rb

-

Posts

4,182 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by rb

-

This is interesting, why do you think this will be a great investment? Germany historically has had low ownership rates and stable prices. So number one there is a large rental market. 2. RE is quite cheap in German cities. 3. Due to the interest rate situation ownership rates and prices have started to tick up in recent years. I think situation will continue. 4. Cap rates are pretty good by themselves so you don't need a lot of price appreciation. 5. There are some reits that are trading around book. Also they don't take a chunk of money out for their private "administration company" which is nice.

-

As others, I don't have very high conviction after the recent rally. Two ideas that I think will work are BUD and German real estate.

-

They can do a lot of things. Convert to other currency and invest/finance ops. Make EUR denominated investments. Finance European operations. While on the surface BRK doesn't have a lot of European business. The subs do a lot of business in Europe. The insurance subs and PCP quickly spring to mind. Warren also has a history of taking debt when it's cheap. I think sometimes is just for shit and giggles, just for fun cause he can do it. The issuance is quite small and fairly short term for BRK so I think this may be the case here.

-

As far as I know in Canada IB is your best option for international stocks. As for other brokers, TD offers access to some major European markets for usurious fees. Also Questrade offers international, you have to call in the trade to their desk and fees are high - 1% of value minimum $195 and you probably get fleeced on FX. Not sure what markets they offer but i suspect the diversity is worse than IB. If anyone knows of other brokers, please share.

-

Well look... basically IB isn't for everyone. If you're only investing domestically and in low volume you'll get a better deal somewhere else. If you do higher volume or global investing and you're not looking to pay a fortune to Morgan Stanley then IB is really the only game in town.

-

IB does statement is csv

-

For Canada/Toronto I really like The Scott Mission - food bank etc. I donate to then a lot.

-

Yea some things with IB can be annoying. Account permissions among them. I hate the 2 factor login. I understand security and all but I have a stack of those cards on my desk and it's a pain in the ass. I will admit that the tax free accounts are more annoying and an inferior offering compared to margin accounts. I use another broker for a lot of tax free accounts. All that being said I absolutely love them! They have fantastic execution, great margin rat, an excellent product offering and FX, and global access (even though I'd like more EMs). You get all of this at a fantastic price! No-one really comes close. I hope they only improve from here. :)

-

Fairfax nears deal to buy Allied World for $4.9B

rb replied to eggbriar's topic in Fairfax Financial

http://www.theglobeandmail.com/report-on-business/streetwise/fairfax-financial-plans-ipo-for-company-focused-on-african-investments-sources/article33415475/ paywalled -

ok, is anyone aware aware of any pro real estate trades aside from mortgage insurers and banks?

-

maybe you could share with us some of this data.

-

Thank you kindly good sir! :)

-

Sure, go ahead and take a shit on Canada. Everything's perfect in your non-socialist country right? Land of milk and honey. Everyone is happy and no one is wanting. You sure never had a real estate bubble with your non-socialist efficient markets and all right? Did you have anything useful to contribute to the discussion or did Socialist Canada just blue screened you and you did a memory dump?

-

Right on cue. Now Tim Hudak is calling for the government to lend down payment money to people - i.e. no money down mortgages. Remember, this was the small government free markets guy. https://www.bloomberg.com/news/articles/2016-12-21/lend-millennials-cash-for-houses-ontario-realtor-chief-says

-

Switch to Stella or Becks!!! own BUD now ;)

-

The stock market can up without any change in other assets. Let’s call the cash in all other assets cash on the sidelines. If I take some of my cash from the sidelines and buy a stock from you, I now have the stock and you have cash on the sidelines. The cash on the sidelines has not changed even if the price of the stock has increased. Absolutely spot on! A lot of people have trouble comprehending circular money flows. I keep hearing things like people are moving into stocks. No. Unless they're buying public offerings then if someone is moving into stocks then someone is moving out of stocks.

-

Both Newmarket and Hamilton seem to be inside the Greenbelt. But that doesn't really matter. If there is insufficient supply in Toronto, there will be spillover to Hamilton and Newmarket. If the Bud factory goes on strike, Coors will be in short supply too. So in your view Toronto prices are going up because it is supplied constrained. Then prices in places that are not supply constrained should go up as well? That makes no sense. You analogy is also bad. A strike is a temporary event. A better analogy would be that bud decides to stop selling beer in America. In that case what you'll have happen is coors will build more factories to supply bud's former customers. In the meantime some people will switch to wine and spirits. You won't see beer gain market share as the home ownership rate is going up in Toronto.

-

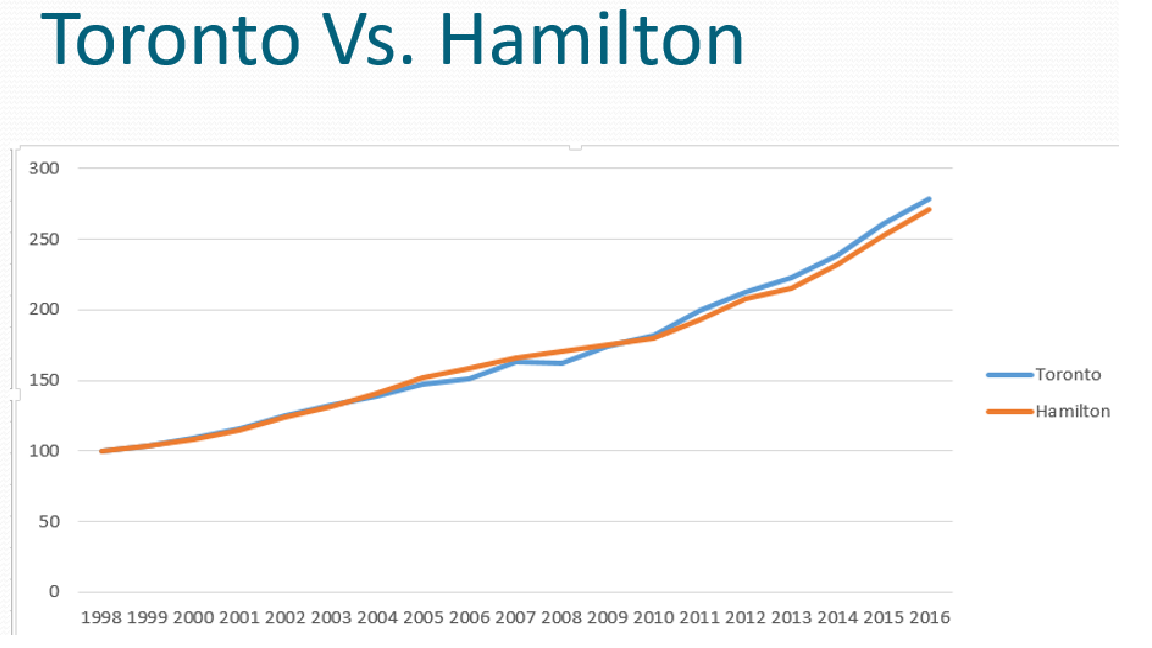

Firstly, anecdotes regarding mortgage underwriting are relevant because mortgage underwriting is centralized and automated at the big banks. If it works for one it works for all. Secondly, it's easy to just repeat the words green belt and supply without actually backing them up. If the green belt is causing supply shortages and prices to go up then why have prices in Newmarket (outside the greenbelt) have kept pace with prices in Richmond Hill and Toronto (inside the belt). If what you say is true then prices increases should be bigger in Richmond Hill and lower in Newmarket. However that's not the case. In addition, how do you explain Hamilton? It doesn't have a green belt and price action in Hamilton has been highly correlated with Toronto. Plus Hamilton is far from a beacon of economic prosperity. I've attached price action for Toronto and Hamilton for the past 18 years. Thirdly mortgage rates have helped but not as much as you thing. I see that today some banks have 3% promotional rates for 5 yr fixed. That seems a bit low. They were higher when I renewed my mortgage a couple of months ago. But let's go with 3%. When we bought the house I live in now (a semi in a Toronto suburb) in 2004. We paid 280K, put 20% down, took out a 5 year fixed mortgage @ 4.5% with a 25 year term. Our monthly payment was $1,245. Right now our house goes for about 650k. If one was to take out the 3% promotional rate and put 20% down, the monthly payment would be $2,458. So it's a massive increase in cost even with the lower rates.

-

Fairfax nears deal to buy Allied World for $4.9B

rb replied to eggbriar's topic in Fairfax Financial

He sounds like a cartain manic depressive fellow I want to sell some shares to... really strange. Yea - This is getting bizarre. I don't have any issues with the acquisition in and of itself, but the 180 degree turn on the U.S. markets as the result of the election with no commentary on rising rates, falling liquidity, strengthening dollar, declining corproate profits, levered corporations, and valuations that appear excessive certainly seems strange. If you read what he's said carefully, he hasn't done a 180 on the US markets but on the US economy. The hedges were not mainly explained in valuation (e.g. CAPE, Tobin's Q) terms. They were explained in terms of protecting the company from another 1929-33 type selloff, which would have destroyed the company in the absence of the hedges. They now feel that that kind of catastrophe has reduced in probability, because we have a quantum shift from a world in which politicians over-regulate and rely on central bankers to promote growth via leverage, to one in which (maybe) government gets out of the way and productivity drives gdp. So the hedges have gone. Doesn't mean they think the market goes up. All they've said on that front is that it will become a stockpicker's market again. Value starts to win again. I have a problem with this idea that productivity is suddenly going to go up and all ills are cured because of the election. This implies something along the following lines: As a business owner I have a project that I can execute that would that would improve productivity of my labor force and I can make me more money. Interest rates are low so I have cheap capital available. But I don't execute the project because I don't like the guy in the White House? In addition economies are large and complex mechanisms. They don't turn on a dime. You don't go from deflation risk and possibility of a great depression just because you had an election. The risk of a stock market crash definitely doesn't go down after you've had a 100% or so rally in stock prices. Others here have said things along the lines of just go with it and don't ask any questions or Prem has a master plan that shouldn't be disclosed, trade secrets etc. Please! Managements are accountable to shareholders. Strategies reflect management thinking and should be disclosed. More disclosure is required when those strategies go bad and when they are dramatically changed. Take Berkshire for example. Their strategy is well defined and well communicated. They say what they will do and do what they said and it works. The fact that the strategy is public doesn't prevent them from implementing it. If Berkshire did something radically different like go and drop 50 billion on airlines or buy Twitter you can bet we'd get a way more detailed and reasoned explanation then "Trump won the election - problem solved". So in 2010/2011 the strategy was buy quality companies at attractive prices (remember the big 3?), hedge the long portfolio and hedge against deflation (a macro call since the hedges were outsized relative to FFH risk). This was based on a view the the economy will stagnate and would be at risk of recession. Ok this is quite reasonable for an insurance company in the 2010 environment. Then they go ahead and ditch the quality companies and buy duds. Ok maybe they've made investment mistakes we're all allowed one or two of those. But one should acknowledge the mistakes, learn and correct. Then we get back to the hedges. The economy in 2014/2015 was different that the one in 2010. They look at the facts and decide that the hedges are still appropriate. They don't take even a reduction. Now you get the election and it's 180 change? I'm sorry but "Trump won the election - problem solved" is just not good enough. -

I'm sorry but I'm not buying the lack of supply story. I'm not very familiar with Vancouver but I am with Toronto. Firstly, why is it just now that supposedly supply has become a problem? Why wasn't it a problem in the 90s? Vancouver was land constrained back then too. In the Toronto area there has been a ton of development. I don't have time right now to pull historical housing stats but they're a lot higher than the 90s. So why wasn't a supply shortage back then? If a lack of housing supply is what's driving up hose prices then why haven't rents matched home price increases? In addition it wasn't just Toronto that prices have gone up a lot. The whole GTA moved in lockstep. Even moving out the the GTA you see the same thing. Over the past 12-14 years price performance in Hamilton has been almost identical to Toronto. Is Hamilton supply constrained? The is no data for cities that are further away but priced have gone up a lot there as well. In Brantford (110 Km away) semis now go for 300k. In St Catharines (120 KM away) single family detached is going for 500k. Underwriting is theoretically supposed to be strong. But I have my doubts about that as well and there have been lots of documented cases of mortgage shenanigans . If that was true you'd expect mortgage approvals to go down as house prices move up a lot faster than incomes because less people would qualify. A personal anecdote: A couple of years ago my sister was making 45k pre tax and didn't have a long or even continuous employment history. Her bf (not married) was making another 40k pretax self employed (read no income verification). They were able to buy a 500k house with 2% down. The mortgage was underwritten by a major bank in branch not through some shady broker. That doesn't strike me as tight underwriting.

-

Do you know what trades they have to take advantage of this?

-

I'm a day and a half drive from Omaha and generally drive to the meeting. It's pretty cheap that way and on the way back I generally stop in Chicago for a few days to take in the city and do some client entertaining. Flying into Omaha around the meeting is expensive. It much cheaper to fly somewhere else and drive in. Places you could fly in are Chicago (about a day drive to Omaha), Des Moines (2 hour drive), or Kansas City (3-4 hour drive). I guess you'll have to look at prices and times and figure out what's best for you. One piece of advice I can give you is to book EARLY. Especially the hotel. Otherwise you'll end up staying in a dump and pay a lot for the privilege. The downtown hotels are pretty expensive. If you're not fixated on being downtown. I'd recommend the Sheraton Omaha at 655 N 108 Ave. It's a nice hotel, price is good, it's close to Borsheim's, free parking, has a shuttle to ChenturyLink Center (15-20 minutes) and has free breakfast and other freebies for BRK shareholders.

-

Surprisingly I have some free time this afternoon so I went to pull some data for you guys to build on my previous post about the economy. Here's prime working age participation rate. It's about 1-1.5 points of previous peak. It has actually been slightly declining for since the late 90s so max participation may actually be lower than previous peak. But of course we can't know that for sure. https://fred.stlouisfed.org/series/LNU01300060#0 Regarding underemployed etc. Here's U6. It is also about 1 point away from it previous low. https://fred.stlouisfed.org/series/U6RATE Here's NLF Want a job now. It's about 1,000,000 people off the lows which is also about 1% of unemployment. https://fred.stlouisfed.org/series/NILFWJN And of course the headline unemployment - 4.6% https://fred.stlouisfed.org/series/UNRATE Basically if you look the data is pretty consistently telling the whole story. The US is basically at a point where it still has some slack but not that much. At current growth rates it is chewing through the slack and it's not far off from full employment. As an aside by looking at other data not posted here. I'd say that where there appears to be a problem is young people. Actually younger people may be a large chunk of whatever weakness there is in the aggregate employment numbers. Can't say more right now because I need to do more research on that. Just a mental note.

-

Well is there economic slack in the US economy? Yes. But a lot less than has been in the past. Even at current growth rates the US economy is chewing through the slack pretty well. This means that current growth is larger then potential GDP growth. The latest GDP growth print was around 3% even that is unsustainable for the US over more than a relatively short period. The idea that growth will accelerate from here and be sustainable for some period of time is just not based on facts.

-

Fairfax nears deal to buy Allied World for $4.9B

rb replied to eggbriar's topic in Fairfax Financial

+1 In the past at least he used data and logic on the macro stuff. There was a legitimate argument for the deflation hedges back in 2010/2011/2012. Not so much for the equity hedges but still. Now he's doing macro calls by feel based not on data but on what someone who lies a lot said during a political election campaign. Then he uses the new calls to make large acquisitions. Oh boy!