CoGreenwich&Laight

-

Posts

38 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by CoGreenwich&Laight

-

Or they didnt / cant sell their PE losers, therefore the lower performance. As of Dec 2017 they had $179MM in NCML and $333MM in Sanmar. At year end 2024, those are $201MM and $44MM. Seven years later. Those were material investments, ~20% of BV? Thats nuclear for IRR. Big positions, big losses, long time.

-

And if the Anchorage IPO is to happen, this share buyback should be accelerated and be explosive, or have a tender as suggested earlier by someone else. I like the idea of compounding with the airports value thru 100mm pax but as im unlikely to see that fully reflected in FIH, i almost prefer a trade sale, they will pay up, assuming we get a div from the proceeds.

-

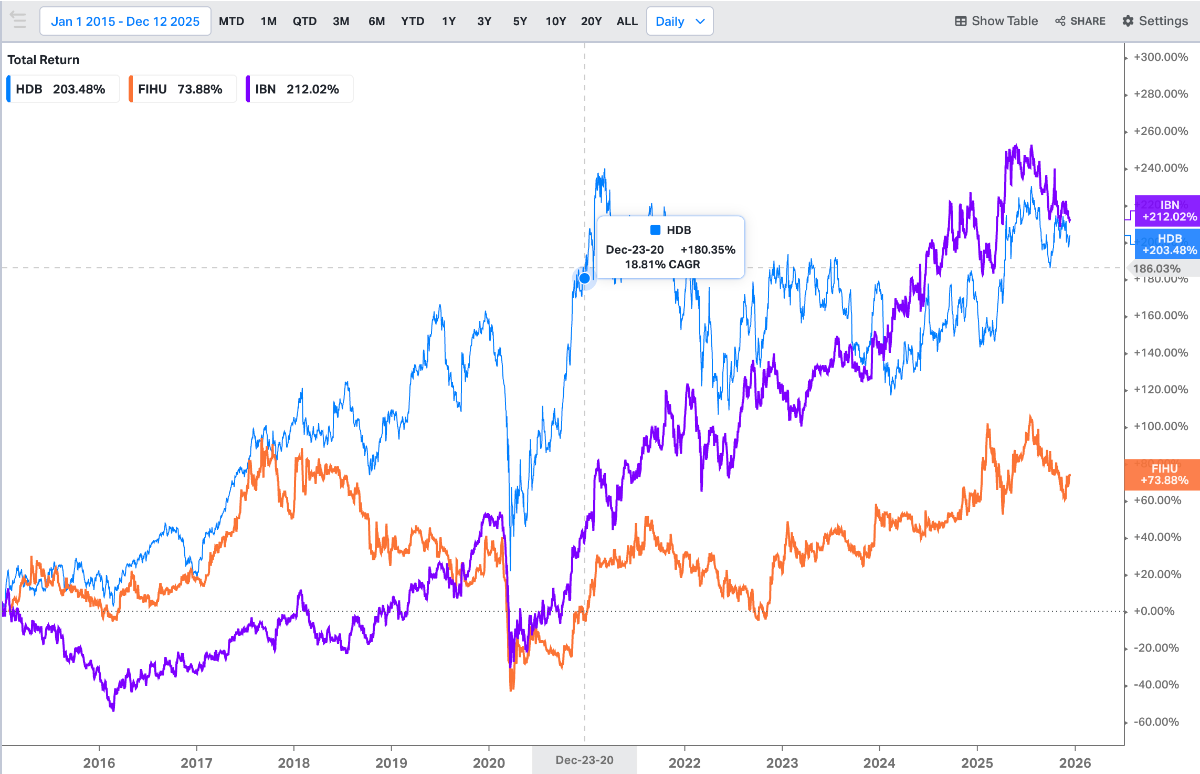

If you want financials exposure, its easily attained. In a far more liquid form. With even better performance. And no absurd, unearned leakage of fees, nor risk of reinvestment. See attached chart on ADRs of HDFC, ICICI, and the govt! owned SBI. FIH performance is pathetic. 72% over 11 years vs 204%-244%. Management should be ashamed, that they are a third of other accessible financials. They should desist from non-airport investments, divest from non BIAL investments, and buyback stock. We can get as much financials exposure as needed but not airports. This is the only way to get closer to intrinsic value. Getting involved in IDBI is unnecessary, the price has tripled since this misadventure started. It would be poisonous to the discount narrowing.

-

they havent purchased any Real shares in almost 2 years. 0.6MM shares for 8.4mm in 2024, and thru June 2025, 341K shares for 5.2MM. Bogus. But of course their fees will drop...as this reduces BV.

-

i agree with your comments. it is a play on BIAL, and thats unlikely to change given how outsized it is as a % of intrinsic value, 75%, more? For eg, if they were to buy say their last deal, Jaynix for $33mm, thats a detraction from shareholders...

-

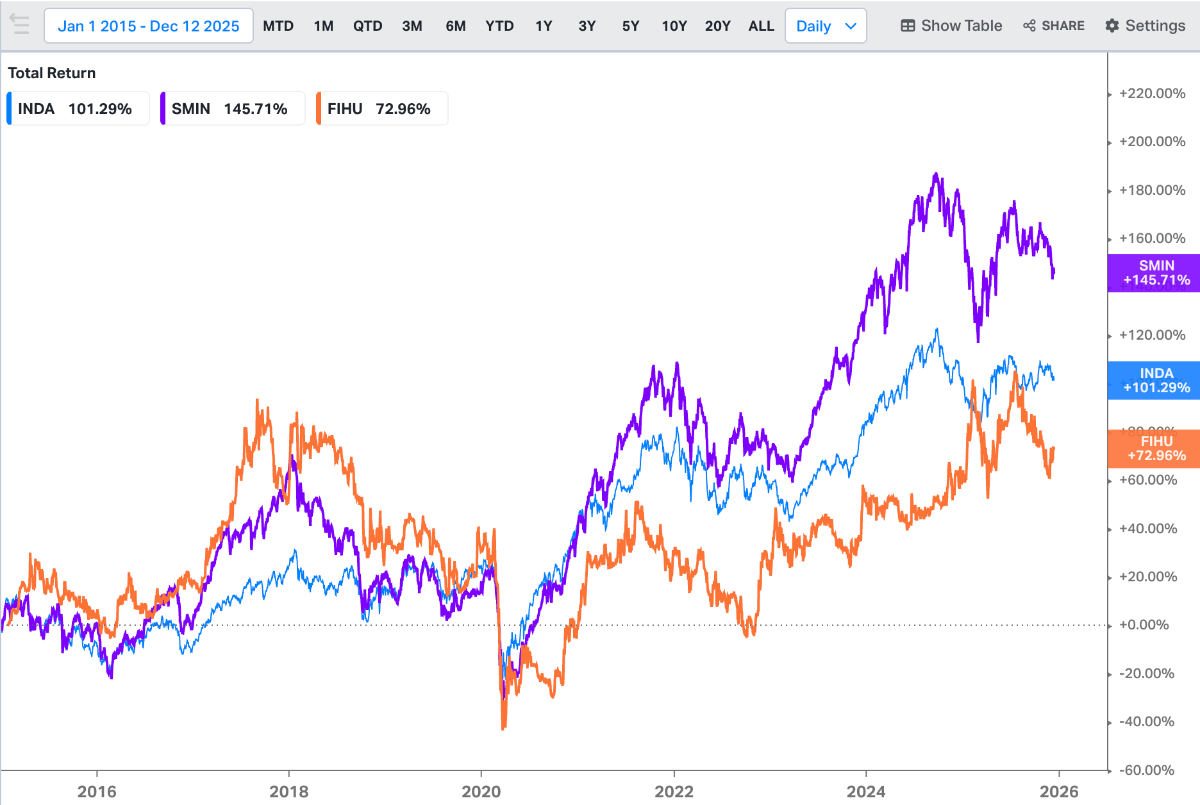

Its actually worse, those fees are in historical dollars. the share price appreciation is in current $. Yes, the first two were contractual but as a controlling shareholder with supermajority shares (unfortunately) you can autopen if you want to do the right thing. They still have that clause there. Why not signal more shareholder friendliness after almost 11 years. Below is the fees / charges, and their performance relative to two ishares India etfs. Their share performance lags ETFs. Do the fees justify the performance failure? With this history do you think the market will self correct and price this anywhere near book value given the fee structure, much lower liquidity, and rare communications with any indepth details? i urge you to consider the charts and use your voice with management. Im long plenty of shares because of the airport and air pax fundamentals in India, which will only fully be valued if mgmt changes this structure. 11 years is not cherry picking any data. FIH can be valued at the figures quoted above for intrinsic value only one way...aggressive buyback, desist from non airport investments, change structure to carve out the airport so that people who want to invest in other stuff can.

-

see my last comment for rationale on why they should not get it. Every $ invested is marked down 35% as shares trade at that discount or more. Its transparent to everyone that the airport is worth more, so the discount is greater...50%-70%perhaps. So take cash at 100% and mark it down by buying something else. Own the airport, more of the airport by buying shares, narrow the discount, its the bet thats bailed them out, while other material ones have failed and other minor ones dont matter.

-

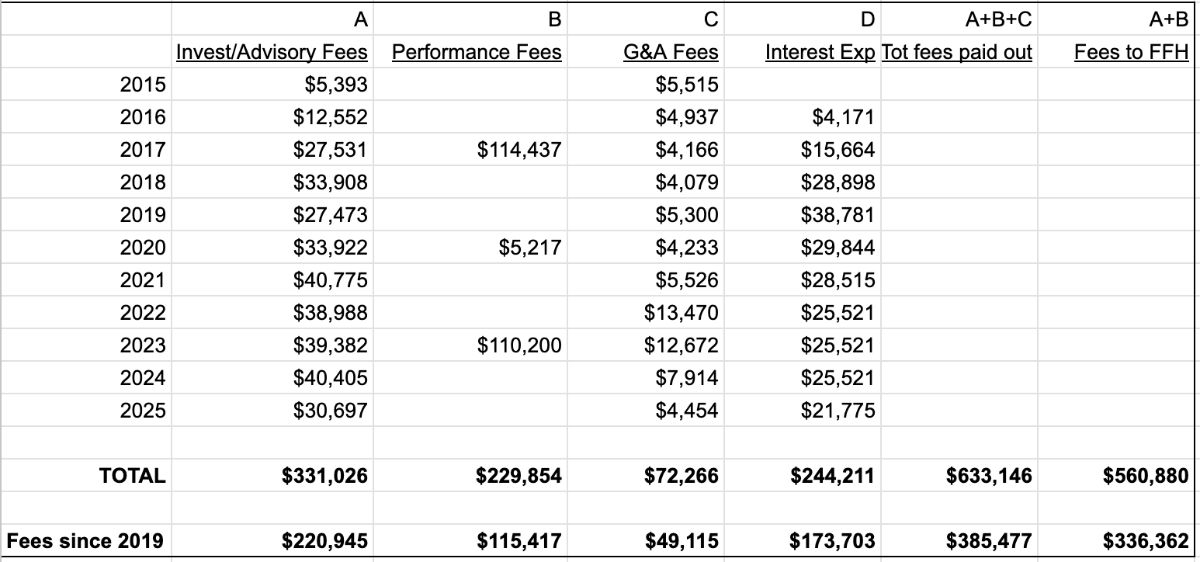

Yes, they are quite excellent at marketing and waxing lyrical on investment philosophy. Lets look at the numbers. Its been 11 years now since launch. BVPS has compounded at 6.7%. If you mark the book up to $26 for addl' value to BIAL, the cagr is 9%. But one cant eat book value, the share price has compounded at 4.7%. Does that reflect 'ocean that is full of opportunities' seized? yes, the ocean is there, the fisherman is faulty. While shareholders have compounded at 4.7%, with no dividend, FIH shareholders have paid out $633 MILLION in fees (investment, advisory, and G&A), of which $561MM is to FFH. And further have paid out $244MM in interest, to hold a cash heavy balance sheet to pay fees on the cash balances. And all this to match an SOE heavy, large cap index they choose. That being aside 6.7% or 4.7% or 9% doesnt reflect a risk adjusted return to invest in India where the base rate for the most part has been at 7%, compared to just over 4% for the USA. It is what it is, they've bombed on their large investments Sanmar and NCML...at their preferred marked up price. BIAL can be a home run. Thats all they should own. So no, I vehemently disagree that they've seized the ocean of opportunity you refer to, and definitely havent earned their fees. I wont go into this more further till i hear the push back on the facts. The structure has failed therefore the 4.7% return to shareholders, the investments have failed if they are anything under 15% net, which is their target per PW. Just the facts through the fog of marketing and celebrity worship.

-

Thanks. I'd much prefer that FIH buys back their own shares more aggressively than this co-investment with a minority stake as it will likely have to be given the price tag. Owning more airport/share is the best use of capital given the discount the shares trade at to NAV. Cant wait for this long drawn out hallucinant misadventure to fail for FIH...which has impaired their ability to buyback their own stock, and their political capital to execute on the Airport and related promises.

-

BIAL stakes would be consolidated into Anchorage pre IPO is my understanding per PW comments this year. BIAL should be valued differently from Anchorage, as Anchorage is the vehicle for further infra transactions (airports ++).

-

From my understanding, it is Anchorage that will go public, with all the BIAL equity. However the stakes from Siemens and a bit from earlier are outside of Anchorage. If i have this right, i wonder whats the process of valuation for injecting the non Anchorage BIAL stake into it, as the other valuations are seemingly 'stale' and 'low'.

-

likewise...all of the last few weeks in fact...

-

I was curious as to why FIH was able to purchase the two 10% stakes in BIAL from Siemens at what seems to be materially below intrinsic / fair market value, ie ~2.6bn for 100%, ...knowing well that Siemens understands the airports economics and growth outlook intimately as they were an insider. Any thoughts?