longlake95

-

Posts

789 -

Joined

-

Last visited

-

Days Won

4

Content Type

Profiles

Forums

Events

Posts posted by longlake95

-

-

27 minutes ago, thowed said:

Truck-load arguably canaries in coal mine for recession? People getting out?

OR

Great companies valued thusly, and valuation just reasonably de-rating a little?

n.b. I haven't read the ODFl call yet.

Great, well-managed companies - I am attempting to dribble in to ODFL on a day like today.

all of the above. Partly, I think, a hang-over from absolute boom times in 2021-2022. Many companies still working down bloated inventories. The truckers are obviously exposed to that, along with general cyclicality. But the really well run ones, like ODFL and TFII will do smart things during slow times and gush cash on the next up cycle. All that I know is the stocks will move higher before we read about the end of the freight recession in the paper.

-

5 minutes ago, ValueMaven said:

What's going on with ODFL? Down again ...

down in sympathy maybe, TFI reported this morning. Truck-load in a very sorry state these days. Bedard, says this freight environment is one of the "worst in 30 years".

As for TFII, considering the environment, they put pretty numbers.

-

Doo. Great song. Ya, she's amazing. Under-rated.

-

My latest crush. Highly under-rated. Amazing voice.

-

Same. I’ll be the guy crawling across the finish line at the race on Sunday.

-

Parsad, thanks for the notes on the AGM. I was there this year, nice to see/meet so many of the managers of FFH companies and managers of some of the larger investees. 2 things really jumped out at me this year. Firstly, more discussion on buying better businesses and letting compounding work its magic ( a la, BRK). Second, I think I heard Prem correctly, when he said they only need a 5% return on the investment portfolio to achieve their 15% growth in BV hurdle. The 30 year return has been 7.7%CAGR. It reinforces how they just need to keep hitting singles and doubles for this to be a REALLY good investment over time. A few home-runs will just be icing on the cake.

The discussion on owning financials (and the 2.5x multiplier effect) in a growing economy was very interesting as well. Hard not to get excited about India for the next couple decades.

-

1

1

-

-

Ya, sorry, drifted….

-

3 minutes ago, Jaygo said:

I have a much easier time finding value here though. Wajax, FFH, DOO, Doman, Equitable all under 10P/E

The US equivalents are generally valued higher.

Agreed, however, a great example of the perfect combo is Canadian domiciled - US/international operations, think FFH. SJ, sells most of their products in the US.

TFII, Canadian based US centric. I’ll pay up for this model. Not much though I’m thrifty. -

It’s unfortunate, and that’s the reason Canada will never be as successful as the US.

I spent a lot of time down there, and their work ethic is much greater than north of the border.

Another reason to have a bulk of your assets at work outside our borders.

-

That’s the problem Jaygo, you’re the exception. You work hard like I did/do, and you built your net worth. Not afraid of work. Now we have the generation behind us, that’s used to the government propping them up. Yes, I know, not everyone is lazy…

but, tell me why, in Canada 40% of Canadians receive more in government benefits then they contribute to system. Talk about long term damage.

Rant over.

-

bought more GIL on the 26th. I'm in the camp that Chamandy is coming back. Probably wrong though.

-

Just now, SafetyinNumbers said:

I hope Viking doesn’t mind me responding but I’m almost certain the Canadian banks that are acting as counterparties are fully hedged (i.e. they own the shares directly). The play here is the income they earn on financing the TRS for FFH. They are not betting against FFH, they are simply providing credit.okay, that makes sense, thanks, so the banks are the middle man... would love to know who the underlying counterparty is...

-

Viking:

I apologize if you covered this in the various threads already, but, don't you find it very interesting that the TRS counter-party is the Canadian banks. I guess they (the banks) really do have a "Chinese wall", when you have the investment research side of the banks basically all pounding the table on FFH now. If the analysts are already onside/or coming on side recently, as to the value in FFH, then who the hell is making the call to be the counter party to the FFH swaps? Just seems very peculiar.

LL

-

I think he is too smart. I prefer the dim-bulb approach.

-

4.39% CAGR since inception (2002).

-

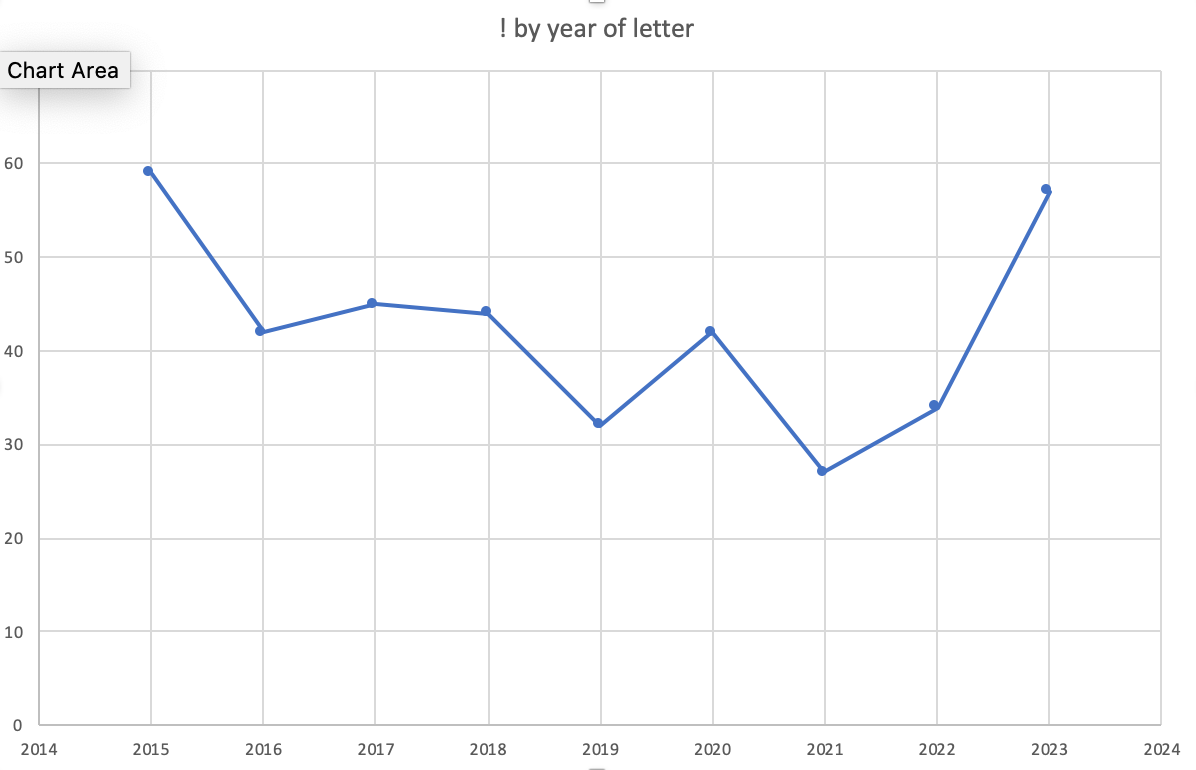

4 minutes ago, gfp said:

Clearly we are back from the doldrums of exclamation point frugality

looks like a perfect buy signal in 2021...

-

1 minute ago, formthirteen said:

Thanks. Seems like a good alternative to cash.

ya, I have a basket of floater prefs, where I've parked cash until a good idea comes along. I'm in the camp (probably wrong, lol) that rates are higher for longer, so these floaters are a good place to be. Incidentally, based on a $25 par, many of these prefs are 8% money for the issuer(s). So, if rates do stay higher for longer, maybe they take some of them out and issue lower rate prefs.

-

That’s really neat. I miss Charlie.

-

parked more $$$ in FFH.PR.D, yielding 9.6%, goes ex-divvy this Friday.

-

18 hours ago, Munger_Disciple said:

I am not sure you are correct. Buffett actually sold a few shares of his Berkshire stock in the 70s when his wife wanted to buy a house in Laguna Beach. More importantly, Buffett said this in the 2014 Special 50-year shareholder letter:

"Another warning: Berkshire shares should not be purchased with borrowed money. There have been three times since 1965 when our stock has fallen about 50% from its high point. Someday, something close to this kind of drop will happen again, and no one knows when. Berkshire will almost certainly be a satisfactory holding for investors. But it could well be a disastrous choice for speculators employing leverage."

I'll try to find the my source on this (read this a longtime ago) : but I'm fairly sure when Buffett bought ocean side house in Laguna, he promptly put a mortgage on it, and put the proceeds right back into BRK. He just carried that little mortgage around, cuz it was dirt cheap $$$ and posed no financial harm.

-

15% FFH + 5% FIH +0.5% FFH.PR.D = 20.5% or so…

-

2 hours ago, backtothebeach said:

The Japanese trading house investment is truly a masterpiece.

Purchasing high, durable dividend yields, with hedged currency, using almost free money. After a 30 year sideways market, right before take off. Stunning.+1

-

Agreed. I think the biggest lesson for me the last 20 years, has been to constantly re-assess if your thesis has under-shot or over-shot as the fundamentals play out over time. If you’ve under-shot like I did with HPS.a, where the business has blossomed mightly ahead of my thesis, JUST SIT ON YOURS HANDS. Continually re-assess. Easy to say, hard to do. But sure is fun.

Confirmation bias can really kill your returns.

-

Ya, it’s been quite the ride. Bought in 2020. Trying to water the flowers and pull the weeds here - letting winners run. Sitting on my hands, mostly, very interested to hear their commentary on current business conditions and the backlog. I think they earn +$6 this year.

LL

Berkshire Hathaway Annual Meeting 2024

in Berkshire Hathaway

Posted

Register a few shares directly in your name. You’ll get the AR materials sent directly to you. Works really well.