sholland

-

Posts

50 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Posts posted by sholland

-

-

Quote

What’s a good way to estimate future natural gas prices?

IMO the difficulty in forecasting natural gas prices is the reason that this is known as a widow maker trade. Natural gas is a pure commodity sensitive to warm winters and lacks a cartel like OPEC to limit overproduction.

-

1 hour ago, Luca said:

Are you sure about 10x earnings for GDP/Inflation growth as a general rule? It depends on interest rates, maybe 10x is fine at 5%+ rates but at 2% rates, a high quality company that is in a saturated market, has a strong moat and pays 80% of cashflows via dividend shouldnt trade at 10x. If you take 10x as your exit multiple you wont find anything that looks good because quality still trades at 20x+ because it almost pays as much as bonds right now and can continue grow those 5% earnings but bonds can not.

Id say that moaty high quality businesses with little growth left but that will grow sales with inflation and keeps margin stable should still trade a bit less than risk free rate.

“The value of a business is the present value of all the future cash flows expected to occur over the lifetime of a business which is discounted at an appropriate discount rate.” - Warren Buffett

Whether the business has a moat or not does not enter into the DCF calculation. The rules of thumb I presented are just my 1st level approximations. You are correct to think in 2nd and 3rd levels about the value of a business.

-

As mentioned above, P/E multiples are a shortcut for DCF.

If you have a steady business (no growth, but no decline) it should be worth roughly 10x owner earnings.

Throw in some growth and you might justify a P/E multiple of 15.

Some extreme high growth companies like Google & Facebook in their heyday justified very high P/E multiples.

I believe that every beginner should verify what I said above with DCF models and get a feel for the process. Once you get a feel then you will not need DCF.

-

Oil producers, especially ones located in Canada. Consensus seems to be that OPEC will defend $90 oil until it is no longer defensible.

-

At the 14:15 minute mark this guy (Thunderf00t aka Phil Mason) claims that battery technology is probably as energy dense as it is going to get if you want to maintain things like safety, reliability, and rechargeability. Any exports on this board disagree?

-

Quote8 hours ago, Spooky said:

Somewhat off topic - I've been thinking lately about something that Buffett said at the AGM with respect to the World War II period and the US federal government re-organizing the whole economy and government under direction from someone from Goldman Sachs to build its war time production. Does anyone have any good books or resources about this time period and the changes to the political system and economy that took place?

-

This routine is recommended by Nassim Taleb and myself. I did it for over a year before getting back longer duration routines.

-

On 6/19/2023 at 11:27 AM, This2ShallPass said:

To the insurance experts on the board, can you pls suggest 2-3 companies that are close to Fairfax from hurricane exposure standpoint?

I'm giddy about Fairfax prospects over the next few years as well. But it's ~30% of my pf and I want to be prudent, so planning to take small otm hedge to reduce my losses in a worst case event.

You might want to look at shorting Florida insurer UVE. I shorted it (unprofitably) in 2017, 2018, and 2019 on the belief that 1) the Florida Legislature passed laws that screwed up the market and 2) a repeat of the following hurricanes would bankrupt the company:

Repeat of 1926 Miami Hurricane

Repeat of 1928 Great Okeechobie Hurricane

Repeat of 1947 Fort Lauderdale Hurricane

Repeat of 1992 Hurricane Andrew

I can provide more information if this is something you are interested in as I believe the Florida insurance situation has not changed much since I last looked at in 2019.

-

55 minutes ago, Maxwave28 said:

20% makes sense to me. Thanks for the input.

I’ve always struggled with the fact that selling outs exposes one to black swan events for little premium.

Is that a fair analysis?

conventional wisdom says only sell puts on stocks you want to buy anyways. When Buffett owned part of BNSF he sold $70 puts. I am obliged to pass on this tale of caution from Charlie Munger:

I knew a guy who had $5 million and owned his house free and clear. But he wanted to make a bit more money to support his spending, so at the peak of the internet bubble he was selling puts on internet stocks. He lost all of his money and his house and now works in a restaurant.

-

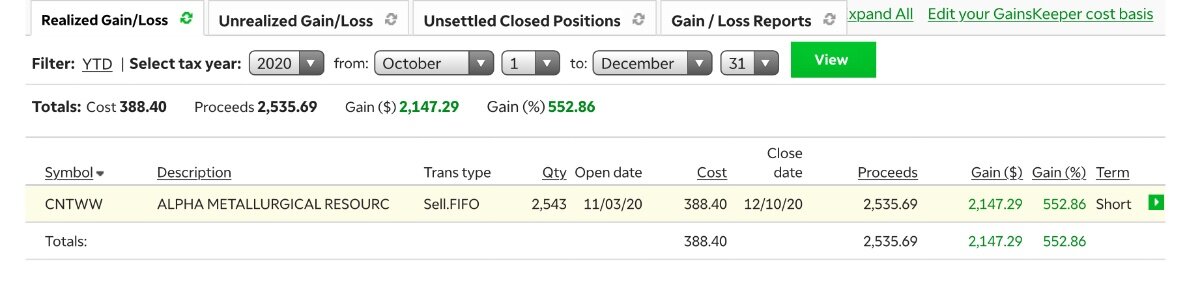

$CNTWW haunts me. In 2020 these were very illiquid. After watching these dip to $0.10 I tried to buy over 40,000 at $0.15, but only managed to buy 2543. After quickly making a couple thousand dollars tax free forever in my Roth IRA I sold. $CNTWW top ticked over $150. I missed my only chance I’ll probably ever get at a 1000 bagger. These are the little anomalies that small sums of money can take advantage of that large sums cannot.

-

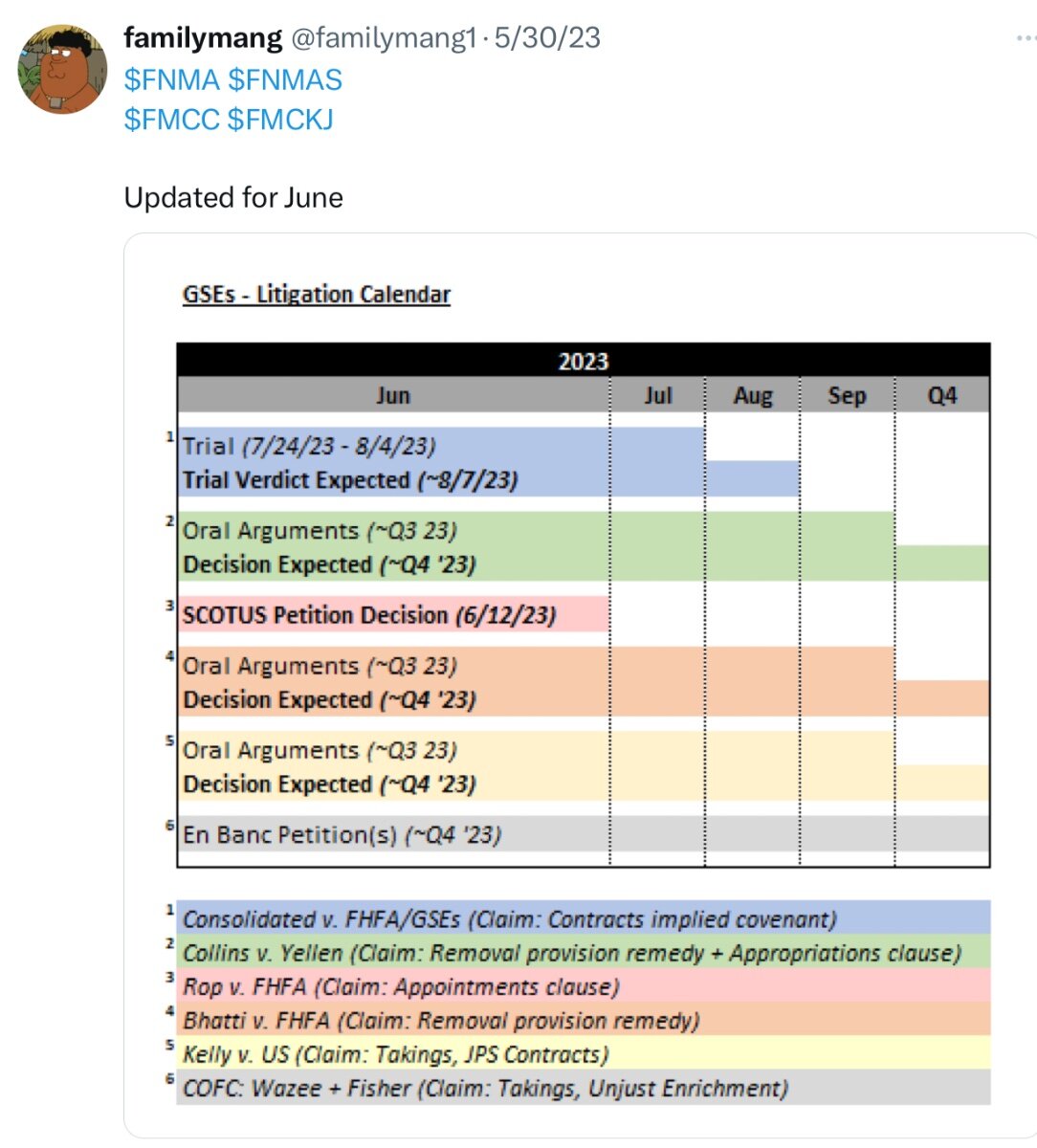

4 hours ago, TwoCitiesCapital said:

My patience, and hope in court cases, is running thin after 12 years. Just getting exhausting watching these things trade lower every day after being dead money for a decade.

Anybody keeping a watch on the progression of any of the cases through the courts? Any encouraging signs?

follow this guy on Twitter to keep up with the progression of the cases

-

Not giving us much to go on, but perhaps you are talking about Goehring and Rosencwajg

-

Agreed - I believe that the difficulty of holding the extreme temperatures and pressures over a significant amount of time (the triple product or Lawson Criterion) will prevent fusion from being a viable energy source for several decades, if ever.

-

I don’t live in Canada, but my understanding is that tax pools are transferable in a takeover/buyout. My understanding must be wrong because Prairie Provident an enterprise value of ~$140M and $861M of tax pools ($560M of which are immediately deductible). Why isn’t PPR being bought out?

-

“There is only one thing in life more important than making a little money, making a LOT of money” - John Paul Getty

-

It took me about 15 minutes to find the Bernie Sanders letter and the Warren Buffett response letter. Links below:

https://www.sanders.senate.gov/wp-content/uploads/Sanders-Letter-to-Buffett.pdf

https://www.sanders.senate.gov/wp-content/uploads/Letter.pdf

-

In the 9/6/2019 en banc opinion, (9) 5th Circuit judges ruled for prospective relief (sever the “for cause” restriction), (7) judges dissented saying that the proper remedy was retrospective (vacate the Third Amendment).

The Supreme Court has since ruled that “the shareholders no longer have any ground for prospective relief, but they retain an interest in the retrospective relief they have requested.” The Supreme Court also ruled that “Only harm caused by a confirmed Director’s implementation of the third amendment could then provide a basis for relief.”

IMO the proper remedy is to vacate the implementation of the third amendment by Senate-confirmed Director Watt starting at the beginning of the Trump Administration ($27B for $FNMA & $18B for $FMCC).

However, the Trump letter provides the argument that if not for the unconstitutionally structured FHFA then Mel Watt would have been fired 20-Jan-2016 and the GSEs would be released from Conservatorship by now. (JPS worth par)

What other retrospective relief is possible?

https://assets.realclear.com/files/2021/11/1921_trump_letter_to_rand_paul.pdf

-

If the government wants to win in the takings case all they have to say is that dividends will be resumed when the GSEs are fully capitalized. Current trajectory is about 15 more years. Preferred shareholders aren’t entitled to dividends until fully capitalized.

-

5th Amendment Takings claim is 1-2 years away. On the eve of that case does anyone think the preferred shares will not be trading much higher than 8-9 cents on the dollar? This seems like the point of maximum pessimism.

-

18 hours ago, muscleman said:

90% of your portfolio? That's insane! You seem to have high confidence on law and order, which hasn't happened for such a long time.

While I would never encourage anyone to make this a 90% position, I wouldn’t call it insane if someone has a high risk tolerance. If SCOTUS agrees with 9 of the 16 5th circuit judges that the NWS is an ultra vires action then the stock goes up bigly this month. If SCOTUS rules that the NWS is within FHFA’s statutory authority, then the plantiffs will be asking for liquidation preferences + interest @ around 9% per annum in the other court cases. Only Receivership can take away the preferred shareholders’ liquidation preferences. Receivership is extremely unlikely because Receivership will cause nearly $6T to be added to the national debt.

-

This message board has been unusually quiet lately. Am I the only one trembling with greed with the prospect of SCOTUS agreeing with the 9 of the 16 5th Circuit judges that the NWS was an ultra vires action?

I noticed that the 5th Circuit has 10 judges appointed by Reagan, Bush, or Trump and 6 judges appointed by Clinton or Obama.

9 of the 10 consecutive judges agreed that the NWS was an ultra vires action.

All 6 six of the liberal judges disagreed.

Doesn’t this mean that we can expect SCOTUS to rule 6-3 or 5-4 along party lines that the NWS was ultra vires?

-

Orthopa,

The exact answer to your question can be found here:

-

I do believe that SG will think that it is disrespectful of scotus to argue then settle. but respect seems rather old fashioned these days...

cherzeca - you believe that there will be a settlement before 9-Dec-2020.

I believe that all negotiation occurs at the 11th hour.

If true, then when do you think is the latest that settlement happens?

Seems to me that the court’s time is still wasted if settlement happens 8-Dec-2020.

-

Seems to me that it might take ~10 years to reach the 4% minimum leverage ratio. Even if g-fees are raised it will take time for earnings to increase across the entire book of business. Many comments suggest that private capital investors will be unwilling to invest the substantial equity capital needed if the re-proposed capital rule is not changed significantly. Like Tim Howard, I’ll also be very interested to see how Fannie and Freddie, and their financial advisors, react to where Calabria appears determined to take them.

Energy for AI

in General Discussion

Posted

I believe that point #2 is irrelevant to the discussion because of Jevon’s paradox.

https://en.wikipedia.org/wiki/Jevons_paradox