Dazel

-

Posts

676 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by Dazel

-

I bought shares on the pull back today as well!

-

I would add that the bond portfolio has had a very good first quarter….They did not add long term bonds in the fourth quarter. Did they add in the first quarter? The 10 year went from 4.79% (mid Jan) to a low of 4.11% Wednesday. Fairfax duration of approx 4 years has done well.($800m gains?) At some point i believe the team will start buying long bonds again.

-

I have not gone anywhere and Fairfax is acting how I thought it would in Fairfax 3.0. Solid as a rock in a market that I can’t really even look at without shorting it. Don’t short a bull market is a lesson Fairfax learned the hard way so I am doing my best to stay away. New information and I will be back but for now Fairfax 3.0 is the only place to be.

-

Fairfax 3.0 is on script the company is powerhouse and every piece they can pick up adds to intrinsic value. Hard to imagine they paid anywhere close to fair value in Ukraine. as for wild fires costs I have NO idea.

-

Thats positive at Chubb bond rates have not moved enough to cause enough trouble for the insurance industry. In another thread I “speculated” that Bradstreet may gave taken short term bond gains and went long term…he is the bond kind. We will see in a few weeks….

-

Thanks for the numbers Viking. my spidey senses feel that Bradstreet sold short duration and went long duration in the fourth quarter and is continuing to do so now. Because it’s what I have been looking at. Long bond yields (UST’s) have peaked in my opinion. That’s where the money is….stabilizes operating earnings for decades.

-

Viking, Our work horse. What number should we expect for annual earnings…unless Bradstreet sold bonds at the beginning of the quarter they will be down in the fourth quarter mark to market…$800m paper gain in the third quarter.

-

Thanks Daphne. I owe Fairfax my time for sure. Bet they are having an absolute blast at head quarters! Fairfax 3.0 will be soooo fun!

-

bonds trade like stocks except bonds send interest payments (interest rates are much higher now and there is much more volatility) during the trading where as there is smaller yield from stocks/dividends and Bradstreet is the best in the bond business. Take a look At ticker “TLT” (UST long bond) there is an 50% spread from high to low this year! Educate your self from there. Corporate bonds trading and income would be the higher returning bond instrument (more volatility) and in a very aggressive stance could take allow Bradstreet to do 10% plus. Most everyone should be looking at the bond market here as it is more attractive then the stock market for sure! It makes me giddy to think Bradstreet now has $40b to play with! In 2002-2003 he made a billion bucks on a $5b long bond bet. He made $2b plus (30x) on credit default swaps in 2007-2008. i also said it was an outlier like for coke going up 10X in 10 years…in the 1990’s. Google and Apple etc trounced those returns Buffett got a good chunk of Apple. Bond bets gone bad….ask Bank of America and Charles Schwab the other side of Bonds they have well over $100b in unrealized losses from buying long bonds a few years back. Make no mistake Bradstreet is the “Bond King” and the investing world has never heard of him.

-

Fairfax 3.0 will have very few investors left from this board and that is the reason I created this thread. Everyone has very good points that are negative because they are biased from Fairfax 2.0 and no one can blame them. Those that were around during Fairfax 1.0 did not ask where the growth would come from when the stock went from $3 to $30 or $10 to $100 or $30 to $300. I have my own biases of course. Would I have been able to hold Berkshire? After coke went up 3X would I have thought it would do another 7X? Do I think that Bradstreet can do 10% a year? Yes I do. Is it probable? Yes to me it is…to the market no it is not. Do you know what the compounding is on that? Do you what market multiple Fairfax would get on that? Think Markel and think $10b a year. So coke doing 10X in 10 years or Bradstreet doing 10% a year over 10 years what is more probable? Gotta love markets.

-

https://simplywall.st/stocks/ca/insurance/tsx-ffh/fairfax-financial-holdings-shares/dividend You have to set up an account to see this but it is worth noting their cashflow valuation and future value for Fairfax is $5,400 cdn. This is the first time I have seen Fairfax get this type of valuation. Fairfax 3.0

-

Thank you! Awesome Look at 1990 to 1998 at Berkshire actually started in 1988. Coke went up 10x then 2015 to 2023. Apple went up many X as well Bank of America….These are the greatest investments ($made because of concentration) of alltime. Take apple and coke out of Berkshire and what does it look like? I am disappointed in myself for not including Mr. Munger in my previous posts! He is the architect of the above investments and Buffett recognized this in a recent annual letter. Buffett could not and would not have made and held those bets without Munger. Did Prem and his team blow these investments away? Fairfax has made “large bets” on their own stock. First in 1990 (buying 20% back @$20 that’s 100X) and now they are in the middle of buying back a big chunk of under valued shares. (Swaps@$375 headed for 10X?) The buyback program now will get massive if the stock remains here and Long term Shareholders will make multiples more if cheap shares can be retired. Fortunately, there is more than one way to get to heaven and if Prem and his team are more comfortable going the way of Teledyne then so be it. Teledyne on steroids of course because of the rocket fuel.

-

This is why I would to like to look at Fairfax 3.0 compared to Berkshire 2003. size matters especially for future growth. I would argue Fairfax is in better shape because of Prem’S focus on insurance companies. Buffett is king so this is not a slight. Prem especially was focused on fixing Fairfax insurance business in 2003 and be doing so he was in the trenches so to speak. This gave him insight into the value of not only his businesses but also into the industry and made many strategically “awesome” acquisitions including as Viking said buying all of Northbridge and Odyssey Re. Many of Berkshire’s businesses long acquired have tanked during that time and Munger alluded to this in 2020. Buffet spent $30b on precision castings, news papers became worthless and Prem was busy building a powerhouse insurance company. Earnings power at Fairfax 3.0 is equal to Berkshire 2003 because of this. The outlier is Buffett himself and his stock picking prowess that is unmatched. Apple was the biggest single stock gain in history he did the same with Coke. Moodys went up 20X from 2009. Bank of America. Prem lacks this skill but has made up for it building and buying private companies.

-

Great work!

-

Fairfax 3.0 is now a powerhouse. If the above scenario plays out with them continuing to knock the ball out of the park the rise in share price could be very Berkshire like it’s the same math.

-

I will run some buyback numbers. Totally agree Viking Everything that matters is per share….and Fairfax has done an unbelievable job of taking advantage of the undervaluation. Hoping they will sell everything not core into this bull market and continue to consolidate and buy back every last share they can here. The math gets wonderful just in time to buy long bonds into the next bear market. Bradstreet won’t miss it.

-

Thank you Viking. I agree with your thoughts and why most missed Berkshire and Markel. Yes I agree volatility would be a Fairfax friend. I think you are light with Bradstreet returning 5% on bonds…remember if he does 7.5%(likely) that’s $3.75b per annum…but I understand your conservatism. He is the bond king. (And credit default king) remember! Do you have a spreadsheet set up that can reallocate what the compounding of the growth in the investment portfolio does to the total return over 10 years? Make it interesting and throw in an 13% year and 5% year etc. This is how Buffett did it at Berkshire…Fairfax is finally at this stage in their evolution where the base operating earnings and the underlying businesses are steady so capital gains juice returns significantly. Example using the above year 1=$70b +$5b earnings year 2=$75b +$5.47b @7.3% year3=$80b + $5.87. @7.3%

-

Markel uses “rocket fuel” as well they have long been trading under the wonderful handle “baby Bekrshire”. They use the same math I have shown above. Fairfax 3.0 has the ability to trade in the “mean” range of Markel’s PE averages. how? Stable earnings…become outstanding earnings with “rocket fuel”! Fairfax 3.0 is on its way there…last ticket to jump aboard will be soon. The market has voted on Fairfax share price the last couple of years but this year they will likely vote and weigh at the same time.

-

-

The Math Berkshire Buffett has set up Berkshire so that all else being equal whatever he returns on His investment portfolio roughly doubles his return on equity. I have not seen the number but I would bet he averages around 11% (Same as the S&P) but with the “rocket fuel” that take his long term average compounding ROE to 22%. When Berkshire was smaller his returns were much larger but scale has taken his long term average to the market multiple…or a little above it. ****Dont start yelling at me! Berkshire never has their entire investment portfolio in equities that’s why Buffett’s return “on his entire investment portfolio” is the same as the S&P. Ie he has $325b in cash right now. Fairfax 3.0 The long term return is around 8.7% and their insurance leverage is the same so this would take the return to 17.5%. These numbers turn out to be very accurate over 38 years. Fairfax also trounced the 8.7% in the early days hence the stock sky rocketing in Fairfax 1.0 All of the incredible amount of work to run these companies to bring them to a “all things being equal” is there to set up the simple math above. Fairfax 2.0 struggled to keep this equilibrium because interest rates went to zero and below in Europe and a general distaste for the bull market we are still in. Fairfax 3.0 could theoretically buy the 30 year bond to maintain a 5% return and secure a 10% ROE with the insurance companies performing well. To return their long term goal of 15%ROE they need to do 7.5% return on the investment portfolio.

-

-

Hoodlum, Buffett’s particular problem with almost assured losses was “Asbestos” the entire industry got smoked on this and it was the biggest problem for Fairfax at the start of Fairfax 2.0. CAT insurance is different as pricing matters most. Ie cyclical…more storms/fires/weather the higher the price and vise versa.

-

-

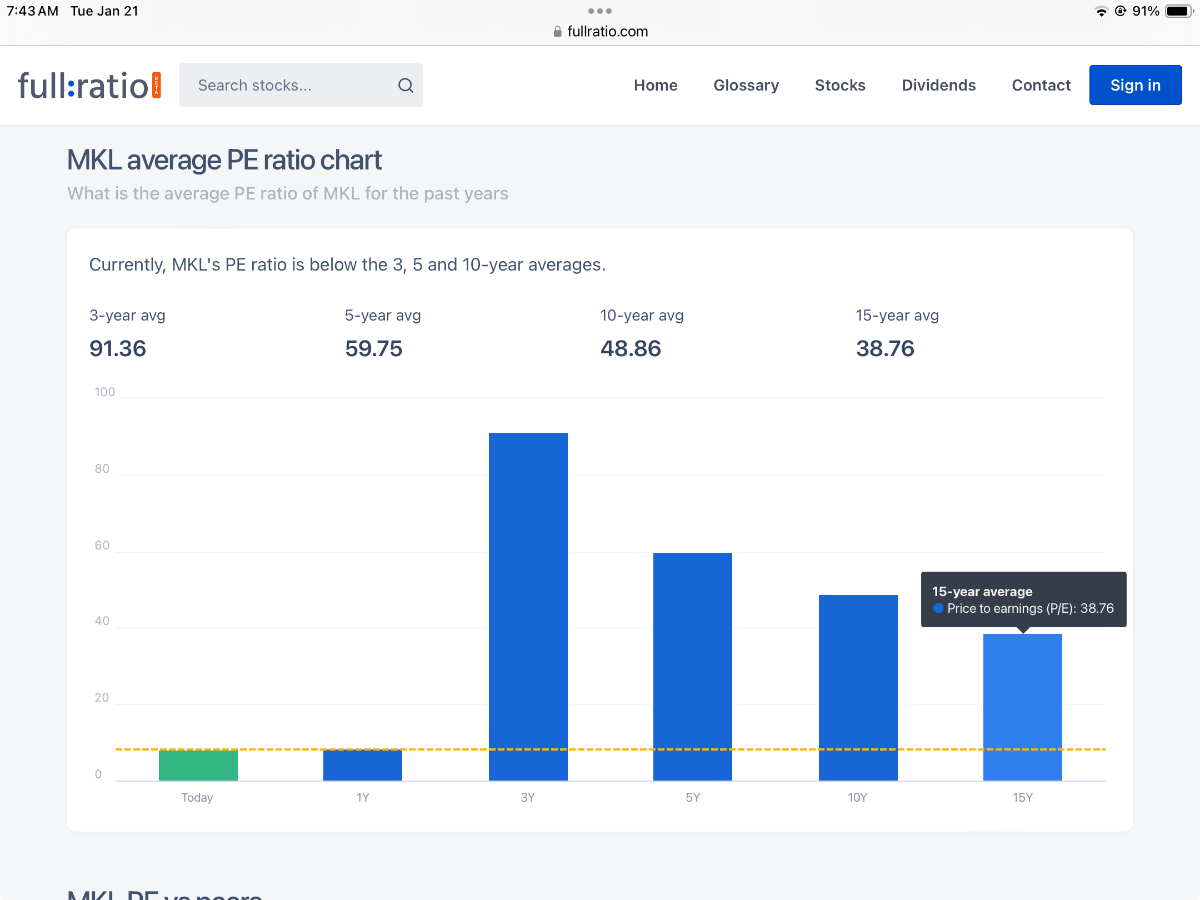

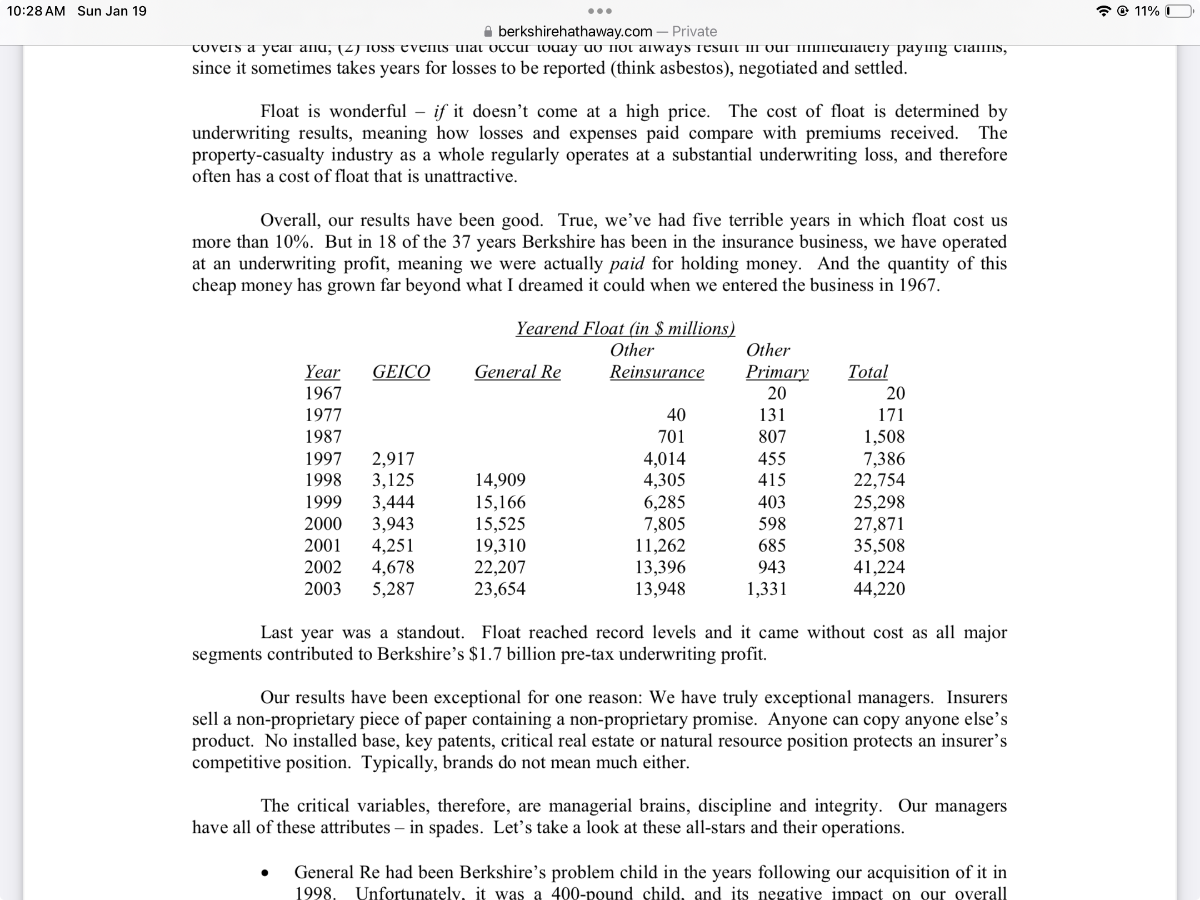

Below is What the insurance numbers can look like compounded vs other less than average companies. This is from page 4 of Berkshire’s 2003 annual report. Mr. Buffett explains the difference between book value and earnings between Berkshire textiles and the change in earnings beginning with insurance company National Indemnity purchase. Fairfax is all National Indemnity and insurance this is in the business that Buffett covets. This annual report is from the 38th year of Buffett ownership and Fairfax is in their 38th year. You will notice that Berkshire’s insurance operating earnings were almost the same as Fairfax at $5.42b!

-

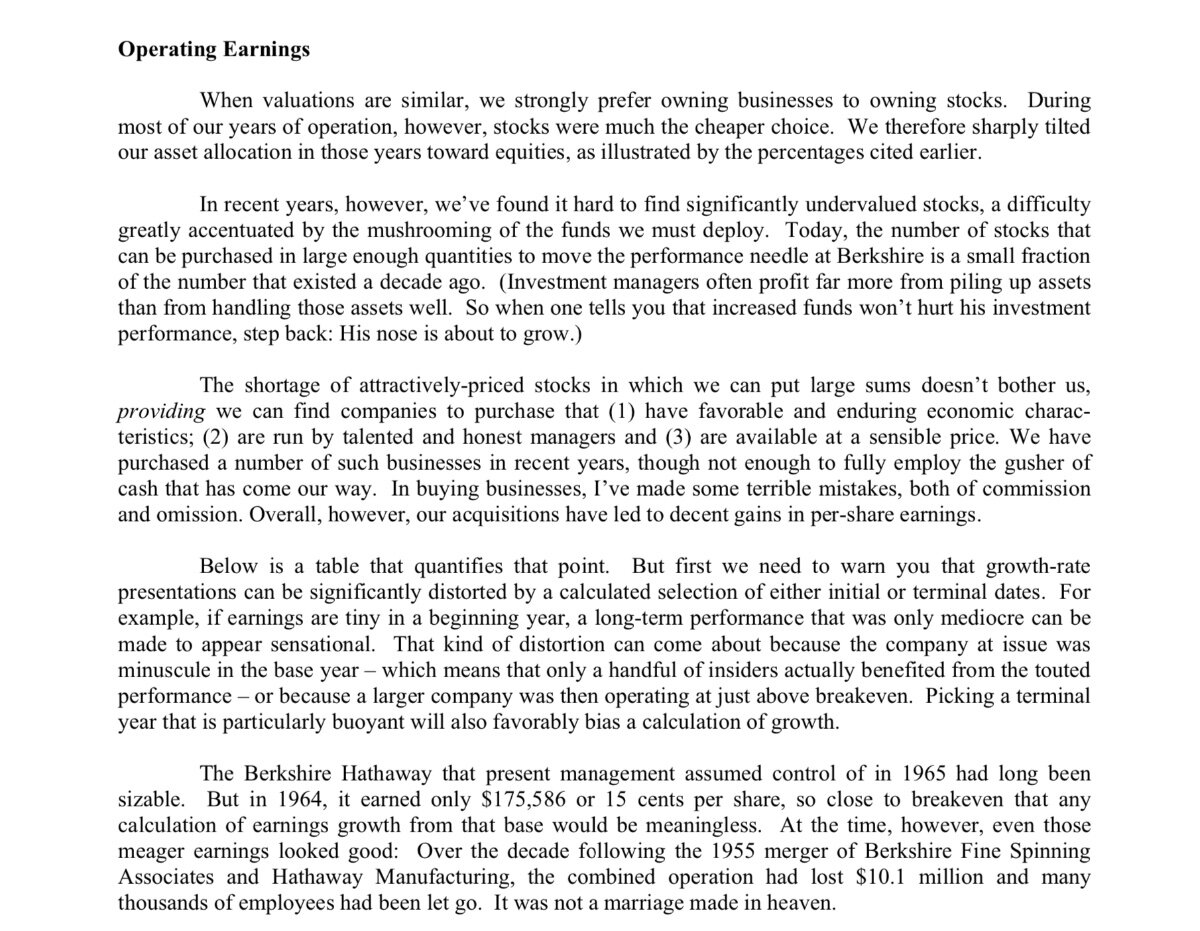

I am going to refrain from discussing the past (after a brief explanation) as much as I possible can on this board because I have done a lot of it over 2 decades! It creates two narratives and I will take the perspective of third or Fairfax 3.0 in this thread. Viking is the king so I will not even pretend to put the numbers work like he does but I will give a narrative and the psychology behind Fairfax 3.0. It might be the most important “thing” for most after all the shares have exploded higher. (Cdn prices) Fairfax 1.0 (narrative they can do no wrong…Warren Buffett of the North) $3 to $600-1984-2000 superstardom for Prem Watsa and Fairfax. Fairfax 2.0 $600 to $60 2000-2003 (insurance companies are garbage Fairfax 1.0 a fraud?) $60 to $400 2003-2008 (not a fraud but insurance companies are still in trouble..Big Short and long bond bets of the decade $400 to $750 2008-2016 (insurance improving Fairfax is a bet against the market even though their shorts were decimated) $750 to $350 2016-2020 (pulled short bets off the table and were left for dead in Covid, company under earning they did not reach for yield market hated it and killed the stock) Fairfax 3.0 $350- $2000 2021-2024 (Re anointed king of the world, cash put to work in an all in bet as well Prem going all in personally, insurance operating profits sky rocket, stock follows) $2000-? 2025 -The magic of compounding at work! How did they do that? Fairfax 1.0 Everything went right! -hard insurance market at the beginning…they doubled their premiums in their first year -1990 recession that hit the stock they took advantage and bought back 20% of the company from Markel. (Greatest trade of alltime?) -the stock joined the bubble market briefly hitting $600 setting up a tough Fairfax 2.0 -High stock price fueled large takeovers that had hidden insurance tail risk that would set up hell for Fairfax 2.0 Fairfax 2.0 there was great frustration with one step forward and two steps back and there are reasons for it that I will not go into detail on an explanation because they “don’t” matter now. -insurance losses of companies taken over almost sunk the company -stocks were expensive -2 crashes nailed one (greatest trade of alltime 2007-2008) and got smoked in the second one (2020) -Blackberry disaster -short selling disaster -zero and negative interest rates (This was the biggest obstacle for growing book value and compounding money) -underneath they were building the foundation for Fairfax and smartly doing it with growing their “rocket fuel” insurance companies through smart acquisition and building. This will be Prem’s greatest achievement the man can build insurance companies like no one else his talent here is unmatched. Fairfax 3.0 It’s built! Time to print money and buy back every last share possible share before the world figures out the intrinsic value per share is above $3000. (USD) Why is intrinsic value this high compared to the market price? Prem and his team built a pure play insurance empire from basically scratch so the book value of these insurance companies is recorded at the cost of building them “not acquiring them”! If these companies were sold individually they would demand many multiples of their current balance sheet value. Proof examples of the intrinsic value above the recorded book value at Fairfax They sold Lombard that was built from scratch for almost 3X book value, $1.7b premiums=$4.6b value. https://www.fairfax.ca/press-releases/fairfax-sells-shares-of-icici-lombard-2017-09-27/#:~:text=Fairfax Financial Holdings Limited (“Fairfax,of approximately US%24548 million. First Capital was sold for 3X book value https://www.fairfax.ca/press-releases/fairfax-and-mitsui-sumitomo-insurance-enter-into-strategic-alliance-and-sale-of-first-capital-2017-08-23/ Global pet insurance sale gain $1.2B! 6X book value…They made so much above book value they did not even announce the gain they were embarrassed! https://www.fairfax.ca/press-releases/fairfax-announces-successful-completion-of-sale-of-global-pet-insurance-operations-2022-10-31/ Intrinsic value is likely at least 3X book value and growing=$3,000 usd per share with the “rocket fuel” of the float that adds considerably to intrinsic value. To be clear Fairfax will “Not” trade at 3X book this week or month but from the starting point of today it will eventually get there because the earnings power and intrinsic value of the companies will take it there. Companies are not sold at 3x because of their value that day they are thought to grow into and above the purchase price paid by the acquirers. “Rocket Fuel/Float” and operating earnings rising to the mean The knock on Fairfax has always been that their insurance operating earnings lagged their peers and they relied on investments to heavily. Not anymore! Their operating earnings are now approaching $5b per year and analysts are waking up to running the numbers with disbelief. They are so large that it is tough to grasp the possibility of how high they are headed. Berkshire had this “aha” moment many years ago before the stock went vertical and Fairfax 1.0 experienced it in the late 1990’s. Berkshire is the yardstick in the investing world but very few (especially these days) understand that Buffett and Munger used math to goose returns. Buffett came up with the term “rocket fuel for insurance float” and Prem and his team started Fairfax with the idea they could copy his model. This is not new to any of us old timers on this board but to the newcomers “float” and the cost of it is the math behind Fairfax 3.0 and the secret to Berkshire’s success. I am going to compare Fairfax 3.0 to Berkshire in a 2003 snapshot to show the valuation of each comparatively without bias at their respective 38 year mark to show how compounding works in the two companies and what is possible for Fairfax. These numbers will “Not” be perfect and there will be errors as I do not have the time nor the interest in being precise! This will be more art than science. What’s possible in the future is up to Prem and his team. Mr. Buffett is unequivocally the best longterm investor of alltime the Fairfax team will not be able come close to his numbers but I hope to prove they don’t have too. I strongly suggest you read Buffett’s Berkshire 2003 chairman letter and all of them for that matter especially for the times we are in. https://www.berkshirehathaway.com/letters/2003ltr.pdf