CoGreenwich&Laight

-

Posts

38 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by CoGreenwich&Laight

-

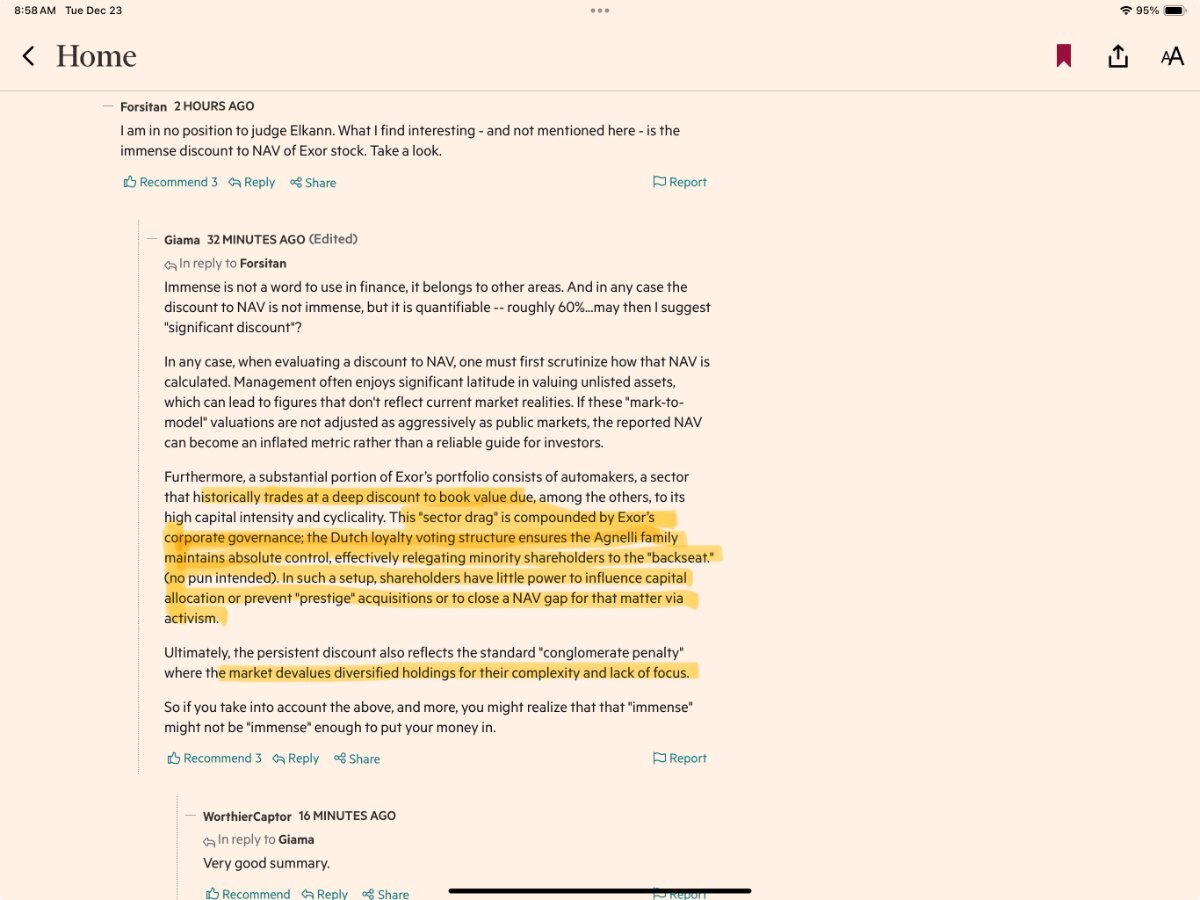

Under no circumstance is IIFL capital a better investment than FIH at these prices. With the airport at 14x current year (not forward) and no value for the real estate, it’s worth 26. With their mediocre track record of returns at best while assuming the best case scenario for the airport, they should give up. They’ve had enough time. If this was an open end fund, the money would’ve flown out. And that’s who they work for. Carve out the airport and that’s how you get full value or a much higher trading value. With its growth and returns, The airport will not trade at any discount and that’s the bulk of the value here. Rest is all crap net of their piggy nepotism arrogant undeserved fees. Prosus and Exor have shitty assets. And plenty of funds do NOT trade at a discount. See what Boaz Weinstein is doing. Read his tweets if you don’t want to deep dive. And see the path CK hutch and Jardine are going down to close the gap to NAV.

-

If I recall correctly The multiple is on “normalized cf” whatever the f that means

-

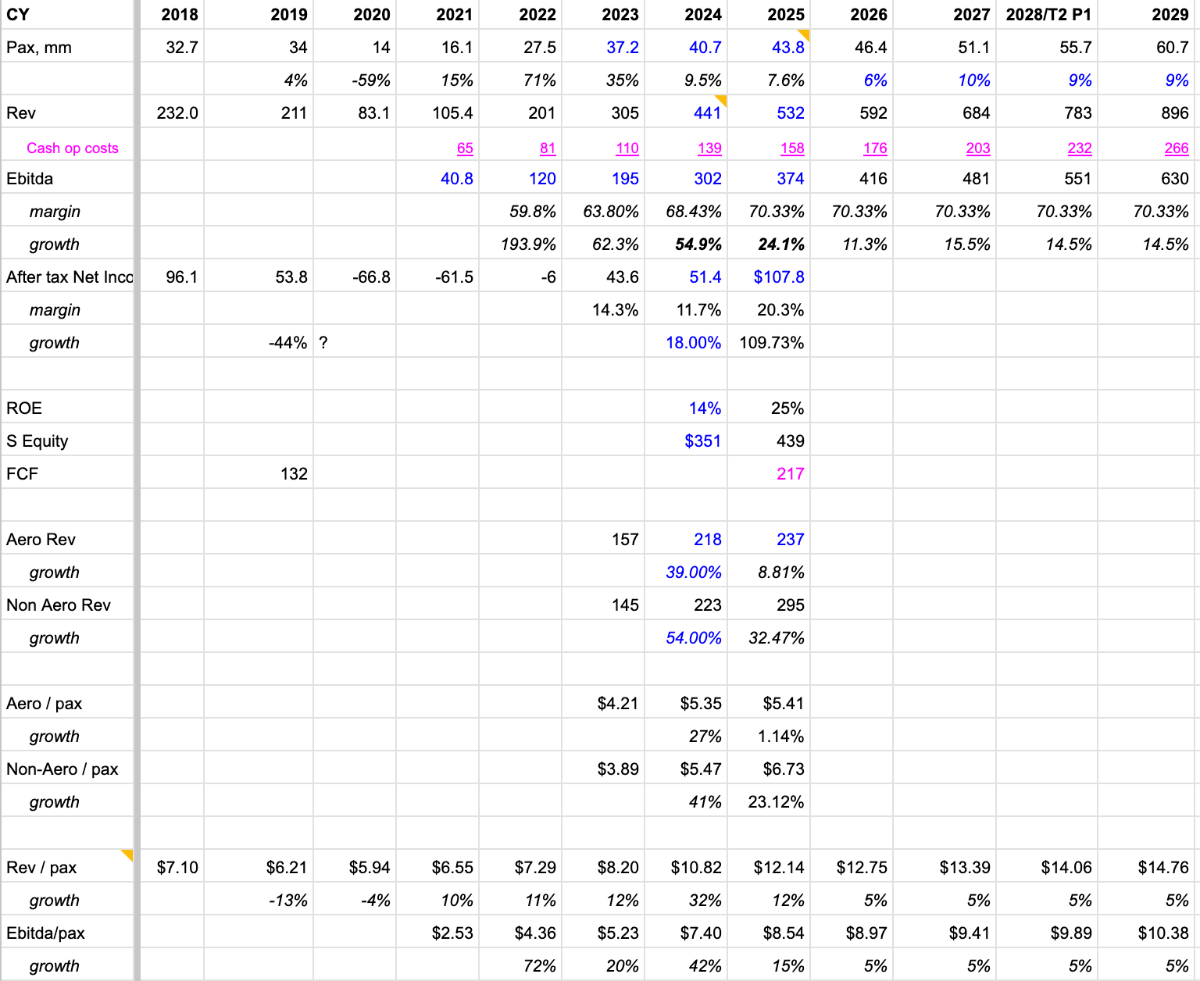

My model which deferred the cy 26 pax growth into the future due to oil/flight frequencies has ebitda of 481 in cy '27. Pre reducing pax growth in CY 26, i think i had 500mm. Some further deterioration due to INR/USD can be assumed...perhaps 3%. CY '24 / FY '25 may have 32mm USD of real estate sales (perhaps not ebitda) which i picked up from debt related doc's. But none of this is very clear. And due to macro, i dont think the IPO is happening this year. It will be deferred. So the question does remain...where will they get the $415MM they need to complete the IIFL Capital transactions...and why not do a dutch tender at $20 for FIH stock if its worth in the 30's to 50s...i just dont get it...yes, it will reduce their fees from book value but thats so dumb. They dont have any currency right now which couldve been the case if FIH traded at 'fair' value...and therein lies the reason for the discount, beholden to their decisions without any recourse, and worse any disclosure...other reasons fail. Anyone know the source of the $415mm for IIFL...? anyone getting responses from the company on this?

-

If you want to be truly complete regarding your calculations, to your 60mm you should add 10 years of fees...Unlike normal private investments that dont pay out till realization, here as you are aware we pay on their own self marked value...at year end it was being carried at 102mm...down 118 in the year, so 201 at BoY,...over 10 years bloated book and performance fees on a high % of book are not insignificant...they raised 1bn on IPO. More importantly, it would be only normal for mgmt to have quarterly calls to discuss investments like these, why the 18mm investment and then the subsequent almost immediate exit...and not leave that to us to speculate. The list of topics is endless, the tax changes in mauritius etc... Under the blankets, this is an airport asset. Even larger now of BV with this writedown. Undisputable. They should report detailed financials for the airport, like other normal airport companies, take quarterly calls to explain the movements in pax movements and YPPs (and its build ups), the impacts of Indigo and AI issues, new horizons etc... Its not accretive to blindly defend this mgmt a la the Trump cabinet as many on this site do. Most of those defenses are pavlovian, illogical and devoid of facts, and they are done by severly conflicted people including those who own 11x more exposure in FFH than in FIH as they proudly self disclose. They are like the raving mullahs looking for low IQ recruits to strap on explosives for suicide missions, promising a sublime future. Exit your FFH, and own FIH for 11 years and you have the right to post, and perhaps the blinders will come off. You know who you are. [the nonsense of IDBIs fees, mkt vs book cagrs, lack of capital to return and to capitalize on disc shares, etc]. Only if mgmt changes their attitude will these shares reflect true value. And they can, the rest are excuses. If they had any morals they would have gone down that path a while ago, it is not rocket science. Ex BIAL, in composite the returns of this vehicle over a sufficiently long time are poor. Just like Sanmar, take the hit, convert to a BIAL only like structure, get an airport multiple, not a discount to some underperforming- poor governance - subservient board failing their fiduciary duty - BV.

-

As the Annual meeting is coming up, below are some updated figures. Fees paid out to FFH now total $572 million. That compares to market cap added or value created of $778 million. In 11+ years what have shareholders received? ~4.5% compound return. Including G&A fees paid, to subsidize the super-voting shares (50 to 1 vote thus are more valuable), fees paid out now total $648 million. Is it ethical to charge G&A fees pari passu when the value creation is disproportionate? What happens at Berkshire? Should FFH be charging G&A fees on top of Investment & Advisory? In the last three years, FFH has been paid close to $150mm, excl performance fees. They've made ONE new investment, Global Aluminum in late 2024. One. With the panoply of fees, FFH share basis is now negative $0.78 to negative $2.29 depending on how you want to look at it. Shareholders have received nothing. Zero. Does it matter what the fees are if we are getting a good risk adjusted return? or a return as indicated by PW to be expected of 15% net to invest in India? Is it gaslighting by management, and servile rabid mouthpieces on various platforms when touting shareholder friendly buybacks, when for the last two years, the pace has dropped off to anything but significant? Half a percent of shares outstanding per year? Mgmt has issued 149mm shares over 11 years, and 134mm remain outstanding today. Is that much different from the SBC equivalent buybacks criticism against tech companies? Particularly when you shout out value being much higher than book, and the shares trade at a fraction of book? The excuses of low share repurchases due to illiquidity does not hold water...its already there, has been for a while, and wont change. That ship has sailed a while ago. The likelyhood of trading at fair value, to be able to issues shares and enhance liquidity fairly is miniscule. Today the implied value of BIAL in the share price is $380mm, a discount of 80+% to marked value, or higher to theoretical intrinsic value. Should management be doing anything but buying back their own shares, hand over fist? Just interest and dividends added up to over $115mm over the last two years relative to ~$20mm spent on buybacks, never mind Net realized gains of $270mm. With single digit compounding of bvps, relative to the risk, and objectives, have they earned the right to invest elsewhere with the shares trading at perhaps close to 50% or less of intrinsic value? While there are other forward thinking steps to get the shares to fair value, a discussion for another day, no investment they will find could be superior to BIAL at this discount. Silence equates to complicity?

-

We shall see, but if there is a rerating, it wont be to the new bvps. The shares will still trade at a discount, so the paid-for-by-shareholders chinese torture takeunder will continue.

-

Other than the poor performance actual and relative of bvps, share price, and particularly relative to their own objective of 15% net cagr, this is all you need to know about why there is a discount to nav, thats it. Never mind their refusal to correct performance, incentive structures, and lack of shareholder friendly action. And on the takeunder comments...it doesnt have to be in one shot as with their previous escapades. This structure is better. Its already in play...they bought shares in 2022 i think it was, while getting fees...so in this case we pay for the takeunder as it unfolds in slow motion over an extended period of shareholder fatigue...they're average cost already is below $0.00. This is the ultimate takeunder, its paid for. These are facts, real numbers, not made up. You can paint any other picture you want, its the case, even if its not preconceived as i believe it wasnt. We can continue to watch it unfold while living in denial, hope and hype. Or, we can try to shift the narrative and discuss this with mgmt, the Board or the press. One of the comments on the X post by BW of latest podcast of BIAL is a request to do a share buyback. There are many who are dissatisfied, who support a buyback as the most important use of capital, on this board and off it. We should form a group and present our case. Both number of shareholders, and number of shares is important. PW is the largest individual shareholder at ~320K shares. I can speak for 222,600. If we get more than PW, another 100k, they should give our rep an audience. If theres anyone up for this constructivist action do let me know. People who want to remain confidential can.

-

Todays FT. Reasons for discounts. Shades of FIH. And justified self preservation reasons to act.

-

Im curious, why are you ok with the discount. Why would you not want this to close? Why not take action to close it, whether successful or not, as management will not? Im sure you realize that their managment fee is on the book value, not a discount to book value. To date they have been paid $331mm on Book Value. And another $230MM on Performance on book value. Nothing is on market value. Why do we have to eat market value and management book value?

-

Sorry i dont see that happening. Discounts exist due to a variety of reasons including, 1/ layers of fees, 2/ corporate taxes, 3/no claim to underlying cash flows, 4/significant capital tied up with private companies with arbitrary mtm tweakable with a 1% move in discount rates, 5/ poor liquidity, 6/ poor NAV growth, ie, investment performance, 7/direct access to underlying shares, 8/dual structure shares, and 9/opaque financial statements. For the discount to close materially, FIH will have to communicate that they care about subordinates, and act on it on multiple fronts - align incentives, adjust fees to reflect performance, capitalize on the discount (SBB). For eg, FFH took their performance fees in cash a whopping $110mm a few years ago. They've broadcast that as doing us a favor by not taking discounted shares instead, and that has been swallowed wholesale. Well, the discount exists because of them, they are taking money out while subs are not getting any, they've repurchased a paltry <1% of shares - over two years...as an example, what if they'd taken that $110mm of cash...and bought "discounted" shares...thats a vote of confidence...win- win-win for everyone...many things like that need to happen...i'll stop..

-

Understandable. But in the interim, all incremental investment capital should go to the buyback...any liquidations like Saurashtra, the latest, should go to BIAL by repurchasing FIH. Subsequent ones can be a mix of paying off the debts (Siemens and Holdco) and buybacks.

-

its always incentives. its not about the pop. its about the implied value of BIAL, particularly given its prospects. The pop if it happens is an outcome.

-

Please see the pdf attached. The last point of which is below. 3/ BUT most importantly why they should ONLY buy back stock. With the shares at $17, the implied valuation of BIAL in the market is a discount of 71% to 84%. Or perhaps much higher, as this is at implied multiples that are well below what are touted as applicable. Change the figures at your will. On the books BIAL is marked at $1,979 mm which is 67% of NAV, or 79% of NAV at the $3.7bn IPO valuation. I believe that number is low at 10x ‘27 EBITDA. The point is that FIH is a BIAL proxy, as stated previously by a member of this group and myself. It's how things have evolved, and perhaps for the best. My position is that FIH should wind down everything else, if not, a conglomerate/holdco discount will continue even post listing. But even more so, if you dont want to agree with me, the bottom line is that it is a tremendous value. Nothing else they can buy has this upside. And we should push them hard to do so. Even they will benefit from the higher performance fees calculations. CoB (1).pdf

-

There are people on both sides of the fence. To measure their aptitude towards their fiduciary duty, the Funds underlying performance, their attitude to shareholders, some feel the last 11 years are enough, and some not so. Some on here were shocked that the Lead Director Hodgson over 11 years owned just 5,000 shares. Worse is that the CEO Ratnaswami owned only 7,000. For those who dont want to leave the next performance period of the shares to their benevolence, to their nonchalance, to chance, there is no downside to expressing our concerns and suggestions, as a collective to the Board. Wheres the downside? Now its one subservient troop member competing to genuflect even deeper to the Emperor at every chance. Change comes with every cremation. PW has passed the baton. To quote James Baldwin, ""Not everything that is faced can be changed, but nothing can be changed until it is faced."

-

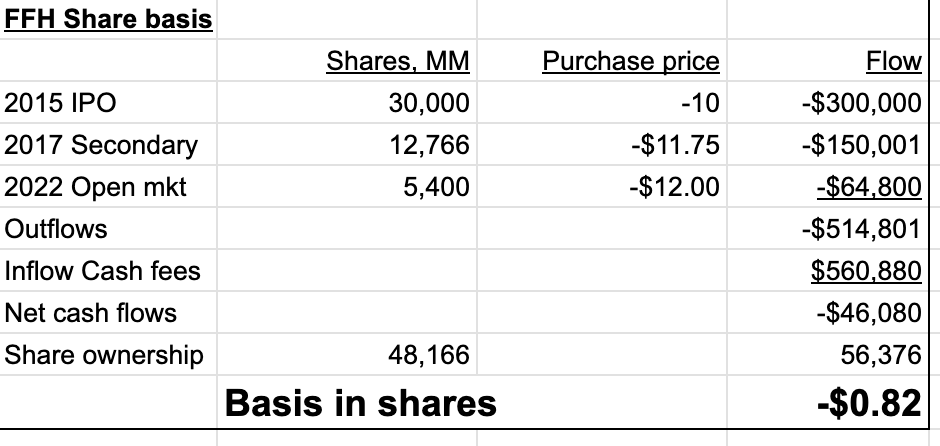

But hey, its going real well for them. Their cost basis is...negative. $-0.82 as per my calculation below, way better than mine...or yours. Cant lose money and it will only get better. Toothless shareholders...hmmmm.

-

conflicts underlined in red. other than watsa' and ceo.

-

If they dont own anything but a superficial amount of shares, they have no incentive to maximize the value for the rest of us. Need a wholesale change with the Board. Interested shareholders should form a group and write to the company and push for an improvement in our situation.

-

The article discusses the Korea discount, as well actions by a company to reduce the NAV discount. And yes, I do believe this is a compliant Board per my last post, and the shareholder base is toothless - due to the supervoting shares. Another reason for the discount.

-

FIH has 11 directors, Apple has 8. Of the 11, only 2, just 2, dont have an affiliation to FFH, Hodgson and Kenny. The rest either work there, are on the Board of the parent, or have worked for or are on the Board of one of the investees. The Board has one legal obligation, to look after the interests of shareholders. With a rubber stamp conflicted Board, 9 of the 11 being related in one way or another, and of the other 2, the Lead Director is Christopher Hodgson who has been there since prior to FIHs IPO. He owns a WHOPPING 5000 share. In 11 years, 5000 shares. Incentives drive human behavior. The sycophant Board is cuckold. These are the reasons for the discount. link to 2024 Proxy page 7 for you to read on your own. 2024-Proxy-Circular (3).pdf

-

"Turns out discounts close when accountability shows up. " https://x.com/boazweinstein/status/2002077686471282722?s=20

-

Corporate governance reform / reducing discount to nav actions. Article from FT yesterday. 1st 3 have free access. https://giftarticle.ft.com/giftarticle/actions/redeem/2097e32e-aac8-4f9b-9223-d0cdc30ba30b "The routine rubber-stamping of such transactions by compliant boards and a largely toothless shareholder base reinforced the notion that Korea was run by and for its largest shareholders." "In 2025, the government has been sprinting to change this. After an overhaul, the country’s corporate governance code now requires directors to consider all shareholders, not just the “company”. Cumulative voting, which enables minority shareholders to concentrate their votes on specific board candidates in proxy fights, is no longer optional for large listed companies with assets over Won2tn; if a shareholder with just 1 per cent requests it, boards must allow it. And there is now a cap on voting rights for any single shareholder — 3 per cent — for the election of board audit committee members, constraining the influence of controlling parties on these critical positions." "Companies are acting, too. Along with other investments in the country, my fund has a stake in SK Square, which has been an early leader in corporate governance improvement, narrowing the discount of its share price to net asset value from over 70 per cent to 50 per cent by divesting non-core businesses and buying back stock."

-

I hope they get 30x, but i think thats a number for March 2025 year. Delhi is getting a 125%+ increase in their new rates on Dom pax for this year and onwards. Jeffries has ebitda growing 40% in FY March 2026. BIAL may get to 400mm but 2q was a very disappointing 0% dom pax growth offset by the ypp. Then this Indigo disruption should mess with 3Q. No, i dont think they are shareholder friendly at all. The opposite. If they were shareholder friendly, you would'nt have a lemming sycophant gatekeeper on the Annual Meeting as moderator keeping away the tough questions. The board is stacked with non-independents, and there are more members than at Apple. And ex-PW they would own some shares and get paid in them. The fee structure would be aligned with subordinates ie market price related. And they'd give us as much disclosure that GMR does with business color on a normal regular basis. And if that NAVps was anywhere near 50+ that you refer to, they should be gorging on the FIH shares not on another random walk. And yes, BIAL is all that matters and I hope that remains the case. I was thrilled with the two 10% purchases. They need to focus just on that. Everything else is a wash to 'subordinate' plebian minorites, while the supervoting shares gorge at the pigtrough of fees while underperforming.

-

As a reminder, and this is material, in general PE funds take managment fees on committed capital, and performance fees on realized gains. They do not take fees on the marked up value of their investments. Over a decade, that differential matters. I point this out due to some participants saying they are conservative on their marks. The thing is, i'd be THRILLED to pay the fees...if they'd earned it. They havent. PW said in the annual meeting that they invest in India to net out 15%+ to BV vs the 9% they have recorded. Over 11 years, thats an underperformance of close to half. It hasnt worked. Wont get there even if BIAL was at commonly perceived IV. Didnt earn the fees. Fold. Disband the team. Stop the panoply of fee leaks. SBB. Move all the chips to the winner, focus on airport+ (hosur, chennai, Bengaluru 2).

-

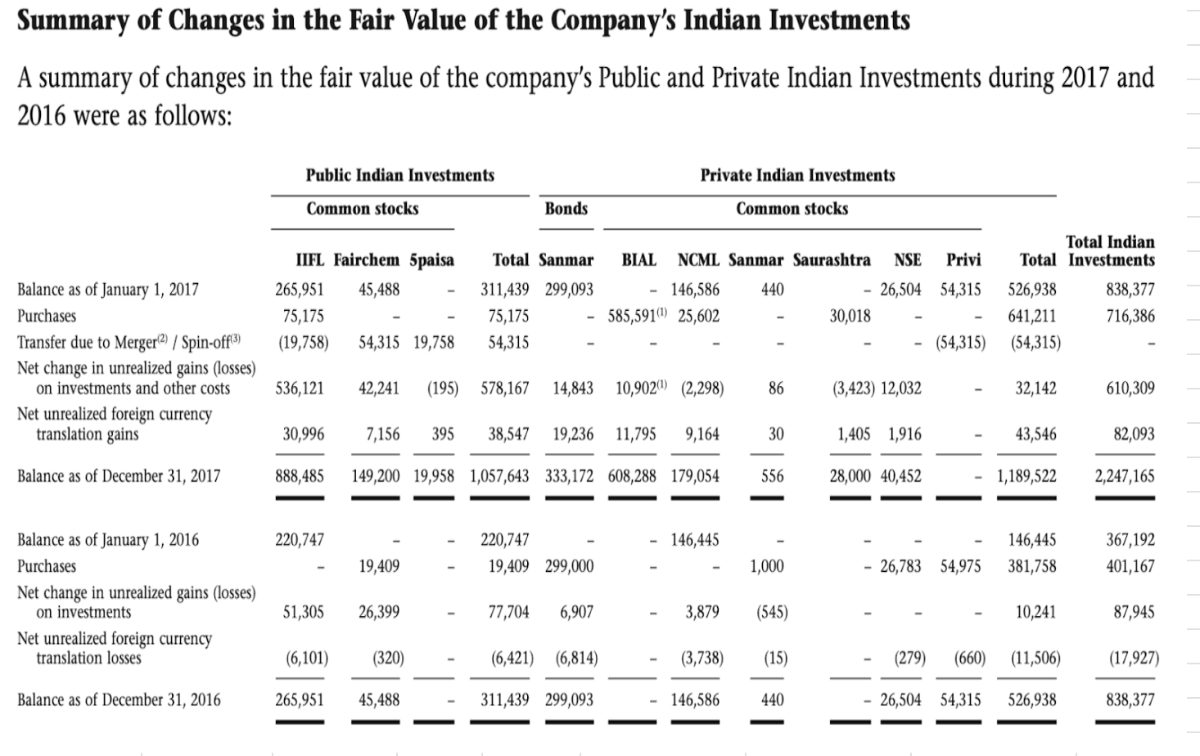

yes, you are right. my bad. attached are the pics of value at year end 2017 and 2024. i dont know how much of those bonds converted into what equity value.

-

You can include NCML in your tally of material investments. So that makes it 2 Bad, 2 home runs, 1 Bad. over 11 years....someone said Ocean of Opportunity earlier. Nah. Was there. Didnt happen here. Sorry. Sometimes its best to fold the cards. Divest non- airport investments, dividend to shareholders or SBB all dividends and divestments. Reduce the underperforming team. Focus on the airport(s) / share value.