fishwithwings

-

Posts

148 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Posts posted by fishwithwings

-

-

CDS & Co. - Does anyone know if the clearing agency is consolidating ownership for multiple accounts or if it's just an individual that holds his share through CDS?

advent-awi-holdings-incinterim-financial-statementsreport-english11-28-2017.pdf

-

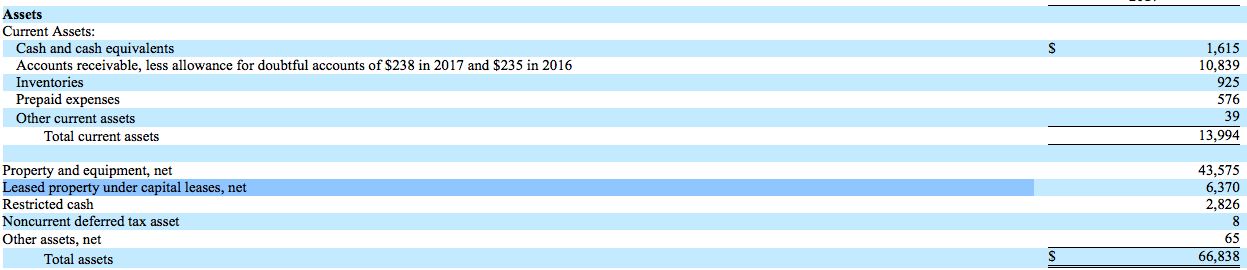

Anyone know which properties the company owns and which ones it leases?

-

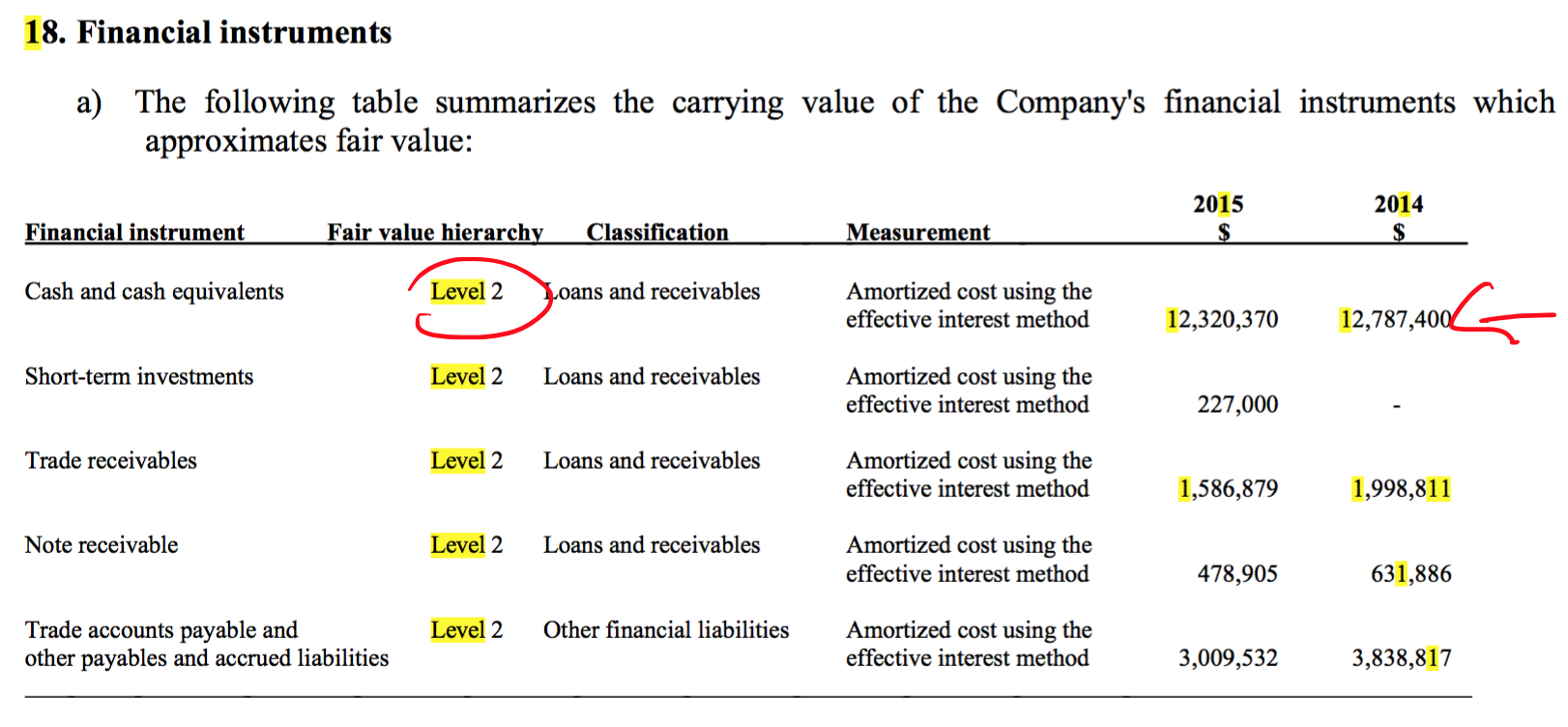

I saw that thread. So I guess it's pretty common? Never knew that time deposits and certificates of deposit included in cash equivalents are included within cash equivalents as a Level 2 measurement. Thought it was always level 1...

-

Is this common, is it something to be concerned about?

Any other thoughts on this?

-

Anyone know where I can find how many shares management owns for a given Canadian company (i.e. Proxy, Annual report, etc)?

Usually beneficial owners are listed in a management information circular on sedar.com.

Great. Thanks

-

Anyone know where I can find how many shares management owns for a given Canadian company (i.e. Proxy, Annual report, etc)?

-

RIA was up ~40% net of fees. 80% in stocks and the remainder was in cash throughout the year.

-

Thanks, Cigarbutt! Lots of good information here....

Thinleyw,

Looked at this (partly identified firm...) in more details.

The "lease" arrangement is relatively unusual.

The initial 10 yr lease was initiated in 2003 and was deemed to be modified shortly after in connection to a significant investment in leasehold improvements by the lessee.

Various disclosures suggest that the lessee effectively has ownership of the "improvements" which are very long term in nature and there were 4 10-yr renewal options that could be applied "unilaterally" by the lessee. At least under US GAAP, this combination of circumstances means that the capitalized asset is being amortized over the useful life of the assets and not over the period leading to the shorter term of the renewal date. Numbers disclosed concerning amortization and the relative absence of change that occurred at the last renewal (2013) would tend to validate this conclusion. I would expect then that, given an unexpected termination of the lease or non-renewal in 2023, the legal title to the "capital leased assets" may go against a simple writing down of the asset to zero.

Interesting case overall in terms of value. The possibility of unlocking of value is highly correlated to a potential catalyst.

If looking for potential validation of the underlying assets realizable value, there are potential digging avenues. For instance, access to appraisal value through insurance protection contracts (property/casualty) or through land/property tax documents. My limited experience has shown that the value discovered in those documents can show higher (sometimes more reliable) values than what is reported on the balance sheet.

Of course, if you are in a scuttlebutt mode, eventually playing the 18 holes may do the job.

Good luck.

-

Very helpful. Thanks, everyone!

-

...Any idea as to what happens to the balance sheet/income statement at the end of the lease when the company returns the property back to the lessor?

The balance sheet gets a "reset" to zero, everything "left" [so far] goes into the income statement. It's IFRS accounting.

So something along the lines of an extraordinary loss for that year?

Thanks again!

-

Each contract is different and if the lessee has to return the "property" to the lessor, you'd have to look at the specific terms of the contract (disclosed?).

I would guess though that both lessee and lessor have a long term mindset and either the term of the lease is very long or renewal is quasi-automatic (for personal or contractual reasons).

Who would significantly invest in leased premises if you have no guarantees about what happens at renewal?

By the looks of it, the company seems to be investing cash into the property in lieu of making substantial rental payments. There is no mention of the lease besides this section. I'm guessing if they decide not to renew, the capital lease would be written off?

-

Not much info but will give it a try.

Given that you have signed a contract for some kind of commercial lease, significant changes after may trigger a re-assessment of the deal terms and reporting.

So, unplanned significant leasehold improvements that occur during the lease contract may require to record the "investment" as an asset to be amortized over the economic life of the of the asset or until the end of the lease.

Let's say you rent a relatively large office under a typical commercial long term loan resulting in an operating lease and, after a while, you make a significant investment to upgrade and have a Starbucks-like café integrated to the office. My understanding is that the lease may "become" a capital lease and the new capital investment that you "own" (leasehold improvements) is capitalized, recorded as an asset and amortized.

Makes sense?

Yes! This is great, IDK, why I didn't, think of this. The reports even state that "the company is obligated to pay $15,000 in annual rent and make leasehold improvements of $150,000 per year. Amounts expended by the company for leasehold improvements during a given year in excess of $150,000 will be carried forward and applied to future leasehold improvement obligations."

Any idea as to what happens to the balance sheet/income statement at the end of the lease when the company returns the property back to the lessor?

-

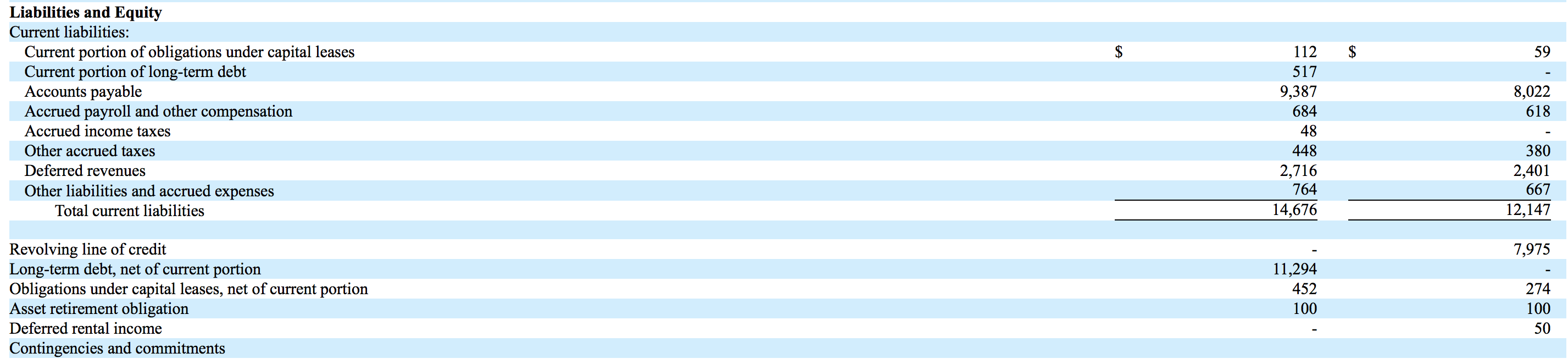

Capital leases, unlike operating leases, are put on the balance sheet. That asset should have an offsetting liability. What company is this?

Not much in the way of an offsetting liability.

-

Anyone know why is the capital lease categorized as an asset?

-

I know this thread is super outdated but has anyone figure out ways to get around opening an account for a out-of-state thrift?

I've spent a lot of time analyzing thrifts and MHCs, I even have a list broken up by state of the non-public thrifts with basic data on assets and loans. I spent a lot of time monitoring three MHCs in the past year and call their CEOs up every few months, so it's an area I feel comfortable talking about.

There are some problems with the strategy though. If you want to invest in a thrift pre-first step, the best bet is to go ahead and do deposits. The issue is that sometimes you can only do a deposit if you actually live in the state. There are ways to get around it (for instance, if your parents lived in MA you could have the deposits in their name)... but it's just a really convoluted process and quite frankly not worth the time IMO. The excess capital isn't really at the insane levels like it was back in Peter Lynch's day.

In the long run, thrifts face significant issues. They tend to put the majority of their assets into mortgages which are bound to take a hit when interest rates begin to rise. Earnings-wise they tend to be pretty poor, they mostly write mortgages and HELOCs, but HELOC lending is facing constraints at the moment (TFSL was told not to increase their HELOC book recently).

So instead, some people try to target MHCs (a thrift that completed the first step in the conversion process) and invest before they do their second step conversion. The problem is, a second step conversion can take years and sometimes might not even happen at all. During that time, MHCs tend to trade sideways.

Some people thought that with the OTS going away, it would serve as a catalyst for second step conversions. But again there is another problem - so far the second step conversion market has been pretty weak. Basically, it's like doing an entirely new IPO and if the market is not receptive to IPOs, you have to lower your offering price. So before, maybe you were seeing second step conversions priced at 100% of TBV, now they might get priced at only 80% TBV. If that happens, you don't get the "pop" in value appreciation that you used to get when a second step was announced.

In addition, most thrift and MHC bankers tend to have a bad reputation -- they are often looked at as being less savvy than commercial bankers and as a result tend to do bad deals when it comes to acquisitions. You have to watch these because when a thrift converts it ends up with a ton of excess capital. They can either use that excess capital to do buybacks, dividends, make more loans, or perform acquisitions. In the past I've seen thrift bankers pay really rich multiples for acquisitions that just weren't worth it.

In the recent issue of Grant's, Joe Stilwell mentions two MHCs he is bullish on - STND and FFCO. He owns 7-8% stakes in each and is a 13D filer (I believe). He has basically told management not to do any deals and to focus on paying dividends and buying back stock with their excess capital. It could work, but it will take a long time and they might run into issues with their assets.

-

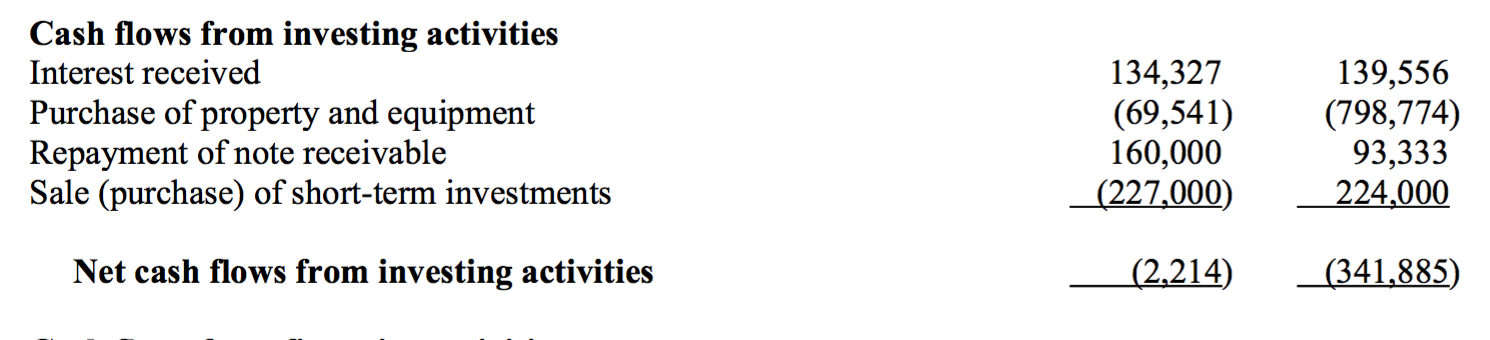

Interest income is not really an operating cashflow. Because the cashflow from operations reconciliation begins with net income, they are backing out the effect of interest income received. They then account for it under the cashflows from investing where it more properly belongs. The intent would be to provide readers with a clearer picture of what the operations are doing wrt cashflow.

This is a difference between US GAAP and IFRS.

http://i728.photobucket.com/albums/ww289/MikeNCathy/IMG_1105_zpsgkvlka3n.png

Great point lessthaniv and this is probably the case.

Great job!

Thanks guys! This is a Canadian company, they prepare their FS in accordance with the IFRS.

-

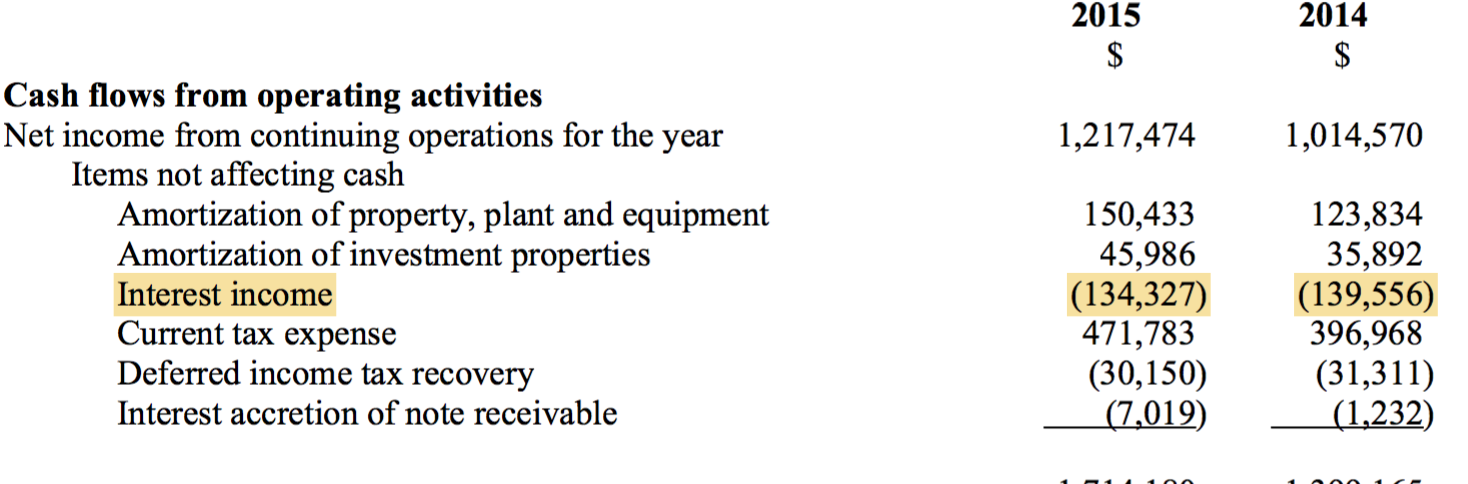

For some reason the company adds back the interest under "Cash flows from investing activities." Is this a unusual?

-

Any idea why Cash is categorized as level 2 and not level 1?

-

Does anyone know why Interest Income is negative (cash used in operating activities)?

-

Thanks for the response. Do you mind taking a look at the example attached... After doing the adjustments you mentioned I still can't figure out how the dividend was figured out.

-

Does anyone know how a REIT calculates their "taxable income?"

What are the reasons for the divergence between GAAP earnings and distributed income (dividends)?

-

Those are probably companies that file with the SEC, but many OTC companies don't do that.

It also works for companies that file their disclosures with OTC Markets, even if they do not file with the SEC.

Nice, didn't know that :)

What about a stock like "KAHL - Kahala Corp."? Couldn't add it on the site...

-

conferencecalltranscripts.org

They don't support companies that are trading OTC.

-

Is there a site that can notify you when a selected OTC company files a document?

{kind=link}

who is Treasureinvesting.blogspot.com ?

in General Discussion

Posted

How did you get permision to view the blog?