.jpg.1d9fac650ed66563afd62b892048d13f.jpg)

Blake Hampton

-

Posts

588 -

Joined

-

Last visited

1 Follower

Blake Hampton's Achievements

")

-

Some people were worried about me, so I thought I might write a final post. I decided to leave the board for my mental health and so that I can keep a more independent perspective. There are a lot of smart people here who bring valuable insights, but I also have to be really careful when weighing others' opinions about the future. Smart people can be just as wrong as they are smart. The best I can hope for is to come to my own conclusions and hope that I'm ultimately proven right. The title of this thread is what I believe every investor should be focusing on, though very few seemingly are. Our national debt and our fiscal deficits are enormous and growing, and both sides of Congress have shown no willingness to meaningfully address them. Pay attention to what some of the professionals are saying. Read Warren Buffett's recent shareholder letter. You'll soon realize that a lot of them are sounding alarms: If you're at all familiar with the balance sheets of our country's largest banks, you would know that many took on staggering amounts of interest rate risk during the periods of low-rates. They loaded up on low-yield assets and are now sitting on massive amounts of unrealized losses. Meanwhile, the government is printing Treasury debt hand over fist, in effect putting further pressure on both rates and the bond market—when our banking system can't handle rates moving any higher. Back in 2023, at his annual shareholder meeting, Buffett said that he doesn't know where the future shareholders of the big banks are heading. Take a second to just think about the implications of that statement. I know it's ironic because I've been harping about inflation, but cash is not trash (in the short term.) When everyone in the system all tries to deleverage at the same time, you could likely experience a crash in risk assets and a scramble for cash. Amazingly, even though the Fed has pumped our economy so full of liquidity that it's basically bursting out of our eyeballs, somehow many have managed to find themselves in the same precarious position that initially got us all here. As they've shown in the past, the government will refuse to let the system fail and will do "whatever it takes" in order to save it. This basically means they'll print even more money. I know that I'm pretty alarmist and a lot of this comes of as a worst-case scenario. We could also have a long period of drawn out stagflation, but I assume that we're almost certain to see a crisis since Congress wont act until something breaks.

-

Russia-Ukrainian War - Political

Blake Hampton replied to changegonnacome's topic in General Discussion

Watching this truly made me want to cry. How can you have nothing but sympathy for Zelensky? He and his country have been through nothing but hell over the last three years—rape, torture, death, destruction—all at the hands of Vladimir Putin, with whom we're now friends with? Trump is, by far, the most arrogant person I've ever seen. He hasn't witnessed even a fraction of what Zelensky has experienced in a day, yet he still has the audacity to treat him like some random fool. Shameful. -

Because this is yet another tail-end risk in the system.

-

Just bought a 3-year subscription to Value Line.

-

I honestly feel like politics is just too important right now to ignore. But this stuff does tend to delve into chaos quick.

-

The things I've seen come out of Cantor Fitzgerald are appalling, and Kevin Hassett coauthored Dow 36,000. I've heard his role as co-author dismissed as a "youthful indiscretion"—apparently "youthful" now means 37. Just read about these people and listen to them talk—they're basket cases.

-

The executive order states, "The Secretary of the Treasury and the Secretary of Commerce, in close coordination with the Assistant to the President for Economic Policy, shall develop a plan for the establishment of a sovereign wealth fund consistent with section 1 of this order." - Secretary of the Treasury: Scott Bessent - Secretary of Commerce: Howard Lutnick - Assistant to the President for Economic Policy: Kevin Hassett From everything that I know and have read about these three, I simply do not trust them in managing our nation's wealth. "Almost anywhere you look—from the popularity of gambling and novel forms of retail investing to soaring crypto prices and the electorate’s choice of president—America is embracing risk." - The Economist

-

You know what Greg, I'm starting to think you might just be right.

-

Thanks for the video.

-

The bubble gets bigger

-

What else is it going to invest in? Bitcoin?

-

Why are we creating a wealth fund when we should really be focusing on the budget? Where is this money going to come from exactly?

-

Weren't these the same people talking about how the governmental bureaucracy is stupid and inefficient?

-

-

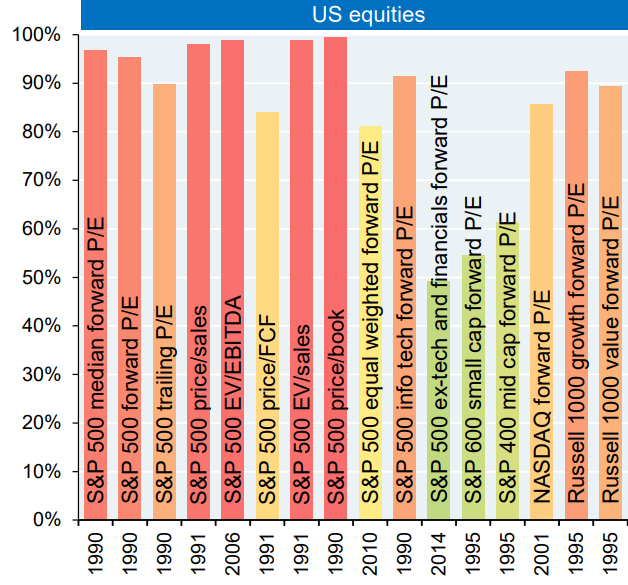

I don't think establishing a sovereign wealth fund during record high market valuations is a good idea. But what do I know?