JimBowerman

-

Posts

63 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Posts posted by JimBowerman

-

-

The easing is always going to happen at the next meeting, it has been that way for a long time now.

Agree with you on that one. Despite their words, ECB unlikely to ease (but no, they aren't out of bullets, they just refuse to use those bullets.)

I (half) jokingly say: You really want the market to believe ECB will ease?...then have Draghi come out on stage with a lie detector showing his heart rate on a big screen behind him. Then have him read the following statement:

"we are doing unlimited open market operations (QE) until inflation is above 2%"

Inflation would go up in 5 minutes before any bonds need to be bought. ECB balance sheet would likely SHRINK if he did that...with inflation rising

I'm only half kidding about the lie detector :-\

Market is sniffing out ECBs weak actions not their strong words

-

imo flows are only relevant in the short run (and even then i'd be skeptical). Its like saying the reason KO went up in the 90s was because Buffett was buying 1/3 of the daily volume in the late 80s. Buffett's flow of money into KO wasn't the reason it went up over the past few decades. It was KO fundamentals

We've had a decade now of low interest rates. No QE for 6 years. Can we really keep claiming its the flow of money into treasuries that is keeping yields low? Maybe it's not low interest rates in EU or flows that is causing low rates in the US. Maybe the market is correct to expect to NGDP growth for the future and thats why yields are low?

2-3% yields in a 4% NGDP world is pretty normal. If folks think we are getting 6% NGDP growth (and 5% bond yields) that would have to be the trade of a lifetime. Short a drastic change in central bank policy we aren't seeing 5% yields for a long time...like decades

-

With the recent ECB nomination and the expected push for more easing and further dive into negative territory, it looks like Europe is following Japan in its path.

https://www.inflation.eu/inflation-rates/japan/historic-inflation/cpi-inflation-japan.aspx

imo Europe (and Japan to a greater extent) hasn't changed the 2050 supply of MB, they've just front loaded the money printing which leads to bloated central bank balance sheets but persistently low inflation. The market has sniffed this out, called the central banks bluff and,the markets have won.

I don't see any long term change in ECB policy and short a drastic change in politics, don't see inflation rising.

Far from an "expected push for more easing", when you look at the anemic NGDP growth in Japan and EU, you see that monetary policy has instead been overly restrictive and tight - and likely to remain so in the future.

Japan stating their target for the JGB is 0% only tightens monetary policy further...the exact opposite of what the bank of Japan wants.

Should note that unhelpful comments from the U.S. regarding the almost useless term of "currency manipulation" also makes any sort of needed devaluation in Japan and EU very unlikely in my opinion. The market knows all this

-

Everyone seems to think that low nominal yields imply "free money" or "central bank manipulation", but let's look at some historical data and see if there's really any difference between say 1960-2005 vs 2005-2018. At least compared to the pre 2005 era, have central banks really started printing more "free money" since 2005?

From 1915 to 2000, US nominal GDP averaged about 6.75% and 10 year bond yields averaged 5.5% or so. Given 4% or so NGDP going forward, are 2.5% bond yields really implying "Free money"? Or these low yields simply a continuation of the pattern of bond yields averaging a bit less than expected NGDP growth going forward? I'd argue it's the latter....

Next let's look at Germany. German NGDP averaged about 8.5% from 1960 to 2005. During that time, German 10 year bonds averaged about 6.75%. Since 2005, German NGDP has averaged a paltry 3.0% with German bond yields averaging about 2.25% during that time frame. If anything one could argue that German NGDP will be lower than even 3% going forward, so the 0% bond yields don't seem extremely out of the ordinary. Possibly a bit low, but given other EU bank regulations etc, it's far from abnormal. What would be abnormal is significantly higher German bond yields given the unlikelihood of higher German NGDP going forward. If folks are going to argue for higher German bond yields, then first they need to explain why German NGDP will be higher going forward.

In my opinion the ECB has shown few (if any) signs that they desire higher NGDP growth going forward, making the low EU yields about right in my opinion.

Far from "Free money", the low EU yields accurately reflect the low EU NGDP expectations going forward

-

That was an interesting read and it seems to fit with consensus thinking among central bankers with, for example, Mr. Bernanke suggesting over the years that real yields are getting lower in developed countries because of maturing age cohorts and search for yield coming from the savings glut.

Just like deflation I guess, there could be 'good' and 'bad' reasons behind low interest rates.

Money is neutral in the long run...That is, over the long run, nominal interest rates don't affect real variables.

That said, as Scott Sumner says, in the short and medium term, nominal shocks have real effects (because of sticky wages) so imo the main argument should be to keep nominal growth rates as stable as possible (which central banks have failed miserably at over the last 20 years)

When looking at nominal growth rate stability (and its correlation to real growth rates) I have to believe we can do better

That said, yes, real growth rates (because of slower population growth) should be lower going forward...but that's no excuse for lower nominal growth rates nor more volatile nominal growth rates going forward (both of which a central bank almost completely controls)

-

RuleNumberOne,

Not to deflect and I’d be happy to continue this further but the whole shadow stats conspiracy has largely been debunked imo. Someone a while back even went back and looked at the subscription prices for shadow stats.com and found the dude hadn’t even increased subscription prices at the same rate as his implied super high inflation rate. He increased prices at the much lower rate implying inflation was lower than he guessed.

Scott sumner (who has forgotten more about economics than I’ll ever know) debunked a similar argument as yours from peter Schiff all the way back in 2013 (see video below)

Summers basic point is that if inflation is really as high as you and schiff claim then rgdp would have to be negative or very low. Something that is very unlikely given the unemployment numbers. You basically have to believe the government is outright lying across multiples surveys (ngdp, unemployment, etc). Even sp500 revenues do to show anywhere near the inflation your claiming

-

It's clear that the private sector is more efficient than the government, but there are certain spending and projects that necessarily need government intervention/support.

On monetary policy, wouldn't the implementation and transmission may also impact inflation and expectations? Is quantitative easing (buying bonds) the most effective way of printing money vs writing a cheque to everyone vs adding a 0 to everyone's bank accounts?

No disagreement on the first sentence. Simply stating that we should do infrastructure spending where its needed logistically etc, not because we hope it will stoke inflation for the economy as a whole.

Imo the transmission mechanism is much less important than the credibility of the target. if the market doesn't believe the target then it won't stoke inflation. As an extreme, you could hand out $50,000 to everyone tomorrow but if you promised to tax that same $50,000 out of existence in 1 years time, then imo very little, if any, inflation would result. If forced to choose, i'd stick with the current system of open market operations, it works perfectly fine when the target is clear. Its only when the target is unclear that we get bloated central bank balance sheets, etc. Bloated CB balance sheets are a sign of failed monetary policy - expectations have not been managed and money has been too tight. See: US, ECB, and the most extreme - Japan...Commonly, central banks with the most tight policy have the largest balance sheets. It's very counterintuitive.

Inflation depends mainly on the expected long term path of the monetary base.

-

"Construction costs in Amsterdam have risen 25% over the last two years.

median home price in the Dutch capital soared 80% in the past four years to €448,000 ($505,000)."

Not sure about Amsterdam, but would guess the same applies....

But in New York, SF etc, construction costs (after removing costs from extra studies, etc) are relatively minor compared to final sale price

Its possible to build 40 story apartment buildings for $300/square foot.

However apartments in NYC/SF commonly sell for over $1200/square foot. Its the constricted supply/air rights/etc that make up much of the cost, and thats only getting worse in SF/NYC (and i presume Amsterdam)

That said, price rises in a certain industry don't imply inflation for an economy as a whole and really don't have anything to do with monetary policy (which is the only way to create long term inflation)

EU and US are very unlikely to see economy wide inflation in the near or medium term, despite rises in prices in certain sectors like housing/health care/, rising oil prices/wage pressure, etc. The oil price rises in the 1970s, and other "cost push" inflations aren't really what causes inflation. It can put pressure on the monetary authorities to print more money so unemployment doesn't rise, but its ultimately the "printing more money" which causes inflation, not the oil price rise, or the rise in housing prices, etc.

The monetary authorities are too scared of inflation to let it get out of control. Will likely have to wait for the next generation of central bankers who didn't grow up in the 1970s inflation

edit: To borrow from Einhorn's analogy...imagine rising oil prices, housing costs, etc as jelly donuts. Imagine the central banks inflation target as your body weight target. Now housing costs, rising oil prices etc will certainly put pressure on inflation just as eating only jelly donuts will also put adverse pressure on reaching your weight goal. However it is not the jelly donuts themselves that made you miss your goal weight (Some guy a few years ago actually lost weight eating only twinkies). Now eating only twinkies/jelly donuts isn't healthy and having rapidly spiking house prices isn't healthy for an economy either (all else being equal). But it's credibility of "the goal weight" which is paramount. It's the credibility of the inflation target which is paramount. The other stuff (i.e. jelly donuts, oil prices, house prices, etc) is just details.

-

Isn't it interesting that governments aren't using fiscal policy but instead focused on monetary stimulus? Clearly, at this point, monetary policy has had limited effect on driving inflation and wages higher, but may be creating risks in asset price inflation.

Don't necessarily disagree that some infrastructure spending would be beneficial, but i don't think we should hold out hope that fiscal policy will stoke growth.

There's something called the monetary offset in economics, which basically states that any increased spending on the fiscal side will be cancelled out if the monetary policy target is credible. I like to think in extremes for though experiments: If we started running a 10% fiscal deficit, but had a 2% inflation target many would worry about upcoming inflation because of large deficits. But the monetary authorities (in theory) could refuse to finance that deficit and stick with the 2% inflation target. Default, etc may happen but if a central banks wants to, it can always overwhelm fiscal policy. This is obviously a bit theoretical and in reality, politics comes into play. But imo, the more likely real world example is that we don't default but go more the japan route where, despite a huge amount of debt, their low inflation target overwhelms any fiscal deficit/debt they've had.

Would also note that if we want to stoke growth, imo monetary policy is less wasteful that fiscal policy (fiscal policy risks spending money on things that aren't needed) whereas monetary policy is more evenly distributed and less wasteful

-

Why is it the low rates have allowed for massive real estate inflation, but not equity markets?

Europe is dirt cheap on a relative basis to the U.S. If low rates act as a guaranteed inflator of asset prices, I would think European equities would've trounced U.S. equities over the past 5-years - but instead they've underperformed massively while the U.S. was raising rates?

Yeah its definitely not a guarantee and theory would certainly be more accurate in a completely closed economy. My guess is many are avoiding EU equities because earning growth is lower there than in the US. That said, i think CAPE for EU equities has been around 20 back in 2018 so not super low either.

That said i don't think market has adjusted to lower rates in either US or Europe and would expect higher multiples going forward (of course this assume Fed and ECB keep their low inflation targets).

Just a guess, but with mortgages it seems more clear cut and would expect the housing market to adjust more quickly as there's less need to forecast future interest rates (assuming fixed mortgage). If there are low rates when I buy a house thats all i kinda need to know. I can calculate my monthly payments and determine affordability. With stocks you necessarily have to guess at what rates will be in 5 years, 10 years, etc

edit: Would add that i'm talking about multiples here not total returns. In fact, while i think PE ratios will be higher going forward, I think total equity returns will be LOWER as earnings growth will be lower and tend to track the lower inflation/lower ngdp numbers going forward. Somewhat over simplistic, but if we expect ECB to have slower growth than the US going forward then wouldn't surprise me to see US outperform on a total return basis, but for the EU to have higher PE ratios during that same time period. Just a guess, and as others like TwoCities etc have pointed out, it may not always work exactly like this over even a 10 year time frame...other options for investing in equities outside one's own country, etc also complicates it a bit as we've seen

-

Denmark has negative mortgage rates and booming house prices. Governments and central bankers in Europe are far more crooked than the US. Throughout Europe you have rock-bottom interest rates and booming house prices. Debauchery of the currency is a mild description. How long can this go on?

https://www.globalpropertyguide.com/Europe/Denmark/Price-History

"Denmark´s negative interest rates continue to work their dangerous magic on both the housing and mortgage markets.

The price index of owner-occupied flats in Denmark rose by 7.88% (7.25% when adjusted for inflation) during the year to February 2018, an acceleration from last year´s growth of 6.87% (5.81% when adjusted for inflation), according to Statistics Denmark."

So for tiny Denmark, - in short - the answer to your question is actually : No. Draghi [et al.] does not decide or have jurisdiction/power over supplementary national regulation.

When looking on what's going on in EU with interest rates etc., you can't just look at it as whole. The economic situations & financial systems are only to various degrees similar among european countries.

Hi John,

Good meeting you as well and great discussion. There's a lot of moving parts imo regarding monetary policy as it relates to asset prices, so i'll try to list out at least my thoughts in bullet point order:

#1 I'd argue that monetary policy in the EU has been TOO TIGHT, not too loose. Yes, the supply of money has gone up quite a bit in the EU, but the demand for money has gone up even further. I think it's helpful to judge tightness or looseness of monetary policy based on nominal G.D.P. (which has been very low in the EU since 2008). Current short term interest rates are not a good metric for judging monetary policy and instead, low short term interest rates are usually a sign that monetary policy has (counterintuitively) been too tight. Theres a lot to this, and I explain it in much more detail across 50-100 pages in my 2017 and 2018 letters (link below in my signature)

#2 Because monetary policy has been too tight, this has led to lower Long term bond yields in the EU. As Buffett says, LT bond yields act like gravity on asset prices. Again, it's counterintuitive, but the implication is that because tight monetary policy led to lower bond yields, this results in higher house prices as mortgage rates tend to track the low bond yields in the EU.

I'm no expert on the specifics of the denmark housing market, and surely i'm missing some factors here (local building codes, zoning, etc), but at a high level i'm not surprised to see house prices rising. But its not because the ECB has been printing too much money...its the opposite...they haven't printed enough money.

I'd like to see the ECB drop its current targets and instead promise to do unlimited open market operations until NGDP is growing at 5% a year. Assuming they do this i'd argue that

1) wages would go up across the EU

2) real asset prices would drop (real house prices drop and (which also reduces income inequality)

3) populism and political tensions are reduced.

edit: as a final example showing how ECB largely controls asset prices at a high level. Lets imagine 2 scenarios. The first scenario (akin to what we currently have) is that ECB keeps money growth low and inflation low over the next 100 years. In this case, I'd expect nominal house prices to grow at a slow rate in line with money growth, but for there to be a one time boost in real house prices as the housing market adjusts to lower interest rates. At the other extreme lets imagine the ECB prints a lot more money than they currently are to the point where inflation averges 10%/yr over the next 100 years. in this case, nominal house prices would rise much more quickly than in scenario 1 (again, nominal house prices tend to track with inflation), however i'd expect real house prices to be a bit lower than in scenario 1, as the high interest rates act as a drag to real asset prices (scenario 2 would also likely result in stocks having lower P/E ratios (proxy for "real asset prices") but HIGHER nominal earnings growth/stock prices over those 100 years). I'm probably not explaining this very well so welcome any feedback!

-

Draghi & Volcker do not set market prices on real estate - buyers and sellers do.

Yes, but a central bank controls the growth path of the unit of account, which is the main measuring stick for those "buyers and sellers".

The central bank can almost completely dictate the size of the nominal economy going forward.

The below table kinda shows that housing (as % of nominal GDP) has been relatively constant.

So at a high level, can't Draghi and Volcker largely determine the nominal price of housing over a decently long time frame?

(Would add that there's no iron law that housing must be a fixed % of GDP - Its just that with various zoning laws, it's (imo) likely to stay relatively constant. Without those laws, there's a (good?) chance that housing would represent an ever decreasing % of GDP, much like food has done over the last century)

https://cdn.theatlantic.com/static/mt/assets/business/1900%201950%202003.png

-

Jim, i agree that generally speaking lower bond yields should support higher PE multiples. Given the abrupt and large move lower in US yields i am wondering if the bond market is forcasting slower global growth moving forward; this will result in lower earnings for companies and usually leads to lower equity prices.

I am just surprised at the abrupt pivot in the thinking of bond investors. 12 months ago all the talk was how 10 year yields in the US would be pushing 3.5% and perhaps even 4%). Today we have 10 year rates below 2.3% with some saying they may fall below 2%. I am just trying to understand what is driving the pivot. The stock market looks oblivious to what has been going on in the stock market and i find this interesting.

I think in the 20th century you had approximately 2.1% productivity growth + 1.25% population + 3.4% inflation = 6.75% nominal GDP growth. No surprise that average 10 year yield was in the 5-6% range during the 20th century with an average PE ratio of 15-20

Going forward, in the 21st century, i'd guess we see something more like 1.75% productivity growth + 0.5% population growth + 2% inflation = 4.25% nominal GDP growth, in which case bond yields staying consistently below 3.5% doesn't seem abnormal to me. P/E ratios around 30 wouldn't surprise me in such a low growth environment.

Important to note that i'm much more sure about population and productivity numbers going forward. The 2% inflation guess is simply an educated guess. Political climate could change tomorrow and 4% inflation could be the norm. I'm not great an handicapping politics so take my inflation guess with a grain of salt. Of course we are all forced to guess at the future inflation rate whether we'd like to admit it or not. IMO Buffett is implicitly guessing at a higher inflation rate by holding so much cash. He very well may be right.

I compared a few other metrics in the 20th century vs 21st century. Very rough approximates and guess, but found the it useful for me.

Should note that, as you mentioned, earnings will be lower despite higher P/E ratios. As you can see in the last row in my table, the overall equity return is lower going forward despite higher average P/E ratios (absolute earnings growth is lower corresponding with lower NGDP growth)

-

Does anyone have any thoughts on what the bond market and the stock market are currently telling investors? In the US long bond yields have been coming down for the last eight months. They certainly seem to be forecasting much lower growth moving forward. The stock market on the other hand is 5% from its highs and seems to see solid economic growth moving forward. The two perspectives do not seem to line up.

My view is the bond market tends to give investors better information than the stock market over the short to medium term.

Imo this is a common misconception. Perpetual lower bond yields/growth lead to HIGHER stock multiples. I guess one could argue over whether growth will be perpetually lower or just temporarily lower. I think with the low inflation target, and lower population growth going forward, that we indeed will have lower (nominal) growth going forward and that stock multiples with therefore be higher than they've been in the past.

As Buffett said: "if you had zero interest rates and you knew you were going to have them forever, stocks should trade at 100 or 200 times earnings".

Lower interest rates = Higher P/E ratios

Would also add that, in general, QE leads to higher interest rates not lower interest rates. Europe has low rates because they haven't done enough money printing...ECB monetary policy has been much tighter than US, hence Europe has lower rates

-

Isn't this the exact opposite of the logic that determines higher growth companies deserve higher multiples? Why would high growth lead to high multiples at the micro level and low growth lead to them at the macro level?

If low GDP is the secret to high multiples, where are they in Germany and Japan 0?

Buffett answers that question here:

-

If you top ticked the S&P 500 in 2007 and held all the way down then back up to present, you'd have averaged something like 7.5% a year.

I don't think stocks are nearly as expensive now as they were in 2007, so i'll throw my guess in the there and predict that stocks will do about 7 or 8% a year over the next decade.

Also don't see a recession on the horizon at the moment, of course that involves some guess work on the intentions/future actions of the Fed, so take it with a grain of salt.

As cameronfed alluded to, multiples should be higher going forward. The standard average 16 P/E Ratio occurred when nominal G.D.P. averaged over 6% in the 20th century.

I think N.G.D.P. will be more like 4% going forward, so multiples will likely be higher...and current multiples are justified on a long term basis

-

There hasn't been "financial repression". Low rates signify policy has been too tight, not too easy.

That said, with lower RGDP growth and 2% inflation going forward, multiples will be a lot higher than their historical average. Stocks are about fairly valued right now (assuming the Fed can keep NGDP on a 4% growth path and not batch it like they did in 2008)

-

Wish he would list performance since inception like Buffett does (ideally by year). Always rubs me the wrong way when this sort of basic info is omitted and can't help but feel its on purpose.

-

I'm missing the option: "Interest rates should be set by the free market rather than a central bank."

Edit:

While reading all the posts saw rkbabang already made my point.

I'm probably beating a dead horse at this point, but i'd just add that imo, the only way the market can truly set interest rates is if the money supply is also dictated by the market (i.e. private currencies). I get confused when people start claiming that the fed only started manipulating interest rates post 2008. The fed dictates the supply of base money, so they are always going to be setting (nominal) interest rates. The market has never truly set interest rates, and the market certainly didn't dictate interest rates before 2008. That said, on a personal level, I don't really care whether we have 0% inflation vs 2% inflation. Real gdp per capita grew about the same in the 1800s (0% inflation) as it did in the 1900s (3% inflation).

-

Nothing the fed does is a market phenomenon. It is government setting rates. No different from the USSR setting prices in their economy either by their own opinions or sometimes by looking at ads in London Newspapers. If the rate is set by the fed then it isn't being set by the market. If the price of Avocados was set by a government board and you asked me "What do you think about the Federal Avocado Board reducing prices in 2009-2013? Did they do the right thing?" My answer would be the same. I don't know. The market should be setting the rate not some board of bureaucrats/experts.

The fed controls the supply of base money, so how can the market ever truly be setting rates? If you're going to have a national currency, someone has to decide how quickly to grow money supply, no?

-

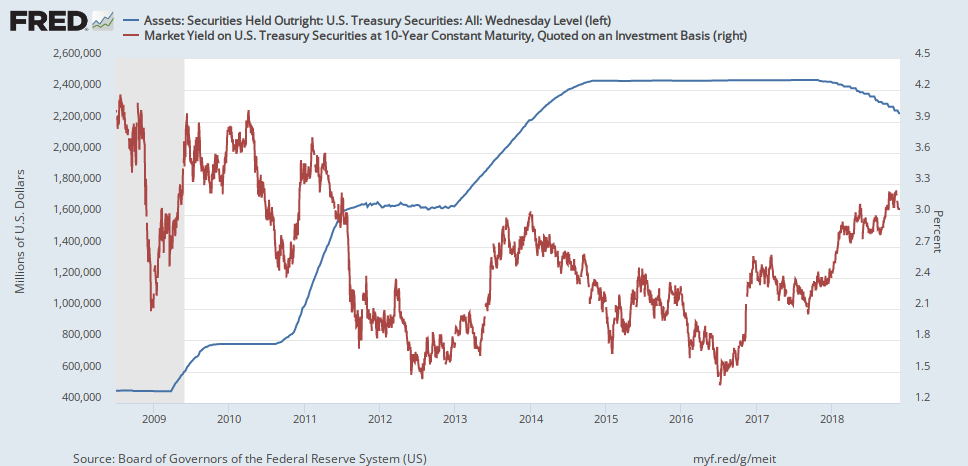

If you overlay the chart of the Fed's balance sheet and interest rates, you can see that the initiation of a new round of QE was always accompanied by an INCREASE in interest rates (In the attached I'm showing the 10-year). I think most people get the direction of causation wrong. The Fed increased its QE efforts when it felt that interest rates were getting too low and therefore deflationary pressures were getting too high.

(Link to graph here as well: https://fred.stlouisfed.org/graph/fredgraph.png?g=meit)

Interesting. We could "fight" back and forth with graphs forever and run into circular arguments but did you consider that whatever effects are produced by what the Fed does or is expected to do happens with a lag? What about what is going on now as we see the early effects of tightening (opposite of easing): are interest rates going down?

maybe4less is exactly right. Under most circumstances, large amounts of QE will result in higher interest rates (espeically when there is a lot of slack in the economy as there was during QE1 -3). Looking at only the first order effects leads one to think that buying more of something should increase prices (and drop rates). However, the expectation of higher inflation leads investors to start demanding higher rates. The 2nd order effect of a central bank buying tons of bonds is to, counter intuitively, raise interest rates. That's why Zimbabwe, Wiemar Republic, US in the early 1980s etc all had very high nominal interest rates during their bouts of inflation, despite huge amounts of bond purchases by the Fed.

If rates remained low while inflation was so clearly going to rise, then you could make a killing borrowing at such low rates. In reality, the market would adjust before you could take advantage...just not that easy to make money like that. There wouldn't be much of a lag at all...it would be fairly instantaneous. Furthermore, inflation would also almost instantly rise today if the Fed promised to print the $15 Trillion in 2 years time. Again, if rates didnt' rise right away, then an investor could borrow a ton at the current low rates and make a killing when rates rose in 2 years. This would be arbitraged out almost instantly causing rates to rise today, well in advance of the actual money printing in 2 years

With inflation its all about expectations.

-

@JimBowerman

The definition of the hot potato effect that you describe does not correspond to my understanding. You seem to imply that the 1,7 trillion injected by the FED through the QEs was transmitted to the economy because banks were induced to lend more. That does not seem to be the case and I understand that even the FED acknowledges that the real economy was not really affected, apart from the unverifiable comment that a worse depression was prevented, which is really something, if true. The hot potato effect that you describe seems to be related to the fact that, through an induced new equilibrium, the new money that found its way into the system eventually stayed at the banks but somehow encouraged chasing for yield behavior. Money did change hands but made it back to the banks as reserves but the result of the flow of new money was higher asset prices (wealth effect), especially in stocks, junk bonds, leveraged loans etc When the "excess" reserves are retired from the system, how do you call the hot potato effect? And what is the opposite of chasing for yield or wealth effect?

I read some of your stuff and look forward to becoming more educated.

My fault, I didn't clarify some of my points (btw Scott Sumner, David Beckworth, etc have forgotten more than I'll ever know on this stuff...would highly recommend them).

I think the first issue is: we don't really know what would have happened without QE. Many point to low inflation/growth as a sign of QE's failure, yet don't talk about the increase in demand for money. Imo, the rise in supply of money from QE was almost entirely offset by the rise in demand for money. With the shock to the system, the demand for money clearly skyrocked, and if we hadn't at least printed enough money to offset this rise in demand, then we would've had massive deflation and a depression. So I think QE had a huge (positive) affect, it was just a bit hidden.

Regarding the hot potato effect...its really only works if the money printed is permanent. As a thought experiment: what would happen if a CB says it will increase MB by 1000x tomorrow, but then promises to remove all this new money in 2 months time? Would inflation result? (I don't think inflation would result, and there would be very little hot potato effect). In the real world, things aren't this extreme. But the Fed increased money supply from 5% of GDP to 25% of GDP, and implied it would remove it in 10-20 years (and is proving that point with QT). Imo that won't cause very much inflation. Increasing money supply from 5% to 25% but promising to never remove it would cause much more inflation. Even better would be promising to print as much money as needed so that NGDP growth stays at 4-5%.

Look at Japan: They've increased MB to 100% of GDP but the whole time they've said/implied "The second growth gets above 0% we will remove the money". So its not surprising that growth never takes off. They snuffed out growth before it ever got started. They've said (almost explicitly) that all the money they've printed will not be permanent.

As for chasing yield/wealth effect, I'd actually take the opposite view. I believe PE ratios would be lower today if we had more QE. Stocks are influenced by 1) P/E ratios 2) earnings growth. If we (overly simplistically) assume earnings grow about in trend with nominal GDP (and remember, a CB can make NGDP whatever they want) then the low growth we've seen since 2009 has kept the absolute levels of earnings low, but this pushed up the PE ratio for stocks. Most, when they talk about bubbles, talk about the high PE ratio, so in a way people equating the fed's actions to stock market bubbles have it a bit backward. PE ratios would likely be lower if the Fed had printed more money. (my logic here isn't airtight, but I just mention it as a counterpoint to the bubble talk - I actually think stocks are fairly valued given the likelihood of low growth going forward)

When we have true inflation (1980's) we see PE ratios plummet and nobody talks about bubbles, etc. When we have depressions, stocks plummet and again there's no bubble talk. Its in this small window of "very low, but positive interest rates" where it gets confusing.

-

But the FED cannot force people to take on loans and it can't force banks to lend which means it can't increase the money supply directly.

I might be arguing semantics, so we if we agree let me know, but while in theory a CB can't directly influence money supply, in practice it can make the money supply whatever it wants. Again, I always like to think in extremes, but if the CB increased MB by 1000x tomorrow and promised to not remove it, then banks in theory could just sit on the money and refuse to lend it out. But that would never happen. Instead this huge increase in the supply of money would decrease the demand for money which would lower the threshold at which banks lend out money (hot potato effect). The money would certainly get lent out because banks would know inflation was imminent. The banks know that the CPI will go up ≈ 1000x...are they really going to sit on excess reserves earning 2% in such a scenario? No, they will lend out the money, likely at a very high interest rate. This process would work in reverse if the CB decreased reserves drastically.

Bigger picture, I think the fixation on interest rates has made us lose sight of looking at the actual money supply, which is ultimately much more important. The monetarists certainly had some flaws in their thinking, but a myopic fixation on interest rates also cause problems, as we've seen since 2009. Shameless plug, but a lot of this stuff in covered in more detail here --> http://bit.ly/2S3Y6P9.

Look at Japan, they are setting their interest rate target at 0%. This ensures that they will never have significant nominal growth. The goal of QE is to ultimately RAISE rates, not lower them. BOJ should instead promise to print permanent money until rates rise to 3% (or whatever their goal is). Counterintuitively, if they credibly promised to print permanent money like this, the increase in velocity would do much of the work, and the ultimate size of the BOJs balance sheet would eventually be much smaller than the current 100% of GDP.

-

No, it's important thought experiments! If they bought $100T the USD would tank and vice versa. You can't view rates in isolation.

Agree that the Dollar would tank. But its my contention that LT nominal rates would clearly go through the roof if they printed that much money.

The bigger point is that a central bank can (almost) always get any sort of nominal interest rate and nominal GDP growth rate that it chooses.

Its a bit worrying that the Fed, etc don't realize its own power and instead blame the low nominal growth and low nominal interest rates since 2009 on other factors like demographics, etc. These have some affect, but the Fed can always overwhelm these factors.

As a final thought experiment, if the Fed truly cannot do anything about low long term rates, why do we bother to collect taxes at all? why not just finance all government expenditures through money printing? Of course, in reality, at some point, printing money will cause inflation and raise long term rates. We just haven't done enough money printing since 2009 (and the money we have printed, has not been very permanent as we are now seeing with QT). The bond market was right in being skeptical of the Fed's willingness to print enough permanent money.

{kind=link}

{kind=link}

POLL: Fed and interest rates

in General Discussion

Posted

Would inflation go up in such a scenario?