SI2020

-

Posts

42 -

Joined

-

Last visited

SI2020's Achievements

")

-

Berkshire Hathaway Annual Meeting 2024

SI2020 replied to good-investing's topic in Berkshire Hathaway

Anyone have any thoughts on the Trupanion event? You can register for the event on their site. https://investors.trupanion.com/news/events/event-details/2024/Annual-Investor-QA-in-Omaha-2024-f_Dz77QGtM/default.aspx -

I had some questions for investors located in the EU. 1) How is Interactive Brokers for EU investors? 2) Any issues with getting dividends from US companies (or Canadian) at the dividend withholding treaty rate of 15% (versus the standard 30%)? 3) Is there ever withholding on acquisitions or special dividends (for example company gets acquired for $10/share but you only receive $8.50/share in your account)? Thanks in advance

-

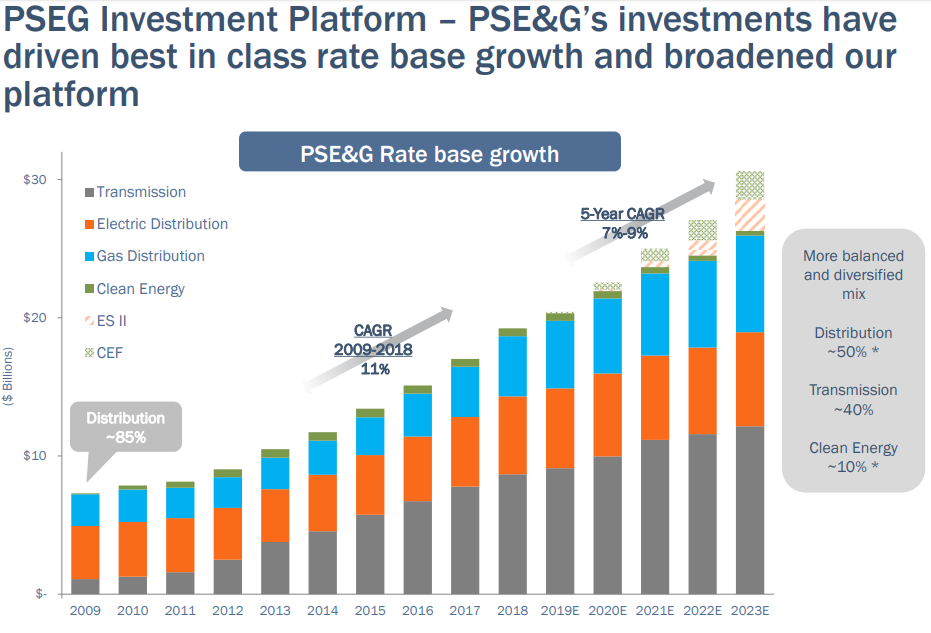

That is fair, the allowed ROE will likely not go up in such a scenario. However I would argue that the utilities are also not valued on the basis of the 5 year yield being at 0.3% forever. Lets take an example: PSEG. They are expecting $3.40 of EPS in 2020. If we value the unregulated business at 5x P/E (5*0.78), that implies that the regulated business is trading at $42.70 or a P/E of 16.3x. Not crazy cheap but doesn't that seem reasonable for the guaranteed growth on the chart that I attached plus the 4% dividend? Under what scenario do they not get that growth?

-

I don't think it's a slam dunk and the starting valuations were high, but I am still surprised they haven't outperformed more given the decline in interest rates. I think the inflation risk is lower with utilities than with bonds. If interest rates were to go up severely, allowed ROEs would likely also go up. In the 80s allowed ROEs were around 15% vs 10% today.

-

In a severely negative macro scenario, what is the impact of the crisis on the 100% regulated US utilities? Can they pass through the impact of lower load through higher pricing? Asking for both the short term and long term impact on earnings.