giofranchi

-

Posts

5,510 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Posts posted by giofranchi

-

-

This one seems to be working out very nicely. From the Independent http://www.independent.ie/business/irish/fbd-faces-battle-for-control-after-shares-soar-35687594.html

The recovery in the FBD share price means that the €70m bond issued to Fairfax in 2015 is now virtually certain to be converted into a near-20pc shareholding in September 2018, diluting the existing shareholders and triggering a battle for control of the only remaining Irish-owned insurer.and

Following the huge losses recorded in 2015 FBD bolstered its balance sheet by issuing a €70m bond to Canadian investor Prem Watsa's Fairfax Financial. Not only does the bond pay a hefty 7pc coupon or interest rate, it is convertible into FBD shares at any time from September 2018 if the FBD share price rises to €8.50 or above.A move to more of these "paid to wait" type deals is very welcome

cheers

nwoodman

Good find! Thank you for sharing.

Cheers,

Gio

-

Thank you very much for all the different perspectives,

When they were poor underwriters nobody thought they would improve someday and become profitable. Now they look like poor investment managers, and of course nobody seems to believe their investment results might improve in the future. Personally, I think it is easier to give them credit now on the investment side then it was to give them credit back then on the operating side. Because they have already proven they can choose investments wisely in the past.

Though I wouldn’t talk about 15% annualized anymore, nor I have any idea which kind of return should we expect from now on, I believe if they manage putting together both good underwriting and good investments, the business model is quite sound and satisfactory results will follow.

We will see.

Cheers,

Gio

-

Sold ACGL and used the proceeds to buy AMZN.

ACGL was a small position AMZN is a small position.

Cheers,

Gio

-

I was about to go to sleep tonight, but decided to come downstairs and post this on the message board because I'm quite f**king pissed off!

This is the 12th Annual Dinner we are doing in Toronto this year. What started out as a little gathering for me and 9 friends in Joe Badali's Restaurant, with Francis Chou doing a fly-by and then sitting, answering questions for 2 hours, grew into what some are now caling the "Fairfax Lollapalooza!" 12 years later!

Each year, little by little, it has grown...with some 165 attendees in 2015 and 148 attendees in 2016. In total, we had raised $130,000 for Crohns & Colitis Canada in memory of JoAnn Butler, when we started dedicating the event to her in 2010.

But this year, something is different! I don't know what, but the ticket sales have fallen well off pace and there has been much less interest. To the point where we may have to scale down the event next year or eliminate it all together! Yes, you heard that right...maybe eliminate it all together!

First, you should note, I do not and have never received a single penny for the work that goes into putting this together each year. Second, outside of support from Fairfax, Francis, Pat Hios, a handful of donors and volunteers, I do all of the work. Alot of time and alot of effort, and frankly alot of love goes into this! All of the speakers donate their time and effort with no fees...in some instances, I pay to fly them in and put them up.

So you may ask, what the hell is Sanjeev venting about...this is his thing and nobody asked him to do this. And you are absolutely correct! But alot of you have benefitted indirectly from my generosity...be it from the great event we put on each year, or from the fact this board is relatlvely free for the user, and has made a shitload of money for some of you and will make money for many of you newer users!

To those that have bought their tickets already this year, whether you may or may not attend, I thank you for your support! To the one attendee, who couldn't make it out the last three years and sent a lovely check for Crohns & Colitis Canada this week...thank you so much! To Fairfax, who give of their time and money with such humility each year, there is no event without you guys!

But where are the rest of you?

- Where are all those cheap, rich bastards as Wayne Gretzky put it last year at the dinner?

- Where are all of you long-time attendees who have become cynical and fickle over the last year(s)?

- Where are all my rich hedge fund friends managing anywhere from tens of millions to billions of dollars!

I don't need your quarterly or annual newsletter. I don't need the annual book you send me. I don't need a pat on the back. I don't want you praising me when you see me at some event. I don't want you calling me to ask me how I can get you in touch with Fairfax because you have some great investment idea or business you want to sell. I need your support for this dinner!

I hope many of you are still coming! I hope some of you get pulled out of the darkness by this post and decide, hey I'll send a check in or buy a ticket, or sponsor a silent auction item...or maybe just give back in some little way! I know you guys haven't disappeared, and I know you will see this.

You can buy your ticket at www.cornerofberkshireandfairfax.ca . Scroll down a little bit and the ticket button is on the left hand side of the homepage.

You can send a check made out to "Crohns & Colitis Canada" and CCC will send you a tax receipt. Mail to:

Premier Diversified Holdings

Attention: Sanjeev Parsad

#301 - 3185 Willingdon Green

Burnaby, BC V5G4P3

You can contact me directly if you want to make a corporate donation or donate a sponsorship item:

sparsad@pdh-inc.com

604-679-9115 ext 205

Otherwise this may be it! Maybe we've run our course and call it a day! But that would be a God-awful shame. There is no other event like this in Canada, and outside of Berkshire's AGM, anything similar elsewhere costs people an arm and a leg!

So whereever you may be, please take note of my pissed off post. Think about how you benefited when Fairfax was warning about collateralized debt, or the massive thread on Bank of America that many of you got rich out of, or when you discussed how Fiat was so damn cheap! Actions speak louder than words...so I'm asking you to act!

Cheers!

Sanjeev,

believe me that I have enjoyed very much the couple of dinners I had the chance to attend!

It simply is not easy for me to come every year from Milan... If it were easier and less time consuming, I would surely attend every single year.

If it is of any help, I can buy the ticket even if I won't be able to be with you this year.

Please, let me know.

Cheers,

Gio

-

-

My only problem is that now my downside protection is gone ;)

My downside protection is the meaningful fcf the businesses I privately own and manage generate at the end of each month.

And I don't know of any other kind of downside protection that really works.

Cheers,

Gio

-

I'm new here but I'll pitch in.

giofranchi, before committing myself to this forum, I went back many threads/posts.

I appreciated your contribution.

Perhaps similar to you, English is not my first language and, during my "productive" life, I invested internally generated funds from my incorporated business. I'm pretty much retired now.

For reasons that don't belong to this specific thread, I have essentially no long positions now. But I keep looking.

Concerning LKQ, I analyzed this some time ago. I will get my file out, update it and plan to provide constructive comments within 1-3 days.

Thank you!

Cheers,

Gio

-

2) LKQ - My thoughts on the company are here:

http://www.cornerofberkshireandfairfax.ca/forum/investment-ideas/lkq-lkq-corp/msg266841/#msg266841

Thank you, Ross! I will look into it carefully.

3) I actually have a personal large position in Berkshire! The reported portfolio is from our more actively managed IB account. There is a large slug of BRK.B stock sitting with a pile of index funds in a Vanguard account. With that said, I am not very excited about Berkshire's investment into Apple.

Ok. I like Apple, therefore I am not really worried about this new and very large investment. Of course I understand anyone has his/her own view about Apple!

4) The long and short of TJX's success is because they can offer something the internet cannot - a treasure hunt. My wife goes to TJ Maxx to find xyz and comes out with a nice sweatshirt and new shoes. I look at internet retail's impact on brick and mortar like this: brick and mortar stores that sell items people specifically seek out are easily replaced by internet retail. For example, if I want to buy a Vitamix blender, Ralph Lauren Polo Shirt, Samsung TV, or Ping driver I could drive to Bed Bath and Beyond, Macy's, Best Buy and Dicks Sporting Goods respectively or I could type it into a browser and purchase online. With retail models like TJX, IKEA, and Costco, you do not have this problem.

Mmm... I am still skeptical... If consumers want a treasure hunt, why cannot Amazon and/or Alibaba give them such an experience?

Let's put it this way:

1) If TJX, IKEA, and Costco could go on giving their customers something they cannot find at Amazon and/or Alibaba, TJX, IKEA, and Costco will be fine. Also Amazon and Alibaba will be fine and will keep growing.

2) If TJX, IKEA, and Costco could NOT go on giving their customers something they cannot find at Amazon and/or Alibaba, TJX, IKEA, and Costco will start to shrink. Instead Amazon and Alibaba will be fine and will keep growing.

Of course TJX's track record till now seems to prove that 1) is more likely than 2). But will it continue to be so in the future? I don't know the answer, and that's why I prefer to hold those cos which will be fine in both cases.

Cheers,

Gio

-

10.7% Cash

7.9% - AXP

7.8% - DIS

7% - LKQ

6% - FRFHF

5.5% - NOV

5.4% - TJX

4.8% - LBRDA

4.7% - LCSHF

4.5% - CHKDG

4.1% - WFC

4% - SBUX

3% - BDVSY

3% - BF.B

3% - IAU

2.8% - WLTW

2.8% - BAM

2.5% - LSXMA

2.2% - V

2.2% - GILD

2.1% - BRK.B

2.% - FWONA

1% - ATUSF

1% - TRIP

1% - KMI

Thank you Ross,

I would like to know your mind on four topics:

1) What do you see in AXP that prompted you to make it the largest holding in your portfolio?

2) I don't know LKQ: another large position of yours. Why?

3) BRK is a small position. What concerns you at this point?

4) Finally, TJX is a wonderful compounder: why do you think they have been so successful in a very tough environment for retailers?

Cheers,

Gio

-

Included in realized losses in 2016 was a loss of $2,663.9 million realized in the fourth quarter when the company, recognizing fundamental changes in the U.S. which obviated the need for defensive equity hedges, discontinued its economic equity hedging strategy, closing all of its short positions in the Russell 2000, S&P 500 and S&P/TSX 60 equity indexes effected through total return swaps.

Donald Trump wins, Tails risks, 1 in 100 year storms, all vanish!!

Debt deleveraging?

All done.

"worried about the speculation in financial markets and the potential for a 50-100 year financial storm"?

No more.

"However, we have warned you many times in our Annual Reports of the many risks that we see and the great

disconnect between the markets and the economic fundamentals."

No more.

"Most investors consider the

2008/2009 recession and crash to be a once in a generation event – and it’s over! We differ because we think we

escaped the serious adverse consequences of that recession as a result of huge fiscal stimulus from the U.S., even

greater fiscal stimulus from China and the reduction in interest rates to 0% with massive monetary stimulus in the

U.S., Europe and Japan through QE programs. There is nothing to fall back on now if the U.S. and Europe slip back

into recession."

Now we have Trump!

"The potential for unintended consequences, and therefore of pain, is huge."

There can be no pain with Trump as president.

Vinod

Thank you for this. Just makes it all the more ridiculous.

I was relatively understanding of the partial move post-election to reduce duration and hedges. I did the exact same thing until we got more clarity on tax reform which had the potential to be a BIG change in my thesis. As time has passed, it appears tax reform won't happen quickly and won't be anywhere near as big as most Republicans would like, so I've added mine back.

Fairfax, on the other hand, went ahead and sold all of their bonds and killed their hedging program in the middle of a tightening cycle with valuations at their 3rd most expensive ever while corporate profits are significantly off their 2014 highs...all because of a change in president?

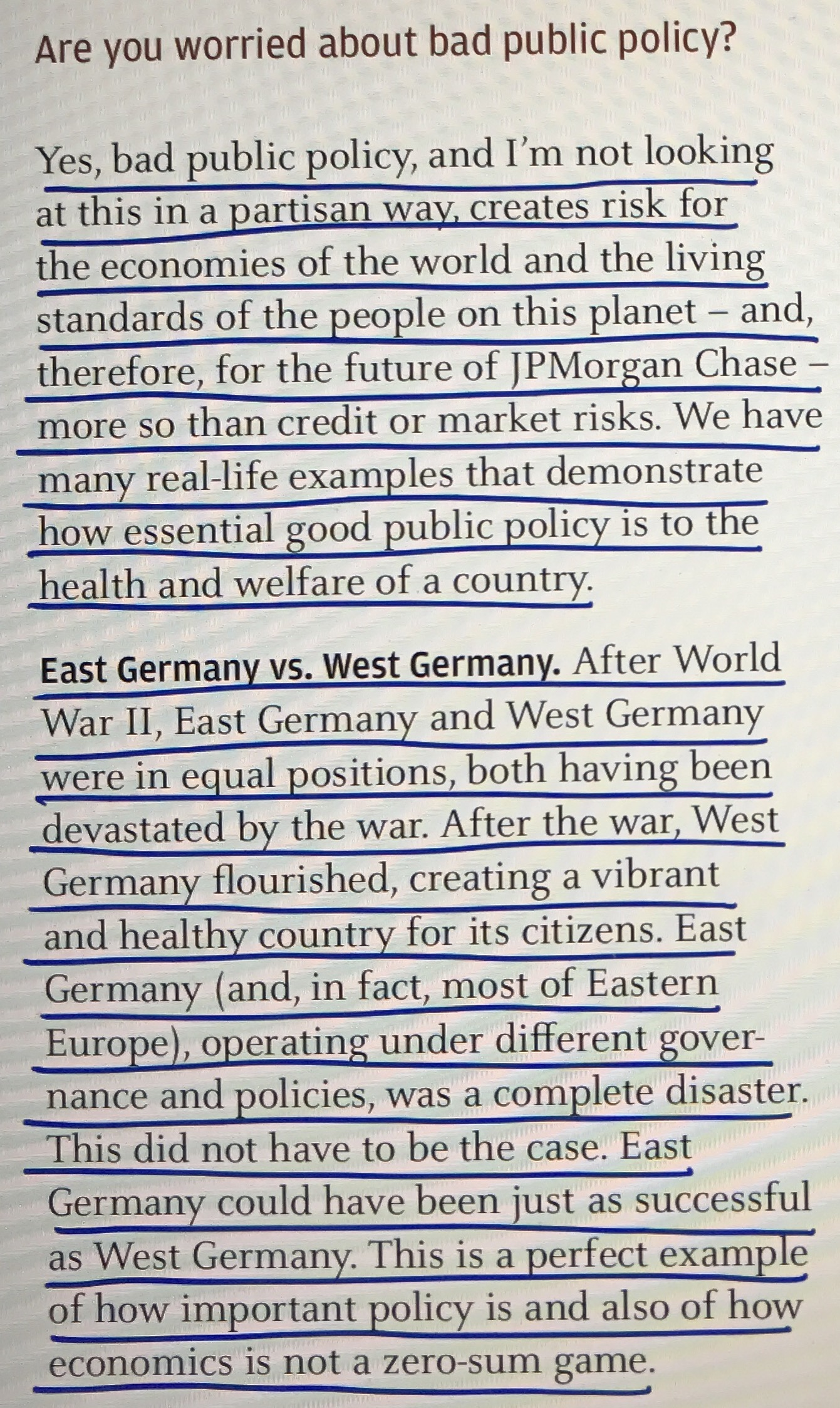

How important is public policy? (JPM 2015 AL)

Cheers,

Gio

-

Here are the facts:

- Weather forecasts. They tried to predict rain. The sun shined a lot. How about building a ship that will do fairly well at both and bad times instead of predicting weather like that? Instead of trying to be wrong...wrong..wrong....right, what about ...ok if wrong or right...ok if wrong or right...ok if wrong or right...just like Berkshire and Markel?

- Cigar butts equities. Did very well when they had small to mid size money to invest. Did mediocre with a big portfolio.

+1!

Cheers,

Gio

-

What really intrigues me is whether they will learn from their investing mistakes (as they clearly learned from their insurance acquisition mistakes).

Yeah! That's basically the reason why I am still holding it.

We'll see!

Cheers,

Gio

-

Their hedges were a big mistake, but if they had outperformed the markets with their stock selection there wouldn't be any problem. The real problem is their disastrous stock selection of the last years.

Agreed 100%!

Last year again they lost money with their equity investments. It’s hard to believe…

I still like the business model of course, and I still like management (they have done a great job on the operating side of the business in recent years).

But insurance without good investment capabilities is clearly unsatisfactory: they should prove they can be good stock pickers again.

Cheers,

Gio

-

After about a month off of sugar my blood pressure was down 20 poihts.

By "off of sugar" which percentage of carbohydrates in your diet are you referring to?

Those days in which I stay below 40% are the ones when I eat no bread, no pasta, and no desserts...

Cheers,

Gio

-

Things were not doing well for me not that long ago. It seemed that I could do no right in my personal and investment life. And it turned...

Very glad to hear that! And I agree 100%.

Cheers,

Gio

-

I have opened a position in The Travelers Companies (TRV):

Average annual operating return on equity over the last 10 years: 13.8%

CARG in BVPS over the last 10 years: 9.7%

BVPS in 2008: +5%

CAGR in dividends over the last 10 years: 10.1%

Total return to shareholders for the last 10 years: 250%

Dividend Yield: 2.2%

Payout Ratio: 25%

Debt/Equity: 0.26

Price/BVPS: 1.4

P/E: 12

This is imo an outstanding company selling at an attractive price.

The change in management that occured last year might constitute a source of uncertainty. Anyway, Mr. Schnitzer already was CEO of Business and International Insurance, and seems to know the company very well and to be perfectly alligned with its culture.

Cheers,

Gio

-

I did not see this book discussed because it was buried several pages deep...

Just finished reading this book. Agree with other posters that it is well researched, somewhat to overly positive etc.

Overall, it is well worth a read; I would in fact highly recommend it to folks who have a large proportion of their networth in BRK. (I do). The continuity of culture is paramount to my continuing ownership; Cunningham addresses this fairly well from different angles but for me, the pivotal signal that the future will be similar to the past will come when the insider cohort owns over 30% of BRK as Buffett did before his planned giving started. The anecdotes provided by Cunningham suggests something like a 10% ownership by the insider cohort as of 2014. I would like to hear an update on this. Also, if the company is successful buying, say, $50 to $100 B of stock over the next decade, that will be tantamount to increased insider ownership.

And, of course, there is no replacement for Buffett. This became clearer to me after this book. Believing otherwise is like believing in tooth fairy tales.

I listened to the book on Audible. Twice already. It has made my driving time very interesting!

I agree with all you have said.

And I have twitted many parts of this book because, besides the continuity of culture and the fact there is no replacement for Buffett, I have found it interesting and useful to know lots of businesses BRK has acquired through the years better.

Cheers,

Gio

-

found the answer

fairfax bought 35% stake in ICici Lombard over years for 347 million. now they are selling 25% of the stake for 1 billion$

not bad

+1

They have been harshly criticized for their investments in equities recently: well, it seems that at least some of them are turning out to be quite profitable!

Cheers,

Gio

-

+1

Cheers,

Gio

-

We know who would run Fairfax and that's the perfect choice in my opinion.

Could you educate me? I missed this. Thanks!

Well Prem runs Fairfax and will until he no longer can...be it physically or spiritually. But it looks pretty obvious who would run Fairfax if Prem could no longer do so. If you don't really know, time to do some legwork and figure it out. :)

Incidentally, no one has ever said anything to me. But after watching it for all these years, I kind of have a pretty good idea of changes at Fairfax that may not seem like much, but are monumental shifts in planning or thinking. Cheers!

Ha - OK! I also have a fair idea, although I am nowhere near as well informed as you. However I read your comment to mean that an announcement had been made, hence the question.

Pete,

It really is obvious!

Sanjeev is going to merge FFH with PDH and he is the one who will be running the show!!

Cheers,

Gio

-

It is exactly what I asked Picasso for... And of course I don't think it would be a bad idea!

I try to stick to "great businesses, with great management, at fair prices" because the time I devote to investing in the stock market is limited: I run a business which provides useful services and products and which has given me great satisfaction (until now at least!). And the endeavor to make it grow consumes the majority of my working time.

But I recognize the fact that other investing strategies (micro-caps, restructurings and special situations) might uncover much more value and therefore yield much better results. Like the FELP thread has demonstrated or like the results posted by writser and Hielko demonstrate.

I wouldn't mind investing with a manager who has a good track record in finding special situations that have been rewarding, who takes the time to explain in great detail what he is doing (like Picasso has done with FELP), and whose fees are reasonable.

Cheers,

Gio

-

Seems like a lot of the members with 30+% returns in 2016 had a lot of exposure to commodities in 2016. Just wondering if you guys can provide more details on how you were positioned going into 2016? Did you have the existing commodities position already? Were you able to pick the bottom or come close to picking the bottom? One of the member had mentioned that he was down 40-50% in 2015 and the near 100% was just getting him back into being even. If you can share if the 30+% was just getting you back to even or if it truly built upon your flat or positive returns in 2015, it would be very helpful.

I know that FELP was a great trade for a lot of people on the board.

I am reading the FELP thread.

The timing was almost perfect and therefore some good luck might have been involved. Nonetheless, I am really impressed by the amount of very carefully executed work Picasso has put into this idea! Really amazing!

I know I would never be able to dig so deeply and masterfully into any stock market idea.

Picasso, next time you start a thread and notice I am not following, please send me a wake up call through DM!!

Cheers,

Gio

-

Another member of the FELP mafia, nice!

Picasso,

Is there a thread about FELP?

If so, I would like to read it and understand your reasonings about the company.

If not, where could I find more information?

Thank you!

Gio

-

The equity of my company has increased 16% this year. 12% from operating results + 4% from investments. I have also paid out a 1.5% dividend. Since 2010 the BV of my company has increased at a CAGR of 17.3% (dividends excluded).

2017 operating results should be solid: in 2016 we have signed a contract for monitoring the structures of hundreds of residential buildings in Northern Italy and the seismic retrofitting of a few. Last year we have signed a contract with Salini-Impregilo for some seismic analysis of the structures of the new metro in Lima (Peru), a relationship that has worked well this year and will go on in 2017. In 2016 we have also signed contracts with Autodesk and Oracle University to provide specializing courses that are very much sought after by engineers and architects: they should add meaningfully to both our top and bottom line in 2017. On a sour note a good contract with Italcementi will come to its end next year... Overall, though, I expect operating results to be quite satisfactory in 2017.

I invest the free cash of my company in the stock market (funds that I still have at my disposal after all the investments for growth in my company have been made): results in between 5% and 10% will be more than enough to achieve my goal of compounding BV at 15% annual for many years to come. Last year and this year have been disappointing.

Cheers,

Gio

FFH share price

in Fairfax Financial

Posted

If you believe FFH could increase equity from now on like MKL might do, or that FFH could increase both BVPS and dividends like TRV might do, FFH is clearly undervalued today.

On the other hand, if you believe FFH will go on performing like a mediocre insurance company, FFH might still be overvalued.

I am not adding more shares right now: it is not a judgement about their future prospects, but it is simply because I like a diversified portfolio and don't want to let any position become too large.

Cheers,

Gio