vinod1

-

Posts

1,671 -

Joined

-

Last visited

-

Days Won

4

Content Type

Profiles

Forums

Events

Posts posted by vinod1

-

-

Ive been chatting with a lot of folks and most of the time the lens of investment is one of a value investor. I continue to be amazed by the abundance of traditional businesses that are "cheap" but troubled. Look at some of the threads here for example. DD, AMC, XOM, GHC, certain types of real estate...dont get hung up on the specific examples. The contrast between these businesses and the ones RuleNumberOne likes to talk about is incredible. But beyond that, it got me thinking. All the classic value investors and books about such things talk about cycles and buying when things are out of favor and then achieving these heroic returns from being a contrarian. The TBTF trade was really the last classic example of this that worked. But otherwise, everything now, for at least the last half decade if not a bit longer, IMO has just stayed out of favor and continued its decline. Almost as if cycles dont exist and just transitioned to permanent secular declines. Commodity names have sucked forever now. Miners too. Many different types of real estate. Financials, Insurance, media, healthcare, energy, auto....quite a lot here. In a market many describe as in a bubble, and a few percent off all time highs, the list of traditional businesses at shitty valuations and often described by rational investors as having "too much hair" is incredible.

So I guess the million dollar question is, do these ever become cyclical again(IE as in trade at premium valuations), or have we for some reason, maybe Fed induced, caused there to be a hitch in the way investments and businesses are valued? More or less rendering these things permanently challenged and essentially just part of some which ice cube can melt the slowest contest?

I see several things going on that explain what we saw in the markets.

The two really major structural drivers of asset market returns over the past decade are

1. Internet

2. Low interest rates

Internet is to me on the same level as discovery/invention of fire/wheel, steam engines/electricity, etc.

Just as steam engines and electricity has fundamentally altered the economic/business climate, Internet is doing the same. Can you think of any of the CPG companies (Coke, PG, Nestle, etc) without the invention of steam engines/electricity? These companies laid waste to many smaller artisan type small scale businesses. Now Internet is negatively impacting many of the businesses that value investors are fond of.

Similarly low interest rates have elevated asset valuations and had different degrees of impact on different businesses. The impact to value investors in this case is that elevated valuations is leading them to holding on to lot of more cash (it seems like 6.5% real returns for stocks are divine right for investors) or go insane (Berkowitz).

Now you have the normal cyclical fluctuations in different industries. Didn't banking go through the cycle? Many of us benefited from that particular one. Airlines, Housing to name two also went though a cycle.

If you look at Shopping (Retail as well as RE), you can see the long term structural impact of Internet . But there is some cyclical stuff that is going on as well. Same with Energy. Longer term structural impact of many alternative energy and EV is overlaid with cyclical stuff.

So I do not think anything really changed in terms of cyclical fluctuations. There are structural changes that are overlaying with cyclical changes that is hiding the cyclical parts.

Vinod

-

Thanks Liberty!

On a related topic, what do you think of need for sunscreen? It seems to me that humans have evolved to be in the sun, so cannot see why it would be needed. Any thoughts or research you have done on this?

Vinod

I've seen both sides of the argument.. I ended up falling on the side of using sunscreen and getting more Vit D through supplementation.

I think humans throughout evolutionary time mostly didn't live long enough to worry too much about skin cancers and skin aging (the sun will make your skin visibly age much faster), a lot of the problems happened after reproduction age, which is an evolutionary blind spot, and throughout most of that time most humans probably had darker skin pigmentation than I do, which also provides some natural protection. There's also issues with the ozone layer being damaged in post-industrial times (some of that has been partially corrected by banning CFCs and such, but not entirely).

That's my vague understanding of the situation. I still get plenty of sun without sunscreen, but if I know I'm going to be out for a long time in the sun not being covered too much, I always try to wear good sunscreen now.

Excellent points! That makes a lot of sense.

I was recently talking about evolution with a biology professor and she made the point that evolution cared (in terms of increasing your chances of survival) only if it helped in reproduction. That is why women live longer than men, because older women help their daughters care for the children, which in turn led to women having more children. So evolutionary wise there is an advantage for mothers to have their grand mother live longer. Men, apparently no so much :)

Thank you!

Vinod

It's not quite as simple as that, but yes, things that tend to happen after reproduction don't get encoded (or at least, not directly, which also leads to the interesting stuff in epigenetic).. That's why aging and the diseases of aging aren't programmed, but rather, a blind spot that evolution hasn't had a time to solve against because for most of humanity's existence, there were few very old people, and they didn't reproduce. There can be secondary effects, like having longer-lived adults helping the germ-line indirectly (ie. grand-parents increasing the chance of survival of their grand-kids).. I'm no expert, but I remember that at the time (10-12 years ago), I learned a lot from this series of posts:

https://www.lesswrong.com/s/MH2b8NfWv22dBtrs8

Of course reading Darwin's Origins of Species is recommended as a good starting point, but this book is also a good place to learn:

https://www.amazon.com/Adaptation-Natural-Selection-Christopher-Williams/dp/0691026157

Thanks for the links! I did read Origin of the Species 20 years back. Need to read it again as I do not remember a thing.

Vinod

-

Thanks Liberty!

On a related topic, what do you think of need for sunscreen? It seems to me that humans have evolved to be in the sun, so cannot see why it would be needed. Any thoughts or research you have done on this?

Vinod

I've seen both sides of the argument.. I ended up falling on the side of using sunscreen and getting more Vit D through supplementation.

I think humans throughout evolutionary time mostly didn't live long enough to worry too much about skin cancers and skin aging (the sun will make your skin visibly age much faster), a lot of the problems happened after reproduction age, which is an evolutionary blind spot, and throughout most of that time most humans probably had darker skin pigmentation than I do, which also provides some natural protection. There's also issues with the ozone layer being damaged in post-industrial times (some of that has been partially corrected by banning CFCs and such, but not entirely).

That's my vague understanding of the situation. I still get plenty of sun without sunscreen, but if I know I'm going to be out for a long time in the sun not being covered too much, I always try to wear good sunscreen now.

Excellent points! That makes a lot of sense.

I was recently talking about evolution with a biology professor and she made the point that evolution cared (in terms of increasing your chances of survival) only if it helped in reproduction. That is why women live longer than men, because older women help their daughters care for the children, which in turn led to women having more children. So evolutionary wise there is an advantage for mothers to have their grand mother live longer. Men, apparently no so much :)

Thank you!

Vinod

-

For those you with kids in middle/school or going to college, there is an outstanding presentation by a fellow board member (boilermaker75). The best 20 minutes you can spend on improving study skills.

Vinod

-

Matthew Walker recent post responding to some of the questions/criticisms:

https://sleepdiplomat.wordpress.com/2019/12/19/why-we-sleep-responses-to-questions-from-readers/

Liberty,

Thanks for all the bringing all the sleep resources into this thread. Very helpful.

I know you have mentioned something about Vitamin D. Could you please share any resources that you found helpful in this area?

I mostly follow the evolutionary logic that it is best to be in line with whatever humans have evolved over the thousands of years. This goes for both diet and sleep as well and your thinking seems to be similar as well.

What I do not understand with Vitamin D debate is how we might not be getting enough of it. Is it related to not being as much outdoors? Sorry for the diversion, but if you want me to send a PM, I would do so.

Thanks

Vinod

Indeed, we're indoors a lot more, wear more clothes, many of us live at higher latitudes than is ideal, etc. We also produce less of it as we age. Ideally, you'd get a blood test to see your serum levels and then take supplementation to bring your levels to within the optimal range (take gelcaps - not dry tablets - at mealtime, as it is fat-soluble and better absorbed with food).

I don't have the studies and research I did at the time handy, but that should all be fairly easy to find. I take 5,000 UI/day during the summer and 6-8,000 UI/day during the winter (I'm a 6'1" male in Canada, YMMV).

Thanks Liberty!

On a related topic, what do you think of need for sunscreen? It seems to me that humans have evolved to be in the sun, so cannot see why it would be needed. Any thoughts or research you have done on this?

Vinod

-

Thanks! Bought it.

Nice patience, just like a good value investor waiting for your price! I bought it two days ago :(

LOL, thanks. I buy some books at full price too... ???

Got $5 for ebooks if you spend $20 on ebooks deal expiring tomorrow. Not sure if I'm gonna figure out another $15.01 to spend on something. ::)

That $20 promotion is why I went ahead and purchased Why We Sleep. Each semester I give a couple of lectures (This Spring will be my 76th semester teaching!) on "How to Learn." One think I talk about is thet the role of sleeping for learning. So I wanted to read "Why We Sleep" during the Holiday break to see if there is anything I can add to my lectures.

boilermaker75.

Wow! That is impressive.

If possible, could you please share any details for those of us who are not in a position to take your course? Any pointers to blogs or teaching material you can share would be very helpful. If it is an online course please do provide links.

Always interested in the "How to Learn" category both for myself and for my kids. And I am sure many board members would likewise be interested.

Thanks

Vinod

I'm actually working on making these more polished and updating the material. When I do and get them recorded, in a couple of months, they will appear at https://nanohub.org/groups/u

But for now,

Thank you!

-

Matthew Walker recent post responding to some of the questions/criticisms:

https://sleepdiplomat.wordpress.com/2019/12/19/why-we-sleep-responses-to-questions-from-readers/

Liberty,

Thanks for all the bringing all the sleep resources into this thread. Very helpful.

I know you have mentioned something about Vitamin D. Could you please share any resources that you found helpful in this area?

I mostly follow the evolutionary logic that it is best to be in line with whatever humans have evolved over the thousands of years. This goes for both diet and sleep as well and your thinking seems to be similar as well.

What I do not understand with Vitamin D debate is how we might not be getting enough of it. Is it related to not being as much outdoors? Sorry for the diversion, but if you want me to send a PM, I would do so.

Thanks

Vinod

-

Thanks! Bought it.

Nice patience, just like a good value investor waiting for your price! I bought it two days ago :(

LOL, thanks. I buy some books at full price too... ???

Got $5 for ebooks if you spend $20 on ebooks deal expiring tomorrow. Not sure if I'm gonna figure out another $15.01 to spend on something. ::)

That $20 promotion is why I went ahead and purchased Why We Sleep. Each semester I give a couple of lectures (This Spring will be my 76th semester teaching!) on "How to Learn." One think I talk about is thet the role of sleeping for learning. So I wanted to read "Why We Sleep" during the Holiday break to see if there is anything I can add to my lectures.

boilermaker75.

Wow! That is impressive.

If possible, could you please share any details for those of us who are not in a position to take your course? Any pointers to blogs or teaching material you can share would be very helpful. If it is an online course please do provide links.

Always interested in the "How to Learn" category both for myself and for my kids. And I am sure many board members would likewise be interested.

Thanks

Vinod

-

I find it increasingly difficult / impossible to run my portfolio. It is simply too time consuming to research individual stocks given how diversified I like to be. I am looking for options. I am a Canadian investor.

I know i should buy ETFs but I just don't like how popular they are. I feel that mutual funds are my best option. I am hoping someone can provide some good suggestions. Mawer and Beutel Goodman look interesting. Are there any other names people like?

I came the other way around. Moved from indexing (between 2001 to 2005) to active investing (from 2006 onwards). I would suggest reading The Four Pillars of Investing by William Bernstein. Of all the books it has the most intellectually honest case for indexing.

It has the answers you are looking for and it provides a detailed rationale for that approach. The main thing is you need to buy into that approach and it should make sense to you. Otherwise, something might cause you to change the strategy probably at the wrong time.

Even if you do not go with indexing, atleast you would have thought through the issues presented and take a different approach if that is what you want to do.

Vinod

-

I agree with Spekulatius. A compounder is a business that grows its IV at a very attractive rate for a long time into the future.

There are a lot of good ideas mentioned and they are going to compound IV at very high rates. But the issue is always going to be forward returns from the current prices.

I have been selling a bunch of compounders whose returns have now been driven into the low single digit range. Moody's, S&P Global and MSCI, all in this bucket had their stock prices increase a whole lot more than the business values over the last 18 months. Many other compounders have also behaved similarly but atleast the forward returns are still in the acceptable range for now so holding on.

Vinod

-

Liberty - Thanks for the links! Appreciate all the links you post, many of which I would have missed if not for you. My comments below are directed at the authors.

Since at least 2 decades Buffett, et all are talking about MOS and how it comes in different shapes and forms, not just low price. What is See's purchase?

This is a bunch of jargon laden BS. Author tries too hard to sound sophisticated, "ergodic" - come on, it straight from Taleb :) Ants and applicability to finance - Mauboussin mentioned that in 2005 and I was really impressed at that time, now not so much.

Vinod

I'm not saying it's a new idea that he invented from scratch. Of course it's basically a restatement of "management quality matters a lot" and he explains some of the reasons why.

In investing, all the important ideas are basic. We just forget them constantly, so we have to revisit them over and over again and hope for incremental insights and better memory scaffolds so they are easier to recall and apply when needed and such. That's my method anyway, good for you if you can look at something once and never relearn it and apply it perfectly going forward.

The issue I am pointing to is that the message is needlessly complex and jargon laden to convey simple points.

I try to capture all the investment wisdom I come across and document them, precisely because I want to review them periodically. I even have a recurring task on my calendar every quarter to read them. Please see attached screenshot.

So when I tried to read these articles to capture the main points, I found it needlessly complicated and I gave up. Hence my irritation. Perhaps I should not have posted my comments, if I have nothing nice to say.

Again, I really appreciate all the links you post and I do find them very helpful.

Vinod

-

Liberty - Thanks for the links! Appreciate all the links you post, many of which I would have missed if not for you. My comments below are directed at the authors.

Since at least 2 decades Buffett, et all are talking about MOS and how it comes in different shapes and forms, not just low price. What is See's purchase?

This is a bunch of jargon laden BS. Author tries too hard to sound sophisticated, "ergodic" - come on, it straight from Taleb :) Ants and applicability to finance - Mauboussin mentioned that in 2005 and I was really impressed at that time, now not so much.

Vinod

-

Another more wide topic: perhaps "investing" per ce is too wide an area and the deliberate practice should concentrate on smaller area. In some sense you are doing that by saying "I'll practice business result prediction" and get feedback on that. This then excludes a lot of other parts of investing like position sizing, buy/sell decisions, etc. Would be interesting to hear what other smaller parts of investing might be amenable to deliberate practice. 8) For example, something like position sizing seems to be difficult to get factual feedback on. Similar issue with buy/sell decisions.

On many of these things, I just defer to Buffett, Graham and Damodaran (for valuation related). These guys are the best in the business, and have spent a lot of time thinking through these problems and have also written extensively. So no need to reinvent the wheel. Many of these other things you mention like position sizing and buy/sell decisions are not very amenable to deliberate practice I think.

On sell decisions, one thing I did make a change is how long I am going to wait for business under-performance. If business is going according to my expectations, I am not going to bother much with price. If a business does disappoint after several years of steady performance, what I found is that it is going to disappoint for a while. So tend to look very closely and critically at the business and bite the bullet and sell it at a loss. I am not talking about a quarter or two and I am not a momentum investor. But what I want to avoid is the drip, drip of a little underperformance in a quarter and stock is down 10%-15% and one generally thinks the price/IV ratio has improved since your estimate of change in IV is lot lower than the change in stock price.

This might not be strictly deliberate practice but watching the business results of a large number of businesses you get a good feel to make decisions based on gut. Not very scientific.

Vinod

-

I had one question to you. Ericsson also emphasizes the pain part of deliberate practice: "Deliberate practice takes place outside one’s comfort zone and requires a student to constantly try things that are just beyond his or her current abilities.". In other words, if one is not doing something outside their comfort zone, they are not getting better. Do you have any comments on this? Or do you feel that this does not apply to investing and it's enough to find your area/niche and just keep at it inside the niche? Or perhaps you have a different interpretation of constantly stepping outside comfort zone in the area of investing?

The way I think about this, is to try to learn about other businesses, even those that are not in my circle of competence or even interest. For example, I went through the valuation exercise for a few dozen SaaS stocks, even though it was pretty clear to me that these are no where near the range of where I would be willing to buy them. Planning to study blockchain, etc. May not be strictly deliberate practice but idea is to learn other businesses and especially where value is being created in the economy. Since that is where the money ends up being made and it might inform you about a thing or two about the impact they might have on the companies you own.

Vinod

-

Regarding a coach. I wanted to learn from 1. Ben Graham or 2. Buffett or 3) Seth Klarman. Not going to happen. So I did the next best thing that I could think of.

I spent nearly 6 months reading almost exclusively about Ben Graham. Going through security analysis with a fine toothed comb and making notes of each chapter of two versions of the book. If interested my notes are below.

http://vinodp.com/documents/investing/security_analysis_index.html

I want to get into his head and see what he is thinking. So I read the book, took the notes as above. Then took a break and tried to summarize the whole thing at a higher level in a couple of pages. Ended up with 3 pages. After that I felt like I understood his approach.

Going off topic here but the most surprising thing I found is he does not really try to find IV. Rather he is trying to say the business cannot be worth less than $x. This is a tidbit but there much to learn from his approach. Sad that his approach gets boiled down to net-nets, cheapo stocks and formulas.

Similarly with Buffett I summarized his teachings and incorporated his main points into my investing approach. I did not spend focused time like Graham since I have been reading about him for a long time and I just needed a couple of months for this.

As far as valuation is concerned I spend maybe 6 months on Damodaran's book. Did the same by developing a chapter by chapter summary and then a 2 pager of higher level summary. I think I got into his head pretty well.

Even though I spent a long time on Damodaran, I ignore many of his recommendations and think he got somethings not wrong but of little practice use. I ignore for specific reasons but the end result is consistent with his intent. Learned a lot though and it improved the nuts of bolts of my valuation.

I try to summarize a lot of other investors as well but the above three are my shadow mentors who had a big influence on me. There is a lot of writings from these people and I think anyone willing to put in the effort can learn a lot by such study.

There are advantages to learning from a real live person and honestly if someone I had a shot with someone I admire I would have loved to jump on that chance.

Vinod

-

Jurgis,

I would try to answer this in separate posts as time permits.

Regarding frequent factual feedback. This is tough to get in investing as you noted. So a focus on the business results would mitigate some of it but, even then, you do not know if some unexpected tailwind/headwind or some random event impacted the business results. For example, in bank stocks, I (a) overestimated revenues and (b) underestimated how efficiently they could be run and © how much credit costs would be lower than normal. The end result is that my earnings forecast for a number of bank stocks hit target very closely as (a) got balanced out nicely by (b) and ©. So I know that it is a result of two mistakes cancelling each other out. That feedback helped me fine tune my go forward estimates.

Even PE multiples or market prices are important to get right. We know that over the long run the market is generally right. So if a business is consistently being priced at a higher or lower multiple than my expectations means that I could be missing some factor that market is paying attention to and I am not. So that is a good data point as well to know. Lots of issues with this as well since the stock would be greatly impacted by the market multiples, so we need to take that into account as well.

Vinod

-

To give an example from investing, what I am looking at ADS around $200, it reminded me of the mistake I made in IBM. When I looked back at the mistakes I made when I bought IBM, the similarities are striking. Right down to management commentary. So I laid out what I thought is most likely to play out for ADS through 2021. What I expected in 3 years, it played out to a T in 1 year. I am cherry picking something that played out really well, but in other cases it helped me to get out before any damage is done when I realize similarities to other mistakes. Still too early to tell if I am right for the right reasons.

Vinod

-

The concept of "deliberate practice" is something that I have been applying both to investing and for teaching my children - from baseball to math.

I picked up this concept sometime in 2011 after reading "Talent is Overrated". To me the whole idea around deliberate practice made a ton of sense the moment I read about it and it has stuck with me since.

As far as Investing is concerned here are some things I do that I think helped (what else would I think? :) )

1. I do a detailed write-up of every investment idea I research. Some more thoroughly than others. It has either a 3 or 5 or 7 or 10 year expectation of how I would expect the business to evolve. What I think are the key drivers and what I think are the key risks. It also has my expectation of revenues and/or earnings or book value for whatever period.

2. Keeping an investing diary where I record what I researched, why I either bought or did not buy and at what price.

3. Any major ideas that I have about things like say profit margins of US companies, my interest rate expectations, market multiple expectations if I have any, how some industries are going to evolve, etc also go into the diary.

After 3-5 years, I look back at my ideas and see how they performed relative to my expectations (business drivers, not price) and try to figure out why I diverged. Is it some random event that I did not account for or whatever.

I also look at things that I passed up on and the price at which I passed them on and what the current price is.

I also look at big ideas and see how I fared. What I learned about the big ideas is to have low confidence in any of these. To take them with a grain of salt and be fully prepared to be completely wrong. Believe me this has/had been a massive help. This big idea part I have been doing since 2005. I got out of market in 2007 (went to ~35% stocks) due to worries about profit margins and market multiples and realized that was a dumb mistake and did not make that same one again in 2011/12/13...

Vinod

-

I bought it too. To me it is good for a 15%-20% puff and nothing more. Buy at close to 0.9x BV and sell out closer to 1.05x BV.

But I am under no illusion regarding a number of things

1. Its insurance business have gone from terrible to "do not suck" anymore. Does not mean they are good businesses.

2. A P&C company to me always comes with a ton of tail risks. I am not particularly imaginative but I can imagine enough scary scenarios that can impair value. FFH does not have a lot of offsetting exposures to positive tail events on its investment side like it did during 2008-2009 period.

3. Its investment portfolio is particularly exposed to economic tail risks.

4. Many think they have a great bond management team. Perhaps the best in the world. I disagree. No out-performance. Fooled by randomness at its best.

5. FFH investment team did not become dumb. They are smart. To take a fishing analogy (dangerous since I know nothing about fishing). Imagine there are several ponds and some ponds yield a lot of fish. Now imagine if some environmental factor depletes fish in some of the ponds. I think that is what happened to FFH. Replace pond with "value stocks" and environmental factor to "Internet". So investment returns are going to be tough going forward not only because of this but a number of other factors.

6. What happens if interest rates remain low or even turn slightly negative for an extended period of time? What returns would the investment portfolio generate in this case?

I did make an investment very recently. But if it goes up 20%, to me there is no MOS.

Vinod

-

investmd - Ask yourself if you are someone new who has just found Fairfax and started researching the company and you do not have any emotional baggage of knowing Prem and participating in its fantastic record during the great recession, would you make an investment in Fairfax now?

If you think afresh it might give you a better perspective.

I sold in late 2011 or 2012 I think and it was really tough to let go. I pretty much learned value investing as the Fairfax saga was going on and learned a lot reading Fairfax annual reports and benefited a lot from its Great Recession performance. So I was sad to sell and it was also a very large position. But when BAC was around $10 and Fairfax was $420 it was much easier.

Vinod

-

The much maligned Mr. Market got Fairfax valuation right over the past decade better than most.

Vinod

-

Those who are putting the blame on value investing being out of style or on indexing really should read "Factors from Scratch" at the link below:

https://osam.com/Commentary/factors-from-scratch

It would disabuse them of such notions.

Vinod

-

Ben Graham must be turning over in his grave. Do not blame value investing or indexing.

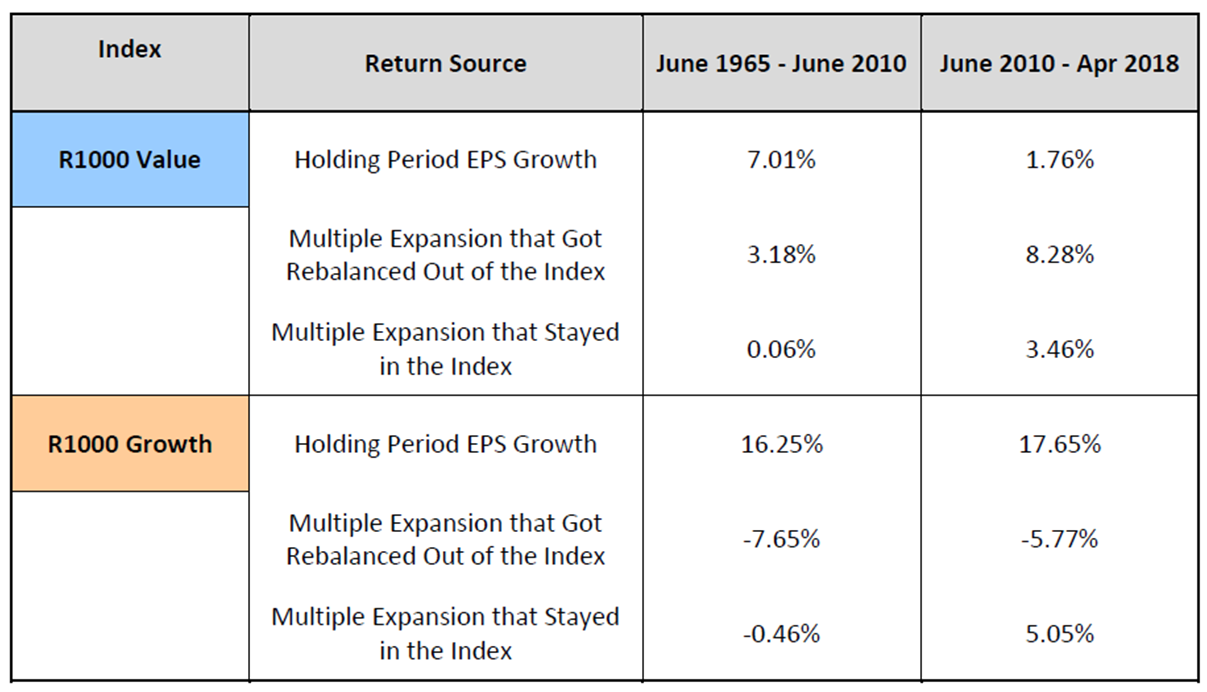

What happened over the past decade is that earnings for companies that fall in the value spectrum have not grown as much as they have historically done. Why that is so is a separate topic of discussion. Where as for the growth stocks they are pretty much in line with history. See attached table from philosophical economics blog. Pay attention to the earnings growth rate of value.

This earnings slowdown for value stocks is what is causing the under-performance. Market is paying attention to fundamentals. That is in line with what Ben Graham has been teaching. Stocks. Long Run. Weighting Machine.

Fairfax portfolio and Fairfax itself performed poorly because the earnings of their portfolio companies and itself were below par. Are we really blaming indexing for Fairfax's portfolios poor returns? Should Blackberry be worth $100 because Fairfax first paid what $45 a share several years back?

Vinod

-

Opened the S-1 after reading all the hoopla about WeWork. The first two sentences are:

"We are a community company committed to maximum global impact. Our mission is to elevate the world’s consciousness."

For some reason, it reminds me of Sardar Biglari.

Vinod

Has The Grand Experiment Killed Cycles?

in General Discussion

Posted

I was reading a book "Factfullness". In this the author pointed out how when we blame some person/establishment we stop thinking.

The blame instinct describes our tendency to find a clear, simple reason for why something bad has happened.

When things go wrong, it’s easy to assume it’s due to bad people with bad intentions.

Rosling writes, “We like to believe that things happen because someone wanted them to, that individuals have power and agency: otherwise, the world feels unpredictable, confusing, and frightening.”

“The blame instinct makes us exaggerate the importance of individuals or of particular groups,” writes Rosling. “This instinct to find a guilty party derails our ability to develop a true, fact-based understanding of the world: it steals our focus as we obsess about someone to blame, then blocks our learning because once we have decided who to [blame] we stop looking for explanations elsewhere. This undermines our ability to solve the problem or prevent it from happening again because we are stuck with over simplistic finger-pointing, which distracts us from the more complex truth and prevents us from focusing our energy in the right places.”

Look for causes, not villains. When something goes wrong don’t look for an individual or a group to blame. Accept that bad things can happen without anyone intending them to. Instead spend your energy on understanding the multiple interacting causes, or system, that created the situation.

Look at how many people blame Fed/ECB or Indexing. You don't have to ask their portfolio performance to know how they did.