rayfinkle

-

Posts

233 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Posts posted by rayfinkle

-

-

On 4/19/2023 at 7:51 PM, LC said:

I don't have transformation experience, but two pieces of advice:

-need to have a team in place you can rely on

-sometimes, a public execution is necessary

Yea 100%

-

I'm considering buying a company and would love to get some thoughts on lessons learned from those that have done this themselves. I am currently working on narrowing my search aperture. But for now the possibilities are pretty unconstrained. Specifically, target co ideally has some of the following characteristics:

- Cash flow positive, or with a bulky cost structure that can get to CF+ (I've managed large-scale cost takeouts / turnarounds. This is unpleasant but doable, especially if purchase price reflects the work to be done)

- Can be large or small. I have financial backing to do a bigger deal (e.g., $2-500M in market cap), but smaller is also fine. I'd say small end would be $500k-1M in cash flow to owner

- Prefer software type businesses but have operated and am comfortable with "boots on the ground." In PE days did both, but have operated more in the former recently.

- Can be public (though this is harder to execute for a bunch of reasons) or private

I'd appreciate anyone's thoughts on lessons learned (positive or negative).

Thanks!

-

Does anyone know how US-based investors can trade options on Australian exchanges? IBKR won't let me...

-

great recs, thank you! good fodder for reading list.

-

I just listened to this podcast. It had some fascinating anecdotes about processes to make decisions. Does anyone have interesting books, etc. to get deeper on this? For example, I've read a bunch on similar topics and this podcast introduced me to a concept that was net new to me.

Thanks all!

-

hey everyone- I ended up going with First Republic. They make it really easy to apply and for existing mortgage customers it is quite cheap. It's not the highest LTV, but at the end of the day it is by far the easiest option.

I'm going to end up with ~70-80% combined LTV.

I have an interest only first mortgage with a ~2.2% 10 year rate lock and I'll put on another 10-20% LTV in floating rate HELOC at 4-5% (prime plus a modest spread).

Thanks, and let me know if you have questions!

-

I'm wondering if anyone does analytics on the composition of ownership of a stock in detail. Specifically, by taking some inputs (13f/g's, daily weighted average volume, etc.) we can likely get a sense for what the weighted average entry price is for various owners of the stock. This can inform things like:

- is there likely to be tax loss selling?

- are folks "playing earnings" vs. more value oriented

Does anyone do this and find it useful? Are there data sources for it?

Thanks

-

On 7/5/2022 at 4:27 PM, fareastwarriors said:

im still working through it, albeit slowly.

I found lots of credit unions that will go to 80-90% total LTV. But most have a dollar cap or $4-600k. Many are lower.

I found a few “relationship banks” that seem willing to do lower LTV (65-75%) but at extrémale low cost levels (eg prime plus 10-25 bps).

-

On 5/20/2022 at 8:45 AM, CorpRaider said:

EDIT: Thanks for this discussion everyone (including OP whomst was dunked upon).

I deserved it! Thanks everyone! I’ll report back w what I end up doing

-

17 hours ago, Gregmal said:

Yea I second that. I just don’t find a HELOC attractive when you can/could just do a cash out refi into a new 30 year fixed. I proudly smashed the refi button on 4 properties last 18 months. Been laughing to the bank ever since. It’s almost too good to be true. Where else can you borrow 7 figures at 3.5%

Yeah I did this and my first mortgage is great. I just want standby capacity. Even at [5%] floating or whatever I like the ability to lock in borrowing capacity (vs draw right away).

-

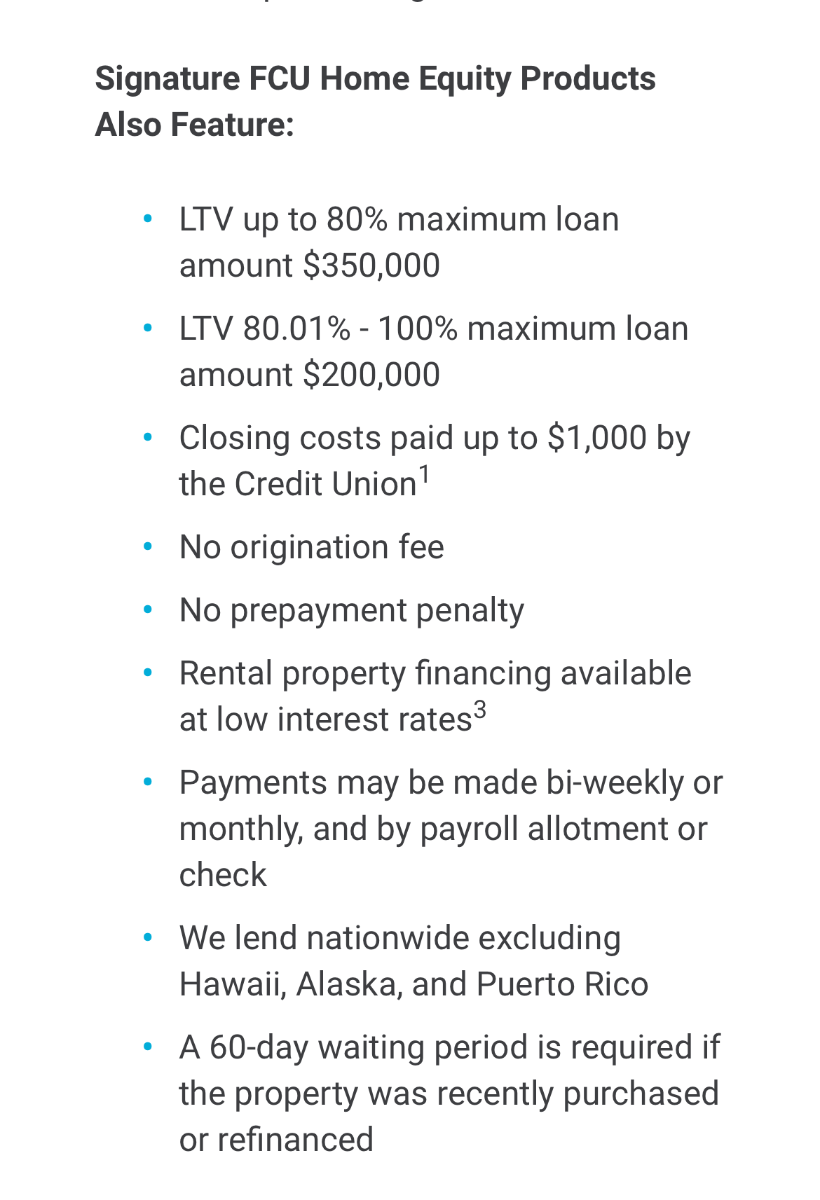

17 hours ago, thepupil said:

Signature federal credit union is aggressiBe on LTV I went to 97% LTV with them on a 2nd mortgage (but not a revolving HELOC) the rate was 5-6% though (I think 5.25%)

Thanks this is great!

-

3 hours ago, fareastwarriors said:

What's the question? You want to see what others are getting to compare?

Oops yeah that’s embarrassing. I pressed publish too soon! Yes, wondering if anyone has any lenders / tips that they’d recommend.

thanks!

-

Hey all! I live in the SF bay area and am looking to get a HELOC. When I've done that in the past I've observed the following:

- It's hard to get data, because online portals spam you

- I would like to get aggressive on LTV... I've found that different lenders are willing to be more aggressive on this sort of thing. E.g., in the past local credit unions have been best since they know the local markets

- Some banks have hard limits on $ of loan. I'm hoping to be on the upper end

Thanks all!

-

On 3/27/2022 at 8:34 AM, Gregmal said:

There’s a thread on it and the story is still pretty much the same. Just treading through the whole “time” aspect of the story. Q3 we should really start seeing some fun stuff. But elevator pitch is simple. You’ve got enough water to support a few good sized cities. $1.8b in “eventual” dollars. And the Sky Ranch project currently in phase 2 which should generate cash in excess of the current market cap over the next 5-7 years or so. As the homes get built the recurring revenue from water services grows. Oh yea, it’s all happening in one of the fastest growing MSAs which also happens to be facing a water shortage; Denver. Basically a JOE Jr.

Thanks Greg!

-

On 3/25/2022 at 1:09 PM, Gregmal said:

Yea you can tell someone is desperate so Ive just been hanging out and waiting for asks to come in. Under 12 been whacking 3,000-5,000 share lots all week.

Hey Greg- mind linking to a thesis if one’s handy? Been off the forum for a few months! Love forced selling…

-

7 hours ago, ERICOPOLY said:

You talked about things like leverage and free upside. Look, I'm not saying anything like that.

I'm just saying:

1). you are taking ONLY the downside of the diversified basket of 100 names (none of the upside)

2). you are taking ONLY the upside of the concentrated name (none of the downside).

Derivatives were created for swapping risk. I'm not saying anything unusual or surprising.

Thanks. That’s more clear to me.

-

On 1/9/2022 at 2:54 PM, ERICOPOLY said:

It's why buying ATM calls on 30% notional portfolio value make sense, funded by writing puts on 30% total portfolio notional across 100 other names if your risk tolerance is such that 0.3% position sizing in any one name is as large as you can tolerate.

Sigh...

Hey Eric- hoping to clarify what you mean here. Can you let me know if this is what you mean?

30% notional exposure in ATM calls....

- ...gives you the same exposure as if you'd invested in the underlying with 30% of total dollars, but puts less $ at risk

- ...Therefore ppl may be more likely to actually make a concentrated bet

- ...the downside is that you are time-bound and will have to roll the calls (increasing your basis) to keep the trade alive past expiry

30% writing puts...

- ...Funds the premium for the above calls

- ...Is equivalent to "limit orders" on a diversified basket of names at the strike

-... to clarify, are you contemplating these as ITM / ATM / OTM?

When combined...

- ... buying the calls, funded by puts, means you have 30% of the portfolio "reserved" in case the puts are exercised. In this sense the trade is leveraged to the upside but not to the downside

- ...you get "free" upside in the sense that if you were going to buy the positions that you wrote puts on anyway, you now get similar exposure to those names PLUS a rider on the call options

- ...you lose on the puts in two possible ways: 1) is if the underlying puts (assuming they are OTM) are never struck, so you never get the long exposure, and then those stocks go up. you'd therefore lose the upside, 2) if the puts are exercised and the stocks go down. (1) leaves you worse off than just getting a position in the underlying; (2) is equivalent to owning the underlying

- ...the calls main drawback is the duration. If you have to roll them to keep your exposure you suffer some frictional costs in maintaining the exposure. Over time this could erode returns

Did I get this right?

-

On 9/27/2021 at 8:32 PM, andomori said:

- Sharesight

- Wallmine

Thanks!

-

On 9/22/2021 at 3:33 AM, shhughes1116 said:

x2. I do the same in Excel.

Thanks! Any chance you’d be willing to share an anonymized version of the spreadsheet so I can look at the calcs?

-

On 9/17/2021 at 12:39 PM, rayfinkle said:

Hi everyone! I have a several brokerage accounts spread across several institutions. My goal is to see my returns over time across these accounts by various cuts. Ideally this includes:

1. Using a standard definition of returns that ideally aligns with how funds publish them;

2. Can show these returns across a few accounts / institutions (IB, Schwab, etc.)

Does anyone have tips on how to solve this? I know each institution has a view of performance for accounts within that institution. But I haven't found a way to look at this across institutions without downloading data to a spreadsheet and running somewhat complicated math that may or may not be the "right" definition of returns (accounting for inflows, outflows, etc.)

Thanks all!

Thanks!!! Will try

-

Hi everyone! I have a several brokerage accounts spread across several institutions. My goal is to see my returns over time across these accounts by various cuts. Ideally this includes:

1. Using a standard definition of returns that ideally aligns with how funds publish them;

2. Can show these returns across a few accounts / institutions (IB, Schwab, etc.)

Does anyone have tips on how to solve this? I know each institution has a view of performance for accounts within that institution. But I haven't found a way to look at this across institutions without downloading data to a spreadsheet and running somewhat complicated math that may or may not be the "right" definition of returns (accounting for inflows, outflows, etc.)

Thanks all!

-

Thanks- will check it!

-

Thanks- will check it!

-

Is anyone an expert on form 4 disclosures? I’m hoping to build on my basic understanding. Some specific questions:

- what is the best source for seeing which companies have buying or selling activity?

- how does one differentiate option exercises from outright purchases? I’m trying to understand when leaders put their own capital at risk at market price.

- with respect to the prior bullet it can be tricky since options can be exercised cashless or on a cash basis.

thanks so much!

Buying a company--lessons learned

in General Discussion

Posted

Super helpful. Thank you!