Leaderboard

Popular Content

Showing content with the highest reputation on 10/29/2025 in Posts

-

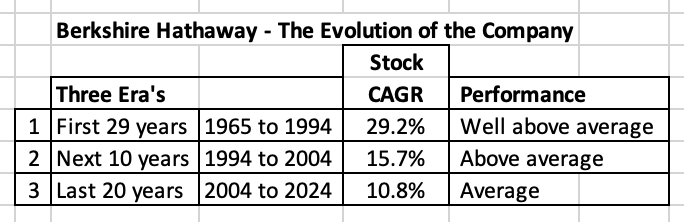

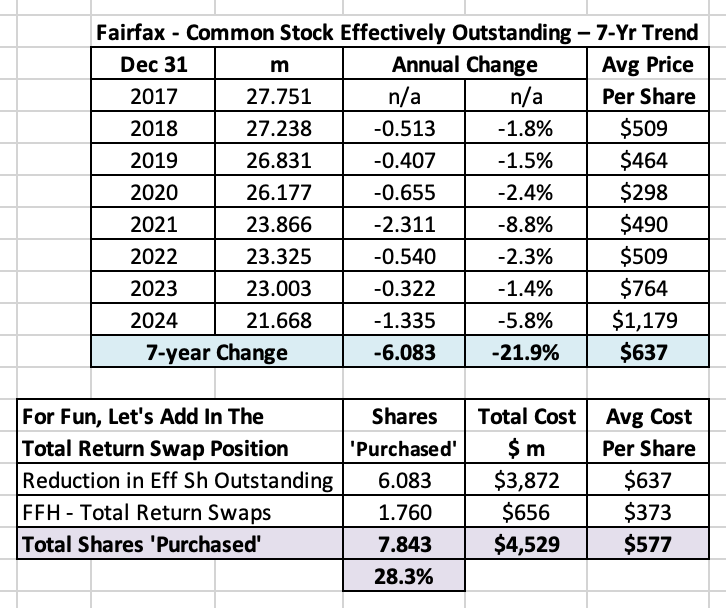

What is Berkshire Hathaway’s biggest problem today? ‘Only a fool learns from his own mistakes. The wise man learns from the mistakes of others.' Otto von Bismarck Berkshire Hathaway served as the inspiration for Fairfax’s creation way back in 1985 (when Hamblin Watsa purchased Markel’s insurance operations in Canada). Today, Berkshire Hathaway is at a much different life stage as a company than Fairfax. Being a much younger and smaller company, Fairfax has the opportunity to learn a great deal more from Berkshire Hathaway. Berkshire Hathaway is almost 60 years old as a company (in its present form). If Buffett could do it all over again, would he do anything differently? Of course he would. But let’s try and focus our discussion a little more. Today, we are going to ask a simple question: What is Berkshire Hathaway’s biggest problem today? Berkshire Hathaway’s biggest problem today is its size - it has grow into a massive company. Berkshire Hathaway has a market cap of over $1 trillion, making it the 9th largest publicly traded company in the US. I don’t think this is a controversial thing to say. And that is because Warren Buffett has been warning investors about this problem for decades. It has been getting worse every year. And it will continue to get worse every year moving forward. Why is size a problem? Berkshire Hathaway generates an enormous amount of excess capital every year. But because of its size, it now has a very limited opportunity set. This makes reinvestment of its excess capital very difficult. This lowers the rate of return the company is able to earn. As a result, the growing size of Berkshire Hathaway has been slowing the CAGR of the stock for decades. From a well above average rate of 29.2% for the first 30 years (1965 to 1994). To an above average rate of 15.7% for the next 10 years (1994 to 2004). To an average rate of 10.8% for the past 20 years (2004 to 2024). The rate of return being generated today is not a terrible thing. But clearly it is not what it once was. What is the root cause of the problem? The root cause of the problem is the power of compounding and time. As any investor knows (especially Buffett) compounding is an amazing and unstoppable force. Especially when given enough time. The result is magic. Decades ago, Berkshire Hathaway’s share price got to the exciting part of compounding curve (the hockey stick part). Ok… Yes, Buffett is the GOAT. Are we done? No, not so fast. Let’s ask another question: Was there anything Buffett could have done to stop the problem from happening? No, I don’t think there was anything Buffett could have done to stop Berkshire Hathaway from becoming such a large company. Ok. Dead end. Let’s reframe the question: Was there anything Buffett could have done to slow the problem from happening? Yes, I think there likely were some things Buffett could have done to slow Berkshire Hathaway from becoming such a large company. Like what? I can think of two things: Stock buybacks Buy and hold forever (steep aversion to selling anything) Both of these are big topics. Today, I am going to focus only on buybacks. How does buying back stock shrink the size of a company? Share buybacks are paid for using cash. This shrinks both assets and shareholders’ equity. Lower shareholders equity shrinks the size of the company. Stock Buybacks One of the reason’s Berkshire Hathaway got so big was Buffett refused to do any stock buybacks for many years. Even during extended periods when the company’s stock was cheap. Yes, Buffett had a good reason for not doing buybacks - he could usually earn a better return by allocating excess capital in other ways. This was clearly the right short term decision. And, with hindsight, arguably the wrong long term decision for the company and shareholders. Quality at a fair price “A great business at a fair price is superior to a fair business at a great price.” Charlie Munger Price/valuation might have been part of the problem. Perhaps Buffett was simply being too cheap - only wanting to buy back Berkshire Hathaway stock when it was wicked cheap (not just cheap). This would have severely restricted the opportunity for Buffett to buy back stock. This also makes no sense. Munger (supposedly) taught Buffett that it was preferable to buy “a great business at a fair price.” Why would this logic not apply to Berkshire Hathaway itself? Berkshire Hathaway was not just a great business… it was the best business in the world. And at many times in the past its shares were available at a fair price. A double standard? What is puzzling is Buffett loves it when companies he owns do big share buybacks (when their stock is trading at a low valuation). Apple is the best recent example. Buffett has been a big cheerleader of Apple’s buybacks for years. (Interestingly, massive buybacks have helped slow Apple’s own ‘too big’ size problem.) When it came to buybacks, Buffett seemed to have two standards - one for Berkshire Hathaway and another for the publicly traded stocks it owned. Buffett finally capitulates In 2011, Buffett finally relented and issued an official buyback policy for Berkshire Hathaway. But he set a buyback valuation threshold of 1.2 x BV. Really? That cheap? The result was Berkshire Hathaway repurchased few shares in the subsequent years. In 2018, Buffett ended the buyback valuation threshold of 1.2 x BV and gave management more discretion with when doing buybacks. As a result, the pace of buybacks increased quite a bit. But Buffett was decades too late - Berkshire Hathaway had already become a monster in size. The window of opportunity to use buybacks as a way to keep Berkshire Hathaway small was long gone. The Berkshire Hathaway multiverse Now imagine an alternate universe - imagine a past where Buffett was more open minded to share buybacks - actually did them in size at the appropriate times. Perhaps up to valuation threshold of 1.5 x BV - hardly a stretch for a company of Berkshire Hathaway’s quality. Would that have perhaps lowered past returns a little for investors? Probably a little. But it would have kept the size of the company smaller, perhaps much smaller. And this would have likely allowed the company to continue to compound at a much higher rate of return for a longer period of time - perhaps much longer. Summary Buffett has known for decades that Berkshire Hathaway was becoming too large of a company. After all, if anyone understands the power of compounding and time it is Buffett. I think it can be convincingly argued that Buffett did not do enough to manage that specific problem, especially 20 or even 30 years ago (when it was becoming apparent). Like being more open minded with stock buybacks (the concept and the price at which they made sense). Is this perhaps an example of where Buffett was not thinking long term enough? Yes, that question is a bit of a mind-bender. But it appears ‘long term’ to Buffett might have meant ‘during his lifetime’ (in terms of Berkshire Hathaway being an above average compounding machine). Of course, Berkshire Hathaway is a wonderful company. But it is no longer an above average compounding machine. And the risk for the company moving forward is it shifts from an ‘average’ to ‘below average’ rate of return for long term shareholders. Is there a lesson here for Fairfax? Yes, I think there is. An important one that is not on the radar today of long term investors. Buybacks are good because of all the usual reasons: When done at favourable prices (i.e. below intrinsic value), they deliver significant value. They increase the ownership stake of long term shareholders. They are a high certainty capital allocation activity. They are a sign management is rational and working in the best interests of long term shareholders. For compounding machines like Fairfax, we now have one more good reason to do buybacks. Especially when looking 10 or 20 years into the future. By meaningfully shrinking the size of the company (with aggressive buybacks over a long period of time), it allows compounding to continue at above average rates of return for a much longer period of time - it extends the runway of a compounding machine. Another important lesson: Don’t cheap out on the price you pay. As Charlie Munger taught investors, pay a fair price for a quality business - this will allow you to buy back many more shares than would otherwise be the case. What has Fairfax been doing? Fairfax has been aggressively buying back its stock since 2017. From 2017 to 2024, it has reduced effective shares outstanding by 6.1 million, or 21.9%, at an average cost of $637/share. The shares were repurchased at a crazy low price. And a significant number of shares have been repurchased. And if we include the FFH-total return swaps, Fairfax got exposure to 7.8 million of its shares, or 28.3%, at an average cost of $577/share. A very good news story is even better. In 2025, Fairfax has continued to buyback shares. YTD (to September 30, 2025), my guess is they have taken out around 400,000 more shares. In August and September, shares were likely repurchased at around $1,700/share. We will get details when Fairfax reports Q3 results on November 6, 2025. It appears Fairfax is comfortable paying ‘a fair price for a great business.’ This is another example of Fairfax moving up the quality ladder when deploying their excess capital. Bottom line, it looks like Fairfax has gotten the memo - they appear to understand Berkshire Hathaway’s size problem. And the management team at Fairfax appears to be doing something about it - in a pretty aggressive way. With buybacks it looks like Fairfax is thinking long term - the benefits of the buybacks being done today will flow to shareholders for decades into the future. This discussion leads us to another really important and related topic. Is having a chronically low share price (valuation) a good or a bad thing for Fairfax? Having a chronically low share price (valuation) has been a gift for Fairfax and its shareholders. It has allowed the company to buy back an enormous amount of stock over the past 7 years - to get exposure to 28.3% of its effective shares outstanding at a very low average price ($577/share). This was also a high certainty/low risk use of capital for Fairfax. The interesting thing is aggressive share buybacks have not impaired the company’s ability to grow its top line (the NPW of its P/C insurance business have increased in size by about 150% from 2017 to 2024). As a result, the per share value creation for long term Fairfax shareholders has been enormous. Bottom line, a low share price - especially if it persists for years - is a big benefit for long term Fairfax shareholders. Remember this when you look at Fairfax’s stock price each day.

1 point

1 point