vinod1

-

Posts

1,667 -

Joined

-

Last visited

-

Days Won

4

Content Type

Profiles

Forums

Events

Posts posted by vinod1

-

-

This is the Great Imaginary Financial Crisis (GIFC) of 2023.

It seems a lot of people just realized that bond yields and bond price are inversely related and particularly this seems like a magical revelation among the tech bros.

Banks are in good shape. As always, any bank that has a run will collapse. If a bank has a run and still does not collapse, it is doing something wrong.

If we are going to have financial drama, I am all for it.

-

8 hours ago, Viking said:

i agree that insurance is different from banking. Here is the piece i do not understand… when interest rates were falling the past 5 years to essentially zero in 2020/2021 did all these P&C insurers not book massive ($billions) in gains on their fixed income holdings? It looks to me that when interest rates were falling the gains from most of the fixed income portfolio flowed through the income statement and book value. I would have expected that in Dec 31, 2001 there should have been billions of gains sitting in the ‘held-to-maturity’ portfolio at all these insurers.

But now that interest rates have spiked higher massive losses are suddenly showing up… and have conveniently been tucked into the ‘held-to-maturity’ bucket so losses do not flow through the income statement. Is my understanding correct?

Essentially, the gain (from cratering interest rates) is allowed to flow though the income statement but the loss (from spiking interest rates) is not allowed to flow through the income statement?

There is a logic here i do not understand. If anyone has an answer i am all ears.

There is a difference between Statutory Accounting Principles (SAP) used by insurance regulators to assess an insurer's viability vs. GAAP which focuses on financial reporting of economic profits.

SAP is more focused on solvency and per my understanding uses amortized cost not MTM. GAAP allows either based on HTM or Trading Assets and profits are reported based on this classification.

So yes, to the extent that any insurance company did not use HTM, they would have booked gains and now have to book losses. But insurance regulators are not looking at GAAP book value, they are looking at Statutory Surplus (Statutory Book Value if you will).

Many P&C companies have 5-6 year on average for payout. So any given year you are looking at 15%to 20% of portfolio that needs to be liquidated at a maximum and that if the company is in runoff. Most likely it is at least maintaining its book of business which means that much in cash in coming on for new investments. So I do not see much impact from bond losses to P&C companies.

Even if you assume they liquidate 20% of bond portfolio and that fell 15%, we are talking about a 3% hit to overall portfolio. Simply no way P&C can be compared to a bank which is subject to runs.

Most P&C companies use ALM strategies. In fact that is a core function. Their payoffs closely match the bond portfolio.

My biggest position is FFX for little over an year. First bought sometime in 2005/6/7 I think at $106, completely exiting in 2011 at $418, sat out most of the last decade except for a cigar puff buy and sell for tiny bumps. I did not trade any stocks in all of 2021 and did not look at the market and hence did not realize how cheaply it was trading. I went to all index in 2020 soon after the pandemic to focus on my kids as I knew if I have any individual stocks I would sucked into spending a lot of time on 10K's. I again started looking at individual stocks in 2022 and bought FFX again and this time, for a longer term hold.

I am not arguing FFX strength at this time. But that does not mean other P&C companies are somehow in trouble.

-

15 hours ago, Viking said:

Happy to add to my already oversized position in FFH today. Price traded at $635 for much of the day. Stock is down 9% off its recent highs. BV is $658. My guess is they will earn $130/share in 2023. My guess is Q1 earnings will come in around $35/share. They paid a $10 dividend in January. So my guess is March 31, 2023 BV will be about $685 ($658 + $35 - $10 = $685).

But what about its $38 billion fixed income portfolio. Rising interest rates over the past year must have resulted in billions in held-to-maturity losses… right? Wrong. As crazy as it sounds, Fairfax fixed income portfolio was positioned perfectly on Dec 31, 2022. It is a big, big WINNER from rising interest rates. It is better positioned than any large financial institution i know (bank, insurance etc).

Most insurance companies are sitting on billions of held-to-maturity losses right now. These losses did not flow through the income statement. These losses did hit book value (so most now prefer to report ‘adjusted book value’). Yes, the held to maturity losses don’t matter. Silicon Valley Bank thought the exact same thing 10 days ago… and it didn’t matter. Until something happened THAT NO ONE THOUGHT WOULD HAPPEN. Well, now all those held-to-maturity losses do matter. so much so that Silicon Valley Bank is out of business and its shareholders have been wiped out.

An accounting gimmick resulted in poor decision making at financial institutions (they did not manage their interest rate risk properly). That is now resulting in a loss in confidence in the financial viability of many financial institutions. An interest rate risk has quickly and unexpectedly morphed into a solvency issue.

It will be interesting to see how investors discount held-to-maturity losses on insurance companies books moving forward. Insurance is different? Really? That is what banks thought 10 days ago too. And it was right. Until is wasn’t.

I would imagine insurance regulators are probably better understanding which insurance companies a have large held-to-maturity losses sitting on their books. Does this force more conservatism at insurance companies moving forward (i.e. slower growth)? Does this extend the hard market? Bottom line, financial system panics are never a good thing.

So at a share price of $635, Fairfax shares are trading at a P/BV of 0.93. Cheap. For a company that is poised to grow earnings by $130 in 2023. This is an effective earnings yield of 20%; or a P/E = 4.9. That is very cheap. And a company that is a big winner of rising interest rates…

I hope the stock keeps going lower in the current financial panic. Fairfax stock has become the gift that keeps on giving (rising stock price with big swings happening 2 or 3 times a year).

Insurance is really different from banking. The insured cannot claim hurricane damage for the year and ask for the money to be paid. The liabilities are pretty predictable. That is why ALM is a big deal at P&C's.

-

On 3/14/2023 at 12:31 AM, gurjot said:

good year all around including exclamations! and modi praises!

The level of ass kissing is nauseous. Cost of doing business in India.

-

It is said that the last refuge of scoundrels' in patriotism.

I find the last refuge of underperforming investment managers/investors is blaming the fed. Low rates, fed is enriching the rich. High rates, fed is hurting the poor.

The fed did get a few things wrong. Some of their choices are a bit baffling, but not entirely so if you can just try to think from their point of view. I think they are doing a wonderful job. Perhaps the best of any government institution in USA.

-

4 hours ago, Castanza said:

It's a tough thing to do as the culture the last decade has been "Why pay off loans or hold cash when you can get 7%+ in the market?". Nothing wrong with that thinking, but people miss the stress and fragility that can come with "high capex" lifestyles. Wife and I put investing 2nd to debt and had a goal of paying everything off by 30. Paid the house off this past year and live completely debt free. Feels great not being owned by anyone and not can focus completely on savings and investing moving forward. Did I sacrifice some solid returns but not going 100% in investing and making minimum payments on low interest debt? Yeah I sure did, but you can't put a price on peace of mind. Just my two cents.

I agree completely that you should do what gives you the most peace of mind. After all what better use of the money?

That said, you are leaving a lot of money on the table. If you have a $500k mortgage at under 3% rate for 30 years, you are going to have about $500k less after 30 years due to this - using average balance over the years and 4% higher rate of return than mortgage rate.

Also you still have the real estate taxes that need to be paid. So it is not exactly free and clear ownership even if you paid off the mortgage. It is only a question paying less.

Personally I get a kick out of knowing I am paying 2.5% rate, as even the most credit worthy Governments cannot get this rate for most of history for borrowing over 30 years.

-

-

3 minutes ago, mike_3772 said:

"that Jamie Dimon must be the only person still around at that level in US banking - hopefully his long memory is intact and matters."

They first begged him to buy Bear, Stearns. Then they forced him to take TARP warrants he neither needed or wanted. Then, forced him to settle claims from the Financial Crisis of around $22 billion dollars (during the Obama administration). I wonder if he remembers any of that?

Dimon wrote in one his annual letters that when the Fed asks him to buy out another financial entity he would say "No Thanks".

-

Almost! 20 percent! increase! in! exclamation! points! from! 2021 AL!

27 to 32!!!!!!!!

-

It is bit concerning to think

15 hours ago, stahleyp said:I believe all too often people add unnecessary complexity to a topic and it makes for less rational thinking. So don't get too hung up on human rights and slavery.

Keep in mind the key to morality either lies within society or outside of society. The ultimate question really boils down to what is the source of our morality/moral intuitions/moral compass? Or as I like to say, is there a Moral North Star our moral compasses point to or do we simply follow whatever our wishes are? Remember, if there is no North Star there can be no South Star either (ie immoral action).

Savery is just a topic that people are more emotionally invested in. You can make the same argument with things like Nazism, honor killing, outside of the norm sexual relationships like in Ancient Rome or Ancient Greece, etc. Literally we find "evil, bad, wrong" can apply.

I'll go on record to say that if God doesn't exist, all of those aforementioned things are okay because each society ultimately creates their own rules for morality. It is irrational to judge those society's and their made up standards to our made up standards; therewould be no defining Absolute Standard against which to measure. Ultimately there is no right or wrong beyond mere opinion if God is simply and only human idea.

That's why I think it's funny when atheists think there is a "right thing to do" in any way outside of arbitrary opinion even they, in some cases want obedience. They demand definitve evidence for God but demand no evidence whatsoever for their "magical morality" that we "ought" to follow.

OMG! The only reason you are not murdering your neighbors and raping women is because the Invisible Man said so? If for some reason, they were not mentioned or if there is a over-the-air update to the rules from the Invisible Man in the future which allows these things, you would merrily go along?

-

Buffett has never let his macro views influence how much of his portfolio would be in stocks versus cash. Even when he went out of the way to warn about high valuations in the broad market, possibility of sustained high inflation, and large dollar devaluation, he did not let these concerns influence his portfolio. In retrospect, it is clear that he would not have had his record if he sold out of stocks every time he thought the market or even his holdings were fully priced.

The perfect example is in 2009:

We’re certain, for example, that the economy will be in shambles throughout 2009 – and, for that matter, probably well beyond – but that conclusion does not tell us whether the stock market will rise or fall. -Buffett

-

55 minutes ago, changegonnacome said:

What did we say before about profits?........something about them getting whacked I think? To standstill at this ~4000 level the only option is to keep paying higher and higher multiples for lower and lower earnings.........expanding multiples you say, we've done that before? Yeah I agree....but this aint the 2010's with ZIRP stretching out as far as the eye could see....we are now in IIRP (inflation interest rate policy!)....the old time math says that with interest rates rising on risk free or less risky fixed income alternatives....one should, all things being equal, be paying less of a multiple for earnings on equities. Maybe Buffet got confused with all that gravity talk before

Perhaps Buffett is confused about these too...

Don't pass up something that's attractive today because you think you will find something way more attractive tomorrow.

or

Charlie and I don’t pay any attention to macroeconomic predictions. We don’t know the future of the “macro” and I can’t remember a single investment decision that hinged on the macro. We have a little conceit, that if we don't know, who would? But people do it all the time: talking about the macroeconomic future—but this isn’t productive. They don’t really know what they’re talking about. To ignore what you know to listen to what someone else who doesn't know, doesn't make sense. People will do well if they own solid businesses (if they didn’t overpay). If they attempt to time their purchases, they will do well for their broker but not for themselves.

or

Charlie and I continue to believe that short-term market forecasts are poison and should be kept locked up in a safe place, away from children and also from grown-ups who behave in the market like children.

or

A different set of major shocks is sure to occur in the next 30 years. We will neither try to predict these nor profit from them.

or

Forming macro opinions or listening to the macro or market predictions of others is a waste of time. Indeed, it is dangerous because it may blur your vision of the facts that are truly important.

-

There is a good article that is worth reading called "What if You Only Invested at Market Peaks?".

Basically about a guy who saves all his money up to that point and ends up investing just the day before start of the last 4 major bear markets and what his results where. I did not check the data but passes the smell test.

https://awealthofcommonsense.com/2014/02/worlds-worst-market-timer/

-

Read Grantham's latest. His fair value for S&P 500 is 3200. His assumption on required return is 6.5% real (not stated in article but I have been following him for 20+ years and understand his methodology). So about 9% nominal. Change to 8% and fair value ends up being 3600-4000 range which is my estimate.

Vinod

-

There is no government manipulation of inflation data. It is just a difficult thing to measure and the bureaucrats actually do a pretty good job. One of the few.

Inflation is highly personal and each of us experience differently. As they say our personal experience trumps any data. I bought a Camry LE in 1997 for $19,500. Another Camry LE in 2011 for $20,000. PC's, phones, cameras, etc. All cheaper and better. There are a lot of clothes, shoes and other stuff that were outsourced and quality went down but they got cheaper. They became more of a use a few times and throw.

There is a billion prices project that produces inflation figures similar to official data.

http://www.thebillionpricesproject.com/

Vinod

-

16 hours ago, TwoCitiesCapital said:

It depends -

You could buy the low coupon variants where the primary yield is the amortization to par. In that case, you're probably not going to get prepayments because those bonds are people like me with mortgages at 2.75% we're not letting go of. But you're taking more duration risk if you're wrong on rates.

If you buy newly issued, higher coupon bonds with more yield coming from the cash flow, the only way they're getting prepared/refinanced is if property values hold up - which they currently are not - because people won't be able to refinance with sub-20% equity. Those bonds will likely be money good for a few years too, with low prepayments. If you're skeptical, buy discount bonds as in the first example.

2020 basically pulled forward nearly all refinance activity for the decade IMO.

Thanks!

-

15 hours ago, Dinar said:

Go to professor Aswan Damodaran at NYU. He did and still does a lot of work on equity risk premia at various times.

I am talking about estimate for transaction/expenses/etc prior to the 1950s for holding diversified portfolio of stocks.

I follow Damodaran's work and learned more from his "Investment Valuation" book than from CFA exams.

-

Not very familiar with agency mortgage bonds but I would think that the 6% bonds would be called if rates dip again and you would end up with reinvestment risk. Please correct me on this.

Vinod

-

7 hours ago, TwoCitiesCapital said:

While this argument was made, it NEVER held water. Inflation is precisely why equities fell 20%. Equities never do well in periods of elevated inflation. They may do better than bonds pending how quickly and how prolonged the inflation is, but real returns are almost always negative.

The receding of inflation WOULD be bullish for stocks if not for the earnings/economy being the next shoe to drop.

I haven't done work on the bottom up earnings myself to come up with aggregate earnings, but I think the hot to earnings will be significant given inflation in the supply/labor chain (and the inability to pass along all of those costs), higher USD crushing foreign earnings, and rolling any debts at higher rates (though this will be minimal for the next 2-3 years).

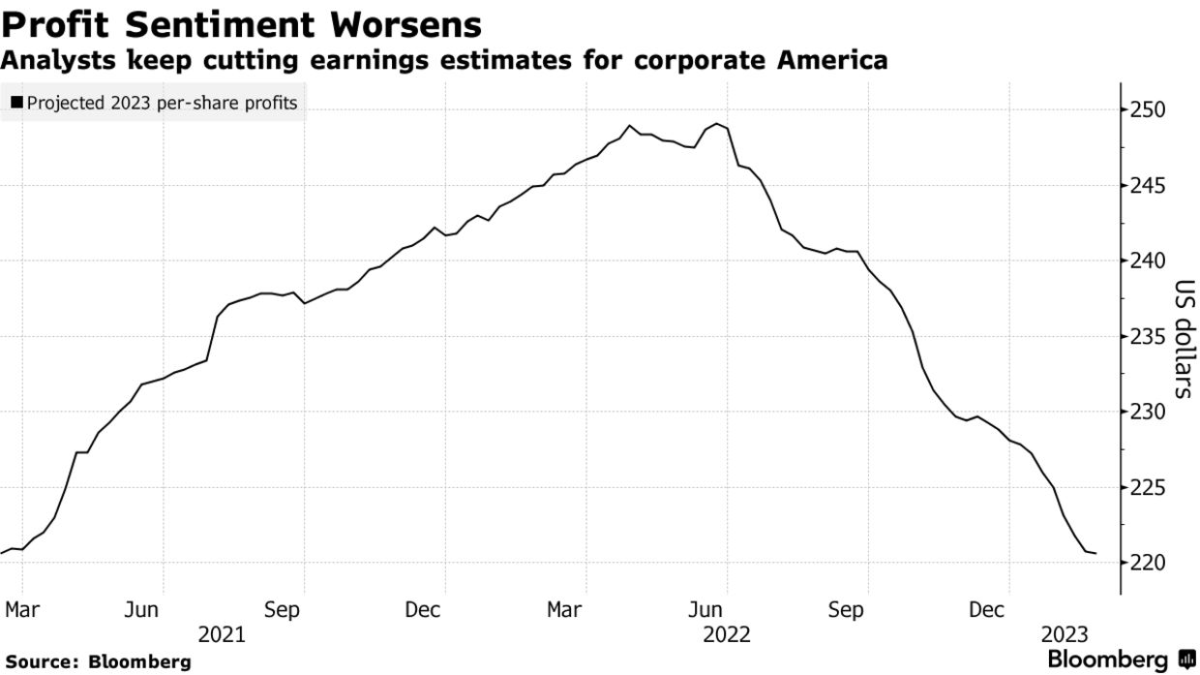

Morgan Stanley's base case is $190 with a bear case of $180. I think that under-estimates it and there one of the more bearish ones on the street. Revenue growth for the last 20 years averaged something like 3.5%. In 2021 it was closer to 12%. That's all stimulus. I think you'll see A LOT of that come back out now that money supply is contracting and we're not stimulating. If revenues fall by 5-10%, doesn't operational leverage suggest the hit to earnings will be quite a bit more than 5-10%?

Inflation is never good for any financial asset. The argument is what holds the most value long term in case of massive inflation.

Just for kicks, if you model an inflation of 10% for 20 years in US. Real GDP growth of 1 or 2%. Profit margins collapsing by half to 6% range from 12% now. PE multiples falling to 10. You still end up with 9-11% equity returns.

Not good at all.

But most likely far better than bonds. If inflation is going to be 10% over such a long period means Fed is likely not keeping rates high. In which case, cash would suck as well.

Vinod

-

7 hours ago, mattee2264 said:

For me it is still a question of valuation.

Bulls can talk about 4000 SPY being reasonably valued by using generous forward earnings estimates that seem to rest on the idea that any recession will be mild or short lived and earnings will soon surpass the 2021 peak of just under $200 a share. But 2021 earnings got a pretty massive assist from monetary and fiscal stimulus, cheap debt, pent-up demand and other favourable factors that are unlikely to recur going forwards.

The TINA argument for high valuations is a lot weaker now you can get 4% on bonds. The inflation argument for favouring equities despite expensive valuations is declining as inflation is coming down. Any economic recovery is not going to get much of an assist from fiscal or monetary policy. So I do not think you can count on earnings catching up to bring valuations down to more reasonable levels.

2022 earnings are going to come in below $200. 2023 earnings at best will probably be flat and more likely will fall somewhat. So even if you think earnings can get back to $200 by 2024 you are paying 20x two year forward earnings which is a very rich multiple.

Incidentally at the end of 2021 bulls were still talking about how 2022 earnings estimates were $250 and therefore 4800 was only 19x earnings.

S&P 500 earned $153 in 2018 and $157 in 2019. Definitely closer to peak but not a fluke or from something totally unsustainable. So let us say, an average of $155 in 2019.

Nominal GDP is 18% larger in 2022. In addition, about 4% of net share buybacks took place over this period. Adjusting for this gets to $190 per share in 2022.

The massive boost to earnings you are talking about is gulp $10 more on a base of $190! Less than 5% might a tad excessive to call it a massive boost.

Early last year my assumption was exactly like you, that there must be a massive boost to S&P 500 earnings. It just made sense, what with all the nonsense going on with SPAC, Crypto, ARK and the general sense of exuberance. But when I looked at the data, I could not make it out in the earnings numbers.

I do agree that to grow from here is going to be a real headwind.

Vinod

-

4 hours ago, valueseek said:

This makes sense but somehow I have not come across this argument being put other places. Whatever I am aware of most people peg ERP above 5%. Is there any research or document or articles you have seen this or is more your thinking/analysis? Thanks.

I was an indexer from 2001 to 2005 and thinking/researching ERP one of my favorite hobbies (isn't it sad?) and I picked this up somewhere in that timeframe. It might be something I read somewhere or it might be my own thinking but hardly any of my thoughts on investing are original.

One of the reasons I got interested in stock picking is because of the low ERP.

Anyway the argument has definitely been made by Siegal and Philosophical Economics which reinforced my own conviction (no confirmation bias, of course

). But I did not see anyone make estimates of this.

). But I did not see anyone make estimates of this.

Vinod

-

13 hours ago, Dinar said:

No, because you are assuming zero growth, or growth that is worth zero. (when returns on marginal capital = cost of capital), you are correct. When there is growth and return on marginal capital exceeds cost of capital then that justifies a higher p/e. Technically, we should not even be looking at earnings, but at free cash flow.

+1

Damodaran has a spreadsheet you can play with. Assuming $200 earnings in 2023 and 75% total payout (which is about average of last few years) to get free cash flow of $150 and using your 3% risk free rate and 3.5% ERP, IV of S&P would be 4800ish.

His model is internally consistent unlike many others from wall street. For example, long term earnings growth is limited to the risk free rate. So in above the valuation is based on S&P 500 earnings growing at 3% rate over the long term.

-

2 hours ago, changegonnacome said:

3% Risk free rate + 3.5% ERP............is a PE of 15 no?

No. Earnings yield is not your return. In a crude and approximate way you can say the earnings yield is your real return. So total return is earnings yield + inflation, again in an approximate way.

-

If the argument is S&P 500 is going down "X" percent this year because of "Y" reasons, you are just pissing over everything Buffett, Munger and Graham taught.

Is The Bottom Almost Here?

in General Discussion

Posted

Every idiot who underperforms blames the fed. This has been the theme for the last decade.