StubbleJumper

-

Posts

2,160 -

Joined

-

Last visited

-

Days Won

4

Content Type

Profiles

Forums

Events

Everything posted by StubbleJumper

-

@Viking and @glider3834 One of the reasons that FFH's share price is in the shit-hole might be that market participants have lost confidence in Prem's decision making, and frankly the shorting episode and the deflation derivatives make that a reasonable position to hold. My view is that there are a great many good things going on with FFH, but frankly it can take a long time to re-establish confidence after episodes like that and you need a long string of clear and consistently rational decisions to convince people that you are back on the rails. The problem with BB and RFP is not the money (well, for me it's the money because I'm a cheapskate!), it's that the continued hold strikes people as irrational when there has been six months of good exit opportunities. So, is the bizarre decision making over, or is it not? Well, I don't blame anyone who is hesitant about Prem and who looks that BB and RFP with a jaundiced eye. Now, let's move on from impressions and deal with the money, because there's a bit of a bifurcation there. FFH has had *two* good opportunities to dump BB at US$14-ish and it is now trading at US$10-ish. That's US$400 million that has at least temporarily evaporated. Same deal with RFP, it trades at ~US12.25 and it could easily have been dumped at US$14.25, which is another US$60m. It is what it is. We have 27m shares outstanding and Prem has flushed *multiple* opportunities to exit legacy positions that would have provided US$460m more value to shareholders. He has basically flushed US$17/share through those decisions (so far). He might end up being right, in the end, and maybe it's not a permanent flush. And US$17/sh isn't a death-blow by any means. But the impression is not great. So, let us move to the reason *why* the impression isn't great. Prem flushed enormous amounts a shareholders capital on the shorts and to a lesser extent the deflation derivatives. Was it US$175/sh, or thereabouts (seriously, I haven't done that depressing math, but someone on this board must have). All that bullshit about ridiculously ill-conceived and stubbornly held decisions was supposed to be over, right? Well, here we go again, another US$17 of bad decisions. What's the annual quota of losses from shitty decisions, anyway? Is it US$25, or is it higher? Maybe flushing US$17 is a "good performance" in the context of the past. That's a tough sell. But, if you want to convince people that you've refocused your investment decisions and are better managing the downside, the failure to sell a couple of positions this year might have cost FFH a bit of market confidence. And rightly so. SJ

-

We need to be honest with ourselves because we ourselves are the easiest to fool. Yes, FFH has reduced its share-count on plenty of occasions, but was it *material*? Yes, when the share price was completely retarded in the 1990s, FFH bought back a boatload (much to Prem's credit) and then when it was completely retarded the other way, they issued a boatload (once again, much to Prem's credit). Let's deal with the reality of the two most recent decades: What Prem has been saying since March/April 2018 is good. Let's hope that the implementation reflects the stated intention. SJ ***edit*** BTW, does everyone see the shares outstanding in 2015? That's the year when Prem re-weighted the multiple voting shares to hold his control level at ~42% of the votes. If he wants Ben and Christine to continue to control FFH after he eventually cannot fulfill the role of CEO or Chair, the share-count needs to drop *below* that of 2015. Let's hope that is a source of motivation for the Watsa family.

-

The deflation swaps were the right thing to do, as was the equity hedging. The issue with both was the notional value that was being hedged with each instrument. I have yet to see a compelling explanation about why it was a good idea to "hedge" more than 100% of FFH's equity exposure, nor have I seen a compelling explanation about why it was a good idea to "hedge" more than US$100 billion for deflation. I put quotations around the word hedge, because if your hedge ratio exceeds 1 you aren't hedging, you are speculating. As far as the deflation swaps go, the downside wasn't too costly if you had enough conviction to agree that speculation was the right course of action. The equity swaps had a significant downside. Should FFH have had enough conviction to push their hedge ratio over 1? Did FFH manage the downside well enough? IMO, it was a risk management issue that revolved around position-sizing. Or maybe I'm just too conservative. SJ

-

I'm guessing that Prem wants to eventually buy back a large slug of FFH shares, but the question is how fast can it be done. When Prem re-weighted the multiple voting shares to ensure that the Watsa family would retain control despite the issuance of a large number of subordinated voting shares, the one concession was that the re-weighting would apply for only as long as Prem held either the position of CEO or Chair (or both). Well, Prem is currently 71 years old and is probably hoping to emulate Buffett once again and work until he's older than Methuselah. But, setting aside Prem's preferences, the life-tables say that his life expectancy is about 16 more years. If he's at all realistic, he'd be hoping that he can still function as chair in his early 80s. If he wants Christine and Ben to have control of Fairfax over the longer term, he needs to start buying back a crap-load of subordinate shares. Prior to the re-weighting, Prem was able to retain control over FFH with about 40% of the votes because people had confidence in him, but I don't think any shareholders have any reason to extend that support to Ben or Christine. I would agree with you that many founders cannot morph from empire building to shrinking the capital base, but we should keep in mind that Prem might have more motivation than most. SJ

-

I would argue that family control is a common enabler of an entrenched management team. In most companies, mediocre performance tends to attract activist shareholders who push management changes. But, when the poor management is coming from the controlling family, there's no real way for market participants to discipline the management team. While the Desmarais entities didn't trade below book for prolonged periods, the long-term mediocrity resulted in a 5-year period where the share price was basically 1x book. But, when there are no consequences to mediocrity.... I'd say that Fairfax is on the right path, but it might take a few years to convince the market of that. If people are suspicious of whacko decisions by Prem, then 2021 might not be reassuring. He has promised to stop the short-selling and he hasn't taken any large, new macro bets like the CPI options. But, on the other hand, how does the market view Prem's decision to not sell BB or RFP when the opportunity presented itself. It could take a number of years of good performance to convince market participants that the wacko decisions are a thing of the past. ELF and FFH are definitely different beasts, but don't forget that ELF was a diversified P&C and life outfit until it divested the P&C subsidiary to focus on the life business. No, it's not so much about benchmarking one against the other as noting that mediocre performance and entrenched management can result in long-term low valuation. Doesn't mean things can't be turned around, but it's not unusual for the market to assign low valuations to those situations. At least the Demarais family seems to have gotten some traction over the past year after making considerable structural changes and investment in new business lines. FFH has made the investment in new business lines, but is the management better? I guess we'll see how that evolves. SJ

-

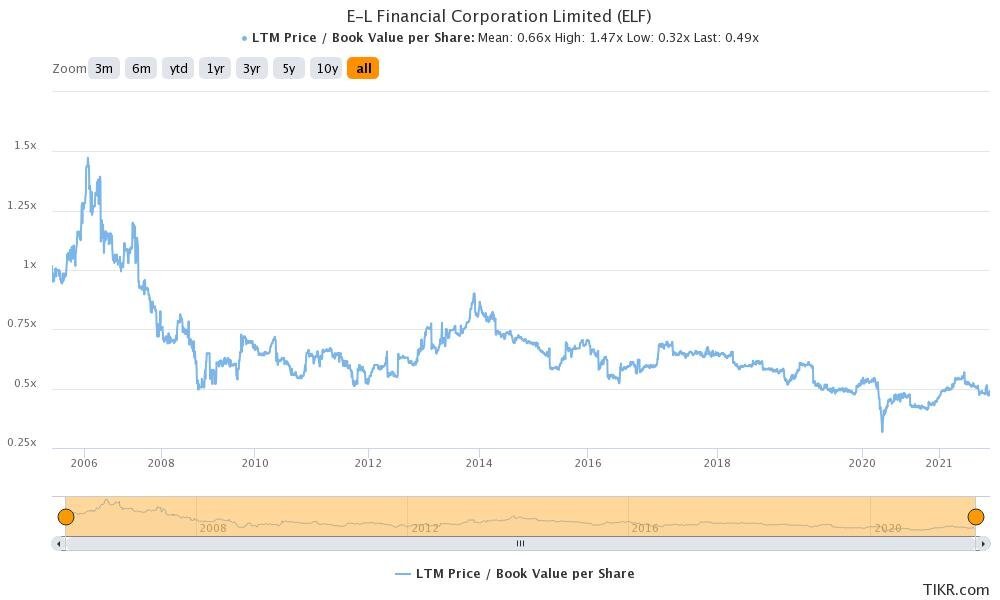

With respect to discount to BV that the Fairfax entities trade at (ie, FFH, FF India and FF Africa), I would note that this is not entirely unusual for family controlled companies. One only needs to look at the Jackman family entities, namely E-L Financial, Economic Investment Trust and United Corp. All of them have chronically traded at a discount to book, despite solid but unspectacular management by the Jackmans:

-

So BV on Dec 31, 2020 was $16.37. FFH's hurdle to earn a performance fee on Dec 31, 2023 is BV growth of 5% per year, not compounded, which would be $18.83 by Dec 31, 2023. And your rough math is that we are already at $21 today? Looks to me like FFH is going to earn a healthy fee and will receive a healthy slug of Fairfax India shares 27 months from now.... SJ

-

If they do charge a mgt fee to Anchorage, it would cascade with the existing mgt fee that Fairfax India currently pays (ie, if Anchorage bought an asset it would trigger a fee, and then that new asset gets consolidated into Fairfax India, which triggers a second fee). SJ

-

I would say that E-L Financial, Economic Investment Trust and United Corp are the poster-children for companies that chronically trade at a discount to book. The Jackman family appears to have been engaged in the slowest process of taking ELF private that I have ever seen. The "weak hands" have not disappeared over the many years. But, does the Jackman family care? They don't appear to have any intention to sell their position, so they just slowly consolidate their position using the discount provided by the market. Maybe some family members are losing sleep over it, but if so, it's not obvious to an outside observer. Maybe Prem is worried about his reputation, but if that's the case, he certainly picks his spots where he worries but ignores a great many other opportunities to protect or bolster his reputation. SJ

-

You've delved right down to the bottom line, I'd say. The prevailing market price really only matters if you intend to sell (a portion) your holding or if you need to use it as collateral. But, if you don't intend to sell or borrow against it any time soon, why do you care if the market price lags (this applies to both Fairfax India and FFH shares)? Pete has provided the best potential explanation for that, which is that a capital raise might be desirable at some point, but short of that, if the shares trade at a discount for a decade, why would a long-term holder (like FFH) care? SJ

-

Who knows what the assets are truly worth. Probably around $20, but there is much uncertainty about what they could actually sell for. In the meantime, FFH's performance fee of 20% of any growth over the hurdle becomes more like 30% of any growth over the hurdle if they are paid in shares that are trading at two-thirds of book. So, we FFH shareholders should pray that this discount will prevail until December 2023. I'm not sure that OMERS would buy shares in either FFH or Fairfax India. It seems to me that the deals involving OMERS and FFH usually take the form of investments in specific assets for which FFH has a buy-out option at a price that always seems to return 9% for OMERS. A cynical fellow would describe that as borrowing money from OMERS at 9%... SJ

-

I always recommend that people reflect on Prem's personal interests. So, in this case, Prem owns a considerable slug of FFH but I don't believe that he personally owns a meaningful position in Fairfax India (but please correct me if my understanding is poor). Prem gets a benefit from the increase in Fairfax India's BV because that ultimately flows to FFH. Through his shares in FFH, Prem also gets a benefit from the annual investment fees and the tri-annual performance fee triggered by growing Fairfax India's BV by more than 5%. When there is a large performance fee, it can be settled by issuing Fairfax India shares to FFH at the prevailing market price. So, from where I sit, Prem (and all of the rest of us FFH-only shareholders) benefits when Fairfax India's accounting BV grows quickly triggering a performance fee and that benefit is even more pronounced when Fairfax India trades at a discount to book. The discount to book matters to Prem because it provides an opportunity for a discounted share buyback which pushes book up and helps trigger the performance fee, and once every three years a discount to book would be the lollapalooza factor when FFH actually receives shares for its performance. Prem's a pretty smart dude. I recommend that people always follow the money. SJ

-

No torrent of abuse is headed your way. Your view is as legitimate as any other. That certainly could be a short-term issue. But, BB's stock price has been high enough on multiple occasions since January that FFH could have exited the position at break-even or perhaps better. My take is that Prem could have resigned from the board in January or February and liquidated FFH's position a few months later if that's what he wanted to do. The fact that it didn't happen suggests to me that he didn't actually want to dump the BB position. Never say never, there's always a possibility that they turn things around and earn enough money to justify the current US$6 billion market cap. FFH's position is worth, what, about US$1.2 billion today? Give them another 18 months and we can tack on another $175m of opportunity cost if they don't turn things around. If they do turn things around, is a market cap of $8b or $9b even plausible? So far, I haven't seen any compelling arithmetic to get me there. But, maybe there's an upside that I am just unable to see. SJ

-

Are they getting better at it? Hard to say. FFH's purchases have always been a mixture of strikeouts and homeruns. As you noted, Atlas and Digit have worked out wonderfully well so far, but other purchases such as the Port of Churchill and Toys R Us not so much. The good news is that the recent flops have been smaller than the homeruns, and FFH seems to have at least done a good job of managing the downside once it realized that those recent acquisitions were flops. The persistence of the Blackberry position is perplexing. As you noted, FFH didn't hesitate to exit the Bank of Ireland position and they've sold plenty of other assets in the past. But, with BB it seems like either Prem has got religion about the company, or maybe John Chen has some photos of Prem in a compromising position... SJ

-

1. Does Prem personally have any dry powder remaining? When he announced his personal purchases last year, I posed the question on this board about where he found the US$150m to do so. Was it loose change that he dug out of his sofa, or did he borrow the money and use the multiple voting shares as collateral. Turning to this year, do you figure he still has more loose change in his sofa, or that he'd be keen to borrow another 9-digits of money? I'm guessing no, but then again, I was a bit surprised that he scraped together the US$150m last year. 2. The TRS surprised me even more than Prem's personal purchase. If the underlying stock price moves in your favour, they are great, but if it moves against you, you need to periodically pony up some cash. In that context, having exposure to 1 million shares is a manageable risk, but I question where Prem and the Jen Allen would place the ceiling. So, if you have exposure to, say 3 million shares through a TRS, and the market goes against you by $50 (like it has done over the past four months), you need to find US$150m of cash for your counterparty. So, what's FFH's ceiling on that kind of cashflow risk? Given the value of the underlying, at what point can they continue to credibly describe it as a buy-back measure, and at what point does it become plainly obvious that it's pure stock price speculation (ie, TRS of a couple million shares is at least a plausible buyback measure because we're only talking about a notional value of US$800m, but once you get to 3 or 4 million shares, it's pretty clear that there's no medium-term prospect of actually making that volume of repurchases). 3. It is almost certain that there will be some volume of open market purchases, but how much? FFH is borrowing money from OMERS at 9% using Brit as collateral sold a portion of Brit to OMERS, to raise cash for the holdco, so is that really indicative of being in a position to make meaningful repurchases? Clearly you can borrow at 9%, buyback shares on the open market at currently prevailing prices, and improve continuing shareholder wealth. But, do you really fund large repurchases by putting your assets in hock selling portions of your assets? I'm guessing that there will only be small-ish repurchases (ie, ~US$100m), but I've been surprised by FFH before. 4. De-leveraging would be nice, but I'll believe it when I see it. When was the last time that we saw FFH's nominal debt level decline in any meaningful way (unless you consider borrowing money from OMERS selling a portion of an asset to OMERS to repay the revolver to be a debt repayment)? My guess is that they use the holdco cash to fund the holdco's operations for a couple of years, and allow organic growth to moderate their relative indebtedness. If they can grow BV by 20% or 30% over the next two years, debt ratios will look a great deal more reasonable (they are already much better than they were 12 months ago). 5. I hope that's what they do. But, option #6, which you have not written, would be another acquisition. Prem has been a serial acquirer for the past 20 or so years. Whenever there's any financial capacity, he seems to find something to buy. My fear is that this past habit will continue to play out. SJ

-

Without wanting to go down the political rabbit hole, the proposed new tax does raise a bit of a timing issue for FFH's typical approach of triggering paper gains to bolster its EPS and ROE numbers. If there are opportunities to trigger paper gains, it might be best to do so in the next three months so they appear on tax filings for 2021 rather than deferring them to 2022 or later (assuming that the new government will be unable to appoint a cabinet and push the new tax legislation through before parliament's Christmas break). SJ

-

The annual dividend alone is once again nearing 2.5%...anybody interested in dividend stocks?! SJ

-

I went to a Montana's restaurant for supper a week ago Monday, and it seemed about normal to me. It looked like they might have pulled one or two tables out of the dining room in an effort to promote social distancing, but of the remaining tables, about 70% were occupied. That's not too bad for a Monday night, which was actually Labour Day Monday. I went to a competing chain restaurant for supper on Wednesday last week and it was a similar story, about 75% full. The business seems to be coming back, but I wonder how many of the anti-vaxxers are also restaurant patrons? There are already vaccine passports required in Quebec, and they will soon be implemented in Ontario. Are the 15% of unvaxxed also heavy restaurant users? SJ

-

If the moons and stars align in such a way that BB is able to get US$3 bil from those patents, the arithmetic for the company's valuation actually becomes plausible (not attractive, but at least plausible). A market cap, net of cash, of US$3.4B doesn't require a crazy income number. It's not inconceivable that BB could eventually earn US$200m, but as they say, I'm from Missouri... SJ

-

Getting a bil for the patents would be great for BB because it would bolster their cash position, which is very important for a company that had negative cash from ops in Q1 and has had virtually no cash from ops over the past couple of years (you still need to burn a little on maintenance capex and some growth capex). But from a valuation standpoint? Well, BB currently has a market cap of US$6.4B. How much distributable cash should they be earning every year to justify that market cap? Perhaps US$400m or US$500m? They are nowhere near that, and it's not at all obvious that they'll get there any time soon. So, okay, now with an additional bil of distributable cash on the balance sheet, their net market cap would be more like US$5.4B. What do they need to earn to justify that adjusted market cap? Maybe $350m or $450m per year, on a sustainable basis? It would still be a dog, just a bit less of a dog. SJ

-

In Canada, a couple of our ambulance-chasing law firms have successfully certified a class of litigants who had their covid related business interruption claims denied. It appears that Northbridge is one of the insurers that has been named. It's a bit of a tradition to list everybody and his dog as a defendant for a lawsuit, so it's unclear whether this actually portends an expansion of legitimate covid indemnities for NB, but the dollars could very easily become material: https://www.theglobeandmail.com/business/article-court-certifies-class-action-lawsuit-against-14-insurers-over-business/

-

Name The Biggest Losing Investments By Fairfax In Their History

StubbleJumper replied to Parsad's topic in Fairfax Financial

Sanj, stop apologizing for these guys. Torstar was not going to be a home run under any circumstance. FFH was piling capital into TS in 2006. We are now in 2021, for Christ's sake, and the S&P has tripled over those 15 years. You can't put lipstick on that pig. It's a similar problem with Abitibi and BB. If all of the moons and stars align, FFH might actually get a return *of* its original capital, but there has been a grossly inadequate return *on* that capital for the past decade. But the bigger problem with your view on this is that you seem as if you are satisfied if FFH is rescued by exceptionally good luck. Seriously, when FFH piled ungodly amounts of capital into BB nearly a decade ago the investment thesis was NOT that the company might eventually make scads of money on security software for cars. Their original thesis was clearly ill-conceived, and if by some miracle FFH is able to recuperate its capital from BB that will be mostly the result of good fortune, not good analysis. Similarly, I would also be particularly disturbed if "commodity bets" were the theses behind Resolute and Stelco. Can you just imagine Prem saying to Brian, "Hey I have an idea. Let's buy a commodity producer because once every 25 years or so, the market goes completely nuts and maybe we will have record prices for a few months and will be able to find a great fool to take the position off our hands." Whatever thesis originally drove the debt issuance to Abitibi was proven ill-conceived a decade ago, irrespective of the possibility that FFH might get lucky enough to at least get its capital back (but again, return *of* capital after a decade is not compelling because we expect a return *on* capital). As for the other fuck-ups, they are much more difficult to track and evaluate because FFH restructures them into oblivion. The purchase of TIG was clearly a fuck-up, but they broke it into pieces and contributed a chunk to the creation of ORH, moved a couple of chunks into other subs, and ran-off a considerable chunk. It would take a forensic accountant months to figure out whether shareholders obtained an acceptable return on that purchase of TIG from 20 years ago. And that strategy of restructuring fuck-ups is still being employed today. Does anyone really believe that Seaspan management desperately wanted to acquire APR? It seems to me that Prem basically handed Bing a steaming bag of shit. It's a similar deal with Helios, and also with Gravalia and Eurobank, where FFH restructured its fuck-ups by dumping the problem on somebody else. Okay, well that's life. Not every investment is going to work out. Not every thesis will be correct. So let's not pretend that these guys bat anywhere close to 1.000. At least in recent years, they've been seemingly trying to move on from the worst of the losers, but the attachment to BB has been baffling and the failure to dump Resolute earlier this year strikes me as a major error of omission. With FFH, you need to accept that there will be home runs and there will be fuck-ups, but let's not pretend that the fuck-ups are anything other than what they are. SJ -

I'm not sure that it's emotional as much as rational. What cashflows is FFH getting from BB and what is the market value of the shares? At what point does BB start kicking down any meaningful cash to its investors (or at least racking up meaningful retained earnings)? Seriously, you looked at their Q1, right? Did you see anything at all in those financials that gave you the impression that things are improving? Personally, I saw what I've been seeing chronically for years, which is unfavourable revenue comps, and once again negative cash from ops. Sell that POS, take the US$1.2B of proceeds and invest it in something that has a more compelling prospect of providing an acceptable return. SJ

-

We've been wishing that for nearly a decade now. To quote from the film Jerry Maguire, "Show me the money!." SJ

-

Yes, it's worth thinking about the holdco cash balances for the next 12 months on a sources and uses basis: Sources of Holdco cash June 30, 2021 to June 30, 2022: Holdco cash as at June 30, 2021: $1,480m Proceeds from Riverstone and Brit: $1,075m Subsidiary dividends: ~$200m (this might be a shade high, but presumably the subs will send up some divvies) Management fees: ~$100m (this is whatever FFH gets from Fairfax Africa, India, and Hamblin Watsa's investment fee) Interest and divvies on holdco cash: ~$50m Total return swaps on FFH shares: ??? (where are the swaps held, at holdco or in the subs? will the TRS be a source or use of cash over the next 12 months?) Uses of Holdco cash June 30, 2021 to June 30, 2022: Revolver repayment: $500m Eurolife buy-in: $143m Holdco interest expense: ~$350m (based on $6.2B of holdco debt) Holdco operating and admin: ~$100m (need to pay for Prem's corporate jet!) Preferred and common divvy payment: ~$300m Netting out the known sources and uses of cash, the estimated Holdco cash as at June 30, 2022 would be about ~$1,500m. Unless FFH intends to float more debt over the next 12 months, it doesn't really provide much capacity for share buybacks if Prem is sincere about his desire of maintaining a cash balance of $1-2B... SJ