TREVNI

-

Posts

102 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by TREVNI

-

But until the cap gains is realized, the deferred tax liability serves as an interest free loan that continues to be invested in the particular security, which otherwise would not be available to invest if the gain is realized. This of course only makes sense if the particular security itself is worth holding for that period of time. Here's my question. Why not just borrow against a stock, and hedge with puts that are priced appropriately in order to avoid realizing gains? Buffett can pull an Ericopoly. True. I guess we need to consider the accrued tax liability separately from future tax liabilities not yet accrued. This reminds me of the question of how to value float. Let's say Berkshire has a liability that we don't expect it will have to pay for 100+ years (hypothetically). Can we approximate the value of this liability as zero? Buy puts and borrow against... that would turn our equity position into a synthetic call option. Maybe we'd want to sell covered calls too, unless we wanted to be long volatility. I'm not sure how taxation would work if we created a synthetic short position by buying puts and selling calls with the same strike against our long positon-- the IRS might have a rule about that. The deferred tax liability grows infinitely large in absolute dollar terms but is asymptotic. Attached is an older analysis (with a higher tax rate) but shows the growth of KO within BRK and the accrued unpaid tax liability over time. What you see is the deferred tax approach the tax rate asymptotically. Float can be considered as equity if it is cost free. (In that scenario it's better than cost free.) The cost of float determines its worth. At one price it's too costly, at another it's on par with borrowing money, at another it's akin to equity.

-

Thank you!

-

I'm looking for something Munger said a few years ago to the effect of: Do you think Warren would have carefully built Berkshire only to ignore the topic of succession. I've looked in the annual meeting transcripts, and searched Google extensively. I'm thinking it might have been a comment at DJCO, but I cannot find anything. Does anyone remember this, or could point me to the origin? Thanks!!!

-

During that period, Meritage was filing its disclosures with OTC Markets. They're available here: https://www.otcmarkets.com/stock/MHGU/disclosure You beat me to it, KJP! I was not aware of the OTC markets resource, thank you.

-

I use the Boston Public Library's online resources, which has access to Mergent. There are a TON of older annual reports, Moody's reports, etc. on there. If you have a city library nearby you can usually get a card even if you're not a resident. Attached are the reports you are looking for. Good luck! Meritage_Hospitality_Group.zip

-

BRK accounting question. Apparent discrepancy on CF statement

TREVNI replied to TREVNI's topic in Berkshire Hathaway

Thank you Cigarbutt! I just learned something new about accounting. When I look at the 1Q2020 report the CF statement is higher by the same $166MM. Really appreciate it, thanks! -

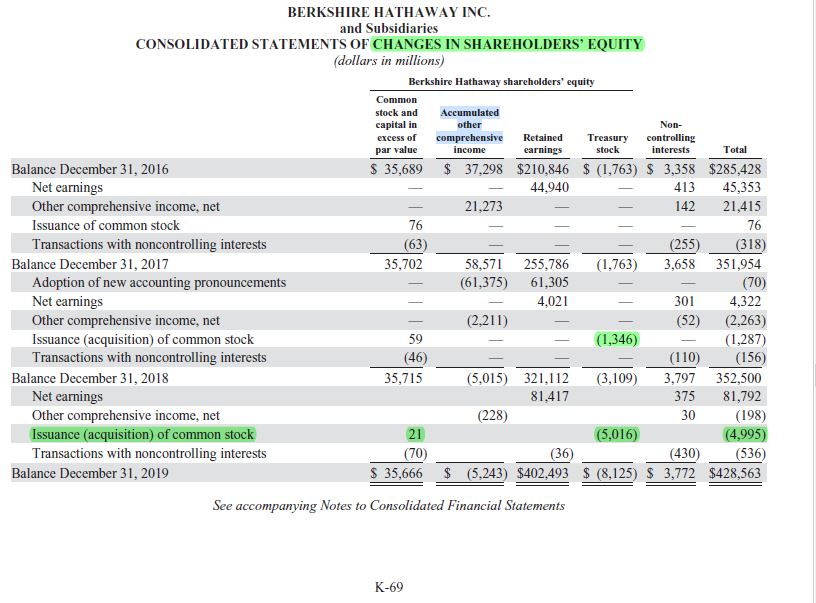

Hoping someone can help reconcile this for me. The acquisition of treasury stock on the CF statement is $4,850 but is listed as $5,016 on the statement of changes in SH equity. I can't seem to reconcile the two. The figure for 2018 reconciles perfectly. Where's the $166 million difference? Thanks!

-

Buffett buybacks: Could Berkshire tender stock?

TREVNI replied to alwaysinvert's topic in Berkshire Hathaway

What, when and for how much they buy are really the only core trade secrets of Berkshire. I highly doubt if they go public with this. Beyond reporting mandated by regulations. Doesn’t make any sense for them. If the idiots want to sell Buffett is not going to try to stop them. I agree with you in general. Buffett has a strong aversion to taking advantage of his shareholders. I just wonder if he'd try to send a message not to be too irrational and sell at these levels. -

Buffett buybacks: Could Berkshire tender stock?

TREVNI replied to alwaysinvert's topic in Berkshire Hathaway

Do you think Warren would issue a press release if Berkshire bought back a large amount of stock intra-quarter? Say 2.5%? As a way to signal to shareholders that they're selling at the wrong time. Or does he wait until the 10Q in May? I REALLY REALLY hope they're not holding back at these levels. -

Yours is a fair question, Munger_Disciple. I'm writing the book that I never found, which was to take a lot of that information and put it in one place chronologically and with some additional depth in terms of financial analysis. I hope to add something to the long-time BRK follower, help the new shareholder "get up to speed" so-to-speak, and provide general business lessons along the way. That's the goal anyway, but as Charlie would say, I'm keeping low expectations!

-

I am writing a financial history of Berkshire and would appreciate any feedback from this esteemed group. Please use the Google Form below. https://forms.gle/AhFdEfgKuUwBLRZi9 While I won't share too much about the book at this point, I can say Warren is aware and supportive of the project. I very much appreciate your help and support!

-

Lemann (3G) and Buffett at Harvard Business School 2017

TREVNI replied to netnet's topic in Berkshire Hathaway

As always there's some nugget of investing wisdom Buffett offers up if you listen closely. He said the capital requirements of See's is taken care of by their gift card float. That must be a $50 million liability at this point! -

Thanks, guys. I do sincerely appreciate the feedback. BTW, I was there in LA when that gentleman asked the question about discount rates. Boy was that painful!

-

I'll just say I'm glad I'll be asking Buffett. You're inferring that the railroads will somehow become obsolete "if/when" solar becomes more common. My question for you is how? How is the grain needed to feed our country going to move from Point A to B because of solar? How are the goods from China going to leave our ports and move throughout the country, because of solar? Trains have a 3:1 efficiency advantage over trucks. Even if they become driver-less and massively more efficient (say, solar / electric powered) they'll still be less efficient than trains. I suspect your answer will be on par with those who thought the internet would kill the old economy. That is, I think you're 100% wrong. BNSF will still be here 100 years from now.

-

LC, bonkers, Picasso, I'd be interested to hear your answer to my question. Would you also be so kind as to point me to words/works by Buffett on the topic? To Picasso's point, everywhere I look Buffett has already answered many of my questions. It's not a question I put together on a whim. How does Buffett look at Sees with its need for seasonal working capital. Is a company that requires a bank line of credit for two months out of the year inherently more risky than another that doesn't but maybe earns a lower ROIC? Should that two months' of capital 2/12ths or 1/6th be counted in the denominator when calculating returns on capital? What other dynamics should one pay attention to? Usually structural changes in requirements for additional PP&E are fairly slow. Working capital can change overnight if a customer can't / won't pay you. I believe there is much more to be learned on the topic, making me, as you say, a better investor.

-

If I'm fortunate enough to get a microphone this year I'm planning on asking the following question. I'd like to hear Warren / Charlie get into the weeds so-to-speak and talk about working capital. I'd be interested in hearing what this forum has to say. What would you give for an answer, and how would you improve the question? Buffett has obviously gone into the subject in the past, I'd just like to pick his brain a bit on some of the nuances of working capital. My question: "My question is about the way one should think about working capital. Is it okay to think of it as simply a component of the total capital that a business requires to operate, with the other component typically Property, Plant and Equipment? How should one think about seasonal fluctuations in working capital as it relates to calculating return on invested capital?"

-

Thanks for the great discussion. There's something else which occurred to me, which is in favor of the "ignore it" group. As many have pointed out, the DTL are largely in a few "permanent" investments. If GEICO were still only partially owned, and the rest traded in the open market, there'd be a huge DTL associated with it. If Berkshire were to ever sell GEICO it'd have a huge gain and so in effect there is a large "off balance sheet" DTL already. If the investments truly are permanent holdings then yes, the monetization is through dividends. What's that I hear, the ghost of John Burr Williams..."A cow for her milk, a chicken for her eggs, and a stock, by heck, for her dividends." P.S. Any feedback (+ or -) on my memos is always appreciated. Thanks!

-

Of course I know I'm splitting hairs here, and that if it's that close you shouldn't base a decision on it. My valuation has large enough a margin of safety that it doesn't matter, I just wanted to do the exercise. Let's say you had a one investment company (Hold Co.) that held only Coca Cola stock. It has a market value of $1,000 on the asset side (the Coke stock) and on the liability side of the balance sheet it was funded by $250 of deferred taxes and $750 of equity. What is it worth? Even if Hold Co. planned to hold onto it forever would you pay the full $1,000? Probably not. Now, if you were a long-time shareholder of Hold Co. and had built up a large deferred tax position of your own the economics would change. Your calculus would be different because in liquidating you'd have to pay the tax. So what I'm really saying is that at the Berkshire level the full per share investment figure is rational. I think it's also rational for a new buyer of Berkshire to discount that figure by the deferred tax liability that would be owned if Berkshire liquidated (which I do not expect to happen). I've spent some time thinking about deferred taxes in the past, and in relation to Berkshire and specifically Berkshire's investment in Coke. You might enjoy them. See here: http://www.meadcm.com/memos

-

I’m fully on board with the “two column” approach to value Berkshire. That is, per share investments plus some multiple of operating earnings. My question is: Should a figure for deferred taxes be deducted from the per share investments column? My reasoning is, if Berkshire only owned investments – nothing else – would an investor pay 100% of the asset value for the investments? Probably not, they would likely deduct deferred taxes in order to arrive at a “correct” valuation. So by this measure we’d need to adjust for the $25,117 million (page 60 of the 2015ar) deferred tax that would be paid if the investment portfolio were turned to cash. This works out to $15,286 per A share, and would reduce the $159,794 figure shown on page 9 to $144,508. Now, it’s relatively minor, but not insignificant, in my view. Thoughts?

-

Does Good Investment Require Good Research?

TREVNI replied to spartansaver's topic in General Discussion

To quote Charlie Munger: "The world is not yet a crazy enough place to reward a whole bunch of undeserving people." I'd say that more effort (hours) does not necessarily translate into more (higher) returns. What is required is better insight, and the way to better insight is better thinking. But of course effort is required, "how could it be otherwise"? -

Thanks for the tip. My error was to click on the "read this article" button, which converted it to horrible OCR text. I've added the remainder of the article to the original post in one PDF. Chicago_Tribune_April_2_1989_Borsheims_and_NFM_article.pdf

-

This is great! Thank you. Do you have the newspaper clipping of page 2 by chance?

-

Why not spend the additional $, and become a member of Farnam Street for $100 for the year. You get a near transcript of the DJCO meeting to complement your audio, plus a boat load of other members-only material (including last year's notes). Amortize the cost over the bonus material and you've paid very little for each item. Full disclosure: I have no affiliation with Farnam Street but I am a recent (and fully satisfied) member. There are complete transcripts out there for free. Is there a value-add to your notes? Not trying to rag on someone looking to make a buck, just curious. I'll just chime in, having purchased these notes 3X before (in addition to one meeting which i attended). I'd say this - it's the best transcript available - and almost like being there. I missed so many things in my own pages & pages of notes in 2013 meeting. All the other notes I've seen are fairly condensed - and very good - but not the same in my book. Too many nuances and fine points to capture. And if my small fee - allows me to not travel and incur much expense - I want the best notes possible. JMHO But there's also audio available (which I would say is a lot more like being there than a transcript), $50 sounds like much when there is free audio.

-

I have a problem that I've been ragging on for a while. My question for him is this: Arlington Value has a large investment in Cimpress, which uses a not-insignificant amount of stock options as compensation. How do you think about employee stock options in terms of determining true owner earnings and valuation? Do you just assume maximum dilution at the plan level and ignore the year-to-year non-cash expense? Take it year-by-year as options are issued? Or something else? Thanks!

-

This is simply poetic justice. I didn't get what I was supposed to do the first couple of times, then I did just as you said and held down to "own" the stock the whole time. Which stock did I get but Berkshire, and I beat all other players haha (bottom left). Crazy to think people trade like that in/out. So much more satisfaction from being an owner.