Phoenix01

-

Posts

280 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by Phoenix01

-

Looks like the CPE index is down to 0.3%. :o The FFH CPI bet is looking better and better. Should be an interesting AGM! http://www.marketwatch.com/story/move-over-oil-strong-dollar-now-choking-off-us-inflation-2015-04-10 Only in March did the Fed kind of throw in the towel, slashing its estimate of PCE inflation in 2015 to a range of 0.6% to 0.8% from an original estimate between 1.6% to 1.9%. The rate of inflation that Fed officials consider healthy for the economy won’t close in on the bank’s 2% target until 2016, its latest forecast shows.

-

As for your concern, about a sell off, I think that there is a very real possibility. I have been disseminating a cap rate spread sheet for the use of small investors for years and it does include such things as maintenance and vacancy. What you find when evaluating real estate in Toronto is that it makes no financial sense at all unless capital appreciation is relied upon to make the investment.

-

Developer Jon Stovell of Reliance Properties specializes in delivering housing to those young people who are eager to purchase real estate, and also willing to live small. He believes that the millennial market has a lot of untapped potential, but he says cities such as Vancouver aren’t keeping up, with their outmoded regulations. They must be outmoded since THIS TIME IS DIFFERENT!

-

Good piece, thanks for posting. 1+

-

WOW!!! It looks like millennials have completely missed the point that cash as a store of value. As long as the cashflow covers the expenses, all is good. There are going to be a lot of people living in their parent's basements for a long time.

-

Hi Al, The Central Banks have created a major global stretching for yield that has affected everything (Sovereign debt, Corporate Bonds, Junk Bonds, Real Estate, Stocks, ...). When the elastic snaps back (don't know when & don't know how) it has the potential to be colossal. Do you have plan for this possible long tail event? What if RE is down 50% and stock are down even more and the Cdn $ is crushed? Will you be OK? Will you be able to take advantage of the amazing bargains that will be offered up? Do you have some sort of insurance policy against this scenario?

-

Fear of missing out is the fuel that drives bubbles.

-

Very good point. One needs to be protected as they move forward. Many are getting complacent and will not be protected. That is what will trigger a correction. The Canadian RE will simply be swallowed up by other global events, no matter what arguments are put forward.

-

I agreed - although I think real estate in Canada is probably not quite the same as the tech bubble where some assets were priced at avg of 165x p/e multiples - and the market participants bought using margin - I believe the high end real estates in Canada are bought with cash... and many 'average' condos were bought with more stringent downpayment and insurance requirements. That's not to say a bubble is not here and won't burst... but I have a hard time seeing that's the same as the tech bubble. Gary During the tech wreck, even the Queen of England was trading stocks. Everyone was doing it, except for a few notables WB, Prem, etc.. We are seeing global inflation of all assets simultaneously. There is a possibility that all assets will reverse simultaneously and very quickly. Long tail events occur when people are not expecting them. BLACK SWAN!! Today everyone is convinced that a 50% drop in Canadian RE is not possible. Is a 50% drop reasonable in light of the global asset inflation over the past 7 years? What if everything drops at the same time? Will global funds pour into Canada for refuge? Who knows??? BLACK SWANS are possible and very few are prepared to deal with such an outcome. Personally it looks like pick up quarters in front of a steam roller. Not worth the risk.

-

There seems to be a general sense that nothing huge can occur in the housing market. This itself is a risk. In a severe global downturn, risk aversion will take over and funds will run from risky assets. The proverbial tide will go out and so many things will get clobbered simultaneously (junk bonds, EM bonds, stocks and currencies). It has taken years to inflate global assets and it will take much less time for all of them to come back down to earth. It is getting harder to sit back and watch everyone else making money in this environment, and that is exactly why those that can resist being drawn into the markets, will be well positioned when the inevitable will eventually occur. Remember how Buffet was ridiculed because he would not board the tech wreck of the 90s?

-

Could anyone post a pdf file of the transcript? Thank you! :) Gio Thanks again for the transcript. Prem mentioned last year that the US bond rally was coming to an end. This could be really good time for FFH to dump them for productive assets.

-

I have also noticed this delayed reaction and also that a relatively small position ($5M) can significantly move the stock price. Perhaps the thin volume, high stock price and poor visibility (not traded on the American exchanges) all contribute to this phenomenon. I wonder if FFH fits into some category that requires the trades to be vetted by an investment committee before the trades can be executed?

-

There is also the experience and synergy that the insurance subs share under the leadership of Andy Bernard. This will have a positive impact on the other subs.

-

That is the FFH strategy!

-

He does not look like he believes what he is saying. However, he also does not know what will happen.

-

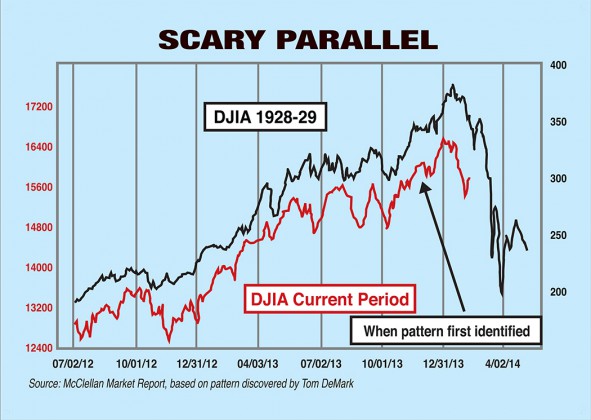

Packer, Technical analysis does not have a fundamental basis that holds up, otherwise the quants would always win. Technical analysis works until is does not work, and then your screwed. The point of posting the graph is to highlight that the trading pattern then and now are similar. It is an observation, not a conclusion. I do not have an opinion, but it is an interesting observation. Will it be a self-fulfilling prophesy? Will it be another Internet joke? Nobody knows. There is no point in either supporting or rejecting the graph. Just enjoy it!!!

-

Here is an interesting graph. If history repeats itself, we will have some really interesting discussions at the FFH AGM.

-

That would have been epic!

-

Packer, ValueLine shows their median stock estimated P/E ratio is 17.8 (it varies between 10.3 & 17.5). The median stock estimated Div Yield is 2.0% (it varies between 4.0% & 2.0%). The median stock estimated 3-5 yrs appreciation potential is 35% (it varies between 40% & 185%). All the needles are pointing to red. It does not mean that anyone knows when it is going to blow up, but I will be keeping my distance. It will take a really sweet deal to draw me back in, and I do not see any.

-

It all comes down to margin of safety. Are you reaching for yield or shooting fish in a barrel? In an overpriced and fragile economy, what sort of returns are you going to demand? Are those returns available today? My perception is that there is a lot of of reaching for yields, so I am stocking up on dry powder and waiting patiently.

-

Exposure to a single commodity and customers that are concentrated in one sector. High debt & capital requirements. In light of a possible economic downturn, I have been buying puts against some of the most vulnerable players.

-

Here is a link to an article by Soros that does a nice job of highlighting the major financial risk that exist today. http://www.project-syndicate.org/commentary/george-soros-maps-the-terrain-of-a-global-economy-that-is-increasingly-shaped-by-china There is a lot of fragility in the world. It will not take much to trigger a crisis.

-

Txlaw -- anything else you can share about what Brian said? Thanks. I can't really recall the specifics. For some reason, I feel like it was quite similar to Kyle Bass' view of the world at that time. My major takeaway was that HWIC had positioned the portfolio in a way that was anticipating some sort of global macroeconomic disaster -- an echo of the financial crisis due to money printing and governments taking on more and more debt. And that because they really believed in this view of the world, they would not be taking the hedges off anytime soon. Since I totally disagree with the hedging strategy, it was a very worthwhile thing to hear from someone other than PW because it solidified my decision to stay away from FFH until they actually take off the hedges. I recall that it was all about the uncharted territory and unintended consequences. FFH spends a lot of time trying to figure it out, and they did not know what would happen next. The risks of something bad happening (especially in Japan with Abenomics) was very real and even probable. I look forward to the AGM to see what has changed.

-

Rogermunibond, Thank you for the link. I will need to re-read it a few times to full understand all the ideas that are discussed. Regards

-

Kyle Bass seems to have done his homework and has a high conviction that Japan is with 2 yrs of a debt default. I know that FFH is also really concerned about Japan (informal discussions during the 2013 FFH AGM). Do you have any other sources that can provide further clarification on the current Japanese situation?