bmichaud

-

Posts

1,593 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by bmichaud

-

Curious what your IRR is on your JNJ position with dividends reinvested.

-

Shiller backward 10 year P/E estimate off this decade?

bmichaud replied to original mungerville's topic in General Discussion

I was under the impression the 2002 and 2008/2009 recessionary earnings included in the Schiller E kind of offset the inflated portion of the balance. I could be wrong though, as you may be right that sales are also inflated. -

Shiller backward 10 year P/E estimate off this decade?

bmichaud replied to original mungerville's topic in General Discussion

I imagine at every historical peak in profit margins there was exhaustive analysis conducted on why that time was different and how it was difficult to see what would drive margins the other way. It is pretty clear based on the data that deficits are driving margin expansion - both Hussman and Montier discuss at length. Here is Hussman - http://www.hussmanfunds.com/wmc/wmc130408.htm Regarding cash on the balance sheets - yes corporations are much healthier than in 2007, but the SPX in aggregate still has net debt!!! I'm not yet entirely sure why cash can be backed out of the market cap when there is a net debt position.... -

Shiller backward 10 year P/E estimate off this decade?

bmichaud replied to original mungerville's topic in General Discussion

Munger, Can you explain in a bit more detail why you are adjusting the Schiller earnings downward? Doesn't the Schiller method adjust for margins? Forward SPX sales are about 1,100 - assuming the long run average NPM of 6%, that's about $65 of normal earnings. At 1560, that's a 24x pe. I'd say normal margins are more like 7%, which means $77 and a 20x pe...just to give the market the benefit of the doubt. 31x pe seems high but definitely curious as to how you get there. -

Newspapers: FT, WSJ, op-ed and bus sections of NYT and WPOST Periodicals: Economist, Value Investor Insight, Hedge Fund Wisdom (very mediocre but decent source of info) Blogs: corner, pragcap, big picture, short side of long Other: Off Wall Street - great source of deeper industry analysis On top of company filings, presentations, transcripts and available sell side notes, the above provides more than enough daily reading and a steady stream of ideas. I personally do not find much use in large screens - I haven't figured out how to narrow down a list of 50 "low-pe" stocks especially when I don't want to own more than 10. Not too difficult to figure out what the most hated sectors and stocks are just reading the paper and following financial sites such as Bloomberg and CNBC. Somewhat related side note - I just finished reading the Forbes article on Icahn from this week. Awesome depiction of how he does business - much like Buffett he never leaves his office and does a lot of work via the phone. With his Dell investment - according to the article he saw the headline that Michael Dell was taking it over and figured the stock must be cheap since Mike was putting so much equity into the deal and decided to put $1B into the company. I love it!! He is a brilliant guy, but he puts his pants on no differently than the rest of us - guarantee you be did not put in a tenth of the work Ackman did on HLF, but decided that such extreme action such as shutting down HLF entirely doesn't happen very often and that the stock is extremely cheap. Same thing with Dell - guaranteed be doesn't know the ins and outs of the future of the IT business....it's a cheap frickin stock with limited downside and he can put a lot of money to work.

-

Another Indication The Bull Market is Coming to an End!

bmichaud replied to Parsad's topic in General Discussion

It's actually 0% now :) -

Another Indication The Bull Market is Coming to an End!

bmichaud replied to Parsad's topic in General Discussion

Quick update on my anecdotal contra indicator... In addition to a lengthy phone conversation yesterday, I swapped probably 20 emails today in response to vehement and repeated attempts to convince me that the market will not decline without the Fed tightening, and since that wont happen for a couple of years it is smooth sailing until then. A couple more nuggets - the dividend discount model is bunk because it is "not real cash flow", and corporate buy backs still add value even though shares are not actually declining hahahah!!!!! A shocking conversation to say the least, especially coming from someone who is relatively intelligent. As Ericopoly said in late 2012 with regard to his excitement in anticipation of BAC's inevitable rise....I am currently quaking with greed!!! The bull case of cheap stocks relative to bonds, central bank tail risk removal and the QE put is permeating investor sentiment right now. It's palpable. -

Another Indication The Bull Market is Coming to an End!

bmichaud replied to Parsad's topic in General Discussion

Good post. I agree with everything except I believe the market has priced this in with stocks projected to return less than 3% nominally over the next 7 years (per GMO). -

Another Indication The Bull Market is Coming to an End!

bmichaud replied to Parsad's topic in General Discussion

That's what I was thinking. I think it is recency effect leading folks to conclude that you need shoe-shiner stock recommendations and a credit mania for a market peak - the tech bubble had crazy individual euphoria whereas the 2007 peak was void of the individual but heavy on credit speculation and liquidity. -

Another Indication The Bull Market is Coming to an End!

bmichaud replied to Parsad's topic in General Discussion

Will they allow firms that would otherwise be unable to obtain financing to acquire companies? Or they drive rates lower? -

Another Indication The Bull Market is Coming to an End!

bmichaud replied to Parsad's topic in General Discussion

Please help me, b/c I do not understand. You keep saying to look at yields prior to when QE1 was announced.... A) What yields are you referring to? And B) What are you comparing them to? -

Another Indication The Bull Market is Coming to an End!

bmichaud replied to Parsad's topic in General Discussion

Why will that drive prices higher? That's a known event taking place - hasn't the market already accounted for that? Were CLOs a driving force behind the tech bubble market peak, the 1987 peak, or any other market peak outside of 2007? I honestly don't know - but I see that argument a lot so I'm curious. -

Another Indication The Bull Market is Coming to an End!

bmichaud replied to Parsad's topic in General Discussion

From August 1, 2010 thru May 1, 2011 the TLT dropped -6.55%. Thus over the entire course of QE2, treasury yields ROSE - precisely the opposite of what the Fed tried to achieve. From May 1, 2011 thru September 30, 2011 the TLT rose +28.65%. Thus during the "risk-off" phase triggered by the European debt crisis, treasury yields fell as investors sought safety. From August 1, 2010 thru May 1, 2011 the JNK rose +3.76%. As expected, investors sought risky assets as reserve balances rose during QE2, thus non-treasury yields fell. From May 1, 2011 thru September 30, 2011 the JNK fell -11.52%. Obviously non-treasury yields rose during this risk-off phase. 9/30/11 thru 9/30/12: JNK rose +7.92%. Junk bonds rose more in a non-QE period than they did during QE2!!! 9/30/11 thru 9/30/12: TLT rose +2.81%. CONCLUSION: QE is all in your head. I said what drove huge margin expansion - deficit spending. The market anticipates - thus the rally out of March 2009 was well in advance of deficit-driven margin expansion in anticipation of said margin expansion. Had the Republicans had their way in early 2009 and actually balanced the budget, I promise you we would not have had the rally we did. QE's effect (whatever it may have been) paled in comparison to stimulus money finding its way into the Main Street's pockets (versus bank reserve balances at Fed banks). -

Another Indication The Bull Market is Coming to an End!

bmichaud replied to Parsad's topic in General Discussion

True. But I wonder what individual equity inflows were at the all-time high in 2007 prior to a 50% decline. I don't remember euphoria at the 2007 highs outside of the institutional manager world. And by institutional manager I mean hedge funds - mutual fund managers are lemmings that are fully invested at all times, thus their "market exposure" is erroneous. -

Another Indication The Bull Market is Coming to an End!

bmichaud replied to Parsad's topic in General Discussion

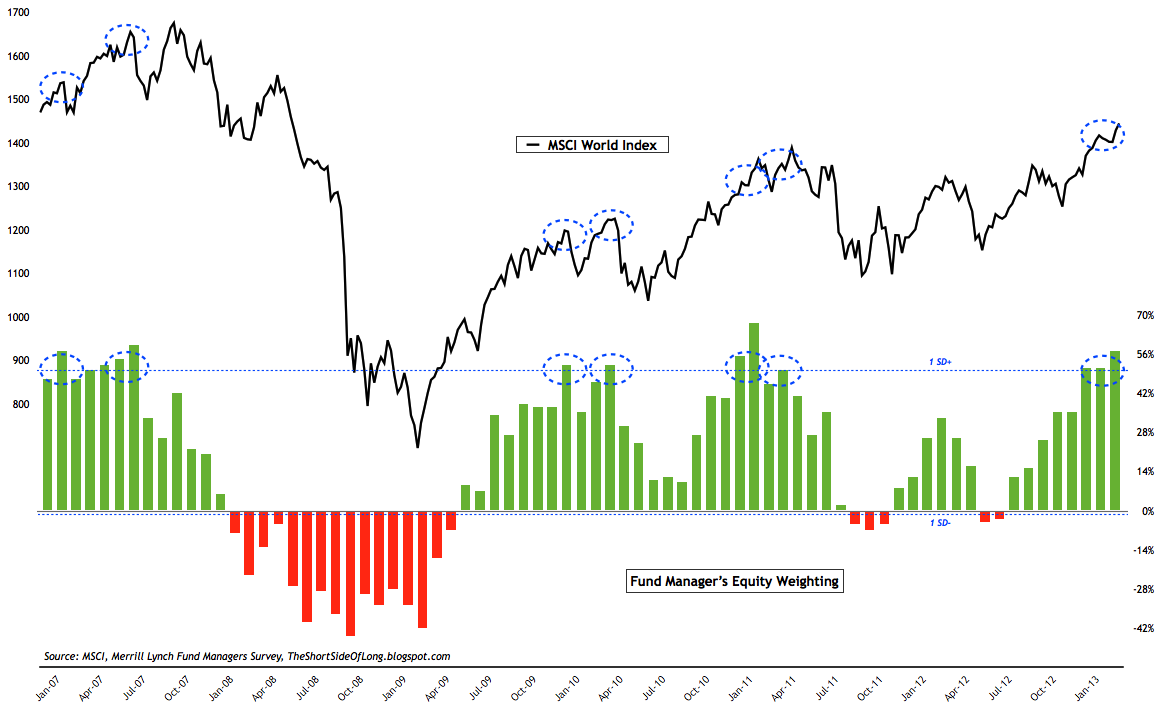

Further.... The ECB has not printed a single dime since July 2012 - all Draghi said was that he'll "do whatever it takes". Simply knowing a sovereign backstop was in place was enough to allow for risk-takers to come back in the market. Literally zero Euros flowed through the EU financial system "into" sovereign debt, bank debt, bank equities and broad equity indices. And the ECB balance sheet has actually contracted recently.... So if QE is purely psychological, then it must follow that QE is actually back-stopping something such as Draghi's yet-to-be-implemented OMT program. But wait - OMT actually backs the sovereign debt market. If you short Spanish debt to yields of 7%, you are going to get your lunch handed to you bc OMT-based printed Euros will actually buy unlimited amounts of SD at yields far lower than 7%. What is QE backstopping in order to induce risk taking? It's certainly not backstopping the treasury market - yields RISE during QE. Is it backstopping junk bonds? Last I checked A) the Fed does not buy junk bonds and B) primary dealers do not buy junk bonds with reserves held at the Fed. I think it's one of the biggest investment farces of all time. What happened to the so-called "Greenspan Put"? Did it prevent a 13-year secular bear market with two 40%+ declines? It's gotta be something else driving the market. It's gotta be corporate profits and psychology. Revenue is flat to declining. Corporate profits are contracting. And psychology is high (See attached chart)....

-

Another Indication The Bull Market is Coming to an End!

bmichaud replied to Parsad's topic in General Discussion

They do not rise prior to investor action - they rise during QE as investors sell/short safety in order to buy risky assets. Depends on what rates you are talking about. Treasury yields? Yes. Non-treasury yields in fact fell as investors took on risk from October 2011 thru September 2012....WITHOUT the help of QE. Which rates? Non-treasury rates? Heck no - everyone was risk off due to the euro crisis. Treasury yields? Yes, as investors sought safety. The Fed coming in and backstopping BAC and C (think Tepper) could have....fiscal stimulus could have. Didn't matter - sentiment became far too negative. QE was already in place. Likely the massive deficits drove it, b/c the deficits drove the huge margin expansion we've seen since then (have you seen expansionary deficits in Spain? no. Have you seen profit growth in spain? no.). -

Another Indication The Bull Market is Coming to an End!

bmichaud replied to Parsad's topic in General Discussion

I understand Dalios deleveraging thesis and keeping rates below nominal growth. However, I don't understand the mechanics. Why does rising reserve balances all of the sudden induce investors to take risk? Think about it - the act of buying risky assets drives down non-treasury yields. If someone were to explain QE to an alien, the alien would assume the Fed first drives down rates and THEN investors would buy risky assets!! It doesn't happen - the Fed causes treasury yields to in fact rise and investor action is what drives down non treasury yields. So do investors drive down yields via buying, and THEN feel compelled to buy more because rates are even lower??? Stocks were on a tear from October 2011 to September 2012, as well as all risk assets, and the Fed was not doing QE. Merely operation twist. My conclusion? QE has nothing to do with risk taking - but rather sentiment and profitability drive risk taking. Sentiment became far too negative in 2011 thus driving a QE-less rally into last September....and record high profit margins are driving the illusion that junk rated companies will never default again. QE 1 began in late 2008, yet the market proceeded to decline to its March 2009 lows. Yes QE was expanded, but massive profit expansion and extreme pessimism drove the post bottom rally. Optimism is high by virtually every measure and profits are flat to declining - I don't see how the rally materially continues. -

Another Indication The Bull Market is Coming to an End!

bmichaud replied to Parsad's topic in General Discussion

Barry Ritholtz and Hussman both use the argument that the Fed kept the market from declining further in 2011.... What did the Fed do in 2011? They implemented operation twist. If someone can walk me through the steps of how OT put a floor under the market, I would be very much appreciative. Further - if someone can walk me through how QE makes its way into stocks I would like that too. From my understanding, the Fed swaps dollars for treasurys on PD balance sheets - mechanically how do those dollars make their way from a bank balance sheet to the stock market? Are banks buying equities and I don't know about it? Last I checked, WFC, C, BAC and JPM have little equity exposure. QE is purely psychological IMO and with the entire hedge fund universe fully invested on the belief all risks are contained due to QE and the market is somehow cheap based on record high profit margins, I'm concerned. -

Another Indication The Bull Market is Coming to an End!

bmichaud replied to Parsad's topic in General Discussion

I assume most investors have their go to anecdotal contra indicator....well mine just flashed a giant sell signal last night. For reference, the day the market bottomed post election last year he was arguing that headlines were only going to get worse and was raising cash.... Last night the argument was that all risks are now off the table and the market won't correct until the Fed tightens. -

Another Indication The Bull Market is Coming to an End!

bmichaud replied to Parsad's topic in General Discussion

To moore's interest rate thesis... http://pragcap.com/interest-rates-will-rise-before-the-fed-funds-rate-rises -

SPX fair value was between 800 and 900 versus 1100 and 1200 now.

-

As predicted, market move was frothy

bmichaud replied to moore_capital54's topic in General Discussion

Let me rephrase.... Just as Moore was oddly pounding his chest after a one-day 1.8% decline, it is equally as odd that some here would feel the need to roll out quotes regarding the perils of market timing after a mere 3% move off the 1495 bottom.... -

As predicted, market move was frothy

bmichaud replied to moore_capital54's topic in General Discussion

Institutional money managers being fully invested, with margin no less, is going crazy. Every time we've had a market top in the last three years, everyone has said "this is the most hated rally ever". Obviously there is something out there that ultimately drives the market down - it only makes sense that when everyone is all-in, that there are few if any buyers left..... yes the market can flop around 3 to 5% in either direction, but I don't see how those moves are material when the risk is for a 15 to 20% correction. -

As predicted, market move was frothy

bmichaud replied to moore_capital54's topic in General Discussion

As Becky Quick rightly pointed out to Buffett when discussing the current market, Buffett is already prepared for a market decline with copious amounts of cash on hand plus more flowing in every month. He is already hedged. Just as Moore was oddly pounding his chest after a one-day 1.8% decline, it is equally as odd that bulls would be encouraged by a mere 3% move off the 1495 bottom..... -

As predicted, market move was frothy

bmichaud replied to moore_capital54's topic in General Discussion

SD?