giofranchi

-

Posts

5,510 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by giofranchi

-

Dan, your great experience would be a tremendous gift to us all! I am really looking forward to sharing ideas with you, and to studying your recommendations! As you might read in the Pershing Square 2012 Q1 Letter (see attachment), later this year Bill Ackman is planning to launch the private phase of Pershing Square, which will be listed on the London Stock Exchange. Watch out! giofranchi Pershing-Square-Q1-2012-investor-letter.pdf

-

Liberty, I am here to listen to people who DO NOT AGREE with me! People who agree with my viewpoint are flattering, but much less useful! So, I will always try to explain and delve deep into what I think, but I will always ask for someone to prove me wrong too. That’s what I really seek! And should I be rude with someone who gives me what I look for?! To be clear, when I say I am long North America, I basically mean that I am long the USD. And these are the reasons: 1) If you haven’t already read it, I highly recommend “The Debt-Deflation Theory of Great Depression” by Irving Fisher (find it in attachment): he basically says that there are all kinds of economic troubles and uncertainties, and then there is debt. Once we have let the system get too much levered, trouble inevitably follows. Therefore, all the developed world is still in great trouble, and, in a world of trouble (see the new issue of the Gary Shilling Insight attached) “the buck is the world’s safe heaven”. 2) The Euro Zone is in worse shape than the US (see the attachment US vs. EZ), and the Euro Zone has got a serious problem of leadership: we do not even have a Treasury! Who will take the necessary decisions? Mr. Draghi? Mrs. Merkel? Mr. Hollande? The Bundesbank? Mr. Monti? Mr. Rajoy? …A committee? Yes, probably a committee… and a committee never works!! If I remember well, it was Henry Kissinger who asked: “Who do you call, when you need Europe?”. Especially in a crisis, leadership is paramount! 3) The US has the clear possibility to become energy independent. And what if a trading deficit becomes a trading surplus? As far as I am concerned, Gary Shilling’s investments recommendations represent very good value in an era of deleveraging, even though they do not strictly adhere to the Graham’s value investing philosophy. “I don’t take break in my search for value” – Michael Burry giofranchi THE_DEBT-DEFLATION_THEORY_OF_GREAT_DEPRESSIONS.pdf insight-0812ab.pdf US_vs_EZ.pdf

-

“Who buys this stuff? For Japan’s corporate zombies it is evident that equity serves only as a sop for the banks and other debt holders. Mazda trades for just 11% of sales and at a 40% discount to book. That might make it look cheap, but it has little relevance if company management has to persistently issue more and more shares to keep the bankers from pulling the plug. It might be that Ben Graham’s value style of investing only worked so well in the 1930s because American firms had purged themselves of debt liabilities. It is my contention that value does not mix well with debt.” Hugh Hendry – April 2012 We all know the two pictures attached: in the 1930s US total debt / GDP (first picture) declined rapidly and it remained relatively low for the next 50 years. Then, in 1998 it was almost back up to the 1933 level. Also, in 1998 security prices were very high, and, with a very brief exception at the beginning of 2009, they have always stayed at historical high levels. So, at the end of the century, for the first time in almost 70 years we had both very high debts and very high security prices. And what followed is the second picture: BRK was killed by Gold… a almost completely useless, but glittering!!, cube of 67 feet in each direction. Those managers who really outperformed in the 1998 – 2011 stretch, Mr. Watsa (who loaded the boat with CDS), Mr. Einhorn (who shorted Lehman in 2008), Mr. Ackman (who shorted MBIA), Mr. Burry (CDS), etc., saw value differently. Shalab, I agree with you, when you say that Mr. Buffett has always been opportunistic. And right now the best way to be opportunistic, as far as I am concerned, and AS LONG AS WE HAVE BOTH HIGH DEBTS AND HIGH SECURITY PRICES, is: - to be long north America, - to be long the stocks of undervalued, owner-operated companies, - to be long (just a little bit) gold, - to be short small cap growth stocks, - to be short highly leveraged stocks. Maybe BAC is different from Mazda… maybe not… I don’t really know. So, I stay away. giofranchi US_Debt_-_GDP.pdf BRK_XOM_GOLD.pdf

-

txitxo, you are surely very good at what you are doing! Congratulations! You talk exactly like the nuclear engineer friend of mine is used to talking. And he is very successful too. So, I do not doubt that your method has great merit and that it deserves to be studied. Actually, I wasn’t hedged in 2007. I was worried and I moved to blue chip stocks: BRK.B, KO, JNJ, PG and XOM. In 2008 they behaved better than the market, but they were down nonetheless… After they recovered, at the end of 2010, I sold them fortunately with a profit, and moved to owner-operated companies, which are the businesses I really like. Don’t get me wrong, KO, JNJ, PG; XOM, etc. are awesome businesses, but… what do I really know about them? Who am I really partnering with? When my firm starts a new business idea, I want to know everything there is to know about it, and I want to be sure the right people are in charge. So, I reasoned, why invest differently? As you might have guess by now, Mr. Singleton of the former Teledyne Inc. is my “role model”! By the way, have you read “The Magic Formula” by William Poundstone? It is interesting to note that Claude Shannon, a great scientist, at the end of his life could have boasted a wonderful track record in the stock market (not far from Buffett’s track record!). He ran a very concentrated portfolio, of which the greatest majority of funds (by far!) was invested in Teledyne Inc.! So, a scientist like you, invested in an owner-operated company, the way a business person like me would do, and was very successful! That gives me hope… My company engages in structural engineering for civil and infrastructural developments, and manages a for profit Master School at the Politecnico of Milan University. They are both low margins businesses, but what gets to the bottom line is all free cash (maintenance capital expenditures are almost nil, and also growth is very cheap). So, I extract cash from not too good businesses and try to redeploy it buying very good businesses at attractive valuations. In a sense, I am copying what Mr. Buffett did with Dempster Mill Manufacturing and many times again during his career! Unfortunately, I am not that successful… I judge our results based on the increase of my firm’s equity at the end of each year. So, my investments return is not the only part of the equation: the earnings from our operations matter a lot too. Until now we have done pretty well, but we are still young and unproven: we got incorporated in 2004 with little capital, started operations in 2005, and I began investing our original capital plus the first retained earnings in 2006. Right now the business environment in Italy is dire… Results from our operations will surely suffer! Fortunately, I work with permanent capital and I don’t have to worry about redemptions. I ask for Mr. Watsa (FFH), Mr. Einhorn (GLRE), Mr. Loeb (TPOU), Mr. Steinberg (LUK), Mr. Marks (OAK), Mr. Flatt (BAM), Mr. Tisch (L), and Mr. Biglari (BH) to help me!! ;D I could not agree with you more! ‘Thinking Fast and Slow’ is a terrific reading!!! giofranchi

-

txitxo, maybe I misunderstood you, but on a 10 years basis the table shows a much better performance with equity hedges than without equity hedges... Well, of course I tried to do that... and it never really worked! But I guess it never worked JUST FOR ME. I don’t see any kind of edge in such a strategy, and I do not really like to put money in something I don’t understand, just because a screen says it is cheap. So, maybe, I didn’t try hard enough!!! Anyway, as far as I am concerned, that’s not investing. That’s trading with a value-based system. And I know some successful traders, but none who employs only value screens. Yet again, that might be because they manage too much money… Talking about Mr. Buffett, I have read all The Buffett Partnership Letters… twice. Describing a workout (Sanborn Map), already in 1960 he wrote: “Last year mention was made of an investment which accounted for a very high and unusual proportion (35%) of our net assets…”. That doesn’t look like a diversified portfolio! At the end of 1961 his net assets under management were $3.210.568,59, and he was already talking about “control” situations: “Sometimes, of course, we buy into a general with the thought in mind that it might develop into a control situation. If the price remains low for a long period, this might very well happen… We are presently acquiring stock in what may turn out to be control situations several years hence.” And in the January 18, 1963 letter he described the investment in Dempster Mill Manufacturing Company: and, as far as I am concerned, that’s investing! In 1963 he managed $9,4 millions, about $70 millions in inflation-adjusted dollars. I have never read anything about screens, but, if he happened to use them, he probably did so for just few years: in 1963 his capital under management was already too much! If I may ask, I am genuinely curious: what kind of returns did you achieve in the last five years, employing your screens? giofranchi

-

berkshiremystery, you make me breathe a sigh of relief: if Mohnish says AIG is out of his circle of competence, I cannot really be blamed to give up on AIG. Even if I will miss a big winner! giofranchi

-

Well txitxo, I won’t speak about the Dark Energy endeavour… but I hope that studying and acquiring businesses will prove to be, at least, a little bit profitable!! :) Take a look at the attachment: it is from the FFH's 2011AGM, and it shows the Hamblin Watsa Investment Performance in common stocks, with and without equity hedging. On a 5, 10, 15 years basis, the performance with equity hedging is significantly superior to the one without equity hedging. Even on a 15 years basis, the strategy with equity hedging returned 2,4% per year more than the strategy without hedging, which is big! On a 5 years basis, the strategy without hedging got literally killed! You may object that FFH can’t invest only in small caps. And you would be right: they are compelled to invest in medium and large cap stocks. So, is it possible that, if you invest in small caps and hedge, your performance will suffer, while, if you invest in medium and large caps and hedge, your performance will be much better? Is that what your model suggests? If so, why are you investing in FFH without hedging? I wouldn’t define FFH a small cap! That's exactly why I am hedging!! giofranchi 2011AGM_Hamblin_Watsa_Investment_Performance.pdf

-

Shalab, I wish I knew!! No, really: the Italian economy remains a mystery to me!! But, I think I see two main problems: 1) A COMPLETE LACK OF TRANSPARENCY: regarding Biglari’s compensation plan, and how he changed the rules, I was told “you don’t know what you are getting”… well, please don’t misunderstand me, but it made me smile… Come to Italy, then you will really understand the true meaning of unaccountability! North America is by far the place where you can find the greatest amount of reliable information. In that regard, Italy is still way way way behind… And how could you do business or invest without reliable information? 2) TOO BIG A GOVERNMENT: not just “big”, but also, which is even worse, “intruding”. Everyone looks for favors from politicians, because politicians are extremely powerful, even in business. I guess that is true worldwide, but we know how to take it to the extreme! I think in Italy we are still a socialist society at heart… and that is always very bad for business! Ah! As an aside, the Euro clearly is not helping either: if I remember well, the one we are currently living trough is the fifth recession, since the Euro was introduced… Hey! 1 recession every 2,5 years… something is just not working! Unfortunately, I can’t elaborate further… I have got too little, reliable information!! ;D giofranchi

-

tombgrt, Horizon Kinetics has just released its Q2 Commentary. Probably, you have already read it, but I attach it anyway. On page 10 they write: “The largest holding in many of our strategies, and that which probably attaches to the greatest number of predictive attributes, is Liberty Media Corporation.” Do you own LMCA? I have nothing but the utmost respect for Mr. Malone, but I haven’t invested alongside him yet… He is 71, probably won’t go on compounding for the next 20 years, but, let’ say, 10 years, at the rate he is used to compounding capital, are perfectly fine with me!! If you own LMCA, how do you value the company? You think it is undervalued right now? Thank you very much! Q2_2012_Horizon_Kinetics_Commentary.pdf

-

tombgrt, thank you very much! I always read anything Murry Stahl writes with extreme interest and attention! He is just great! Regarding LUK, I meant 20% CAGR in market price per share, not in book value. And my assumption was based on the fact that right now it is trading below book value, while usually it has traded far above book value! Finally, I like the hedges right now, because in a deflationary scare, both LUK and BAM, which I currently own, will suffer. Mr. Watsa is worried about deflation… so am I! David Rosenberg, Gary Shilling, Lacy Hunt are worried about deflation… so am I! And, if that happens, I want to have the buying power to double down aggressively both in LUK and in BAM. Vice versa, if that never happens, I am comfortable accepting a lower return on my firm’s capital for a while. giofranchi

-

ERICOPOLY, I was wondering: any idea why Mr. Watsa is not investing in BAC or in AIG right now? I know they are outside my circle of competence and I stay away. But I agree with you that BAC is extremely cheap right now, and I wouldn’t mind being invested in BAC through FFH. Like I don’t mind being invested in JEF through LUK, even though I would never invest in JEF by myself. Like I don’t mind being invested in YHOO through Third Point Offshore, even though I would never invest in YHOO by myself. Thank you very much! giofranchi

-

It should be added that, obviously, things in the stock market are much more chaotic and volatility is much greater! A market that decreases in value 0,5% each year for 7 years in a row is never heard of! And, if you are hedged, you can take advantage of any opportunity that may come your way during a market plunge. After the market has plunged, your hedges will be worth more, and you could double down in Leucadia. Furthermore, after the market has plunged, the margin of safety embedded in the price of the whole market will be much greater. So, instead of keeping a 100% hedged portfolio, you may decide to be only 50% or 30% hedged, depending on the severity of the market plunge. giofranchi

-

txitxo, I am an engineer. I have always been very comfortable with mathematics. I don’t want to brag, but it’s a language a speak fluently. Some years ago I started doing something similar to what you are doing, with a nuclear engineer friend of mine. He is even more comfortable with mathematics than I am… actually I know few people who are as comfortable with mathematics as he is! And he is successful in the stock market, just like you probably are. After a while, though, I realized that what I really take pleasure in doing is to run a business, and to study how other businesses works, and to acquire the ones I like the most, little by little. If I could buy entire businesses, that’s what I would be doing 7 days a week, 24 hours a day… and I would gladly forget about the stock market! Unfortunately, I still don’t have enough capital to implement that strategy successfully. So, I am compelled to buy businesses in the stock market. And that’s exactly what they are: BUSINESSES IN THE STOCK MARKET. To believe that they are completely free from the stock market gyrations, as if they were private businesses, to me sounds just naïve and, most importantly, simply not true! So, when I buy businesses in the stock market during a secular bear market, I seek two margins of safety: the first one embedded in the price of the business itself, the second one embedded in the price of the whole stock market. Obviously, in a secular bull market the second margin of safety would be much less important! Probably, I would disregard it altogether! According to what I believe is the actual margin of safety embedded in the market, I may decide to be 100% hedged, 70%, 50%, 30% hedged, or not be hedged at all. Right now I am 100% hedged, and I am just fine with it. Please, follow me for a second. Take, for instance, Leucadia National: yesterday it closed at $21,68, while at March 31, 2012 its book value was $25,8. It’s trading at 0,84 x book value. Now take the June 30, 2012 GMO 7-Year Asset Class Return Forecasts: US small – 0,5%. You know how accurate the GMO 7-year Asset Class Return Forecasts track record is. As you told me, in a year or two anything could happen, but, if you consider 7 years, the market becomes a “weighing machine”. That leaves us on one hand with a company, which returned a 19,8% CAGR from 1979 to 2011, trading below book value, and on the other hand with a basket of US small-cap stock (Russell2000), which are priced to deliver a negative annual return for the next 7 years. Now, I know that Mr. Cumming is retiring in 2015, but Mr. Steinberg is 68 and, you know what? If he decides to retire at 75, like Mr. Cumming is going to do, it will be exactly 7 years from now! At 0,84 x book value, Leucadia is priced to perform at least as good as in the past: 20% CAGR. But, let’s assume a 15% CAGR. We have already seen that the Russell2000 is priced to deliver a negative CAGR during the next 7 years. But, let’s assume a positive 5% CAGR. If I invest now $10.000 in LUK and $10.000 in RWM, 7 years from now I will be left with $33.600 ($26.600 in LUK and $7.000 in RWM). That translates into a 7,65% CAGR on my original investment of $20.000. While the market, the Russell2000, delivered a 5% CAGR. I have beaten the market with very low risk. Obviously, it gets even better if LUK performs in line with the past, and the Russell2000 performs in line with GMO forecasts: if that is the case, I would be delivering a 12,7% CAGR on my original investment of $20.000, running a very low risk! And without any leverage! It gets better and better, if you can invest in FFH, which employs this strategy, adding the benefit of float, “insurance leverage”, or the safest kind of leverage! So, I agree with you that, if you want to achieve a 20% CAGR for the next 20 years, this strategy is not the one to follow. But, once again, if you really will achieve a 20% CAGR for the next 20 years… then you are in another league, and there is nothing of value I can say to you! giofranchi

-

Thank you ERICOPOLY, I really get your point! You know, I think I have the 'forma mentis' of a business owner, which is slightly different from the one of a money manager: and I guess certain kind of investments will always be difficult for me (for instance, BAC or AIG today), even though I do believe they will turn out to be great winners… It is either a case of emotional stupidity, or a case of too narrow a circle of competence… most probably it is both!! :( giofranchi

-

1) Don't care about that. In fact, today Buffett has only "limited" influence on the future BV growth that BRK will achieve. I can also sell my stake and put it in FFH at any time or the other way around. I don't have to be in one of the two for 20 years. (But I also don't pay taxes on return.) 2) Sure. But it's not like Prem is working with a 9-numbers figure either. He has billions to look after as well. 3) Can't really compare both in that way. FFH is more leveraged and needs the hedges in this environnement, it's not just a macro bet. And I'd say that BRK's mountain of cash is a nice hedge as well. 4) This is hard to quantify. I believe that BRK will do just fine in almost any market. Sure, they would suffer more in a recession or market downturn but would it really matter for intrinsic value in 10 years? 5) One is almost completely insurance, the other also has many operations like BNSF, Marmon, Lubrizol, Netjets, See's Candies, ... Hardly comparable based on BV! Even without Buffett, BRK is worth much more than 1xBV. I'm not sure how much FFH would be worth without Watsa. I also know for a fact that BRK's future growth is far more certain than FFH's. FFH's growth is more sensitive to Prem's future successes and failures. tombgrt, Mr. Zell would have liked your answer very very much!! Simple, but true and clear ideas! Thank you very much. 1) I like BRK very much. Generally, though, I don’t like a business without an owner, who takes responsibility for all that really matters. First of all, obviously, allocation of capital. I really view the act of buying into a business like partnering with its owner. If Buffett’s responsibilities in BRK and his influence on BRK’s future will be less and less important, as far as I am concerned, that is a minus, not a plus. 5) Generally speaking, I like to compare any business, based on “Future book value”. That’s to say current book value + future earnings – future dividends. Only when this approach really doesn’t make sense, I use “owner’s earnings” yield (high-tech, bio-tech, etc.: obviously, I don’t invest in high-tech, bio-tech, etc.!). Stealing from “Accounting for Value” by prof. Stephen Penman of Columbia Business School, I like to think of the value per share of a business as the sum of the following parts: Value per share = Book value + Value from short-term accounting + Value from long term growth (or Value of speculative growth) What could materially differ from BRK to FFH is the last part: Value from long term growth. Of course, with BRK at 1,2 x book value and with FFH at 1,05 x book value, the market is already assigning no value to the speculative growth of both companies. Certainly, you may judge BRK’s Value of speculative growth worthier than the one of FFH, because BRK also owns BNSF, Marmon, Lubrizol, Netjets, See’s Candies, etc., but I am not so sure. First, it is called Value of speculative growth, because any growth is just that: speculative. Second, I guess it is not easy at all to make a $200 billion company grow. giofranchi

-

"I believe that the best way to manage money is to go long and short stocks. My theory is that if the 50 best stocks you can come up with don’t outperform the 50 worst stocks you can come up with, you should be in another business." - Julian Robertson And again, from the beginning: "The wise investor will disregard the day-by-day fluctuations of the stock market or real estate market and base his buying and selling on these long periods of rise and fall. Above all, and I repeat it again and again—he must have liquid capital in time of depression to buy the bargains and then he must sell before the next crash. It is difficult if not impossible to do this but the conservative longtime investor who follows the general rule of buying stocks when they are selling far below their intrinsic value and nobody wants them, and of selling his stocks when people are bidding frantically for them at prices far above their intrinsic value—such an investor will pretty nearly hit the bull’seye." - The Great Depression, A Diary I am not talking about market timing. I am talking about margin of safety. When there is not enough margin of safety, I think the way to invest is the one Mr. Robertson suggests. Exactly what Mr. Watsa is doing right now. To go long aggressively in a secular bear market, without any protection, stocks must be “selling far below their intrinsic value and nobody wants them”, or a HUGE margin of safety baked into the market. Exactly what Mr. Watsa did at the beginning of 2009. Regarding Europe, I would still be cautious: if Mr. Hendry is right, France is just a year away from nationalising its banks… and it won’t be pretty! On this regard, please check out what Charles Gave has to say (see attachment). giofranchi Daily+7.25.12.pdf

-

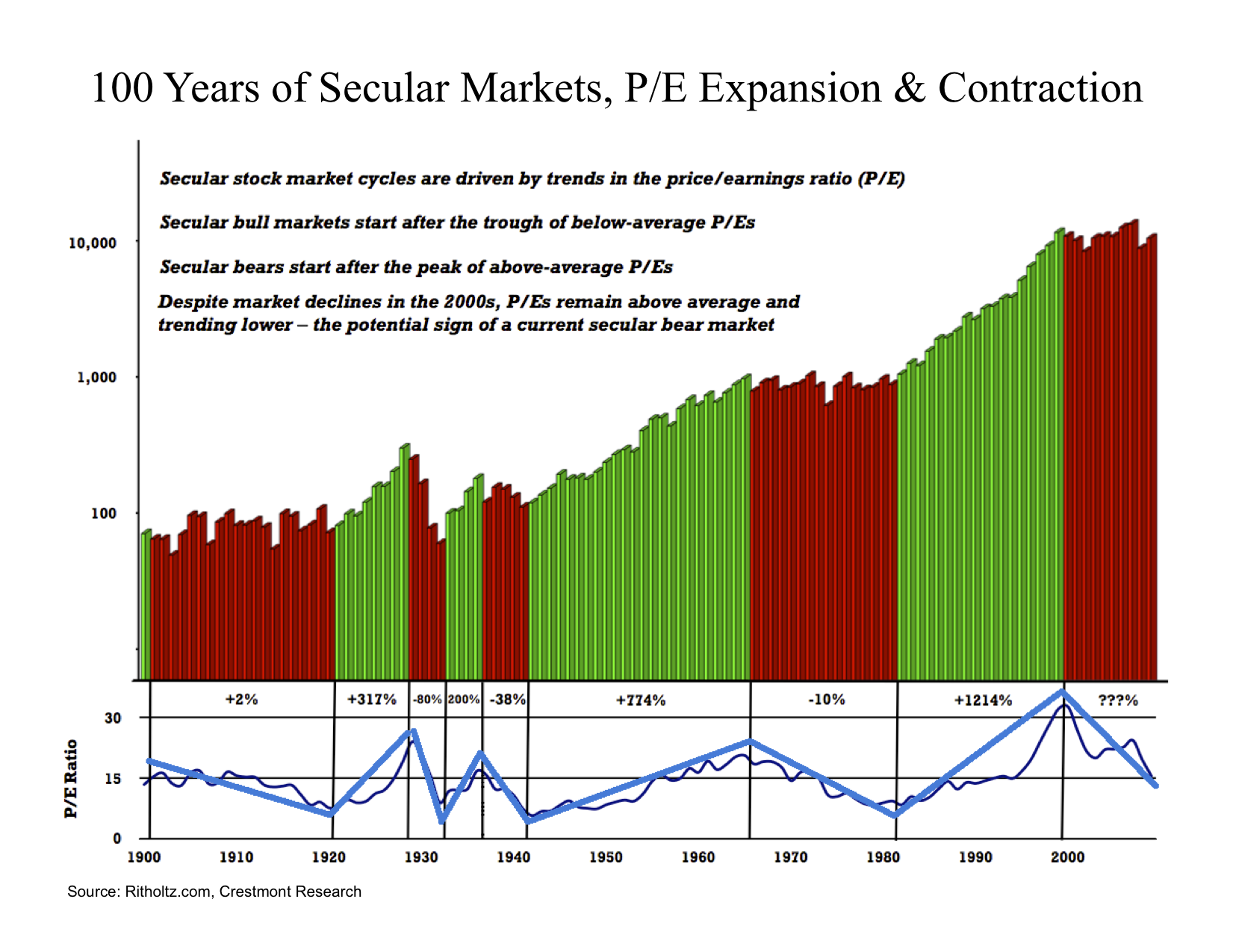

ERICOPOLY, I wasn’t talking about BAC. I simply won’t invest in mega-cap financial companies that I do not understand. No matter what their shares’ price is. If you understand BAC, the way certainly Mr. Berkowitz does, you will make a lot of money, along with Berkowitz and others. Glad for you! Instead, I was talking about market valuations. And, whether you use the Shiller P/E, or the Market Value / GDP ratio, or the Q Ratio, or the GMO 7-years Asset Class Return Forecast, or the Regression to S&P Composite Index Growth Trend, or you pay attention to the very accurate work done by John Hussman, one thing seems clear to me: market valuations are not consistent with a secular bear market bottom. At least, I have still to find someone with an analysis rigorous enough, to convince me of the opposite. Please, mind I didn’t say ‘market valuations are high’, that might be more debateable. Instead, I just said ‘market valuations are not consistent with a secular bear market bottom’. That is true, even if we use the S&P500 TTM P/E: right now it is 15,93, while at secular bear market bottom it has always been below 10. Please, check the image in attachment (which, of course, you already know!). Last week the TTM P/E of the Russell2000 was 31! Ok, I get that they are small-cap and growth stocks, but do you really think that people would be willing to pay 31 times earnings (for any kind of asset), if we really were at the bottom of a secular bear market? I have serious doubts. giofranchi

-

I do not agree. 1) Mr. Watsa is 20 years younger than Mr. Buffett: FFH > BRK, 2) Mr. Watsa has to work with much less capital than Mr. Buffett: FFH > BRK, 3) Mr. Watsa is fully hedged: don’t get me wrong, it is not that “value investing” doesn’t work, value investing is the only way of investing, but, in a secular bear market, when valuations are high, and there is a mountain of debt in the system ($70 trillion of G10 debt is the collateral for $700 trillion in derivatives… 1200% of global GDP… mind numbing!), it is “INVESTING” that does not work! FFH > BRK, 4) FFH relies on insurance much more than BRK: and I like insurance in a bear market, people always need protection, in good and in bad times, what saved the day at BRK in 2008 were the insurance operations: “Most of the Berkshire businesses whose results are significantly affected by the economy earned below their potential last year, and that will be true in 2009 as well. Our retailers were hit particularly hard, as were our operations tied to residential construction. In aggregate, however, our manufacturing, service and retail businesses earned substantial sums and most of them – particularly the larger ones – continue to strengthen their competitive positions. Moreover, we are fortunate that Berkshire’s two most important businesses – our insurance and utility groups – produce earnings that are not correlated to those of the general economy. Both businesses delivered outstanding results in 2008 and have excellent prospects.” Warren Buffett. And I like what Mr. Watsa said in the most recent Q2 2012 Earnings Call: “As I said in the first quarter call, we are growing again. The large catastrophe losses in 2011, very low interest rates and the reduced reserve redundancies means that there is no place to hide in the industry. Combined ratios have to drop well below 100% for the industry to make a single-digit return on equity with these low interest rates.” FFH > BRK, 5) FFH trades at 1,2 x book value, while FFH trades at 1,05 x book value: FFH > BRK, 6) BRK is less leveraged, and therefore less risky than BRK: BRK > FFH. Where does this leave us? FFH 5, BRK 1. Of course, you might object it is too simple a thesis. Quoting Sam Zell: “I philosophically believe that if you can't delineate your idea in one or two sentences, it's not worth doing. I'm the Chairman of everything and the CEO of nothing, which means that the people who work for me come to see me with ideas all day long. My criterion is if they can't concisely explain their idea, then I throw them out of my office and tell them to come back when they can. Simplicity is critical.” giofranchi

-

West, you are certainly right. But, as I wrote at the beginning of this topic, I have nothing to say to people who can achieve a 20% CAGR for 21 years… There is not a single doubt in my mind that they are future billionaires! They do not have even to promote their skills! Money will surely find them! The brother in law of my brother in law (ok, that sounds a little bit confusing…) is Mr. Carlo Pesenti, CEO and controlling shareholder of the Italcementi Group. If I could assure him that I will achieve a 20% CAGR for 21 years (and if he believes me!!!!), he will sell all the cement he possesses, will shut down his multinational company, and will give me the proceeds to invest! giofranchi

-

2013 AGM of FFH - some newbie questions

giofranchi replied to lance2210's topic in Fairfax Financial

I was at the 2011 AGM. Unfortunately, I could not attend the 2012 AGM. In 2011 the Roy Thompson Hall wasn’t completely filled out, and they didn’t check for shareholders’ credentials. The meeting started early in the morning and was finished by noon (if I remember correctly!). Of course, many people on this board can be of much greater help to you than I can! giofranchi -

I called (1 + R/S) the insurance leverage factor. That might be misleading. I think it is much better to define (1 + R/S) as the “investment leverage factor”. While P/S could be defined as the “underwriting leverage factor”. In fact, being R = A – S, it follows that: (I/A)(1+R/S) = I/A + (I/A)(R/S) = I/A + (I/A)[(A –S)/S] = I/A + (I/A)(A/S – 1) = I/A + I/S – I/A = I/S, which is return on equity from investments. Of course, (U/P)(P/S) = U/S, which is return on equity from underwriting. I know this is 101 insurance analysis, but may some “Newbie” can find it useful… at least, I hope so! Lastly, from Investments should be eventually subtracted $7 billion in subsidiary cash, the $1 billion at the holding company doesn’t count. That leaves us with an Investments/Surplus of almost 240%.

-

Shalab, I did not mean to say that BRK and FFH are the same kind of business. Instead, what I meant is the following: 1) when you find a manager with a proven track record, 2) when you understand what he does and agree with his investment philosophy, 3) when he works with permanent capital (not subject to investors’ redemption), 4) when he is still young enough to go on compounding for the next 20 years, 5) when he doesn’t have to work with too much capital yet, that inevitably dampens returns, 6) when he can use “insurance leverage” (which is quite different from “leverage”), and you cannot, 7) when you can partner with him at book value, Etc. etc. etc. Well, it is generally a good idea to invest in his or her company, whether it is BRK or FFH. When you say that BRK had lower float in 1997 than FFH does today, I guess you mean that FFH is more leveraged, and therefore riskier. Of course, I agree. But let’s examine how an insurance company increases shareholders’ equity: T/S = (I/A)(1+R/S) + (U/P)(P/S) Define: T = Total after-tax return I = Investment gain (or loss) U = Underwriting profit (or loss) P = Premium income A = Total Assets R = Reserves & Other Liabilities S = Shareholders’ Equity T/S = Total Return on Equity (1+R/S) will always be positive, and, as long as an insurance company continues to write insurance, P/S will be positive too. So, for T/S to become negative (that’s to say, for shareholders’ capital to decrease), I/A and/or U/P must be negative. Furthermore, I/A is much more important than U/P, because the insurance leverage factor (1+R/S) will always be greater than 1, whereas P/S might be lower than 1 (actually, at the end of 2011 P/S for FFH was less than 1, see Net Premiums Written vs. Statutory Surplus in attachment). And I hope you agree with me if I say that, as far as I/A is concerned, I am fully confident with the Hamblin Watsa Investment Performance (see attachment). This is not to minimize the importance of U/P! Which is extremely important: as long as U/P stays positive, P/S can increase. Furthermore, if underwriting results are good, FFH could “indulge” in a more aggressive investment policy (more RIM like investments… ok, just joking!!!!). And this is why I wrote in another post that, given his track record at Odyssey Re, I really like Mr. Barnard to oversee all FFH insurance operations. If FFH as a whole becomes a profitable underwriter, I believe that this company will be much more valuable than many now think possible. Finally, compared to other insurance and reinsurance companies, FFH does not seem to be too much leveraged: Premium/Surplus is less than 100%, while Investments/Surplus, if from investments we subtract $8 billion in cash, is more or less 220% (see the attachment "Insurance Leverage"). Net_Premiums_Written_vs._Statutory_Surplus.pdf Hamblin_Watsa_Investment_Performance.pdf Insurance_Leverage.pdf

-

We all know the image in attachment. So, what if Jeremy Grantham is right, what if Hugh Hendry is right, what if John Mauldin is right, what if John Hussman is right, what if many other “macro-guys” are right, and in 2017, or 2018, or 2019 will be 1982 all over again? And a new secular bull market will be finally launched? My parents are truly great! They gave me the best education possible, they were always loving, and they always cared for me. But, there is just one regret I keep holding against them (I know, too bad of me!), that is: Why on earth didn’t you invest in Berkshire Hathaway in 1982??!! Ok, they had never heard of Ben Graham or Phil Fisher, so I guess they can be forgiven! But, on this board you are all very bright and knowledgeable money managers, and you know everything about value investing. Nonetheless, I keep reading sentences like the following: “I sold my shares in FFH, because I found greater values elsewhere.” So I ask you: Why on earth won’t you be invested in Fairfax Financial in 2017? Bear with me a moment, and allow me the chance to explain. Let’s assume that in 2017 FFH will be trading around book value, like it is trading today. Most probably, if a new secular bull market is just a few days away, in 2017 the S&P500 Shiller P/E will be no higher than 12. Today it is 22,26. So, I guess in 2017 “greater values elsewhere” will be much more common than they are today. It follows you won’t invest in FFH. Not to invest in FFH at book value implies the following two hypothesis: 1) You have to do better than the markets, even though at the beginning of a secular bull all markets will rally, and it won’t be that easy to keep up with them… anyway, I agree that value strategies perform much better at the beginning of a secular bull than at the end, so let’s check hypothesis number one. 2) To shun FFH at book value, you must be confident to achieve a return on your money higher than the return Mr. Watsa will achieve on FFH shareholders equity. Even though Mr. Watsa is demonstrably one of the few money managers who consistently and appreciably have beaten the markets. Even though Mr. Watsa works with the float that magnifies his returns. Are you so sure that we can check also hypothesis number two? My answer follows: Aaron Marcu remembers the phone ringing one August evening in 2003. It was Ackman – on vacation in Italy – wanting to chat with Marcu about an article he’d come across in a bankruptcy law journal that he thought might relate to MBIA’s involvement in the credit-default-swap market. “Bill, it’s 9 p.m. here,” Marcu told him. “It must be 3 o’clock in the morning where you are.” “This is incredible stuff,” Ackman said. “I can’t put it down.” Here’s a person, Marcu says, who seems to have gotten quite a few things in life right. “He’s tall, good looking, rich. He has a great family, lives in an incredible apartment,” Marcu says. “So what is he doing reading a bankruptcy treatise at 3 a.m. in the morning when he’s on vacation in Tuscany?” - The Confidence Game So, to all the Ackmans out there I say: Ok, not a single doubt in my mind that you will be extremely successful! But, you must stay up until 3 a.m., reading a bankruptcy treatise, on a vacation in… well, wherever you go on vacation! (I will be in Tuscany in two weeks!! Really!! Ahahahahahah!!) Everybody else should heed the always insightful Mr. Buffett: “It’s not necessary to do extraordinary things to get extraordinary results.” I reckon an investment in FFH at book value the simple (“but not easy”) thing that will get you extraordinary results. You may object: 2017??? What about the five years in between?! Well, if all those “macro-guys” are right, in the next five years ‘Bad things are going to happen’ (See the FT article on Hugh Hendry, July 17, 2012). We are still living through a secular bear market. And in a secular bear market asset allocation is much more important than stock picking: “The wise investor will disregard the day-by-day fluctuations of the stock market or real estate market and base his buying and selling on these long periods of rise and fall. Above all, and I repeat it again and again—he must have liquid capital in time of depression to buy the bargains and then he must sell before the next crash. It is difficult if not impossible to do this but the conservative longtime investor who follows the general rule of buying stocks when they are selling far below their intrinsic value and nobody wants them, and of selling his stocks when people are bidding frantically for them at prices far above their intrinsic value—such an investor will pretty nearly hit the bull’s-eye.” - The Great Depression, A Diary I cannot think of a better description for Mr. Watsa. During the next five years, there is the clear and distinct possibility that the protections Mr. Watsa had put in place will be much more valuable than all those supposed “greater values elsewhere”. giofranchi SP_500_1995-2011_and_Projected_Overshoot_2011-2021.bmp

-

On RIM, Watsa Asks For a Little Perspective

giofranchi replied to Parsad's topic in Fairfax Financial

I agree with you! For instance, I have the highest respect for Mr. Barnard and for what he achieved at OdysseyRe until 2010. I also thought it was a great idea to put him in charge of overseeing all the insurance operations: if FFH as a whole starts underwriting profitably, like OdysseyRe has already done for years, I really think this Company is going to be much more valuable than many nowadays believe (on this regard, the first six months of 2012 were just fine!). I would like to start a new topic, titled: What if it is 1982 all over again? See you there! Thank you very much, berkshiremystery! Too flattering! -

On RIM, Watsa Asks For a Little Perspective

giofranchi replied to Parsad's topic in Fairfax Financial

Sorry... I know it is "to imply"... my English is very very poor! :(