klarmanite

-

Posts

107 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by klarmanite

-

Looks like most of the loss incurred in Q2 was related to writedowns on bond holdings due to rising rates as well as unrealized losses in Greece (I'm guessing here on this particular point). Not too worrying IMO. Looking forward to the conference call to get some more color on this.

-

Looks like a maximum 5-7% hit to book values altoghether (if all positions go to zero, more like 7%). I think we can assume Eurobank is toast. The letter to shareholders spells out the exposure in detail, so unless new positions were made this year - let's hope not - stockholders should be fine. Maybe we can hope for an overreaction from Mr Market.

-

What is the blue and what is the green line?

-

I agree Steph. It's one of the main reasons I bought the stock (yesterday). Low correlation to my other holdings Reasonable valuation Fairly low risk of large negative return over a multi-year horizon Great management with skin in the game All things considered an attractive bet. The most reasonable (and common) bearish argument is that it could be dead money for a while. But I'm fine with that.

-

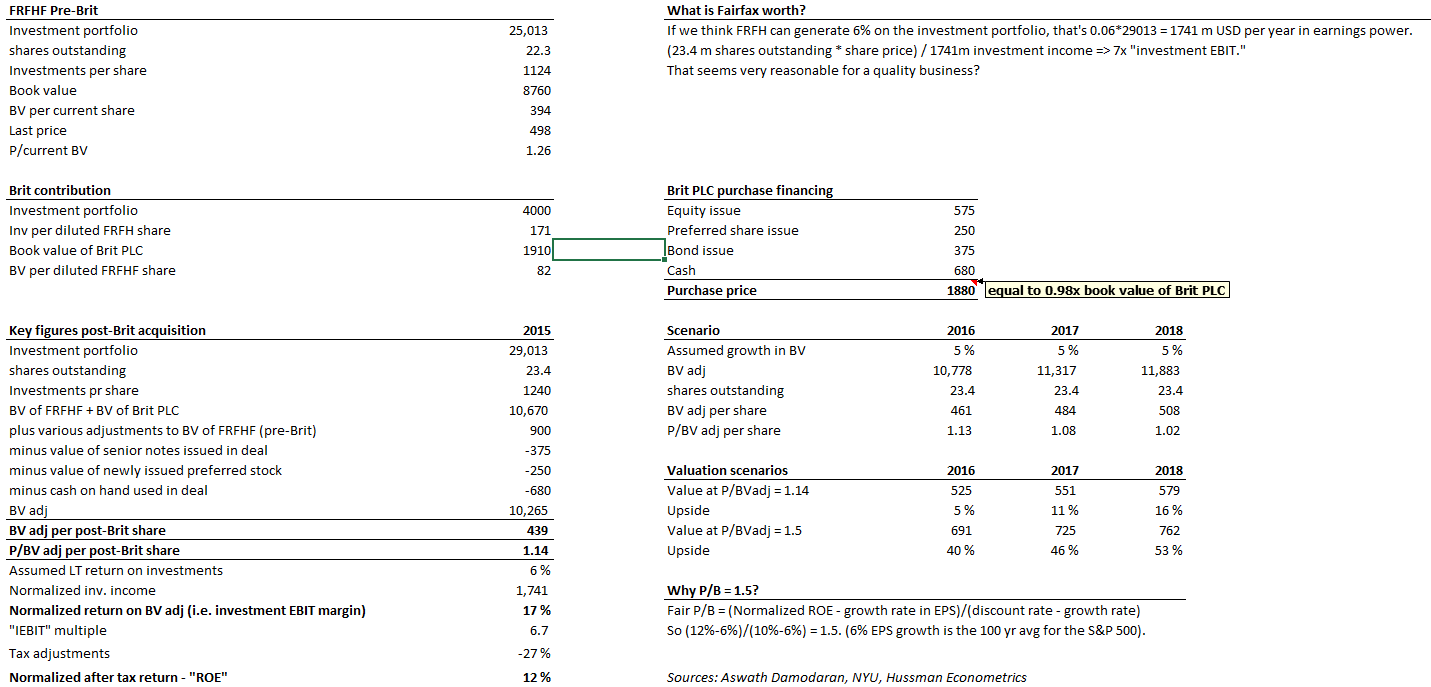

Ok taking a crack at this. Might have some faulty assumptions, so feel free to correct me...numbers are in USD. Whether Fairfax is a good investment depends on how you see the normalized investment returns going forward, in my opinion. I'm making quite a few assumptions here that people may not agree on, e.g. that the cost of float is essentially zero going forward in perpetuity. I also assume that FFH will generate at least 6% over the long term, but over the next few years, wll that's anyone's guess. Hopefully this post can stimulate some discussion, I don't pretend to be an authority on FFH or on insurance companies generally. I will venture to say though that I think these valuation levels are attractive from a long term point of view.

-

Interesting to note that MArkel sold ALL of their shares in Fairfax in the last quarter, as you can see here: http://whalewisdom.com/stock/ffh

-

How will the company look after the Brit transaction?

klarmanite replied to klarmanite's topic in Fairfax Financial

Ah. Thanks Gio. -

How will the company look after the Brit transaction?

klarmanite replied to klarmanite's topic in Fairfax Financial

Thought so. Couldn't make anything sensible out of it. But I don't understand the quote from the letter either. -

How will the company look after the Brit transaction?

klarmanite replied to klarmanite's topic in Fairfax Financial

I don't understand how this can be right. The author writes that investments per share will be 4747 USD after the transaction. How is that possible when Watsa writes in the annual letter to shareholders that Brit's total investment portfolio is 4 Bn USD (p. 6). This is confirmed by looking at the Brit PLC annual report which shows 2.6 Bn pounds in portfolio investments. 4 Bn added to FRFHs investment portfolio would add 171 USD per share of fairfax after 1.15m new shares are issued (total FRFH share count 23.35 m), no? With investments per share at 1124 at Q1 2015, the total investments per diluted share of FRFH should be 1239 USD. On the other hands, Watsa writes on p.7 of the shareholder letter that "Brit's investment portfolio at the end of 2014 constitutes investments of 3510 USD per fairfax share versus 1237 per existing fairfax share currently". Which would take investments per share above the 4000 mark obviously. So which is it? What am I misunderstanding? -

How will the company look after the Brit transaction?

klarmanite posted a topic in Fairfax Financial

Curious to hear from the community on how they see the company after the Brit purchase. Does anyone know to what extent the make-up of the Brit investment portfolio can/is likely to be changed? I'm confused regarding the number of shares outstanding in Fairfax after the acquisition and the net effects on FRFH's book value, investment portfolio and earnings power. Any opinions would be appreciated. -

I think emerging markets asset managers are getting interesting. I prefer the UK based ones over US names for tax reasons (Aberdeen, Ashmore, Schroeders). Working on a write-up on one of them. May post in the ideas section.