genesis01

-

Posts

2 -

Joined

-

Last visited

genesis01's Achievements

")

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

genesis01 replied to twacowfca's topic in General Discussion

If Thompson is selected, the companies aren't leaving the conservatorship as regulated utilities. The value transfer will occur to interested financial establishment parties without any help to the affordable housing agenda that is supposedly what this Administration ran on. Just look who is pushing for her to be in- the same crew that was in favor of the NWS. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

genesis01 replied to twacowfca's topic in General Discussion

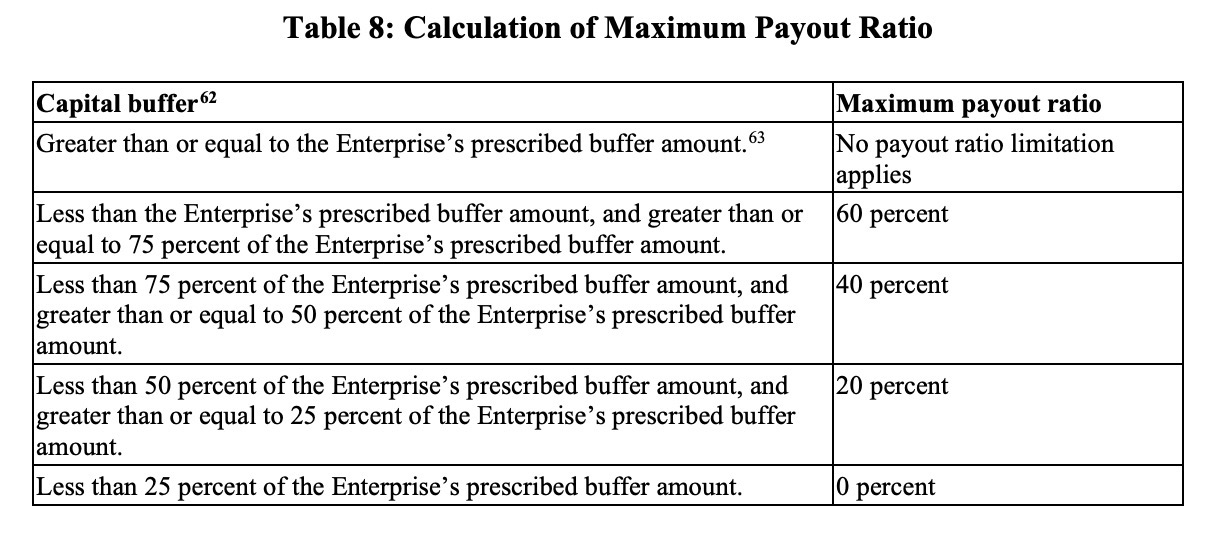

p.9 of fact sheet: "As of September 30, 2019, the combined Enterprise CET1 capital requirement would have been $76 billion (4.5 percent of RWA) and the tier 1 risk-based capital requirement would have been $101 billion (6 percent of RWA)." so forgetting about capital buffers for a moment (which restrict dividends and exec bonus payments), why is this stringent? looks reasonable. what am I missing? yes $76bn is the most bullish case which would be solid news. however i think there's also likely a restraint on the leverage ratio side. they need $152bn (89 + 63) of tier 1 capital for their leverage ratio (excluding buffer), see page 231 and 232. subtract out a reasonable component for preferred and maybe that minimum non-buffer common requirement is 100-125bn vs the 76bn you cite. well, I am still in the fact summary...it will be a long time until I get to p. 231. leverage test (p.3) is "The proposed rule would establish a minimum leverage requirement of 2.5 percent of an Enterprise’s adjusted total assets..." so I dont see that being a problem. p.9: "The adjusted total capital requirement of $135 billion would have represented 2.22 percent of adjusted total assets..." spoiler alert: 2.5pct of 6.1trn of adjusted assets is $152bn. so I shot ahead to p. 231 and see that for fannie, risk based and leverage capital requirements are $81B and $89B respectively, not taking into account buffers. this seems reasonable I have read that bonuses and dividends will be limited if buffers are not met...has anyone read in this release where it discusses how limited?