jfoshee

-

Posts

16 -

Joined

-

Last visited

jfoshee's Achievements

")

-

I am working on a Chrome Extension that will provide me some convenient resources when browsing COBF. For example, I want to easily jump to SEC Filings, Yahoo Finance or GuruFocus while reading the thread on a particular stock. Is this something that anyone else would be interested in?

-

Yes, I'm also a fan of Damodaran's treatment of the subject. Just in case readers are not aware, Damodaran used to recommend proactively adding leases to liabilities because they weren't typically present on the balance sheet. However, since 2019 operating leases are on the balance sheet (along w/ a corresponding asset for right-of-use). See ASC 842. I presume Damodaran has changed his treatment of leases somewhat since that time. And yes the idea of applying these adjustments to historical statements is interesting since we have the benefit of hindsight.

Yes, I'm also a fan of Damodaran's treatment of the subject. Just in case readers are not aware, Damodaran used to recommend proactively adding leases to liabilities because they weren't typically present on the balance sheet. However, since 2019 operating leases are on the balance sheet (along w/ a corresponding asset for right-of-use). See ASC 842. I presume Damodaran has changed his treatment of leases somewhat since that time. And yes the idea of applying these adjustments to historical statements is interesting since we have the benefit of hindsight. -

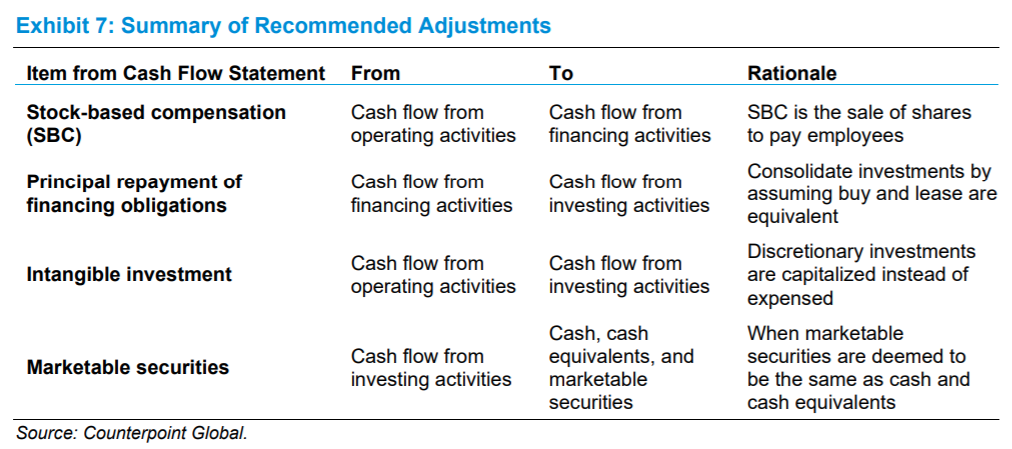

https://www.morganstanley.com/im/publication/insights/articles/article_categorizingforclarity.pdf The linked Consilient Observer article is an easily accessible case study on making a few minor adjustments to the Cash Flow Statement that will appeal to Value Investors. The authors provide not only helpful historical context around the accepted accounting, but also background on the perspective of the investor seeking to understand free cash flow. They recommend 4 adjustments to the Cash Flow Statement, described in the attached table. I personally found the article, and its presentation, to be very helpful! I never liked the simple heuristic of just subtracting PP&E from NOPAT. Herein are some tools for capitalizing R&D and intangibles for a better estimate of the needed reinvestments!

-

Warshaw's site includes additional resources including a self-produced documentary of the same title. https://newonceuponatari.hswarshaw.com/