Leaderboard

Popular Content

Showing content with the highest reputation on 07/14/2023 in Posts

-

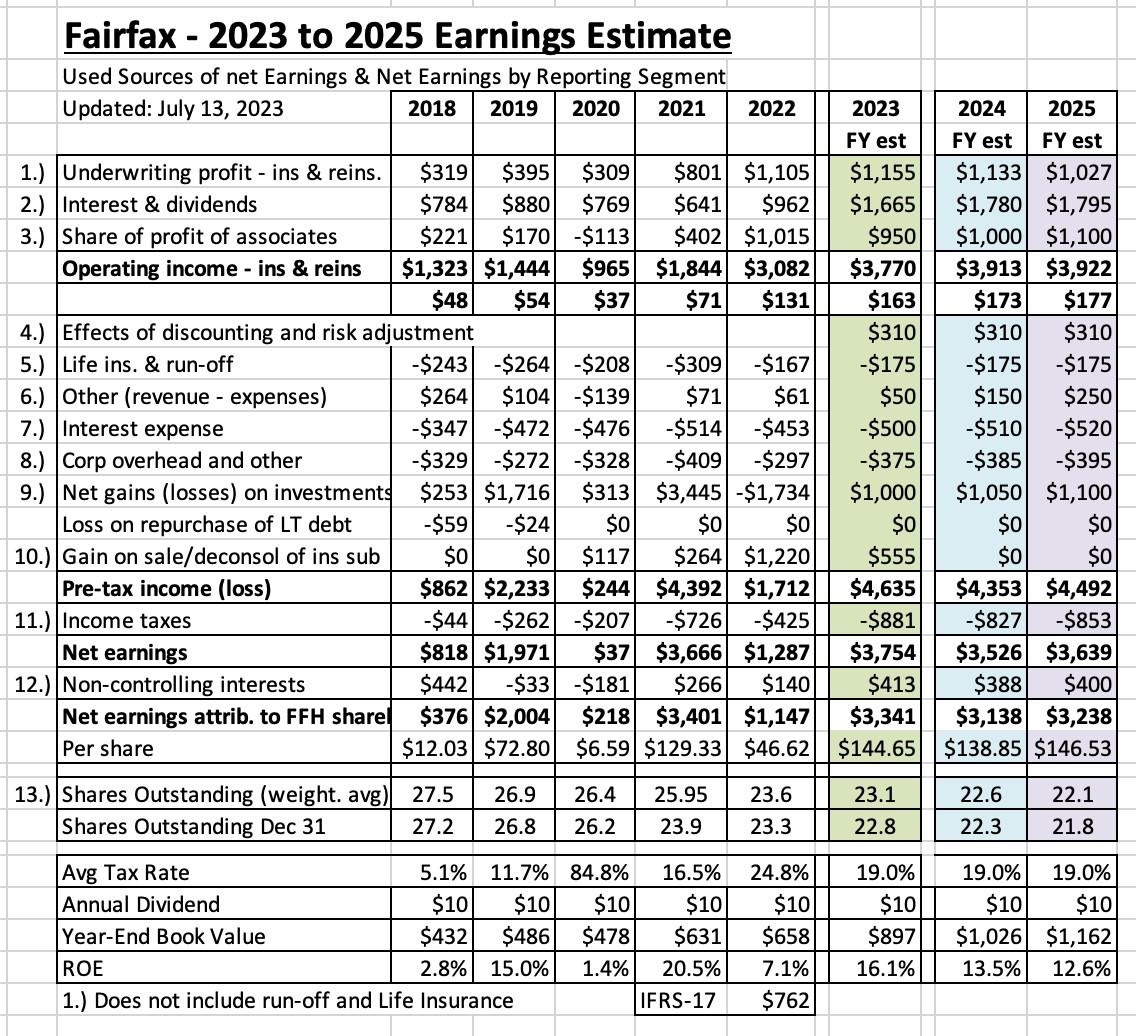

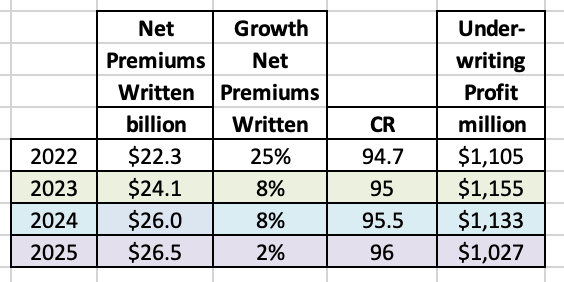

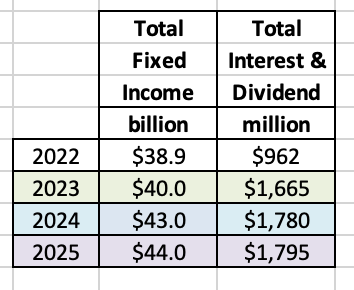

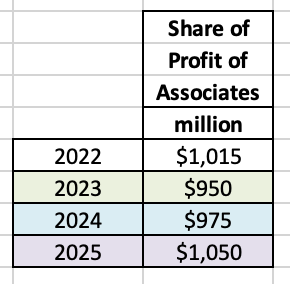

As we begin Q3, this is a good time to update earnings estimates for Fairfax for 2023. And look ahead to 2024. I am also going to take a stab at 2025. I don’t like to go much beyond 2 years with earnings estimates - there are simply to many moving parts. But it useful to get a three year view on earnings to better be able to value the stock price today - so lets give it a shot. My first big learning has been: the GIG acquisition is going to be a material development for Fairfax when it closes. I need to get up to speed with GIG (I may need to revise my estimates below). Please chime in with your thoughts. Too optimistic? Too pessimistic? Any thoughts on what GIG is going to deliver? What important things are missing? Please get into the weeds. Conclusion: Let's skip ahead to the conclusion. My estimate is Fairfax will earn about $140/share, on average, over the next three years. I consider this to be a mildly conservative estimate - what i mean by that is i think it is more likely that earnings will come in higher than lower. The big ‘miss’ with my estimates is capital allocation. We don’t know much of what the management team at Fairfax is going to do with all the earnings (around $3.2 billion) coming each of the next 3 years. Looking at the last 5 years, the management team has been best-in-class with capital allocation. My guess is they will continue to make good decisions (on balance) and this will benefit shareholders - providing a tailwind to my forecast. I am also assuming interest rates remain roughly at current levels. Of course this will not be the case. But if rates rise - or go lower - Fairfax will have lots of puts and takes. I am also forecasting no impact from IFRS 17 (as I have stated before, I am still learning how this accounting change affects Fairfax’s reported results over time.) I love the following 8-year snapshot of Fairfax. It communicates really well the dramatic transformation that has happened at the company beginning in 2021. It is a pretty amazing story. What are the key assumptions? 1.) underwriting profit to be flat to slightly down. Estimates for both premium growth and CR are conservative. When the GIG transaction closes (Q4?) Fairfax will be getting a big boost to its insurance business. I think GIG might be adding $1.8 billion to net written premiums. GIG is the driver to top line growth of 8% in 2024. If the hard market continues into 2024 then top line growth at Fairfax will likely be +10%. I am forecasting Fairfax’s CR to increase from 94.7 in 2022 to 96 in 2025. Do I think this will happen? No. My guess is they will continue to deliver a 95 CR - until I learn something that tells me something new. The hard market will end at some point. But do things quickly turn ugly? Probably not, but not sure. 2.) interest and dividend income: Will increase modestly. Extending the average duration of the fixed income portfolio to 2.5 years largely locks in these numbers. Tailwinds: GIG: will add about $2.4 billion to total investment portfolio. At estimated total return of 4.5% = $110 million. I expect the majority of this would be interest income. PacWest loans: $100 million incremental ($200 million total) to interest income? Half in 2H, 2023 and half in 1H, 2024. Eurobank: likely dividend starting in 2024 = $60 million? Headwind: Short term treasury rates likely come down lowering interest on cash/short term balances. 3.) Share of profit of associates: Will increase modestly. It fell in 2023 because of the sale of Resolute Forest Products - who contributed $159 million in 2022. GIG purchase will subtract $80 million in 2024 (same as what is built in for 2023). growing earnings at Eurobank and Poseidon/Atlas will power this higher. My estimates for Stelco and EXCO are very conservative (a combined total of $110 million per year). 4.) Effects of discounting and risk adjustment (IFRS 17). Interest rate changes drive this bucket. I need time to learn how much. Given I am forecasting interest rates to remain about where they are today I am leaving this number the same over the forecast period. 5.) Life insurance and runoff. This combination of business lost $167 million in 2022. I am forecasting this bucket to lose $175 million in each of the next three years. We should expect Eurolife to grow its earnings nicely over time. 6.) Other (revenue-expenses): improving results from consolidated holdings. In the near term, perhaps we get write downs in both Boat Rocker and Farmers Edge. Recipe should deliver solid and growing earnings of better than $100 million per year. Earnings at Dexterra are growing again. AGT is a sleeper holding. Grivalia Properties is in its peak investment phase; earnings should grow nicely looking out a year or two. This bucket could really start to shine through for Fairfax in the coming years. 7.) Interest expense: modest increase. 8.) Corporate overhead and other: took the average of last 3 years and added 10% 9.) Net gains on investments: This is a wild card. My estimates assume: mark-to-market equity holdings of $7.8 billion increase in value by 10% per year = $800 million. there is a small bump of $200-$300 million per year in additional gains (equities and fixed income). Total return on investment portfolio is: 2023 = 7.5% 2024 = 6.8% 2025 = 7.0% (I get this by adding up the following line items: 2.) + 3.) + 6.) + 9.) and divided the total by the value of their investment portfolio). These percent returns, while high compared to recent years, are hardly heroic given Fairfax is currently earnings about 4% on their fixed income portfolio. 10.) Gain on sale/deconsol of insurance sub: this is where I put the really large monetizations. 2022 was the sale of pet insurance and Resolute. 2023 was the sale of Ambridge and the purchase of GIG (resulting in a write up of the existing holding). I am building in nothing for 2024 and 2025 and this is highly unlikely. We likely will get a Digit IPO at some point over the next year and this could result in a significant gain for Fairfax. We could get an event that triggers a revaluation of Eurobank (carrying value is currently $500 million below market value and this will likely widen significantly in the coming years). We could see an AGT IPO. Fairfax is likely to sell another large holding for a significant gain. Bottom line, this is probably where I will be most wrong with my forecast. Developments here will have a material positive impact to Fairfax’s reported results (earnings and book value). 11.) Income taxes: estimated at 19% 12.) Non-controlling interests: estimated at 11% (not really sure) 13.) Shares Outstanding: reduced by 500,000 per year. This is in line with a normal year from Fairfax. It would not surprise me to see Fairfax do one more big repurchase to take advantage of the low share price while it lasts.

1 point

1 point