merkhet

-

Posts

3,070 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by merkhet

-

It is, in fact, a pretty controversial statement because of the things that you have inadvertently left out: (1) It is unlikely that a person who is symptomatic with ebola is next to you. This is because people with 102+ degree fevers who are vomiting everywhere probably aren't on public transport and/or taking a nice little jaunt to the mall. They are at home. Vomiting. (2) Asymptomatic ebola infections do occur, but they occur because the levels of ebola in their system aren't quite high enough to make them feverish and vomiting. As a result, it is unlikely that asymptomatic person is going to end up getting anyone sick -- maybe if you have an asymptomatic person who happens to also have the flu. I suppose that's possible though it has a low probability. (3) Try not to let anyone cough or sneeze directly into your mouth. Especially if you have just seen them vomit next to you. The problem with that study is that it's literally a lab environment where the monkeys were enclosed with the aerosol for over 10 minutes. This is different than an airplane because the airplane is not a lab environment -- it is more hazardous and/or less sterile. This is actually more important than most people realize. At the end of the day, if ebola was transmittable by air, we would see a much higher rate of infection on par with something like the flu. The fact that we don't see that is pretty damn conclusive for me.

-

per cdc: "if a symptomatic patient with Ebola coughs or sneezes on someone, and saliva or mucus come into contact with that person’s eyes, nose or mouth, these fluids may transmit the disease" That is not what it means to be airborne. The Ebola would be living in the fluid droplets and not the air itself. That's a big difference in terms of transmission. Also, your chances of coming into contact with a symptomatic Ebola patient are slim assuming you're not medical worker.

-

I agree with you and hope you don't feel singled out by my comments. I just meant that people here are starting to sound panicky about the spread of Ebola -- especially since it is not an airborne disease.

-

I'm no expert and no little about how this spreads. The fact that several doctors and nurses who knew what they were dealing with have been infected concerns me. Now I am assuming that they did not roll around in infected blood and may have even have worn gloves while playing with the fecal matter. I suspect this virus is very very sneaky. A virus cannot be sneaky in the same way that a stock cannot be moody. They are, in fact, rolling around in infected blood and bodily fluids by virtue of having to be in near constant contact with the patients that they are treating. The fact that they're wearing protective gear is helpful, but, as I said before, it's a highly infectious disease when it is contained within a bodily fluid of some kind. I swear, the Dow drops 400 points and all of a sudden everyone is worried about everything.

-

People need to stop freaking out. Ebola is highly infectious but not highly transmitable. This means that a little bit of a live virus in your system is going to get you sick. However, it doesn't survive very well outside of your body. http://www.cdc.gov/vhf/ebola/transmission/index.html?mobile=nocontent Just try your best not to roll around in other people's blood or play with other people's fecal matter, and you'll be fine.

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

merkhet replied to twacowfca's topic in General Discussion

(1) is correct. (3) also will not count -- I checked with my accountant about this last week. (2), on the other hand, I'm not sure about. I don't know if it's substantially the same or not. Thanks, Merkhet. If #3 is okay (swapping from one series of Pfd to another), then I feel like #2 (common to pfd) should most certainly be okay given that common and pfd are less "same" than 2 series of pfd. My apologies, I mis-typed for (3) -- my accountant says that a swap of one series of preferred for another series of preferred will be considered substantially similar securities for the purposes of the wash rule -- i.e. no tax benefit. I suspect that for (2) that it's an easier case to make that common and preferred are not substantially similar for the purposes of the wash sale rule such that the wash sale rule will not apply. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

merkhet replied to twacowfca's topic in General Discussion

But wouldn't there be a long appeals process? I feel like this is one of those cases that lasts many years and ends up in the Supreme Court. The losing party only gets one appeal by right. There is no "right" to be heard by the Supreme Court. The Supreme Court must agree to listen to the case. (1) is correct. (3) also will not count -- I checked with my accountant about this last week. (2), on the other hand, I'm not sure about. I don't know if it's substantially the same or not. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

merkhet replied to twacowfca's topic in General Discussion

The Sweeney trial, in the Court of Federal Claims, will be done by the end of next year -- if it even gets that far -- which I doubt. http://www.bloomberg.com/news/2014-10-14/fannie-mae-common-shares-rally-rebounding-from-judge-s-ruling.html An alternative thought is that me-too hedge funds are getting out of their preferred positions. -

Buffett's stock pickers are beating the market

merkhet replied to oddballstocks's topic in Berkshire Hathaway

The methodology seems to indicate they were a little fast and loose with attributions. The chart is still quite good in terms of seeing sizes of investments and the length of investment. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

merkhet replied to twacowfca's topic in General Discussion

Here's to hoping it continues. Would love to roll my common shares into preferred and hoping this difference in momentum continues to maximize my preferred exposure. Theres been 50% difference in the performance between the twp since the drop. Fannie Mae common: On 09/30: $2.69 On 10/14: $2.49 Fannie Mae Preferred S: On 09/30: $9.20 On 10/14: $4.25 I can't imagine a scenario where the preferred gets screwed but the common comes out unscathed. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

merkhet replied to twacowfca's topic in General Discussion

Depends on your broker. -

Buffett Says ‘No-Brainer’ to Get Mortgage to Short Rates

merkhet replied to dcollon's topic in Berkshire Hathaway

Interesting counterpoint. Thanks for bringing that to our attention. I'd note that there are external factors in the last three examples he provides, two in the dot-com boom and one in the housing boom, but it's interesting data nonetheless. I suppose that if mortgage rates increase, and all else remains equal, then housing prices should fall. On the other hand, if mortgage rates increase as a result of an economic boom, then housing prices would increase as well. -

Buffett Says ‘No-Brainer’ to Get Mortgage to Short Rates

merkhet replied to dcollon's topic in Berkshire Hathaway

For many of the members on this form, increasing rates on mortgages might put us in a better position to buy than lower rates. As the rates on mortgages go up, the price of housing will adjust downward -- but, importantly, the percentage required as a down payment (20%) will remain the same. Thus, the opportunity cost of investing in housing (based on locking up capital for a down payment) for many members on this forum will go down quite a bit. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

merkhet replied to twacowfca's topic in General Discussion

Millstein: http://www.cornerofberkshireandfairfax.ca/forum/general-discussion/fnma-and-fmcc-preferreds-in-search-of-the-elusive-10-bagger/msg192150/#msg192150 -

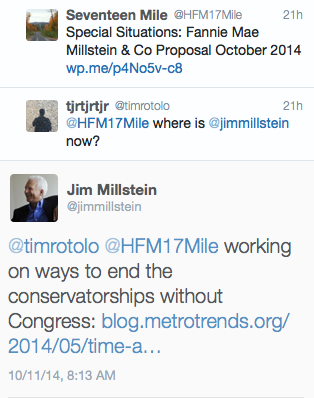

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

merkhet replied to twacowfca's topic in General Discussion

Interesting reply from Mr. Millstein on Twitter (attached). The two referenced links are as follows: http://seventeenmile.com/2014/10/10/special-situations-fannie-mae-millstein-co-proposal-october-2014/ http://blog.metrotrends.org/2014/05/time-administrative-reform-gse-conservatorships/

-

http://online.wsj.com/articles/robert-shiller-on-what-to-watch-in-this-wild-market-1412972484 Seems pretty similar to Buffett's discussions about a zone of reasonableness.

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

merkhet replied to twacowfca's topic in General Discussion

Perry's document deadlines have been set for appeal http://www.valueplays.net/2014/10/08/perry-appeal-timeline-set/ -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

merkhet replied to twacowfca's topic in General Discussion

I think either Congress or the Administration can act in this case. All true, but the fact of the matter remains that either (1) Fannie & Freddie stay nationalized, and losses remain the liability of Treasury or (2) they don't stay nationalized, and the preferred shareholders of Fannie & Freddie participate in some way with a recapitalization. Now, while I think (1) might have some incentive misalignment (cash flow now, losses later), there's two problems with it. The first one is that, since Fannie & Freddie are the only game in town, you're seeing mortgage rejections at origination because of nit-picky crap that John Stumpf has mentioned previously. If the housing market starts to weaken, they're going to start wondering if the nationalized twins are the reason. The second one is that, since Fannie & Freddie are under Treasury control, their lives depend on the whims of whoever sits at 1600 Pennsylvania Avenue. Right now, it's a Democrat. Will a Republican preserve affordable housing? As a side note, a Republican win during the mid-terms to overtake the Senate would probably force the Administration to move on this given that (A) it'll be seen as a referendum on Democrats re 2016, and (B) they might be able to push through unfavorable housing reform legislation. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

merkhet replied to twacowfca's topic in General Discussion

I played around with this thought too - that private capital has a short memory. The rejoinder, I think, may be that the required return demanded by private capital and the available quanitity are the conditions (at attractive terms) you only get one bite at. Argentina is actually a pretty good comparison because, correct me if I'm wrong, it has around $200B of public debt, right? And it pays a pretty punishing interest rate on that sovereign debt. Imagine if you had to raise that amount of risk capital? And importantly, you'd have to raise it immediately after you just told the last group of private capital to shove off... -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

merkhet replied to twacowfca's topic in General Discussion

FNMAT should be "8.25% Non-Cumulative Preferred Stock, Series T, stated value $25 per share." -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

merkhet replied to twacowfca's topic in General Discussion

A few thoughts on the policy issues inherent in Fannie & Freddie. [Warning: super long, sorry] Without Fannie & Freddie (in some form), it seems like the 30-year fixed-rate mortgage goes away. (http://www.cornerofberkshireandfairfax.ca/forum/berkshire-hathaway/buffett-says-no-brainer-to-get-mortgage-to-short-rates/msg192070/#msg192070) Those of you who have invested in AIG would be familiar with the name James Millstein, the Chief Restructuring Officer of Treasury, who was responsible in recapitalizing and privatizing AIG. After stepping down in 2011, he formed Millstein & Co. in DC and began teaching as an adjunct at one of my alma maters, Georgetown University Law Center. http://www.law.georgetown.edu/faculty/millstein-james-e.cfm Incidentally, Millstein has been very vocal about the fact that there's no practical alternative to releasing Fannie & Freddie in some way, shape or form. I would highly suggest reading the two statements I'm linking below, as I think they're fantastic overviews for understanding what Berkowitz means when he says "There is no alternative." Additionally, given Berkowitz's involvement in AIG, I can't imagine that he didn't reach out to Millstein prior to establishing his position in the private preferreds. On April 24, 2013, he gave a statement before the House. (http://financialservices.house.gov/uploadedfiles/hhrg-113-ba00-wstate-jmillstein-20130424.pdf) Editor's Note: We know from the FT article I posted that 2013 ended up w/ $17 billion in PLS issuance, not $20 billion, and is currently at around $4 billion in PLS issuance. He then goes on to talk about how the GSEs in conservatorship are keeping out private insurers. On November 22, 2013, he also gave a statement before the Senate. (http://www.banking.senate.gov/public/index.cfm?FuseAction=Files.View&FileStore_id=b56f105b-7d98-412c-b554-b79bfef60f31) Finally, see his interview on Bloomberg on December 2, 2013. (http://www.bloomberg.com/video/jim-millstein-on-fannie-mae-freddie-mac-2VsoOkALQsGHANjYyzS2LQ.html) Starting @ 4:50 My sense is that he believes, as I do, that unless the government treats private capital fairly in how they deal w/ Fannie & Freddie, it's not likely that they're going to get a second bite at private capital. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

merkhet replied to twacowfca's topic in General Discussion

There's no direct linkage as the District Court of the District of Columbia (Lamberth) is not the same system as the Court of Federal Appeals (Sweeney). While Sweeney could be influenced by Lamberth's reasoning, it would require her to reverse her own judgment and/or actions this far, which I don't think is very likely. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

merkhet replied to twacowfca's topic in General Discussion

@JonAPrior GAO: Housing market at risk from govt dominance (but FHA share dipped in '13), lays out broad points reform must have politico.pro/LxfZ5V -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

merkhet replied to twacowfca's topic in General Discussion

Investors Unite is live-tweeting the call -- -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

merkhet replied to twacowfca's topic in General Discussion

Conference ID is GSE. Just started.