thepupil

-

Posts

5,003 -

Joined

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by thepupil

-

And where did they generate the cash to buy Burlington Northern? whuch is by far the biggest source of operating earnings growth and the biggest part of my point. . Didn't they do some share issuance to buy chunk of the utilities too? Back in the early 2000's? I could be wrong but I thought I read in snowball at peak Berkshire and peak stock holdings valuation he brilliantly issued shares to buy Utes (monetizing increase in investments to grow op earnings). I'm not gonna look it up. Agree with you the 2013 looks better than I originally painted. But I would point out most analyses I've seen believe railroads require higher than d+a maint capex. If I'm wrong and Berkshire operating co is and has internally funded 20% growth and will achieve that in the future, then I'm far underweight, even after adding recently and should go back to 40+%. We both own the same stock and actually have similar target prices. So agree this is a waste of time. I find that in general I'm more bearish than other Berkshire shareholder on both the insurance operations and the future growth of the op earnings . I'll admit to awaiting a collapse in earnings at BNSF for a few years now (once hey build pipelines) and I eagerly await massive insurance losses. Mayby expectations are too low. If I'm wrong I'll make more money than I expect.

-

I used the after depreciation numbers because we are talking growth and growth capex. I didn't think this would be controversial.the share swaps and BNSF are perfect examples of this.

-

The 5.6b of the utility was the equity consideration. I think if you look at my he cash generated by the operating subs versus the capex and bolt ons and big elephants used to grow said subs, you will conclude that the opera tints company has been subsidized. Another reason the historical growth rate is too high is the cyclical upswing at BNSF and crude by rail.

-

the investment and underwriting income was used, limited amounts of share issuance was used (for the big kahuna BNSF); using share issuance represents a monetization of the growth of securities portfolio to buy an operating company and grow operating earnings. Several crisis era investments were settled and harvested for cash also. they did not funded all those acquisitions with the cash generated from non-insurance operating earnings. For example (just because i have my 2013 notes handy). In 2013 they did $15B of non insurance operating, pretax, $11 or $12B post tax. In that year they did $11B of capex, $3B of bolt-ons and bought the Nevada utility for $5.6B. If OpCo berkshire was a standalone company limited to spending within its means, it would've invested $11B to grow. But instead it invested $20B. In that year they did about $3B of insurance gains and $4.7B of investment income. I'm saying the non-insurance gets a little help from its friend. I am not saying the investments were bled. I'm saying they subsidized and continue to subsidize the growth of operating earnings. It's a beautiful thing. You get this constantly increasing operating earnings coupon punctuated by the occasional large investment gain coup (BAC pref/ warrants, Heinz 3X in a few years at current MV, etc.). But once operating earnings reach a certain size and heft relative to the investment portfolio, this effect will juice the operating earnings growth less than it has in the past. It will still be great and I think Berkshire is undervalued. I just can't sit here and let people say operating earnings are going to grow like they have in the past. Because they won't.

-

I see the 10 yrs of 6.6% (a pedestrian absolute rate of growth) and the subsequent 4 yrs of slower than S&P growth as evidence that the investment side of the equation was used to subsidize the growth of operating earnings. This period includes some spectacular investments on Berkshire's part, many of which have been harvested already, underwriting was spectacular, float growth was really great too...So we'd expect investment per share to go up a lot and at a very high rate. But they didn't...Instead they got plowed into growing operating earnings, which is awesome. But there's diminishing returns to this. Let's just pretend that all cash and investments (about $200B) were plowed into something at 12X pretax earnings. This would add $16B to the run rate of $18B, basically doubling it. If you did that 5 and 10 years ago, the affect would be FAR more dramatic. $18B is simply a lot harder to grow. I personally see Berkshire more as an operating conglomerate that grows at a fast rate because it has this "capex fairy" (investment income, insurance biz, securities portfolio) that rains down growth capex upon it to add divisions and accelerate it. But that magical fairy dust gets less potent with the non-insurance operating earnings starting to dwarf the more financial side of berkshire<---yaaaa it's friday...

-

Can't stop chuckling! I really do object to this book value stuff! It's a useful shortcut and it's been promoted by Buffett and I've spent years and years using it myself but still, I find it is precisely this entrenched usage that is leading to BRK being persistently undervalued (especially the insurance operation). What do you guys think of the following simple valuation for the ultra longterm equity investor: 1. The stock portfolio (plus Heinz, Bac, converts, preferreds etc) is worth what it's worth. The cash and IG fixed income is worth 50% of gaap but in any case the discount to be a minimum of $25bn. 2. Total operating income has the interest, dividends, gains derived from the above assets removed. All of the remainder (including an averaged number for the insurance underwriting gains) is then capitalized at a rate that makes sense to the investor keeping in mind that with full retention of earnings BRK has historically grown these earnings at a CAGR of 20%, about double the long term returns of the market. 1 + 2 are then added together and are the total equity value for shareholders. (No subtractions of DTL or Float.) *Note on Float. If float grows over time then the above undervalues the company. And If float declines Buffett wrote in this year's report that it would do so very gradually and probably not any more than 3% per annum. hello my obese simian friend, 1. agree to disagree on incremental debt usage being a separate or quantifiable source of intrinsic value to berkshire. I agree it will and has helped grow IV, but I'm not willing to attempt to try to value that or consider it a separate component of growth in value. To your point, BNSF increased debt by $7.1B over 2012-2014, whereas UNP increased it by only $2.5B. BNSF now has ~$20B, while UNP has ~$13B. So either UNP is underlevered, or you are correct in that the Berkshire structure may allow for incrementally more leverage at the subs where the vast majority of the debt is located. 2. I'd like to say that much of talk about the astounding historical growth in operating earnings does not point out that Berkshire has used big chunks of the securities portfolio in order to grow these operating earnings (way back in the day issued shares for utility company, issued shares for BNSF, turned PG into Duracell, turned WaPo into earnings assets, PSX into Lubrizol add-on, etc.). The growth in investments / share has lagged the market returns because of Berkshire's conversion to more of an operating company. Berkshire has been very good at monetizing the increase in value of the holdings and converting them into wholly owned operating earnings. also the securities portfolio historically ahs been MUCH larger than the operating businesses, so using the securities portfolio earnings to subsidize the growth of the operating earnings had a particularly large effect. This will not be as powerful in the future as it has been in the past. I'll be willing to wager anyone that growth in operating earnings per share is less than 14% over the next ten years, up to 20 shares of Berkshire (b shares that is) as the stakes. To be clear i am referring to the $17.5B of pretax earnings from non-insurance non-investment biz (BNSF, Berkshire Energy, manufacturing and service etc.). You'll get PCP as a head start. 14% growth would imply pre-tax operating earnings of $65B. It is not completely impossible, but would be quite extraordinary. If those talking about growth of the past being the norm for the future want to truly bet on it, I'm willing to take the other side.

-

I'll take a stab 1. Berkshire was VERY undervalued for a long time, it started to re-rate towards some level of fairness in the early part of this year...then... important proxies for big parts of BRK's SOTP fell such as a) UNP is down 28% YTD b) XLU is down 12% YTD, S&P down 7% or so, Berkshire most correlated to XLF which is down 6% or so YTD and about 8% in the past month, BRK/A is a big component of XLF and they trade together c) the stock portfolio hasn't been spectacular, although Kraft Heinz is a giant write-up d) insurance earnings were giant the past two years last year as were derivative gains which make for tougher comps e) I think some are disappointed in the choice of elephant in terms of timing and the actual company PCP I think that's pretty much it. haven't seen or noticed anything else. I've added a little in the recent swoon since KHC added value and the price fell a bit so price/value got a lot better on the move from 150-130. EDIT: Industrials are also down 10% YTD (which you can kind of sort of not really call a proxy for the smaller subs). My whole point is things across the board have gotten a touch cheaper/less expensive, so we should expect Berkshire to get a little cheaper too. As a 26 yr old net saver, I'm all for it.

-

Sorry if not clear, I think of everything in terms of adding back DTL. Burlington = $34B equity plus $18B DTL, Berkshire $240B equity + $60B DTL, etc.

-

I think most people focus on earnings of the operating companies which accounts for the low cost of debt by subtracting the low amounts of interest in order to get to earnings. Railroads Utilities and Energy segment has equity of $91B. Burlington Northern's separate financials show equity of $52B and Berkshire Energy's show equity of $33B (after adding back deferred taxes) = $85B (the difference is from additional holdco leverage not shown on the subs balance sheet I believe). BNSF pretax income is about $6B. BE earnings are $3B pretax, so these are earning about $9B pretax on $85-$90B of equity. . LEt's throw a 20% tax rate on them and get $7.2B of post tax earnings power. What you think these are worth all depends on your required return. I should note that BNSF has $14B of goodwill related to the acquisition. If you think these are worth 20X. These are worth $144B, 1.6X their DTL adjusted book. Berkshire trades for 1.1X DTL adjusted book, so if you are willing to pay market-ish multiple of 20X there is lots of value in BRK-B (for this portion of berkshire at least would be undervalued by the market). If you want to pay 15X, these are worth $108B, 1.2X DTL adjusted book, pretty much the current stock price. It's hard to justify giant premiums to book because then you can buy things like UNP for much cheaper. For example let's say you think BNSF is actually worth 25X $4.8B NI = $120B (2.3X book, 7.5X tangible book, remember a large portion of BNSF's book is goodwill) because its underearning or will grow or whatever (i actually think it may be overearning because of crude by rail but that's besides the point). Then you are paying $120B for BNSF when you can buy UNP for $72B, a 66% premium. UNP earns 33% more pre-tax than BNSF on similar amounts of tangible equity...a 66% premium is certainly not justified. I don't think that even the conservative "modelers" think these businesses are worth book value. They are obviously worth more than book. But their capacity to carry low cost debt is already captured in their earnings, so as long as you take an earnings based approach for those subs, you are accounting for the debt in a way that does not mechanically subtract it. What do you all think BNSF and BE are worth?

-

Is there an intelligent way to play commodities?

thepupil replied to u0422811's topic in General Discussion

Pupil he goes into how often these forward prices are correct a few minutes in: http://www.bnn.ca/Video/player.aspx?vid=684653 The video doesn't work for me for some reason, but far out futures were $85-$90 a year ago, so hey weren't "correct" then judging by today's prices. I'm not buying crude futures, I'm just throwing it out there as an option. -

It did achieve higher than teens growth in earnings power 1) converting cash and stocks to owned businesses, generally in a way that was immediately accretive 2) benefitting from a cyclical upwind in the economy from BNSF (bakken plus other) and lots of housing related businesses vinod, you are looking at equity value which has grown at a lower rate because of the DTL (which decreases the growth from stock appreciation by 1/3 and also likely understates the growth in cash generation from BNSF and Berkshire Energy). The guys that are jacked up saying mid teens returns are saying they expect earnings to keep growing at that clip. You are saying book value hasn't grown at that clip so why would it ramp up. They are different things. I think you all are talking past each other. I think you are correct with respect to the value of stocks and bonds and securities that berkshire owns. No way that grows at mid teens. It will grow at s&p +/- 3%. But operating earnings can continue to grow at a rate that exceeds the growth rate of the securities portfolio. I don't think it would be wise to say "15% / year for 10 years" or something like that, but I think we all agree they'll do okay.

-

Is there an intelligent way to play commodities?

thepupil replied to u0422811's topic in General Discussion

you can buy 1000 barrels of oil for december 2023 (as far as it goes out) delivery on IB. $60 / $63 bid-offer with liquidity becoming MUCH MUCH better as you move in. IB will allow you to post 12% margin, so it's not like this requires a lot of capital. Of course if you lever it, that may prove quite disastrous. 8 yrs seems like a long enough time for marginal guys to bankrupt and oil to "correct". But maybe $60 is the "correct" price. I don't know. Just saying that I had not considered this option until recently. When I was talking to someone about the best way to hedge my BPT short (BPT is a derivative of WTI and prices in much higher than market oil prices). They said "just buy oil". There is also a 500 barrel mini contract. -

if one uses look through earnings (which is what the person who i responding to was using) is it not double counting to count both earnings growth and appreciation of stock prices? the stocks appreciate because earnings grow over time. For example, KO trades for $39 and is estimated to earn $2, it trades for 19.5X earnings. It pays a $1.32 divvy, 3.4% yield. Let's assume 6% growth in dividends and EPS over 10 yrs. If I own 100 shares of KO look through earnings = $200 pre-tax investment income is = $132 My total return over the next 10 yrs (with no multiple change and 6% growth and divvy's reinvested*) will be 9.6%. If you say that the total return is look through earnings of $200 (5.1% earnings yield) + growth in EPS of 6%, it overstates the return because some of the non-dividended earnings are being used to repurchase shares and invest in growth to fuel the EPS growth. If you use "earnings growth + net change in securities/cash", then you have to not use look through earnings. In our KO example if you use look through earnings the total growth in value of KO would be 6% (earnings growth) + 6% (capital appreciation of KO) = 12%. Isn't that double counting and won't that overstate intrinsic value growth? If you use investment income (rather than look through earnings) then you can also count the capital appreciation. Now I will say that all this theoretical gobbledygook is ignoring multiple change. Mr. Buffett is not afraid to monetize his changes in multiples via tax efficient swaps (Duracell/PG, WaPo transaction, Phillips 66 thing, etc.). So I'm not saying he won't take advantage of a re-rating in the value of an owned security (or a business like Heinz, which 3G and team got all dressed up for the ball and bought a shit ton of Kraft with their re-rated and arguably quite expensive Heinz). In the cases where Buffett takes advantage of re-rating, then the total return is indeed greater than investment income + earnings growth. I love berkshire and think it will provide a nice return, particularly relative to the S&P, but just trying to keep expectations of the stock portfolio realistic. *I realize berkshire never reinvests divvy's, this is for simplicities sake. It can also be reinvested at whatever you think berkshire will make over time

-

Is this the right way to think about it? All earnings at Berkshire are used to keep growing earnings (they are retained, not dividended or share repurchased out) so won't total return be equal to (earnings growth + return from change in multiples) instead of (earnings yield + earnings growth + return from change in multiples). The cash flow stream would not grow without capex, particularly the utility and railroad and the industrials. I think the only types of businesses where you can say total return = earnings yield + growth in earnings are See's Candy types of things where almost no capex is needed for growth. If berkshire triples earnings over the next 10 yrs and the multiple doesn't change, shouldn't the stock price triple. But it should not triple + give you even more for earnings over that time period. You can do this type of calculation with dividend yield or truly free cash flow yield (after growth capex), but earnings yield seems too generous right? For example, the S&P 500 trades at 18X (5.5% earnings yield) and a 1.9% dividend yield. If earnings per share grow by 6% per year for the next ten years and there is no multiple change, what is the total return? By the earnings yield + growth formula you use for berkshire it would be 11.5% (a cumulative 196% return over 10 yrs). But that's not what it would be, instead it would be dividend yield + earnings growth, right? Because the non dividended earnings are what is used to grow the EPS (either through investment or share repurchase). Growth isn't free. I would consider the depreciation charges as the amount of capital needed to maintain the position of the existing businesses to grow with the overall economy. Berkshire's purchases of property and equipment in 2014 was approximately $15b, more than double the 7.3B depreciation and amortization charge. A lot of the additional capex was used in the utility and railroad. Buffett has talked in the past how he believes they will earn adequate returns on these investments (10-12% pre tax?). So the additional $8b capex in these regulated businesses should add $800-950mm. In addition, the excess cash flows are used to purchase additional streams of income like VanTuyl. With these additional investments, pre tax operating earnings have increased by 14% in the first half of 2015 compared to 2014. It should be even higher over the entire year as more of the utility projects are coming online and the Duracell and KHC deals close in the 2nd half. The PCP deal alone will increase pre tax operating earnings by approximately 13% and that cash will be replenished quickly to set up the next elephant. I wouldn't bet against Buffett/Berkshire being able to increase earnings significantly over the next 5-10 years. I own the stock and it is my family's largest position. I'm not betting against it, was just questioning the (earnings yield + growth= total return equation). I think berkshire will grow earnings nicely and enjoy a decent return on the capital it deploys.

-

Is this the right way to think about it? All earnings at Berkshire are used to keep growing earnings (they are retained, not dividended or share repurchased out) so won't total return be equal to (earnings growth + return from change in multiples) instead of (earnings yield + earnings growth + return from change in multiples). The cash flow stream would not grow without capex, particularly the utility and railroad and the industrials. I think the only types of businesses where you can say total return = earnings yield + growth in earnings are See's Candy types of things where almost no capex is needed for growth. If berkshire triples earnings over the next 10 yrs and the multiple doesn't change, shouldn't the stock price triple. But it should not triple + give you even more for earnings over that time period. You can do this type of calculation with dividend yield or truly free cash flow yield (after growth capex), but earnings yield seems too generous right? For example, the S&P 500 trades at 18X (5.5% earnings yield) and a 1.9% dividend yield. If earnings per share grow by 6% per year for the next ten years and there is no multiple change, what is the total return? By the earnings yield + growth formula you use for berkshire it would be 11.5% (a cumulative 196% return over 10 yrs). But that's not what it would be, instead it would be dividend yield + earnings growth, right? Because the non dividended earnings are what is used to grow the EPS (either through investment or share repurchase). Growth isn't free.

-

You talking about STON?

-

maybe it's 2/3 of the float needs to be kept around in low returning assets, maybe it's half, maybe it's 100%. I think we can all agree it's not 0% and Berkshire could not dividend out that $80B ( which is why i dislike "investments per share", which no one would talk about if it wasn't used in his letter 20 years ago and rates were very different) or buy an $80B company for cash. I'm not an insurance regulator and don't know the exact requirements. It just seems that Berkshire likes to keep a hell of a lot of cash and fixed income around despite hating on cash and fixed income all the time. Like I said, if my valuation method understates true intrinsic value, then I'm undersized in the name and underestimating it. I'm fine with that. As a shareholder, I would love to be surprised to the upside and be wrong and see more cash and fixed income converted to higher returning assets. I'm not counting float at face value (book value does that). I'm using my perceived capital requirements (which as you point out, may be wrong and overly burdensome) to determine the earnings power of the float over time.

-

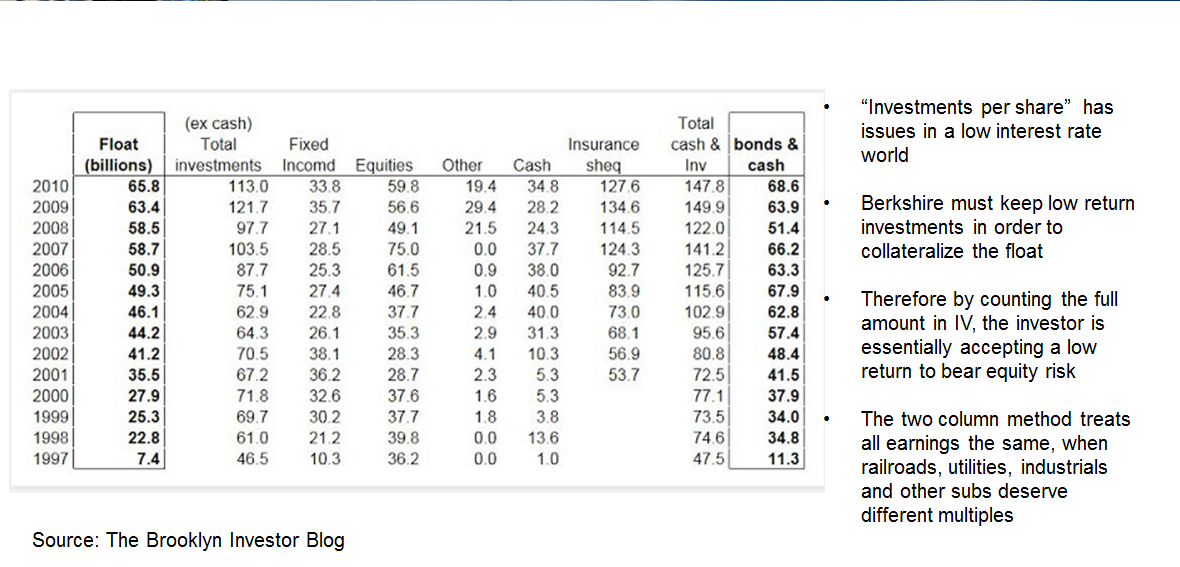

here's a slide from a presentation i did on valuing berkshire (I can't share the whole thing); this portion just piggy backed off brooklyn investor. Notice how bonds & cash corresponds to float. I am trying to value this portion of the business (the combination of the cash + bonds and the float). I don't think it is worth $80B. Two column method makes it worth $80B. The two column method is about how liabilities are accounted for. It accounts for financial debt by deducting interest. It accounts for the deferred tax liability by saying it is worth $0 because it has such low present value and no coupon (I agree with this). It accounts for float by adding it back fully because you have underwriting profits. I don't agree with this for the reasons I've stated. Just peel out the stocks and the operating businesses and think about what you would pay for a company with $80B of cash and fixed income and $80B of insurance float and the underwriting record and float growth track record of berkshire. You may get to $80B but you'd have to be pretty aggressive.

-

Berkshire is an overcapitalized insurance and operating conglomerate. Take all the businesses and stocks and peel those away. They can be valued separately. These may be part of the insurance company (BNSF is owned by one of the insurance co's for example) from a legal perspective, but at a certain degree of overcapitalization, they are not part of the insurance co for valuation purposes*. What you are left with is an insurance operation with no capital ($80B of fixed income and cash offset by $80B of float). The book value of this business is zero. I don't think it is worth zero. I think it is worth what it will earn over time. It will earn the spread on what it earns from its assets and what it earns/loses from its liabilities (underwriting). At the risk of simplifying too much let's just say this is 4%. So $80B * 4% = $3.2B. I would then multiply that by a reasonable multiple. Let's tax affect it to $2.3B and put 10-20X on there = $23 - $46B. So I think that operation with zero book value and zero liquidation value is worth $23-$46B. By no means do I think it is worthless. I just don't think it is worth $80B, which the two column method and its use of "investments per share" implies. I should also note that the more fervent of buffett devotees may object to such slicing and dicing up of Berkshire like this because there are synergies between the financial/insurance side (what i call the no capital insurance co, ie the thing with $0 book and that i think is worth $23-$46B) and the rest of Berkshire. I don't fully disagree. Berkshire is a going concern. But in trying to figure out what i am paying for this business and what it is "worth", I find it useful to slice it up in this manner. What Tilson does is use investment per share AND adds capitalized underwriting profits, which i think is double counting and very aggressive. Hemay or may not think so. Aggressive valuations make for better powerpoints and higher price targets. *Imagine an insurance co with 99% equity to assets. You would just look at the equity and value it because it is so overcapitalized that the relationship between assets and liabilities would not matter. You'd just look at the assets.

-

Eric and petec, I think we all agree. The present hypothetical liquidation value is $0. Assuming berkshire estimates its liabilities correctly, then cash and FI of $80 - float of $80 = 0. And the discounted future streams of earnings is (normalized spread)*(float) + (value from growth in float). Petec, I think the two column method is a little optimistic, but whatever, let's move on. There are probably more interesting debates to be had and we pretty much agree with the main drivers.

-

I look at it as in insurance operation that has $80B of low risk assets and $80B of high risk, fat tail, liabilities. I don't think you can separate the two. As Frank Sinatra would say, "you can't have one without the ooooooooooooother!" I think taking on insurance risk is a very high risk activity. Ajit is a genius but he is not omniscient and I want to get paid a decent rate to bear the risks that he picks for me. Berkshire has made money every year in the last 10 underwriting, but I'll happily bet that won't happen in the next ten. This is why I use an equity multiple for the earnings generated by the spread between underwriting and interest income. Over the last 10 yrs, underwriting profits have averaged 3.3% of the float. I think 0-3% is a reasonable estimate for underwriting profits over time (some would even say 0% is optimistic given the capital flooding into reinsurance markets). I think that underwriting profits are correlated to rates (as in if rates go up, you would imagine underwriting profits would go down because competitors would write less profitable biz) So your key assumptions in valuing the insurance operation are 1) spread between interest rates and underwriting (I think of that as something like 1-4%, but in hard markets like post KAtrina it can be super high, look at 06-09 at General Re and BHRG) 2) multiple (10X pretax) 3) float growth over time (which would influence what multiple you'd want to pay) In the end, if i'm wrong and you are right and berkshire continues to always make money on the underwriting side, frees up more of its cash/fixed income, and continues to grow float over time, and berkshire is worth the full $80B more from adding back float, then Berkshires is worth 15%-20% more than i think it is and I am undersized in the name.

-

If you value the cash as cash because you own the interest, you are bearing equity risk (by owning Berkshire) to receive cash interest, when you could yourself just own cash. Cash and fixed income burdened by insurance risk and regulation will always be worth less than if it were unburdened. You are effectively saying "my discount rate is 1%". Let's say short rates go to 4% (something inhonestlye think won't happen for like 3-15 yrs). You would still be "paying" 25x earnings. You can't separately count the underwriting profits and then capitalize the interest income to the full value of cash. Let's imagine Berkshire's other assets did not exist. They only have the insurance operations which produce underwriting profits and losses, and the cash and fixed income. Let's say the insurance operations generate $3B /year in underwriting profits and then lose a low number like $10B on each 11th year (so they make $30B, then lose $10 for through the cycle earnings of $2B / year) Over a 10 yr period this operation would make $20B pretax. Now let's say short term rates average 1%, 3 % or 6%, so they either make $800mm, $2.4B, or $4.8B / year in interest. At 1%, $2B + $800mm= $2.8B At 3%: $4.4B At 6%: $6.8B At 10x pretax, this biz is worth $28B-$68B. At 15X pretax, it is worth $42-$102B. Only at very high levels of short term rates and high multiples is this business worth $80B. I think Berkshire will have an insurance disaster here or ther and will lose 11 figures in a few years so I don't think you should just capitalize underwriting profits and assume they happen year in year out. EDIT: the curve looked a lot different when Buffett introduced the two column method in 1995 http://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=yieldYear&year=1995

-

And yes the profits generated from this deserve a low multiple, because it involves substantial risk. If you make $3B-$4B a year on underwriting profits and interest and then lose $20B in a bad cat year every 10 yrs, it is profitable and good, but not worth $80B today. If you don't think Berkshire can lose $20B or more in a bad year, you shouldn't own in it. They can and will and I actually long to see some nice big losses and some destruction (minus the human suffering part of course) since it would make Berkshire take share and harden the market.

-

I am saying that if you add back the float entirely, you are not acknowledging that a very large portion of the float will have to always be in bonds and cash and that you don't "own" those in that you can't just dividend them out or use the whole $80B for an acquisition*. Now you do own the profits generated from underwriting and the interest income from that pile of cash/bonds. But that number hasn't been worth the full value of the float in years. Bonds may be overvalued, but it isn't relevant here because Berkshire holds cash and very short term fixed income with little credit risk. It's almost as if they hold $80B of cash ($60b after they buy PCP) To increase the profits generated by the float ( and make the two column method and its inherent assumptions more appropriate) 1) short term rates have to rise substantially ( the earnings power of cash and short fixed income would have to increase to a level where you could say all that stuff they have to hold is earning a lot) 2) it could also work if regulators became less stringent and gave Berkshire credit for all its equities and wholly owned businesses and allowed them to use more of that cash and fixed income to buy businesses. As non insurance Berkshire becomes bigger in relation to insurance Berkshire, this may happen, though I wouldn't want to count on that.* *berkshire will use $20B for PCP deal and buffet publicly stated this out them out of the elephant hunting game for a while. If he could use all of the $80b as he saw fit, then this would not be the case. *i feel like I suck at explaining this; does anyone agree / disagree / get what I'm saying?

-

Oil, wow, WTF happened to all of the oil bugs on this site?

thepupil replied to opihiman2's topic in General Discussion

macro is hard, right? as for oil, we will see. I'm on this board a lot. On every oily thread there seem to be at least a couple bears or naysayers, even back in the initial $100-$80 move, it seemed like there were a few guys warning of more pain. I don't think there is a very strong pro-oil bias here.