cloud

-

Posts

49 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by cloud

-

Value investing at its best .. Based on this topic you are probably best off moving your assets to a savings account. Among other reasons, the main reason of raising cash is to pay down the mortgage. I have 50% bond currently, prepared for paying down mortgage over the next 5 years. I'll prepay 17k this year. The result is that I'll pay off the mortgage in only 10 years. Right now I have 20 stocks of high quality. If I have extra cash laying around plus the dividend received once a while, I still nibble existing positions if they go down more than 10% from last price paid. KORS is at good valuation and it has strong competitive advantage. i started a thread last month to encourage others to buy. I got rid of it for many reasons not because of its fundamental.

-

Interesting.. and complicated analysis. and pretty accurate. Yep. My NEW process is bad in some way. In this case, it probably has 70% chance of working out in the end but I want to sleep better at night and have less worries. It's extremely mentally painful to see half year's saving evaporates in just 1 month with some uncertainty of recovering it and the time it takes. so I am going back to the old one. :) I take mistakes as something bad that we can avoided in the first place but were not mindful enough to avoid them. It's partly due to deviation from what I was doing and partly due to trying out new ideas. I started investing with carefully weighted positions. I avoided having positions more than 10% of portfolio. One day, I learned about options and learned how to sell covered calls. I got much bolder thinking now I have covered call as protection. And I can have bigger positions. I said in first post that little premium can not protect a 30% or 40% drop if the position is so big that not enough new funding can add to the positions to bring down average cost. I learned about concentrate investing from other famous investors like Charlie Munger which he went through lots of pain in partnership years by concentrate investing. There are others like John Keynes who practiced concentrate investing. To what degree, I don't know. Then there's another mad man George Soros. He said famously: It's not whether you are right or wrong but how much you win when you are right and how much you lose when you are wrong. I averaged down Kors too quickly. I wasn't patient enough. My average cost with Kors is $52. If I stick with it, I have a good chance of breaking even or earn a satisfactory return few years from now but I decided to get rid of it. I am giving up the new idea about options and going back to equal weight as best as I can. So in Kors case, I was wrong in the timing and positions size and I lost a lot. When I used equal weight and nibbled positions, I made good profit while still able to sleep at night. I nibbled XRE.TO REIT little bite at a time during the scary time in 2009.(At that time I had no debt, no mortgage. ) I bought all the way to its bottom and had no sweat. I sold slowly all the way up and made good profit. I had mortgage since 2010, it makes me hesitate when I make investment decisions, so I want to get it out of the equation and there's one less thing to worry about. I'll aggressively cut down its size in the next 5 years. Kor's mistake is not devastating. It cuts 75% out of my 2014 return. So my 2014 return is 7% instead of 30%. Overall compounded annual return since started as a newbie in 2007 is ~10%/year. I did not go back to GO. I am happy so far.

-

Speaking of mistakes: Mr. Money Mustache’s Big Mistake

cloud replied to cloud's topic in General Discussion

I am not MMM. I just like to read some of his blog posts to reaffirm some of my views on things. Glad this post is useful for some people. -

Just keep learning and thinking, we can get better and better as time goes on. If I am not hard on myself, I am afraid I'll repeat the same mistake next time. ;D

-

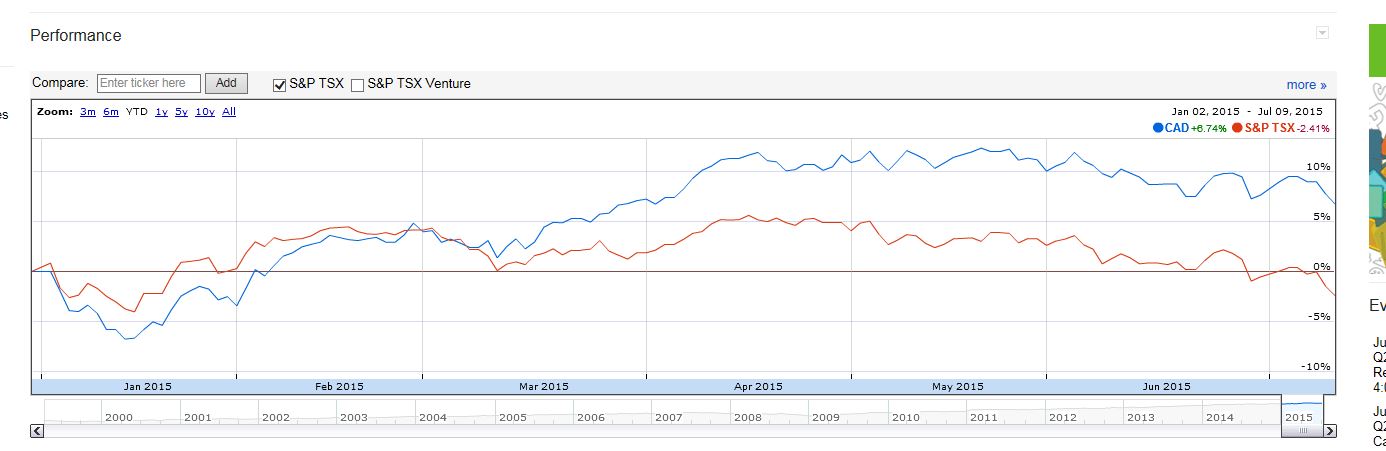

Cash secured put I hope? Better wait for price to come down. They come down more often than we thought. Today is just a beginning. I have a feeling a recession/huge bear market is coming.(china slowdown+Greece debt+market correction causing wealth effect) I find the best way to park cash while waiting for bargain is to buy laddered bond ETF. I split between CLF.TO (Laddered government) and CBO.TO ( Laddered corporate). Right now, I don't mind parking lots of cash. I can always use it to pay down the mortgage as I feel like it. Prepayment is capped at 17k per year. To me, buying calls is like gambling. The loss is 100% if wrong. Professional option traders say otherwise. Blackberry: I was being patriotic and bought a Playbook as a support. They failed me. My thought was that their only hope was to switch the OS to android. Or they'll be squeezed to a corner. You never know how low resources price can come down and when they'll go back up. Predictability is the number 1 thing in investing. That's the good thing about mistakes. As long as we don't make huge one, minor mistakes are good for us to improve in the long term. I always remember Charlie's saying: I don't want to go back to GO. Even I took unnecessary risk, it's calculated risk and I paid the price for it: lost 10% of portfolio. It's little bit painful because my portfolio got a lot bigger in recent years. No more... Equal weight portfolio is the way to go. My DIY RBC equal weight CAD portfolio is only down -6.5% YTD as of Aug 24,2015 (100% stock).

-

http://www.mrmoneymustache.com/2012/02/01/mr-money-mustaches-big-mistake/ Mr. Money Mustache’s Big Mistake “The problem with Mr. Money Mustache”, some people say, “is that he has led this blessed and privileged life where nothing ever went wrong for him! He never makes any mistakes, and that’s just not the case for most people.” I can see why you might think that, since I tend to write to you about only positive things. It’s a habit I picked up about twenty years ago after reading The Magic of Thinking Big, and I’ll never let it go. People who know me will notice that I’ll never say “I’m coming down with an awful cold”. Instead it will be something like “I’m just recovering from a bit of a cold, it should be on its way out by tomorrow morning”. You simply get no benefit from telling others about the problems in your life. At the borderline between useful and non-useful things to talk about, you might mention a life problem you’re working on solving, while talking about what you’ve accomplished so far in your plan to fix it. But since you asked, I think it would be educational to share the story of The Biggest Fucking Mistake I’ve Ever Made In My Entire Life. Just to show how even a BFM doesn’t have to ruin your life, and indeed you will almost certainly come out happier in the end after you get through it. So pull a log up to the campfire and start roasting a marshmallow – because this is a scary one. It was the year 2004. I was happily working as a software engineer, and my new wife and I were living a great life. We had no kids, great friends, great jobs and we were busily ‘stashing and just a couple of years from financial independence. “This is fantastic”, I thought, “What will I do next, after finishing my regular working career?” One day, while passing the time between flights in an airport bookstore, I picked up a discounted copy of “Rich Dad, Poor Dad”, by Robert Kiyosaki. Despite the more recent widespread criticisms of that book and its author, at the time the book screamed to me, “You should start your own business and lead a big exciting businessman life!!” To me, starting my own business meant turning my most cherished activity into a post-retirement job, which of course meant building houses. I already knew a few custom house builders at the time, and they were all doing great business here in Boulder County buying empty lots in good locations, and building luxurious but not overly large houses on them. When I reviewed their numbers and toured their houses, the work and the profits looked great, so I decided to jump in as well. I happened to have a very good friend at the time, let’s call him Dean. Dean and I had met five years earlier, when we randomly ended up as cube neighbors in a high-tech company in Boulder. We had both come to Colorado at the same time in the fall of 1999. He was just off the plane from San Francisco and I had arrived from Canada. We had a good run together in that little company, working on innovative projects together and mocking the more Dilbertesque aspects of our company’s senior management. We bought houses at the same time and helped each other with the renovations and hosted alternating parties almost every weekend. Even after I moved on from the Dilbert company and started a more serious engineering job in the same city, we remained close friends. We hiked, biked, and snowboarded together. And we both had entrepreneurial dreams, inventing dozens of hypothetical plans together and working out sketches of the business ideas. So it was natural that when I decided it was time to start a house building company, that I’d invite my best Colorado friend to be a partner. I thought he would do great, because he had a beat-the-system attitude that I valued. He was the one who taught me that you can argue with credit card companies to have charges removed, that you can buy whatever you want at the hardware store and just return whatever doesn’t work out, and that you could call the town council and ask to have a rule changed instead of just obeying it. Of course, looking back I can also see the obvious warning signs that I was blind to at the time: he was also the one that taught me you can slack off at work, and still get paid the same amount. He used to award himself extra vacation days as “comp time”, even while his regular working hours were 9:30am – 4:30pm with plenty of time for personal phone calls and web surfing in between. He even told me of some <REDACTED – let’s just say youthful moneymaking adventures at earlier jobs that I don’t want to get him in trouble for since this blog has grown very widespread since I first wrote this article> . “Wow, that sounds kind of illegal”, I thought at the time, but I figured it was many years in the past and it was just a typical young person’s testing of society’s boundaries. And he justified it all with such intellectual and socially-responsible explanations. He did volunteer work and helped out friends in need. Wiser readers will at this point recognize the signs of a shifty and sociopathic character, which I now see in retrospect. But at the time, I was just star-struck, as we took two-hour lunches to eat Jamaican food on sunny Boulder restaurant patios and play basketball with our coworkers in the court behind the building, in the time I’d normally assume we should be writing software. So when I presented my new House Building Company idea to this adventurous guy, he immediately latched onto the idea and the planning took off. He persuaded the owner of perhaps the hottest New Urban Design neighborhood in the country to sell us two plots of land despite being unproven new builders. I negotiated with one of the best and most well-known architects in Colorado to take us on as a customer at a drastically reduced rate. The owner of the firm had a soft spot for the young fresh-faced businessman with the same goals as he had – to build housing that was Human and Earth-friendly instead of ostentatious. We teamed up with a sagely old builder as a mentor to watch over us as we built the first house, to prevent newbie mistakes. We were on a roll as we signed on subcontractors to help out, selling the dream to everyone and pre-selling the house before we had even finished building it. But in the background, little warning signs were continuing to pop up. Our financial agreement was that I’d bankroll the whole downpayment for the project, while my friend would only put in the $20,000 or so he happened to have sitting around. We worked on arrangements for compensating me for my increased risk in the project, until he came up with this “brilliant” idea: “Well what about this, if the company loses money, we’ll share the losses equally, so you are NOT at any more risk than me. I’ve got my 401k as a backup plan, and I’ll cash it out in the worst case if we get into hot water”. “Good idea”, I thought, “Now we can just be equal partners! I sure feel good not being the only one at risk”. Ahh, naive little Younger Money Mustache. Trusting to a fault. I never thought my best friend would go back on his word – we’d done everything together for the last half decade! So the project went on. I put in a heap of my own cash and also took out a $90,000 line of credit on my house. I poured every paycheck into that company for a year, to minimize the outstanding balance on the high-interest construction loan. “What could possibly be safer than investing in your very own company at a guaranteed return?”, I thought. One day, an email came from my friend, entitled simply “Need 17k”. It turned out he wanted to move out of the place he was renting and buy a house instead. I expressed some concern about this, since it would take his investment down to zero even while mine had now reached about $200,000. He pooh-poohed my concern, reminding me that I already owned a house, and of course it was only fair that he should be allowed to have one too. We worked like DOGS on that construction company. Well, I did anyway. I snuck time out of my office job to answer emails and work on marketing materials. I worked every night until midnight on budgets and material selection and design ideas. I negotiated a four-day workweek from my employer and started spending every Friday building alongside with the framing crew, to learn, prevent problems, and speed the house along in any way I could. I worked on the site with a carpenter friend on weekends to get even more done. My business partner seemed devoted at times as well. He made some good contributions throughout the project, and he was a smart and organized guy. But I couldn’t help notice that he was still taking weekends off, still volunteering in local organizations, and he happened to take two trips to the Caribbean during the first year of the company. While I worked on our company’s house, he worked on renovating his own new house, drawing a handy monthly salary from our company even while I made contributions to it every month. But our success masked these problems. We sold our first project before it was even complete, for our full asking price. My own labor had cut our costs considerably, leading to a healthy profit margin. But then a long argument started about dividing the profits. I had kept track of my labor hours, and I suggested that I be paid for them at a low rate, since I had used them to reduce the cost of outside contractors. He disliked this idea, thinking that the profits should simply be split 50/50. “It’s not an hours competition”, he said. “We each contributed in our own way. What you brought to the company was your ability to work like a workhorse, and what I brought is strategic ability. If I make a phone call to the city that saves us $2,000 in re-zoning fees, and you do fifty hours of work that saves us $2000 in contracting fees, should you get paid more than me?”. Of course, my own phone calls, such as the one that I made to the architect that saved us $30,000 in architecture fees, and other similar efforts negotiating with subcontractors and materials suppliers, were somehow not considered equal to his own strategic brilliance. By this point, I realized that our partnership was not meant to last, but our company still owned one more plot of land and we were already building the second house on it. The housing market was strong, and I figured we could finish it, sell it and I’d be out of this little situation. So I gritted my teeth and tried to smile. But it happened to be the year 2006, and the US housing market was just about to take a plunge into the shitter. The second house went up beautifully, and problem-free. My now-semi-friend did a competent job at repeating his role in organizing the contractors. And being fully retired from my day job by this point, I was able to spend every day at the site watching over things and building. Potential buyers toured the house every day and we came close to selling it several times before it was done. Then the recession hit, and the house began a long period of sitting on the market. It was shiny and new and luxurious, with its airy, empty superinsulated rooms and cool thermal mass effortlessly battling the hot dry summer of 2007. Then its huge South-facing windows and bright halogen lighting and warm bamboo floors challenged the cold winter of 2007. So much work and care went into that place, and yet there was absolutely nobody interested in buying it. And every month we were going $3000 further into the hole. We got desperate and rented the house out to a group of tenants who eagerly promised to buy the house very soon, as soon as their current financial problems were resolved. Chase Bank backed out of their promise of an open-ended construction loan and insisted that we refinance into a mortgage. This would be no problem, they explained, as long as I could pay down the principal by another $67,000 so it would be a conforming loan of $417,000. At a 7.25% interest rate. My friend was of course grateful that I was able to come up with the $67 grand, since he was in debt from having to live on the low pay our company had given him for the past two years. I noticed, however, that he did not offer to move out of the house he had renovated for himself, or even to sell the top-of-the-line stainless steel LG appliances he had purchased for himself with money drawn from the company. His wife still worked, of course, and her former condo which was now serving as a rental house for them, was also not up on the auction block. “Her finances are separate from mine”, he explained. My wife surely wished she had thought of that trick. Tenants came and went from this house. We kept trying desperately to sell it, and dropping the price. For every showing, we had to visit the house and clean up after the tenants in hopes of having a presentable house. Every month, we split the difference between the $3,000 mortgage payment, and the $2,100 rent, in order to keep the house out of foreclosure. He reminded me often of how ethical he was to keep making these payments, despite his own financial hardships. This went on for a little over two years, but it felt like twenty. But somehow I adapted to the “new normal” and managed to lead a happy life, focusing on raising my young son and taking on carpentry projects to help rebuild my savings. We cut our family’s spending drastically and Mrs. Money Mustache increased her work schedule to increase income as a precaution as well. Finally, in late 2009, we caught a lucky break. A wealthy US businessman who was returning from a long overseas corporate position fell in love with our house. He toured it extensively, spent hours running his eagle eyes over any potential flaws, and eventually made us a lowball offer. He was a shrewd negotiator, but given the state of the housing market at the time, his offer of $450,000 was not that far below market value (which was in turn about $200,000 below our original budgeted selling price). But after the hell we’d been through, I was ready to make a counter-offer and get the deal done. But guess what Dean said? “Ohmygod, guys, my accountant just told me that because I’ve taken so much out of this company, I have a negative tax basis in it. If we sell this property, I will owe over THIRTY GRAND in income taxes, and I just can’t handle that. I’ve already got 50k in credit card debt!! Since I’m a co-owner of this property, I’m not going to sign off on the sale. I think we should hold onto it for a few more years, and sell it for $650k instead. Then I will get enough share of the profit to pay my income tax bill”. “Umm.. Buddy”, I said, “Do you realize my wife and I have over two hundred thousand lost already in this company, and you have about negative fifty, and that you have proven yourself less than faithful in coming through for the company when it is in financial need?”. “I would firmly suggest that you fuck off about your petty thirty grand, sell your LG appliances or your rental house, and let me end the personal hell that we’ve all been battling for the last several years.”. “Well shit”, he said, “That’s just like you, MMM, always thinking everything has to be your way. I wish you could see things from something other than your own perspective. I wish you could hear yourself right now!”. I actually recorded the three-hour conversation where he said this – our final business meeting for that company. Someday I’ll listen to it again, but for now the very idea still upsets my bowels. To make the rest of this long story shorter, I hired a lawyer friend to apply the necessary pressure to have him sign off on the deal. Even so, the deal still required me to pay off the mortgage on this property because both of our names were on it. To accomplish this, Mr. and Mrs. Money Mustache had to scrape together a final $409,000 in cash, the outstanding balance on the mortgage, and pay it to Chase Bank. Dean would still owe me over $100,000 because of the difference between in our investments in the company, but he quite confidently informed me that he did not intend to pay me back, because he was already on the verge of bankruptcy. He reminded me that if he did file for bankruptcy, his creditors would very quickly lay claim to the house we had built, because he was a part owner. My lawyer confirmed that he was right, and that I had no legal way to force him to keep his original promise of splitting the company’s losses. The best we could do is get him off the property’s deed to avoid further problems. Dean had an opinion on this as well: “I can’t sign off ownership on the house”, he explained, “while my name is still on the mortgage. That could be disastrous for me.” Yeah, we wouldn’t want a disaster, would we? But then an interesting thing happened. The SECOND we all signed those final papers at the title company, shutting down the home building company, wiping out the mortgage, and separating my fate from Dean’s forever, I felt a weight equivalent to the entire chain of the Rocky Mountains lift instantly off of my shoulders. Finally, the emotional damage could start to heal. During the peak of the crisis, I had lost my ability to sleep, lost my appetite, and lost 25 pounds of bodyweight over a period of just a few weeks. I could think of nothing but rage, revenge, and worry. To fight back I read several books about stress, its underlying causes, and how to deal with it. I also learned more about happiness, and started keeping a journal where I’d write about my level of worry and my goals for the next day – one day at a time, and then one week at a time. I was feeling better every day, even before the underlying problem was solved. After the deal was done, all this preparation and research compounded with the natural relief of the situation and made me a freakishly happy man. And when I say happy, I mean jumping up and down, sprinting around the block, and then punching a punching bag while laughing out tears of joy until you collapse, happy. I’ve continued to be roughly this happy for the two years since then, taking a life that was already pretty good, and ending up with one that is as good as being a an immortal superhero who lives on a cloud playing a Golden Grand Piano while his best friends accompany on the bass and drums, as the entire population of Earth gathers below the cloud every evening at sunset for an all-night dance party*. And the financial damage has slowly healed too. Extra work, frugality, and even a small boost from the developer of the neighborhood who took pity and decided to forgive a loan my old company owed him, all contributed. I took good care of my expensive new rental house, the rental market grew strong, and I found great tenants who now pay reliably even as they add gardens and lovingly maintain the house as if it were their own. It took a long time, but we’re now finally ahead of where we were before making The Big Mistake. In the end, I spent somewhere in the range of $200,000 on this educational experience. But in the long run, I would dare to say that I’m going to make a huge profit on it when measured over a lifetime. I learned mind-altering lessons about business, law, personal character, and hardship. I learned how to be more frugal and button down when a storm hits. I learned how to be happy even when on paper, very shitty things are going on in your life. And I learned to appreciate the incredible good fortune I have now that I’ve come though that hard time. I’m also working on learning about forgiveness. My goal is to someday be able to see this “Dean” character, pat him on the back, and say “Hey man, I’m sorry about the hard times we went through together. I know it was a tough time for you, and I forgive you.” I’m not yet at this stage, since I still have the odd fantasy about breaking his neck in the crook of my arm after stabbing 450 ballpoint pens several inches deep into his eyes, abdomen, and neck while calmly reciting a poem I would write about how selfishly he handled our business situation. Oh yes, it would be an event that would have Hannibal Lecter himself taking notes**. But over time, as I become wiser and more mature, I will grow past this, and I’ll be a happier man, and a better father and husband, for it. The best revenge is living well. So I make a point of exacting this type of revenge with gusto every day that I live. So why, you ask, has Mr. Money Mustache, the Commander in Chief of the No Complaints Nation written this novel-length complaint to you? It is meant to be an example of how even bad situations can turn good, how pain leads to happiness, and how expensive lessons can still lead to riches. You just have to keep working at it, and hammering through it, one day at a time. Just make sure you end up a bit further ahead each night than you were when you woke up that morning, whenever you can. Your problems WILL. BE. CRUSHED!!! *I do not mean to imply that I am anywhere near as cool as this hypothetical piano player, just that I have been roughly that happy. ** Update: Over three years have passed since I wrote this, and the anger has almost completely faded. I still have no desire to ever see the guy again, but feel that with my new life as great as it is, there is really no reason for anger or regret over anything in the past.

-

For some lessons, we have to learn them the hard way like learning riding a bicycle. We can't learn to ride a bicycle by listening to others. We have to actually ride it and fall a couple times to learn how to ride it. During the last two years, I made many covered calls trades in 2013, and 2014 aided by margin loan. The returns were very good at 40% and 30% respectively.(Mainly because of bull market phase) I thought that's the way to get really rich in a short time. I got over confidence and lost control of position sizing and became too overweight in some positions. At the peak, Michael KORS made up 60% of my current asset and 26% of my net worth.. It started to cause some pain in May, 2015. Taking out emotions and greed, Michale Kors is not the highest quality stock in my portfolio. I know it. It's not a buy and forget stock. but I wanted to recover the lost so I averaged down too much. It's not a predictable stock although it has a very good chance of bouncing back. I am just not sure. So I sold all remaining positions today. I decided to get rid of Michael Kors also because I have a ethical investing rule. I don't invest in stocks directly involve in weapons, alcoholics, tobaccos, animal products etc. Michael Kors's main product is leather goods which I should avoid if I follow my logic but greed and emotion come in play. I was lured by Michael Kors' strong balance sheet, fat profit margin and ROE. I rarely sell low and this is a rare time I admit I made a mistake. It cost me around 10% loss of portfolio this year. There are some other big positions which I sold in July which prevent more losses. Retrospectively, covered call is not worth doing. The small premium it produced and lots of paperwork it involves are not worth it. Often times, the stock rises far above the strike price and I ended up earning less. In the face of severe market drop like in recent months, the call premium becomes worthless and a much lower strike price have to sell to earn a couple % premium then there's a chance of selling below cost! The small premium gives a false sense of safety which encourage over sized positions. I rather buy dividend paying quality stocks and nibble a little bit at a time and ride out the wave. The catalyst of my awakening is interesting. On July 18, and 19th, I participated a Buddhist repentance service called "Compassionate Samadhi Water Repentance" which we repent bad actions we did in the past originated from mind, words and actions.. At one point of the service, there's the mention of repenting our greed, I realized how greedy I became in investing and starting losing my sight. I realized I don't have to get rich quick and I don't have to use margin loan.And I can still do well financially that I can still drive a car, have a nice house to live in and retire early. So I dramatically reduced margin borrowing in July, sold half of Michael Kors in July. I kept 50% thinking there's a good chance it'll rebound because of the ridiculously low valuation. The Michael Kors mistake cost me 1 year of time of increasing my net worth delaying 1 year for me to pay off my mortgage. Similar to what Lululemon experienced, I still think Kors has a good chance of rebounding in a few years but I don't want to own it anymore. The reason of my gotting rid of it is not because of its future prospect but because of my positions exposture, removing margin loan, refocusing on dividend stocks, and also ethical investing. Also my parents' health is deteriorating. I have responsibilities to take care of them. From now on, I'll focus on paying down mortgage, dividend paying stocks, dividend growth, a bit of REIT and a large position in short term bond. Most of my holdings are already dividend paying stocks. I just need to control their position sizing. I'll keep 50% stock and 50% bond until I reduce my mortgage to about $30000, 5 years from now while still keeping some stock positions. Right now it's at $90000. I was planning to move to a bigger house in xyz years. Now I am content to live at the same 160k house(Now worth 180k) for a long time! The mortgage is small. Heating cost, property tax is low. It's easy to keep it clean. I am trying my best to practice minimalism. That's why I don't need to use margin.. I can do well without leverage at all. I can still achieve 10% to 15% return on the stock positions. I know what quality stocks are but sometimes I lose focus and have to refocus. They are the stocks that can be bought and forget. Also I know should avoid resources stocks but sometimes I forget this rule. I don't like working for someone else. I don't like annual performance review and being asked what goals I have for the job next year when the company didn't even change much after 35 years that it still didn't diversify and still rely on government orders. (P.S. any one watched:"Office Space"? Office job is killing my soul.) I don't like having a mortgage. I don't like it at renewal time when they ask you: do you still work at this company full time etc. I hope at next renewal time, I'll say: yes but part time. Working part time without a mortgage a great way to have more time to live a more meaningful life. Today, I sold second 50% of Michael Kors positions and nibbled some Canadian REIT ,banks and Alaris Royalty Corp. . From now on, I try my best to control myself not to buy early so my cure is to nibble positions. Positions sizing is important.Being wrong on big positions is very painful.

-

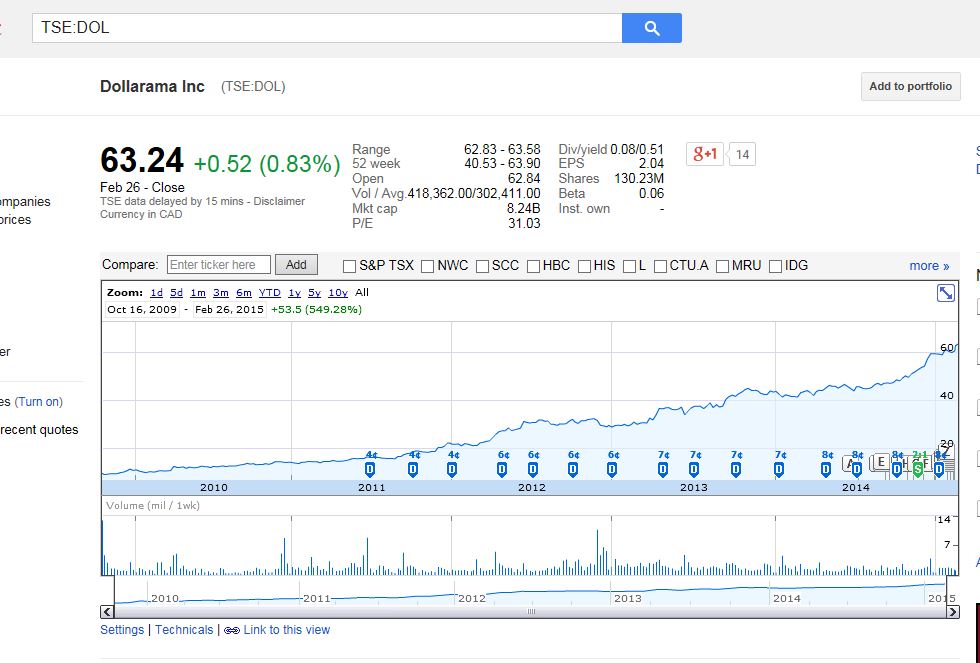

Buying Good Business with a fair price and sit on the ass is Charlie Munger Approach. He said it's better than buy high quality business with fair price than buy low quality business with a good price. It's very boring but simple and profitable. Attached is the result of 12 high quality Canadian stocks with equal weight, it generates annual return of around 15% to 20%, beat TSX by a huge margin. The result is amazing even one of them is a loser: WJX. but the result is still extraordinary. I am very tempted to put all investments into an equal weight portfolio with good businesses and enjoy my life but the problem is it's too boring. I like to do some trading.. If I do concentrate trading on value stocks, I might get +30% year and -10% year regularly. The result will be better but more roller coaster than equal weight approach. Hold quality business with equal weight removing the need to guess which will be winner and which will be loser giving a smooth and satisfactory return. I do have a small portion of investable asset in equal weight sit on ass approach. It works. The result is as expected: smooth and satisfactory, e.g. 10% to 20% per year return. What kind of business is suitable for equal weight and sit on ass? Examples are: Dollarama, CCL Industries Inc. Look at the performance of these two stocks. This is what quality means. Maybe it's not worth the effort to trade. . Maybe I'll boost the equal weight portfolio in bear market.. Buy quality and sit on ass is simple because I don't read their annual/quarterly reports. I throw them out if they mail to me and opted for electronic delivery. I just buy the stock and wait. Before I decide own a stock, I look at two most important things: 1. The product and service. 2. The important numbers on the balance sheet

-

Cloud, At what point do we stop worrying about diet and fitness, and just enjoy things with some degree of moderation. Worrying about it is just more stress, right? If you follow research about stress and its affect on telomeres lengths, that seems to say alot. People who care for a spouse, disabled child, or parent full time without a break have been shown to suffer from chronic stress and it reduces their health and well being immensely. Sorry to say, you shoot yourself on the foot with this. Moderate amount of a bad thing is still a bad thing. Preventing suffering doesn't cause me any stress. I don't worry about preventing suffering. I just take actions to the best of my ability. I don't feel stressful about: e.g. eating healthy, exercising,not drinking any alcohol (meaning no chance of getting in a car accident under influence of alcohol), avoiding smoking cigarettes, no texting and driving. I do see smokers become stressful when they are suddenly cut off from cigarettes. The ability to say no is a key indicator of success in all areas of life. Check out Stanford marshmallow experiment. Now let's talk about stress ... Some people don't care about their financial health and physical health. For example, when they lived carelessly for their whole life without any consequences. Then they reach age of 60,70, after an operation, let's say to take out a gallbladder after a gallbladder attack, they suddenly can barely walk, and experience urine incontinence. (What causes formation of gallstone?) Or worse, they have cancer. Now, because they are not financially independent, they will need their children, probably at their 30s, to become care giver. That's endless medications, doctor appointments. Meanwhile their children are working full time and use up their 2 weeks vacations just to go to their parents doctor appointments. At this stage of life, their children are probably starting to think about or just started raising their own family. If their children don't have high enough income, they are been sandwiched between their own family and their parents. They are called sandwich generations. Some even are so stressful that they can't have their own family. I take care of my financial health and physical health to ensure my children will not become sandwich generations. For wealth, I'll become financially independent at age 45. For health, I want to be like Fauja Singh than one day laying on a death bed dying slowly. "I have seen something else under the sun: The race is not to the swift or the battle to the strong, nor does food come to the wise or wealth to the brilliant or favor to the learned; but time and chance happen to them all." Here's the thing, time and chance do happen to all of us. You might never touch a drop of alcohol and never drive. But what if you're walking and a drunk plows into you at an intersection? Maybe you exercise and eat only the best food but still get cancer. The fact is everyone dies. The person who shoves their face with McDonalds and never leaves a couch as well as the health nut, both die. Sometimes the health nut dies first. There are no guarantees in life. There is no magic formula. Eating perfectly and exercising doesn't guarantee a long life. Just as eating terribly and never doing a thing doesn't always mean an early death. Time and chance happen to us all. There's a stress and worry that I think is robbing some people, it's the stress of being healthy. Of never doing anything unhealthy to ensure a long life. The thing is that's just a stressful as someone who's working a high pressure job. The best way to reduce stress is to actually enjoy life! Talk a walk on a nice day, play with kids or grandkids. Go have a beer with friends. Go hiking or running. Enjoy life. I exercise myself, I like to run. I went running this afternoon. Not because I want to live long, but because I truly enjoy it. I also enjoy a good beer, so I'm having one now. Did I negate the running? I don't know, and honestly I don't care either. Here is a very personal story I'll share. My dad was the model athlete, he held a state record in a sport for years and went to college on a full ride scholarship. He played three sports in college before being forced to choose one. He stayed in shape his adult-life. My mom was into health food. White bread? Never ate it. She used to shop at some boutique health place in the 80s. So fast forward...10 years ago he was diagnosed with cancer. Then his body was riddled with arthritis, it runs in the family. He's had numerous joint replacements. The cancer was gone, then came back and gone again. He has another replacement surgery this week. He said he thinks he needs three more (another hip and two shoulders). He was strong, athletic and did nothing wrong. Yet his body fell apart. His youngest brother was just as athletic and went farther than my dad. He played MLB baseball for years in the late 70s and early 80s as a relief pitcher. Excellent shape as well, kept up with athletics and sports through his adult years. He has a number of health issues as well and hobbles around. I asked him if he could even pitch a baseball anymore, he said he couldn't. Maybe my stories are the anomalies. I feel great right now, but I'm also young. I know I might end up like my dad and have health issues in my 50s. Or I could be like my mom's family and never exercise, eat terribly and live to my mid-90s. The bottom line is this. You need to enjoy life. My guess from your post is you're young and you have the world by its reigns. You already know everything and we're probably all wrong. I just hope in 5-10-15 years maybe some of this will be remembered and sink in before it's too late. I am not know-it-all. I just read a lot and have open mind. Some people died while wearing seat belt. I still wear the seat belt every time I drive. There are many factors affect outcomes in life. I just control what I can control to produce the result I want. I don't worry about what I can't control,.e.g. DNA,accidents, or natural disasters. if trying to live a health life is a worry or stress then trying to beat the stock market is a worry/stress too. We all going to die in the end, the money is not coming with us. Why get rich then? That shouldn't we stop worrying about beating the average market return and just buy the index like most people do? No we don't, we don't want average return, so we put in more effort and get 15%, 20%, 30% / year return. To me, it's well worth it to work extra harder to get 20% to 30% return, I don't enjoy less about life from doing this. In fact, I have more peace of mind and sense of accomplishment getting 20% to 30% return. If life is a dream, I want a good dream rather than a nightmare. There are two major factors deciding our health and life span: 1. DNA which we have no control. 2. Diet and being active. If anyone is interested: How to Live to 101 - Horizon - BBC http://www.youtube.com/watch?v=mc7joeDjF84 This BBC documentary shows couple groups of people living long life and short life. There is a group living a long life due to inter-family marriage and resulting DNA anomaly. They eat lots of meat and drinks a lot and many still live to 100 in good health. There's a group living a short life due to DNA. Other groups living a long healthy life all have same thing in common: low/no meat diet and active life style: Okinawan and 7th day Adventist. Those are very happy people. I don't see them stressful at all.

-

Cloud, At what point do we stop worrying about diet and fitness, and just enjoy things with some degree of moderation. Worrying about it is just more stress, right? If you follow research about stress and its affect on telomeres lengths, that seems to say alot. People who care for a spouse, disabled child, or parent full time without a break have been shown to suffer from chronic stress and it reduces their health and well being immensely. Sorry to say, you shoot yourself on the foot with this. Moderate amount of a bad thing is still a bad thing. Preventing suffering doesn't cause me any stress. I don't worry about preventing suffering. I just take actions to the best of my ability. I don't feel stressful about: e.g. eating healthy, exercising,not drinking any alcohol (meaning no chance of getting in a car accident under influence of alcohol), avoiding smoking cigarettes, no texting and driving. I do see smokers become stressful when they are suddenly cut off from cigarettes. The ability to say no is a key indicator of success in all areas of life. Check out Stanford marshmallow experiment. Now let's talk about stress ... Some people don't care about their financial health and physical health. For example, when they lived carelessly for their whole life without any consequences. Then they reach age of 60,70, after an operation, let's say to take out a gallbladder after a gallbladder attack, they suddenly can barely walk, and experience urine incontinence. (What causes formation of gallstone?) Or worse, they have cancer. Now, because they are not financially independent, they will need their children, probably at their 30s, to become care giver. That's endless medications, doctor appointments. Meanwhile their children are working full time and use up their 2 weeks vacations just to go to their parents doctor appointments. At this stage of life, their children are probably starting to think about or just started raising their own family. If their children don't have high enough income, they are been sandwiched between their own family and their parents. They are called sandwich generations. Some even are so stressful that they can't have their own family. I take care of my financial health and physical health to ensure my children will not become sandwich generations. For wealth, I'll become financially independent at age 45. For health, I want to be like Fauja Singh than one day laying on a death bed dying slowly.

-

Let's look at this objectively. ;) INTJ INTJ Personality Type — The Strategist INTJ Strategists are private, independent and self-confident. They strive for perfection and achievement. They are gifted strategists with analytical, conceptual and objective minds. They are flexible and like to formulate contingency plans. INTJs are able to see the reasons behind things. INTJ Preferences Preferences: Introversion (I), Intuition (N), Thinking (T), Judging (J) INTJs direct their energy inward. They are energized by spending time alone. They typically have fewer friends and prefer small groups. They are private, quiet and deliberate. INTJs are Intuitive people that are always thinking and analyzing. INTJs are very deep and abstract. They are complex on the inside and see endless possibilities. INTJs are Thinkers that make decisions with their head. They are objective and logical. They are critical, impersonal and thick-skinned. INTJs are structured and scheduled. They are controlled and responsible. They seek closure and enjoy completing tasks. Describing an INTJ INTJs can often be described using these words. Analytical Structured Objective Introspective Perfectionist Attentive Controlled Private Responsible Self-confident Thick-skinned Quiet Determined Independent Impersonal Theoretical Intense Strategic Adaptable Complex Conceptual Disciplined Deliberate Abstract Decisive INTJs and Relationships Social interaction is often the Strategist's greatest challenge since it requires setting aside their strategic thinking. They are not affectionate unless they feel very safe. They do not always know how they affect others and can appear insensitive. Since INTJs enjoy deep conversations, more shallow forms of social interaction are often seen as a waste of time. They want their relationships to serve a good purpose. INTJs honor commitments. INTJs and Work / Career INTJs analyze and strategize before they act. In their work they are organized and structured. They can be counted upon. They set high standards for themselves and believe they can achieve them. Coworkers find them private and hard to get to know. Others may perceive INTJs as aloof or annoyed when in reality they are serious and intense. INTJs and Learning / School INTJs love to learn. They often excel in school and achieve all their goals. They are driven and self-disciplined. They thrive with the most theoretical and complex subjects. INTJs are in a constant quest for self-improvement, growth and self-competency. They are usually voracious readers.

-

I added the poll ! I am exciting to see the result although it's predictable one type will be majority on this board. (Like attracts like)

-

Myers–Briggs Type Indicator is very accurate at telling personality than Zodiac Sign. I am an INTJ. http://www.16personalities.com/intj-personality You can find out your type with this simple test: http://www.humanmetrics.com/cgi-win/JTypes2.asp Edit: Poll added.

-

I didn't find Security Analysis useful. Intelligent Investor on the other hand, offers an extremely important concept: Mr.Market.

-

Charlie Munger once was asked one word to describe the reason of his success, his' response? Rationality. Rationally, if I were looking for a woman as a long term partner, I wouldn't look for someone who's a party girl or who frequently hang out at the bar. I would find someone who's a good girl, smart, happy go lucky, feminine, and family oriented instead of career oriented.. i would also avoid women brainwashed by extreme feminism. Also as charlie Munger said: if you want to get a good spouse, you have to deserved a good spouse because a good spouse by definition is not nuts. In other words, if we increase our own value, we get higher value partner. There's no need to chase. Chasing something or someone we don't deserved is a waste of time. Like attracts like. The danger of letting sensors to overwrite rationality is that it can often create great suffering. Binging on junk food is not much different than binging on sex or porn. When people binge on anything, the dopamine reward circuit in the limbic system is being overloaded. If you put a male mouse to female mouse within a confined space and the male will mate with that female. After he's done, he won't repeat it. There's natural mechanism to let him rest. Then the researchers put new female mice into the cage one after another, the male mouse mates again and again.(Coolidge effect: novelty creates new desire) He keeps doing that until he dies of exhaustion. That's the problem of letting sensors become captain. The senors should be servant. Same with food, governments subsidize unhealthy food so the citizens binge on unhealthy food and become unhealthy. I don't know why they are doing it, maybe to create jobs in the health industry. Or the government like junk food themselves.

-

Do you invest in anything that brings profit? I don't. I avoid businesses that don't really benefit others. I invest in neutral or beneficial businesses. Rational thinking should overwhelm sense organs. I am big admirer of vulcan in Startrek. I am not saying all emotions are bad. I rather eat veggies and have a painless old age than indulging in meat and junk food and possibly die slowly with support of meds and medical equipment. Success in one area can often blind sight people in other areas of life. "If somebody told me that I live a year longer by eating nothing but broccoli and asparagus from now on ... every day will seem like as long. I'll stick with the Cheetos and the Coke," Buffett told CNBC in March 2010. " - It's not about living longer. It's about having less suffering. and there are a lot more to eat than just broccoli and asparagus. http://www.reuters.com/article/2015/03/25/us-kraft-m-a-buffett-diet-idUSKBN0ML2SY20150325 "Why Prevention is Worth a Ton of Cure" http://nutritionfacts.org/video/why-prevention-is-worth-a-ton-of-cure/ "Taxpayer Subsidies for Unhealthy Foods" http://www.care2.com/greenliving/taxpayer-subsidies-for-unhealthy-foods.html "Asian men who live in Asia have the lowest risk; however when they migrate to the west, their risk increases. " "Why is prostate cancer so common in the Western culture and much less so in Asia, and why when Asian men migrate to western countries the risk of prostate cancer increases over time? We believe the major risk factor is diet – foods that produce oxidative damage to DNA. " http://www.pcf.org/site/c.leJRIROrEpH/b.5802029/k.31EA/Prevention.htm

-

Not all forms of leverage are bad. Some are good some are bad. And the risks involved also depend on the amount of leverage. Leverage if used wisely can enhance return significantly. Those who tell everyone to avoid all forms of leverage is trying to keep people ignorant. Maybe they are right because many people are not intelligent enough to use leverage. If we look at leverage in investing, it always amaze me when some people are contemplating borrowing at 4% and getting a 7% return from the stock market thinking this is smart move because they are earning a spread of 3%. and they are borrowing for the long term. Well, there's not much of margin of safety here. I like to hold short term debt not long term debt. I prefer LOC/margin over mortgage. I only borrow when the expected return is around 10 times to 20+ times of interest cost and the leveraged investment's expected return can be realized within short period of time, months to 1 year. This is only possible in information age because the market is so efficient at reflecting information. Mr. Market is very emotional in the short term about what he hears. and he likes to predict what the next EPS and gets really upset if it's off by only a few cents. The more percentage the quality stock moves relative to its future value, the bigger the opportunity. If it doesn't go anywhere for more than 1 year, I consider I made a mistake.Worst case is I break even or at a small loss. I think it's very risky to do a leveraged lump-sum investment. Leveraged investment should always involves multiple entry points depending on the price movement..e.g. -10%,-20%,-30%.,-40%.. etc. i am not suggesting averaging down on a value trap! The most important factor in investing to me is quality. Price is secondary. When quality and low price both exist, it's golden. The risk is different at different price so I can have different positions for the same stock with different risk/return ratio. Overall, the returns are being averaged out and the final result mostly turned out okay. Being a small investor is a huge advantage compared to institutional investors. The bigger the portfolio, the harder it is to do leverage safely and respond to situations quickly. Here's a relevant article about leveraged investing: http://www.moneysense.ca/magazine-archive/leverage-investing-borrow-big-retire-rich

-

I bought through recession. I average down all the way to the bottom. For example, during 2008-2009, it's my first encounter with a bear market but I bought REIT ETF: XRE, VNQ to the bottom and sold them on the way up. Now I own a tiny amount of REIT because they are over valued. So it's important to always have additional funding on a short notice.

-

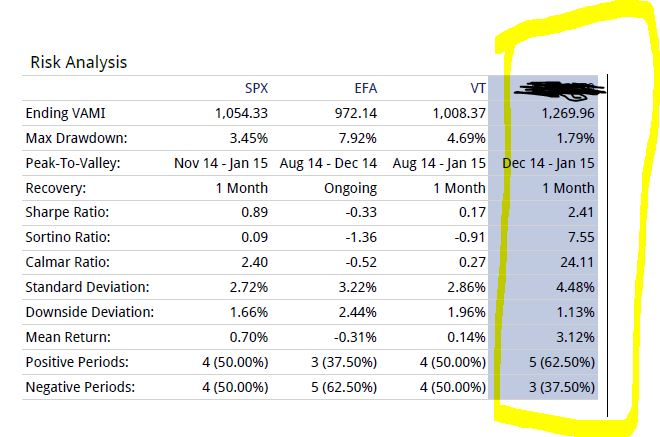

Thanks for the comment. The big volatility was caused by my concentrated value plays. This is the result of margining up to 30% of my long term buy and hold positions. The turn over rate in terms of transaction value is estimated to be around 50% to 100%. The value plays contributed to half of the return. Oct, 2014 was a crazy month. (10% jump) I didn't look into which positions caused the biggest jump. Nonetheless, even I was surprised by that big movement. I try to stabilize the return by having a reasonable exit price for value positions. I don't like to hold value positions longer than 1 year. The volatility was also reduced by selling covered calls on value plays. I am not sure I made money from the covered calls but they reduced the risk sightly. Many times, the share price jumped more than the strike price. I set the strike price so i am satisfy with the return. I have no problem letting the value positions go. Quality + value + concentration = powerful result. You said:"Your E(SD) moving forward is likely lower assuming the current SD is close to the 'true' SD value. Lot of semantics!" I can update the risk analysis couple months from now or year end and see what happens.

-

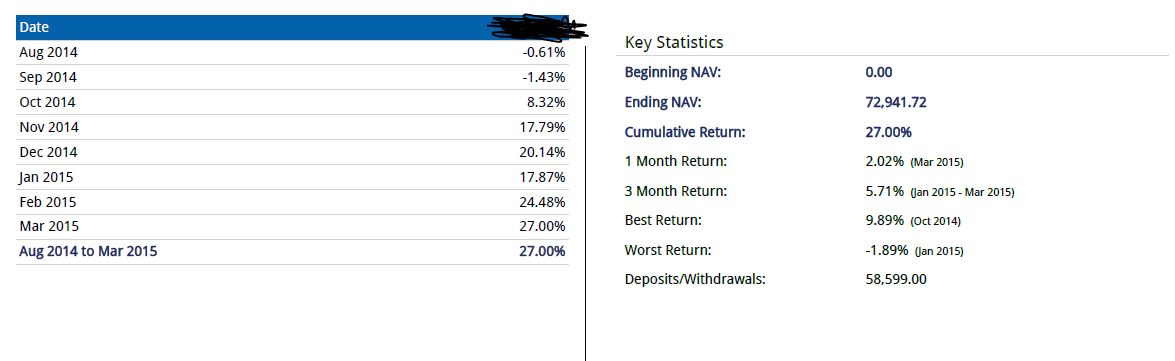

I opened my IB account Aug 2014 and just ran a report since inception. There's a return section and there's a risk analysis section. Combining these two, is it higher return meaning higher risk as they taught in school? Any comments for the risk section? Thanks

-

It seems to be the case. It's up to tax payer to take advantage to actually convert the fund. "This means that when calculating ACB, all amounts should be converted into Canadian dollars. This occurs even if you use a cash balance in foreign currency to purchase a security (as opposed to converting Canadian dollars to make the purchase) or leave the proceeds from the sale of a security in foreign currency (as opposed to converting the proceeds into Canadian dollars)."- http://www.adjustedcostbase.ca/blog/calculating-adjusted-cost-base-with-foreign-currency-transactions/

-

I have an idea to make it simple: never hold USD cash. Put the USD cash in bond or bond funds if you want cash equivalent. It's easier to keep track than USD cash. For me, my USD cash balance will almost always be negative or zero. or how to keep track of ACB of foreign currency: http://www.adjustedcostbase.ca/blog/calculating-adjusted-cost-base-for-foreign-currency-cash/

-

AFAIK. When you borrow, the USD has a cost basis based on the current XE rate. Borrow $1000 USD (at $1.1 CAD) = 1100 CAD Repay $1000 USD (at $1.2 CAD) = 1200 CAD Capital Gain (Loss) = ($100) Buy 100 BAC @ $10USD (at $1.1 CAD) = 1100 CAD Sell 100 BAC @ $11 USD (at $1.2 CAD) = 1320 CAD Capital Gain = $220 Net Capital Gain = $120 CAD In this case, you are basically hedging out the FOREX so your gain calculation is pretty easy. The interest paid would complicate things slightly. Thank your for your insight. I didn't think about the FX gain/loss when repaying the borrowed USD. It makes perfect sense now. It's equivalent to (11USD - 10USD) X1.2 = 120 CAD. But since CRA wants us to convert to CAD before calculating capital, we have to do it the hard way. I think complicated tax rules were created to create "work". To simplify things, I'll use annual FX rate instead of daily rate. I never studied currency hedging. I just do what make sense. That is locking in the elevated FX rate for portion of the portfolio,. The FX rate can go up more and I am missing out or it could come back down and I keep the FX gain. As long as it's at a relative high level, I'll keep selling USD.

-

it's more complicated for me. I borrow USD and buy undervalued US stocks. After the value stocks are sold, my gain is in USD. Then I convert this USD to CAD. Use the CAD to buy bonds. Rinse and repeat. This USD wasn't converted from CAD and its cost is the interest cost. What's my cost base for this USD in CAD? 1:1 ? E.g. Let's say for a $100 USD capital gain on borrowed USD, and I convert $100 to $128 CAD at current exchange rate, my FX capital gain is 128CAD - 100 CAD = 28 CAD?

-

Capital account vs income account and business structure

cloud replied to cloud's topic in General Discussion

Thanks! Whoever has an open mind ,be a life long learner, and critical thinker will do fine in life. It's rare to find people with open mind. Wish you best of luck too , luck as in "preparation meeting opportunities". :) While you wait, you are missing out. The profitable companies continue to earn more profit or expand, the price will follow. Don't get me wrong. Cash is important. I have significant cash position in non-leveraged account. This is a very valuable quote: "A great business at a fair price is superior to a fair business at a great price." Charlie Munger It's the core method of how I select stocks now. Because this method is so boring, I spend my spare time to find some volatile stocks and have some fun. Vitamin Shoppe Inc(NYSE:VSI) share price went nowhere for 2 years but I made 30% to 50% per year from this stock between 2013 and 2015.