tracks SP500 minus the Mag7

mattee2264 replied to rogermunibond's topic in General Discussion

Everything going back 5, 10, 15 years is going to underperform a market cap weighting because we are still in a long secular bull market led by Big Tech and to a lesser extent quality stocks (aka bond proxies). Value stocks tend to be more economically sensitive and economic growth has been anaemic and with tech eating the world there has also been a lot of creative destruction with the new economy benefiting at the expense of the old economy. Chart below is quite interesting. Suggests that an equal weighted S&P 500 index tends to outperform early cycle and market cap weighted S&P 500 tends to outperform late cycle. But not particularly useful as economic uncertainty has been incredibly high post pandemic. And Mag7 are still seen as all weather stocks by most. Higher for longer? In a speculative market investors will still turn their nose up at a 5% guaranteed return. And Mag7 have pricing power so moderate inflation and moderate economic growth supports double digit nominal earnings growth that investors have come to expect. Soft landing? If we return to a low inflation low economic growth low interest rate environment then we've already seen that massively favours secular growers. Hard landing? Tough to call. But amidst recession fears cyclicals have already sold off and Mag7 is seen as a safe haven by many. The higher quality ones are seen as utility like selling essential goods and services. The lower quality ones have such exciting long term growth themes that investors will probably look through a few recession years. And in a hard landing inflation and interest rates will probably come down which is bullish for Mag7. Take off? If we do see robust broad-based economic growth then that will favour small caps and cyclicals and with growth becoming less scarce that might moderate the multiples investors are willing to pay for Mag7. But then again growth was pretty strong in Q3 and Mag7 on the whole posted very impressive growth figures and with Tech Eating the World they will participate in any economic growth and still do well. The main scenarios to worry about would be a stagflationary recession (which seems unlikely) or Mag7 collapsing under their own weight as they prove incapable of living up to the high expectations and lose their lustre. But as religion stocks and one decision stocks it will take a bit of time for investors to lose faith.

-

Saw an interesting chart that ex-US global stock markets are below their 2007 peak. US stock markets are three times higher. It really has been a case of tech eating the world. Historically that kind of divergence of performance would argue for loading up on EAFE and Jeremy Grantham is a big advocate of avoiding USA. Fairly neat way to avoid all the question marks about US debt and whether tech can continue its outperformance with current starting valuations.

-

How Does the World’s Largest Hedge Fund Really Make Its Money?

mattee2264 replied to james22's topic in General Discussion

It does make you appreciate even more how investors like Warren and Charlie can share so much wisdom about how to invest but also how to live. -

If stocks are worth 20x earnings at 5% yields and 25 times earnings at 4% yields then not surprising why we are seeing big swings based on rate cutting expectations. Especially in growth stocks like Tesla and Nvidia where most of the value is in the terminal value and therefore very sensitive to discount rates. But of course the above arithmetic assumes no change in earnings. If rate cuts are accompanied by falling earnings or slower growth then that is a negative valuation factor. And I think the market is being a bit too optimistic in thinking that we can get lower inflation and lower rates and continue to grow at 3% a year. And if growth does slow to 0-1% then that is going to have a negative impact on corporate earnings and growth rates.

-

Is the US economy set for another Roaring ‘20s?

mattee2264 replied to james22's topic in General Discussion

The other important difference is that in the 1920s the USA was a developing/emerging economy. So technologies that allowed mechanisation of agriculture and automation of manufacturing and so on allowed for more rapid industrialisation and massive productivity improvements. And freed up labour so it could be moved into higher value uses. In this sense the new technologies were very much complementary to society. The difference with AI is that it would be replacing a lot of low skill tasks and in a world of billions of people there are no obvious other low skill tasks for them to engage in. So you could just end up with a lot of structural unemployment and a lot more government debt as the welfare system will have to expand and you cannot tax AI the same way you can tax labour and it is also far more difficult to tax companies than it is to tax labour. Certainly AI is a deflationary technology. But I am not convinced it is going to lead to massive increases in world GDP. -

The Fed will cut as it always does when a rate hiking cycle pushes the economy into recession. Historically though the negative impact on EPS dominates the benefit from lower interest rates. And the market usually bottoms about a year after the first rate cut. But this is the era of fiscal dominance. The irony of course is that the stock market places far too much importance on everything the Fed says and does. When aside from causing a few localised fires which they can put out via bailouts 500 bps of rate increases has had very little impact on the economy because it has been swamped by the stimulus that trillion dollar fiscal deficits are giving the US economy. And why would the US government get responsible during a recession? Especially when an election is coming up. And if there is a recession it is much easier for them to overcome the flimsy checks and balances to increase spending. And without a recession, unless something else breaks in a major way, you aren't going to get a major decline in stock markets. It is true that the Fed has less influence over the long end of the curve especially when bond vigilantes are doing their upmost best to impose fiscal discipline. But they always have the option of yield curve control and can print unlimited amounts of money to achieve that. Whether there are long term consequences from seemingly reckless fiscal policy is anyone's guess. But everyone was convinced that QE would lead to disaster. And while it certainly distorted the economy and encouraged a lot of speculation it didn't cause hyperinflation and has juiced stock market returns. I suspect much the same will be true of fiscal policy.

-

Agree re the safety of real assets in an inflationary world. However does that apply to Magnificent 7? If you look at 2022 the inflation shock absolutely savaged Big Tech. 50% declines on average. The V-shaped recovery was because there was a seemingly immaculate disinflation (with an added kicker from AI). You get some protection from their pricing power but if their customers are getting squeezed by inflation there might be a limit to its exercise. And the very high multiples are predicated on double digit growth as far as the eye can see and law of large numbers is starting to work against them. But I am not really seeing a future of high inflation. Perhaps in pockets such as food prices and natural resource prices due to scarcity. But fiscal spending will slowly get diverted into debt service and become less effective in stimulating demand and the higher interest rates necessitated will crowd out private sector spending and we will probably have another decade of sluggish economic growth and moderate inflation (say 3-4% averaged over the economic cycle) until the AI productivity miracle occurs.

-

Yep does seem like another flight to safety to Big Tech underway. Same playbook as during the pandemic when economic uncertainty during the summer led to a a melt up of technology stocks and a sell off of old economy stocks.