MCR

-

Posts

50 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Posts posted by MCR

-

-

21 minutes ago, gfp said:

I am curious if you agreed to use PGR's "snapshot" telematics or did you opt not to?

No, I did not agree to use it. Again, I was pretty shocked by the price differential.

-

Speaking personally, we switched last month from Liberty Mutual to Progressive. We went from $8,700 annual premium for 3 cars (4 drivers) to just under $3,100. I couldn't wrap my brain around how this was possible, but maybe Progressive is looking at this difference as customer acquisition cost...

-

18 hours ago, mjm said:

what state are you in?

I'm in North Carolina

-

As a result of following this conversation, I decided to review my auto (and home) insurance. Just switched providers, saving over $5K for 2023 for auto policy. New 2023 policy for home is effectively same as 2022, but I consider this a gain as I avoid the inevitable increase that's coming from my current provider (increase was just over 26% in 2022).

-

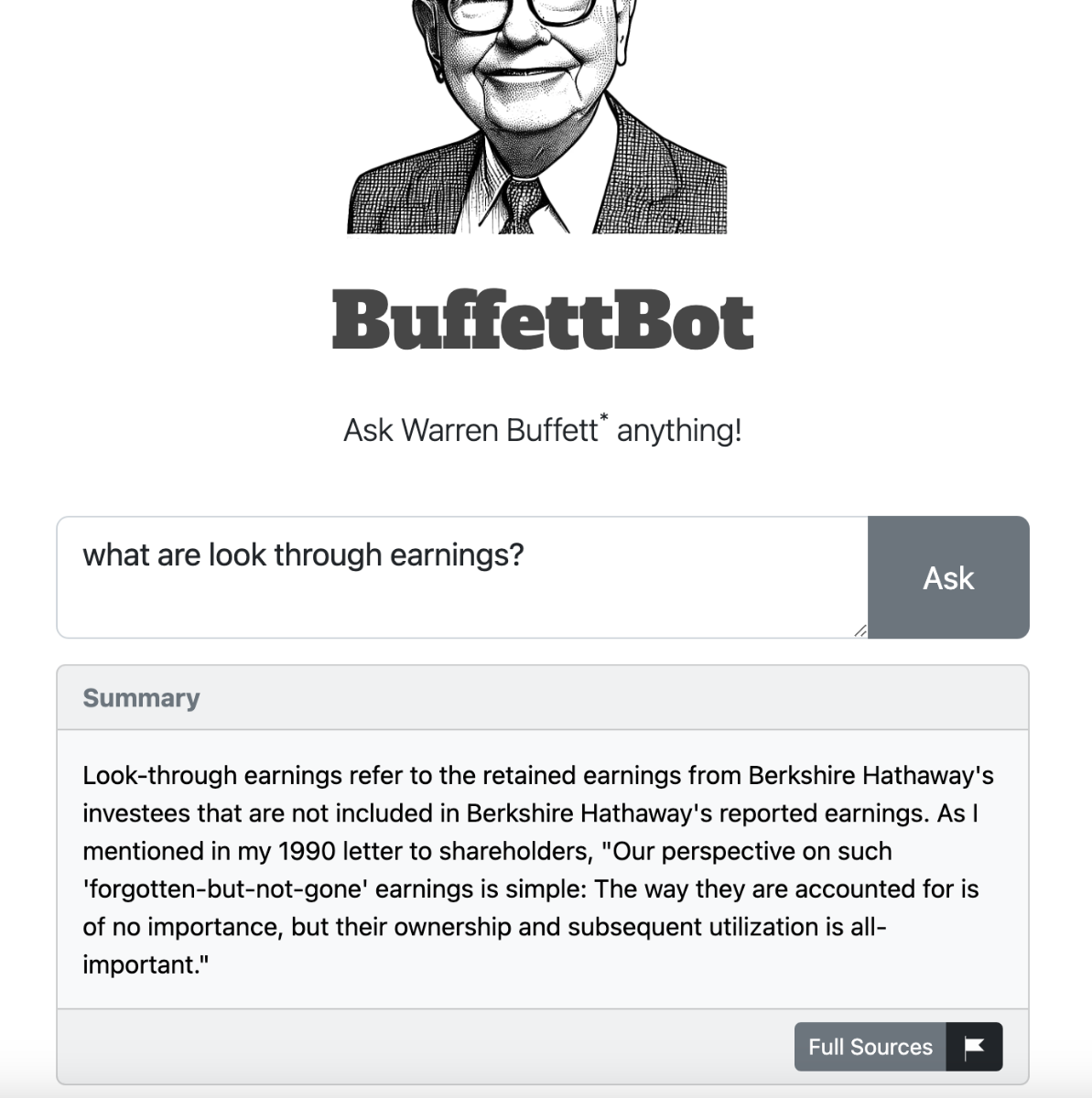

Saw this today on Twitter: https://buffettbot.com/

My first query...not bad.

-

-

15 hours ago, LearningMachine said:

@IceCreamMan, good point.

The benefit of having bigger customer-base is that you can have multiple customer segments within the bigger customer base for new different services in the future. With a smaller customer base, you may not have access to customer segments outside your customer base for different future services.

Also, if you have one of the biggest customer bases, you can afford to spend the most and still have the lowest amortized cost per customer.

Also, customers want an integrated smooth experience with what they already work with, which gives an edge to companies with biggest customer bases already to introduce new services integrated with what they provide already.

For example, lot easier for Apple, Google, Microsoft, and Amazon to win over DropBox. Storage then just becomes a sticky crowbar to get into other services for types of files stored, etc. Similarly, lot easier for one of Microsoft, Google or Apple to win over Zoom, and videoconferencing becomes a crowbar into other services, etc. Another example: lot easier for Google to do street view on Google Maps and build different services integrated with that for different customer segments than it would be for a smaller company working on something else.

I understand this argument with regards to "adjacent possible" markets, but remain puzzled (bordering on skeptical) about long-term moats (competitive advantage) for companies operating in multiple markets/verticals like Amazon (cloud service, grocery store, online retail, movie/TV streaming, music streaming, etc.). This is a lot of competition with companies that can expend energy in fewer verticals because they don't operate in so many (sub-) industries at the same time. Bruce Greenwald and Judd Kahn's 2005 HBR article, "All Strategy Is Local" (and their book, Competition Demystified) has been my touchstone for how to think about this. [I can share full article with anyone interested.]

By contrast (or is it wishful thinking/confirmation bias on my part?), Berkshire appears to be constructed of companies that individually have strong competitive advantages, which in some instances (at least) are amplified by being part of the mother ship. (One example might be the amount of cash BHE can throw at renewables these days in part because it doesn't have to pay a dividend and how the energy tax credits in turn helps the mother ship.)

Greenwald and Kahn's argument is that it's hard to create enduring advantages because they get competed away. But I wonder if discerning between "different services integrated for different customer segments" versus competing in multiple markets/verticals at one time with multiple sets of competitors is clearest in hindsight?

In any case, Greenwald and Kahn's thesis (if correct) make Berkshire's success over so many years just that more outstanding IMO (acknowledging my bias and personal investment in its continued success).

-

Yesterday, while driving on I-85 in South Carolina near Spartanburg I came across a previously unknown (to me) small BRK bolt-on acquisition from 2014--SmileMakers. It was a nondescript building with its logo on the front and the words "A Berkshire Hathaway Company" printed underneath it. (Don't ask me how I read it that fast driving at 75 MPH.) I mentioned the company to my wife over lunch and it turns out she was very familiar with it. They produce gifts that dentists, doctors, etc. give away to kids. My kids have gotten their stuff for years; she told me my daughter got one when her wisdom teeth were pulled earlier this year.

A little digging this morning found a news story from 2014 that the company was purchased by Oriental Trading Company from Staples. Not something we'd likely ever see mentioned in the Chairman's report and too small to move the needle for the parent company, but pretty neat to learn about another way BRK positively impacts people's lives (including my own).

-

-

-

-

Excerpts from interview with Charlie:

-

-

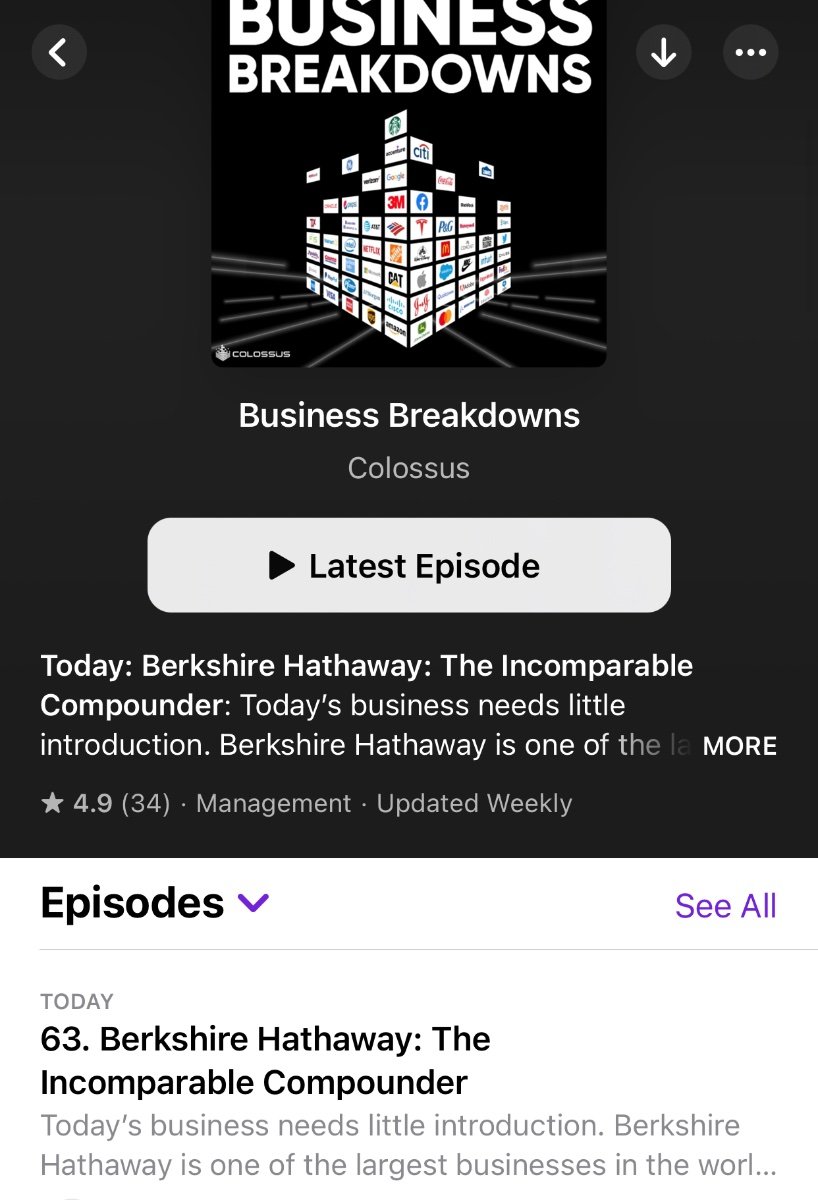

4 hours ago, Xerxes said:

Here's the direct link: https://www.joincolossus.com/episodes/21729827/bloomstran-berkshire-hathaway-the-incomparable-compounder?tab=blocks

-

5 hours ago, ValueMaven said:

@SinbiusNo doubt ... I'm more concerned, or focused if you will on the durable aspect of the ~$40B of operating income annually that the business generates currently ...

I couldn't agree more. After all, BRK at its core is a conglomerate of operating businesses. Very interested in protecting the moat around this group of companies.

Broadening "investor superstars" to "superstar capital allocators", I'm looking for continued smart allocation of the stream of cash coming into BRK, whether it's via purchase of companies in whole (including bolt-ons), purchase of companies in part (shares), buyback of BRK shares, purchase of preferred stock (special situations), loans (under favorable terms), internal capex (e.g. BHE, BNSF, etc.), arbitrage, etc.

-

Interesting thread by Chris Bloomstran analyzing BRK's "underperformance" vs the S&P 500

-

Super interesting infographic from Hendrik Bessembinder's research on wealth creation in the stock market. Berkshire Hathaway is one of the top 20 wealth creators from 1926-2017. (It's also now or previously was a co-owner of several others in the group.) For some reason, the CRSP database used in the study dates BRK to November 1976, which is why it labeled as publicly trading for just over 40 years in the infographic.

https://wpcarey.asu.edu/sites/default/files/2021-10/do-stocks-outperform-treasury-bills.pdf

-

Ever since BRK's acquisition of Duracell in 2016, I've wondered if there is an eventual play regarding electric vehicles (EV). BRK invested in BYD in 2009, which is a long time to develop some insights about the future potential direction of the industry (and market opportunities). However, I can't find much about EV's on Duracell's website (except for this).

I also wonder about the potential impact of the shift to EV cars over the next 20 years on Pilot Flying J's business model. It looks like someone has a brainstorm about what this could look like: https://www.elischwemler.com/design/duracell-electrode

Has anyone heard or read anything about Duracell (or any of the other subsidiaries) as it relates to EV?

-

2 hours ago, scorpioncapital said:

I've read some articles that suggest it is sudden, unexpected inflation that is the problem for insurers. If the inflation is gradual, then the companies can price properly. A fast inflation increase can even bankrupt an insurer. But I do not know how rapid...for example is the current increase very rapid? Also it depends I suppose how long you've fixed your investment assets (duration of bond portfolio) and how much inflation you factored into your underwriting as a potential surprise.

I wonder if this is an example of the potential benefit of BRK as a conglomerate? BRK has the advantage of getting info (close to real-time or with some reasonable lag) on cost increases across an array of businesses/industries, which in theory could be used to inform writing new insurance contracts. The Q3 report never used the word "inflation" but mentioned cost increases many times -- generally attributed to supply chain disruption, the pandemic, increase in cost of raw materials, and increase in personnel costs. A standalone insurance enterprise (e.g. Progressive, State Farm, etc.) presumably would not have this type of first-hand information across an array of industries. The hope is that the extreme decentralization of BRK does not inhibit front running of this type of intel to provide insights to Ajit and the rest of the insurance crew. My guess is that they've got the incentives right for the insurance group to proactively look for this type of information across the BRK subsidiaries...

-

Interesting and entertaining March 2020 article about See's Candies. Don't think I recall hearing before that WEB turned down a $125M offer for See's in 1982. Very wise decision. https://thehustle.co/how-a-small-candy-company-became-warren-buffetts-dream-investment/

-

On 11/23/2021 at 7:42 PM, MMM20 said:

Out ahead of that, no? "Berkshire Hathaway Energy is growing its renewable energy portfolio and continues to de-risk its balance sheet related to carbon-based generation assets. As of December 31, 2020, only 6% of our overall net investment in property, plant and equipment was invested in coal generation assets and 6% was invested in natural gas generation assets" https://www.brkenergy.com/assets/pdf/eei-presentations/2021-eei-presentation.pdf

Thanks, MMM20. Reassuring and not entirely unexpected.

-

Has anyone heard any reference by BHE about risk of potential climate change-related write-downs or stranded assets?

-

On 11/10/2021 at 7:51 PM, Parsad said:

I've always felt that Susan should have been the first Buffett child sitting on the board...ahead of Howard. She's definitely her father's daughter, and has been fully involved with Berkshire, its meetings, engaging its shareholders, etc for quite some time. She has her mother's keen understanding for giving, and her father's instincts on responsibility. Cheers!

In Fall 2011, I took Bob Miles' course "The Genius of Warren Buffett" at the University of Nebraska-Omaha. One of the highlights (apart from a class lunch with WEB) was having Susan Buffett speak to our class about her father. It was clear she was very knowledgeable about BRK, her father's approach, and the culture of the company. Seeing Susan and her father interact during lunch was also a treat.

GEICO Auto renewal Premium Jump

in Berkshire Hathaway

Posted

That's interesting...didn't know about the 96 combined ratio target. We are definitely Wrights...this is interesting background.