keegomaster

-

Posts

46 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Posts posted by keegomaster

-

-

13 hours ago, Viking said:

Fairfax’s equity portfolio looks very well positioned today. Most of the equity holdings purchased since 2018 have been performing well. And, after years of hard work, the poor performing equity holdings (many purchased from 2014-2017) have largely been fixed and are now performing well. In fact, the equity portfolio looks better positioned today than at any other time in Fairfax’s recent history (in terms of size and quality). We are increasingly seeing the benefits in improved reported results. The best recent example is ‘share of profit of associates,’ which spiked to more than $1 billion in 2022; the previous high was $402 million in 2021.

What happened? Four things:

1.) Fairfax learned lots of lessons from the poor purchases they made from 2014-2017. They are putting a premium on management. Hamblin Watsa has decided it is not a turn-around shop - looking to actively run poorly lead/challenged businesses. They are not a piggy bank for poorly run companies in search of cash. It appears to me that Fairfax has tweaked their methodologies used when allocating capital.

Others on this board argue that:

2.) the Fed and the ending of easy money (zero interest rates/QE) is a key driver in the stronger performance the past 2 years of Fairfax’s equity holdings. Value investing is back!

3.) the timing of the cycle is finally working in Fairfax’s favour and this is driving the stronger performance of the equity holdings. Value, resource and commodity stocks are all in a secular bull market.

4.) opportunities available in recent years are more in Fairfax’s wheelhouse (i.e. TRS on Fairfax shares, buying back shares of Fairfax India at 60% of BV etc).

At the end of the day, all of the above is likely partly responsible for the improvement we have seen in Fairfax's equity holdings in recent years.

—————

It can be instructive to look into the past so we can learn. This helps us understand what has been baked in to past results. In turn, this can help us understand what may happen in the future.

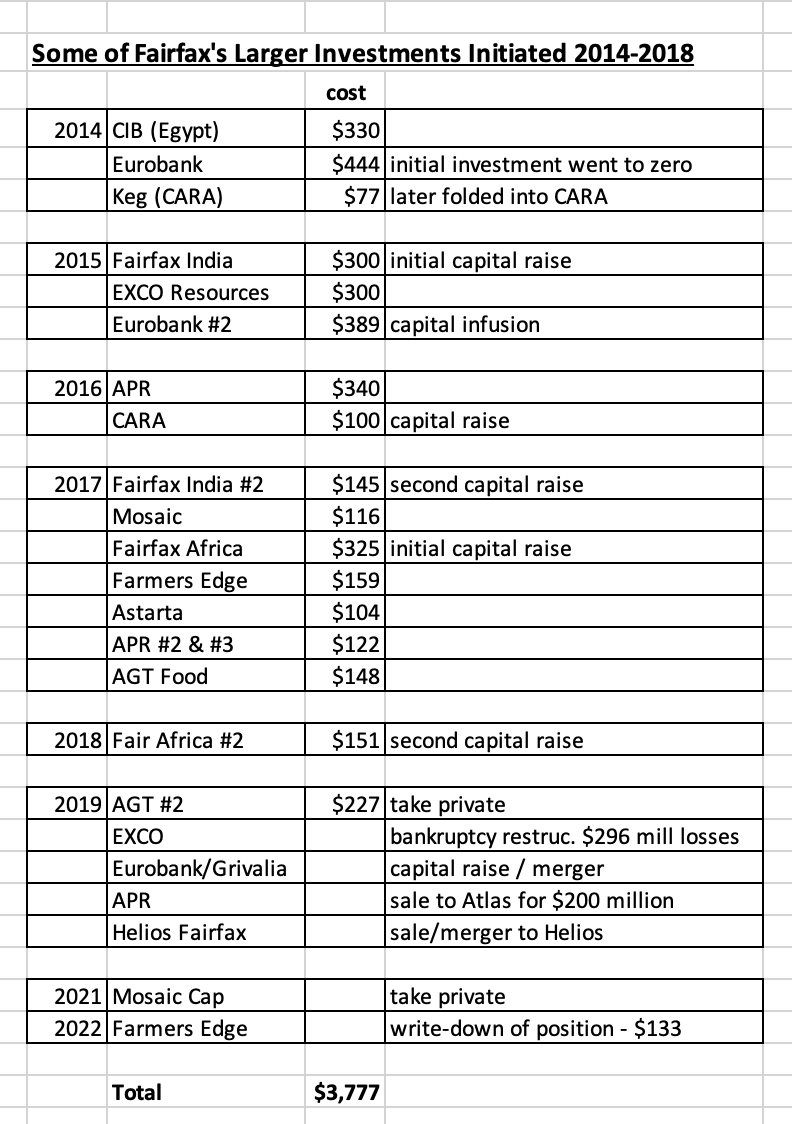

What happened with the purchases from 2014-2017?

10 investments are briefly reviewed below. Fairfax invested a total of about $3.5 billion in these 10 investments over the years. Over the past 8 years my math says Fairfax booked losses in these 10 investments of about $1.5 billion (about $200 million, on average, each and every year). For example, in 2022, Fairfax wrote down its investment in Farmers Edge by $133 million. Stuff like that.

Of course, the far bigger cost to shareholders has been the opportunity cost. Prem says repeatedly that Fairfax expects its equity investments to deliver returns of 15% per year. Applying a more modest 10% target, the $3.5 billion in investments (made 2014-2017) should have doubled in value by now to $7 billion. Clearly that has not happened with these investments. The opportunity cost of the poor investments made from 2014-2017 is likely an additional $2 billion.

This is actually a good news post. The good news is:

1.) the equity purchases made from 2018 to April 2023, as a group, look very good and are performing well.

2.) as I will review below, the problem investments from 2014-2017 look like they are not only fixed - they are also (mostly) poised to deliver solid returns for Fairfax shareholders moving forward. An 8 year long big headwind has now become a big tailwind.

As a result, I expect Fairfax’s $16 billion equity portfolio to generate a much higher total return (percent and absolute) in the coming years than it has delivered over the last decade. Given its current construction, I think it could well compound at 12% over the next couple of years = $1.9 billion/year in earnings:

- dividends = $120 million

- share of profit of associates = $900 million

- consolidated earnings = $240 million

- mark-to-market investment gains = $650 million (not including fixed income)

—————-

Below is a short review of 10 large investments made over the 4 years from 2014-2017.

1.) EXCO Resources (2015): Fairfax’s initial investment was $300 million in 2015. We have since learned that shale was a bubble and it eviscerated something like $5 billion in capital up until 2020. Fairfax reported cumulative realized losses of $296 million on EXCO in 2019 (that’s what they said in the AR).

- Learning: old economic model for shale was a sham.

- The good news: energy looks like it is in a structural bull market; new economic model for shale looks good - focussed on shareholder return.

2.) APR (2016): Fairfax invested a total of $462 million in APR in 2016 and 2017. In 2018 they sold it to Atlas for $200 million (in Atlas stock). The first thing Atlas did was replace the CEO.

- Learning: Terrible business. Poorly managed.

- The good news: APR is now Atlas’ problem.

3.) Fairfax Africa (2017): launched with much fanfare in 2017, Fairfax invested a total $476 million. Two short years later Fairfax exited its management of the business and moved the assets to a fund managed by Helios. The value of the Helios fund today is about $100 million. I am not sure what the total financial loss was for Fairfax on this investment but it was significant. The damage to Fairfax’s reputation was also significant.

- Learning: Hubris on steroids? Terrible idea. Worse execution.

- The good news: Fairfax is partnered with Helios and looks well positioned moving forward in Africa. This is now a small investment for Fairfax.

4.) Farmers Edge (2017): Fairfax invested $159 million in Farmers Edge in 2017. Farmers Edge completed its IPO in 2021 and in the 2021 AR Fairfax said their total investment in Farmers Edge to that point was $376 million. CEO ‘stepped down’ in April of 2022. In the 2022 AR, Fairfax said Farmer’s Edge had a carrying value of $71 million, after taking a $133 million write down in 2022. Market value of Fairfax stake was $5 million at Dec 31, 2022. My guess is this investment, because it performed so terribly post-IPO, has caused Fairfax some damage to its reputation (given Fairfax was the majority shareholder).

- Learning: Yup, SPAC’s were a bubble.

- The good news: carrying value is $71 million. This is now a small investment for Fairfax.

5.) Eurobank (2014): Fairfax invested $444 million in Eurobank in 2014. This initial investment went to close to zero later that year when the ECB came in and mandated a 1 for 100 reverse share split. What was the problem? Greece was in the midst of a depression. What did Fairfax do? It doubled down and invested another $389 million in Eurobank in 2015. in 2019, Eurobank executed a capital raise / merger with Grivalia. Greece elected a pro-business government in 2018. Eurobank fixed its balance sheet.

- Learnings: Just because the strategy worked in Ireland doesn’t mean it would also work in Greece.

- The good news: Greece’s economy is very well positioned. Eurobank, always well managed, is executing well and earnings are spiking: share of profit of associates for Eurobank was $263 million in 2022, increasing from $162 million in 2021. Prem estimated Eurobank could earn €0.20/share in 2023; if so, Fairfax’s share of profits for Eurobank could be well over $300 million in 2023. This investment is looking like it will turn into a home run for Fairfax in the coming years - a Greek tragedy turns to triumph!

6.) AGT (2017): Fairfax invested $148 million in AGT in 2017. In 2019, as AGT was experiencing financial difficulties, Fairfax took AGT private, spending another $227 million (I think).

- Learnings: It takes much more than a dynamic Canadian founder to succeed.

- The good news: from 2022 Fairfax AR: “AGT, run by founder and CEO Murad Al-Katib, had a record year in 2022, with EBITDA of over Cdn$150 million. This is a dramatic improvement from the time of the take-private transaction almost four years ago when the business was generating slightly over Cdn$60 million in EBITDA… Fairfax has an approximate 60% stake in AGT.”

7.) Commercial Industrial Bank (CIB) Egypt (2014): Fairfax invested $330 million in CIB in 2014. Today the position is worth about $240 million. Great company. Solid management. What is the problem? Egypt’s economy has been a slow moving train wreck for decades - with constant currency devaluations.

- Learning: Constant currency devaluations (like 50% in the last year) hurt equity values.

- The good news: the bank is well managed.

8.) Mosaic Capital (2017): Fairfax invested $116 million in Mosaic in 2017. In 2021, Mosaic was taken private (not by Fairfax) with Fairfax owning 20% of the new investment. This investment went sideways for may years (that opportunity cost thing).

- Learning: not every investment you make is going to work out the way you plan.

- The good news: Fairfax found a partner where Mosaic will hopefully be a better fit.

9.) Recipe/CARA (2014 & 2016): Fairfax also made a couple of restaurant investments from 2014-2017: $77 million in the Keg in 2014 (later merged with CARA in 2018) and $100 million in the CARA capital raise in $2016. Recipe/CARA was a poor investment for minority shareholders over its lifetime.

- Learning: the restaurant business in Canada is a tough business. Consolidating it proved to be even tougher.

- The good news: In the take private deal in 2022, Fairfax purchased Recipe at a covid-low price. Recipe has a solid collection of assets that should be able to produce significant free cash flow for Fairfax moving forward.

10.) Astarta (2017): Fairfax invested $104 million in Astarta in 2017. Today that investment is worth around $45 million. I know very little about this investment. I wonder if it is not a similar situation to CIB, with opportunity cost being the big issue.

Honorable mention: Torstar was initiated as a position before 2014 so I did not include it. However, Fairfax added to its position in 2014, 2016 and 2017 (yes, small amounts). In 2020 it sold the business and booked a $52 million loss.

I see lots of self inflicted wounds in the investments listed above - the list reminds me of the Monty Python skit “tis but a scratch" (see bottom on post for some entertainment).

Thanks for the analysis. Can't help but gasp at the value destruction. It's like Hamlin Watsa just set money on fire.

Were it not for the hard market in insurance, and the smart no bond positioning management FFH would not be a good investment.

Thanks for the thoughtful look back, Viking.

-

As another data point Prof. Damodaran has posted the following Implied Equity Risk Premiums updates at the beginning of the month (also showing the preceding month):

Implied ERP on April 1, 2023= 4.88% (Trailing 12 month, with adjusted payout); 5.44% (Trailing 12 month cash yield); 5.72% (Average CF yield last 10 years); 5.19% (Net cash yield); 4.64% (Normalized Earnings & Payout)

Implied ERP in previous month =4.78% (Trailing 12 month, with adjusted payout); 5.58% (Trailing 12 month cash yield); 5.50% (Average CF yield last 10 years); 5.34% (Net cash yield); 4.53% (Normalized Earnings & Payout)

Source: https://pages.stern.nyu.edu/~adamodar/

-

Agree with Tom Russo or Tom Gayner.

-

Hi,

I've been looking for a cheap way to subscribe to Bloomberg, and in the past I have found expired promotions for 2-year subscriptions from 3rd party vendors.

Tonight I came across First American News (FAN), who are offering this 5-year subscription to Bloomberg Digital for $60. Wondering if anyone has experience with FAN in particular, or with other 3rd party vendors in general?

Thanks!

~ Keego

Fairfax 2023

in Fairfax Financial

Posted · Edited by keegomaster

You make a compelling argument. My question is what are the potential scenarios (optimistic, pessimistic, realistic) after three years? What normalized level of earnings could we expect? From the Q1 conference call, and Jen's comments, it seems like earnings will be more susceptible to interest rates due to IFRS 17.