rpadebet

-

Posts

726 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Posts posted by rpadebet

-

-

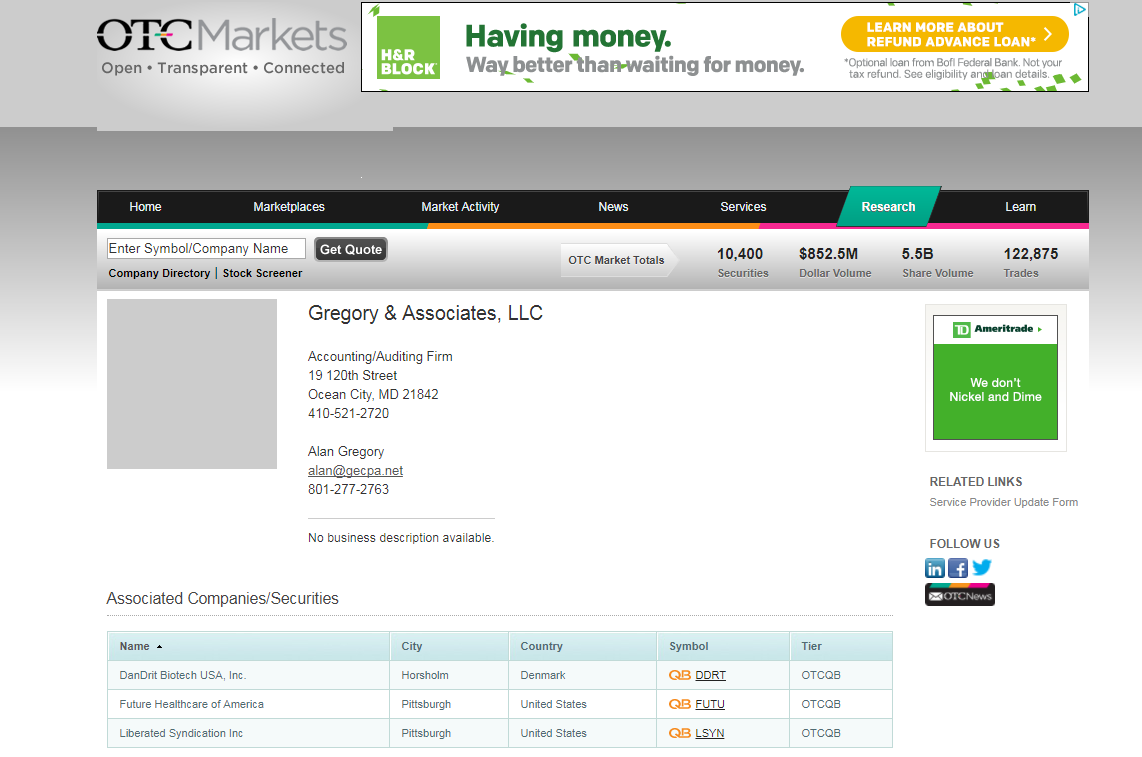

Pretty interesting that their filings refer to auditor in salt lake city

On OTC Markets website it is Ocean city, MD with same name, same phone number but different email id to the one in salt lake city or the one covering amnf. Did he just move? Does he maintain different email ids for different clients?

The PCAOB audits though indicate deficiencies with convertible debt accounting in 2015 and good will in 2011. Not much debt in AMNF (would be more concerned if there was some revenue recognition deficiency) - but I know this argument still doesn't kill the one cockroach theory. It just seems to me that they are an inexpensive auditor. Those audits also don't indicate presence of any other offices except for the ones in Salt Lake City.

-

Liberated Syndication (LSYN). Check them out - $40M unknown OTC traded company that is the leader in podcasting hosting. By hosting, I mean they earn a recurring monthly fee from every podcast on their platform (on top of a chunk of their advertising) for providing this service so people don't have to host on their own website and crash it. They have about 25%-30% market share from my best estimate so they have a real moat. Growing +20% a year, EBIT margins over 41%, and almost no capex so it is a FCF machine. Stock has sold off from $1.90 to $1.60 even AFTER they did an M&A deal beginning of this year that nearly doubles earnings and is super accretive. By my guess it trades at 5x - 7x FCF using very conservative assumptions. Check out the yahoo message board - there is more discussion on it there. (I might start a new message thread here about it actually).

The issue with them is they were spun out of FAB Universal, which ended up being a fraud. Other spin-offs from FAB have done terribly. LSYN still uses the same auditor that FAB used (Gregory & Associates, which is literally one guy in Utah). Almost all of G&A's clients have ended in bankruptcy or fraud. G&A has failed both of their PCAOB audits. The only semi-legitimate client G&A has ever had is AMNF. The cynic in me says clients use G&A for reasons other than auditor attention.

I also passed on LSYN at 40-ish cents so I may be biased now. I have no opinion on LSYN otherwise.

Auditor for LSYN might be a different G&A LLC than the G&A LLC auditor of AMNF.

LSYN guys seem to be from Ocean City, MD

AMNF guys seem to be from Salt Lake City, Utah

Where do you see Ocean City, MD? I'm pretty interested if there is another G&A or if they have a satellite office. That would be news to me.

I went off CIQ so they could be wrong but I just looked at the 10-k and it looks like the same G&A.

I looked at the OTC Markets website for both. They could be a satellite office or maybe the OTC site has it wrong

-

Liberated Syndication (LSYN). Check them out - $40M unknown OTC traded company that is the leader in podcasting hosting. By hosting, I mean they earn a recurring monthly fee from every podcast on their platform (on top of a chunk of their advertising) for providing this service so people don't have to host on their own website and crash it. They have about 25%-30% market share from my best estimate so they have a real moat. Growing +20% a year, EBIT margins over 41%, and almost no capex so it is a FCF machine. Stock has sold off from $1.90 to $1.60 even AFTER they did an M&A deal beginning of this year that nearly doubles earnings and is super accretive. By my guess it trades at 5x - 7x FCF using very conservative assumptions. Check out the yahoo message board - there is more discussion on it there. (I might start a new message thread here about it actually).

The issue with them is they were spun out of FAB Universal, which ended up being a fraud. Other spin-offs from FAB have done terribly. LSYN still uses the same auditor that FAB used (Gregory & Associates, which is literally one guy in Utah). Almost all of G&A's clients have ended in bankruptcy or fraud. G&A has failed both of their PCAOB audits. The only semi-legitimate client G&A has ever had is AMNF. The cynic in me says clients use G&A for reasons other than auditor attention.

I also passed on LSYN at 40-ish cents so I may be biased now. I have no opinion on LSYN otherwise.

Auditor for LSYN might be a different G&A LLC than the G&A LLC auditor of AMNF.

LSYN guys seem to be from Ocean City, MD

AMNF guys seem to be from Salt Lake City, Utah

-

Longleaf referred to two investments they made in Q4, 2017 which they did not name:

We purchased two undisclosed positions in the quarter.

One, like Mattel, was a time horizon arbitrage opportunity where past

mismanagement and a dividend cut obscured the longer term

value and prospects for industry-leading businesses.

The other was an example of how complexity often leads Southeastern

to investments. A more traditionally associated segment of the

company was under pressure industry-wide, taking the stock

to a multiple similar to peers within that segment. In the case

of this company, however, its most valuable segment consists

of leading, protected brands that are growing in strength and

demand.

I am not able to figure these out and hoping some enterprising board members might be able to fish them out.

Thanks

Vinod

Too tough, they didn't disclose much

1. business in turnaround...much more valuable if it turns around and that will take time------plenty of names

2. Sum of the parts > market price .... again many names which fit the bill depending on what value you ascribe to which part.

All they are saying is they are doing classic value investing....

-

If the tax cut works as expected which is to increase employment, wages and investment...it should be bad for stock holders. Seems like more of a Politics thread.

Why bad?

Increased employment->increased wages-> increased expenses/savings/investments -> increased revenues to corps -> higher top-line growth->higher stk prices at static P/S ratio?

It would be more interesting to see how the US population will choose to spend the "tax-savings" in the aggregate at this stage of the economic cycle. Growth investors can find value in those sectors/companies if they guess right. Given the continuous/durable nature of these tax cuts compared to some of the other temporary ones we had, at this stage of the cycle, I would guess people would spend on cars and such higher order durable goods. Lucky for value investors these also sport some of the lowest PE's with good operating leverage.

To the original point of the thread, there was a global rally in stocks last year. Did everyone think US tax cuts benefit companies everywhere?

-

If puts expire in the money, aren't you now exposing yourself to short term capital gains rate instead of the favorable long term rate at a time when your stock itself is down?

Some of the companies we buy stay undervalued for years but don't we hold those hoping undervaluation would be cured?

On the flip-side isn't it ok to have over-valuation persist for a while too?

Why not let some good luck offset some of our bad luck.

We are not all Malone genius. Investing is complex enough as it is without introducing this new tax dimension

-

Don't they do this every year?

I think it is a pretty good concert to get all the disparate small vendors, suppliers, associates into a room once a year and keep them motivated to continue to do business. Something similar happens in Omaha each year too I hear.

-

One other one I am considering is VIG. Yes, it has probably been mentioned already and investing in it will be like watching paint dry but nevertheless it is promising. I will lay out a quick thesis for my own notes if nothing else.

- Low expense ratio .1%.

- Companies with history of increasing dividend.

- Results in a list of stable high quality US companies.

- Neck and neck with S&P since inception, I think it is very marginally ahead but we'll call it a tie.

- Down 27% in 2008 vs 37% for S&P 500.

- Under-performed S&P for the past 2-3 years.

- Grantham has high quality US stocks as being one of the more promising stock areas in his 7 year forecast. Seem to recall there being another forecast with similar conclusion.

Yes VIG is a good ETF. I considered it. I liked the mutual fund VDIGX more though because it had 50 or so stocks in there. VIG has too many stocks to perform that different from a market cap index.

Looking for an ETF which is more like the Magic Formula based ETF with low expense ratio, handful of stocks and fundamental based weighting.

The idea being selection of companies and weighting in the index should be "price blind" as much as possible with the market price coming into the picture at the last possible step. An ETF which implements the Buffett-Graham-Dodd rules. Would also be interested in something which implements the Walter Schloss investing style

-

Take a look at QVAL here: www.alphaarchitect.com

They have a very unique tool http://tools.alphaarchitect.com/ "visual active share" that provides complete transparency as to what's really in the ETF you own. You'll need to sign up to access.

*Long QVAL

Thanks menlo.

I do like the QVAL approach somewhat. The approaches he mentions in his book seem to have a lot of outperformance. I need to dig deeper into this, but do you know whether this ETF tries to implement some of those ideas?

Most of the other alternatively weighted funds mentioned, seem to have too many securities in them for weighting to have an impact. The Davis funds seem to be a good candidate to explore but need to see whether it is a rule based selection or if there is a human touch

And regarding LEXCX, I think there is a certain amount of comfort in predictability of portfolio. Knowing what my fund holds and knowing that it won't change too much if I ignore it for a while is worth something.

By the way, would be interesting to know how many of you use ETF's in your portfolio and if so to what extent.

-

Guys,

I was trying to research and find some true value oriented ETF's out there which could potentially help me automate a portion of a my investing at a lower cost, for unrelated personal reasons. Do any of you have any experience with it or truly like anything that out there? If so what are they?

I am basically looking for ETF's which base their selection on fundamental non-price based qualitative factors and weigh the selections based on some proxy for potential payoff (difference between price and estimated intrinsic value). I am not too comfortable with market cap based approaches given their propensity for overweighting whatever is popular in a given period.

I am looking at a fund like LEXCX where the constituents were selected in the 1920's and not tinkered around with after except for mergers/acquisitions and spinoffs. That has beaten the SP500 comfortably over a long period of time. The idea was to find something like that today for the next 100 years. Want it in an ETF format because, I don't want to deal with forced dividends/taxes etc unless I really need to.

Any thoughts and help would be appreciated.

-

Desert_rat: The idea was to learn from investing mistakes of each other,

Not looking for a confirmation of a particular stock selection, definitely not looking for hugs.

Mistakes are not necessarily where you lost the most money on a stock, you could make money being lucky and it still can be a mistake (that's my example). So if you have made a mistake and have learnt something valuable from it, please share so it would be good for others to learn from your experience.

It is probably tough to think about mistakes in a roaring bull market when the tide is so high, but this is probably the better time to do so.

-

After a brief self imposed hiatus (due to various reasons) I thought I would re-join with a confession.

My worst investment mistake netted me a gain of 40% in less than 6 months. Before you guys think this is some display of false humility or disguised gloating, allow me a chance to explain:

In late summer of 2012, when I was a clueless "investor" (still suffering from it, but it was worse then), I bought a bunch of Facebook stock. Those days I hadn't read any of the value investing principles. Thought Buffet was just another Democrat who made a bunch of money in the market/business. Had suffered through losses in 2008 and hadn't learnt my lessons (not for lack of trying, but was reading the wrong stuff). Luckily for me, through my tryst with "observing" the market stress, I had developed a "feel" then for when things were stressed out enough. So after the FB IPO when investors were dumping the stock for fear of user growth saturation and no mobile strategy, I made a ballsy bet by buying FB @$19.

Then in the fall of 2012- early 2013, in my search for better investing principles, I found religion (this religion of Value Investing). I read a bunch of stuff, all over the place, but hadn't discovered the BRK letters yet. I read about deep value investing on how one buys assets and not earnings. How one is supposed to invest in at a discount to book value. This stuff made sense to the naive me at that point.(After all how could one go wrong buying 1$ for 50 cents? duh!)

I started investing in value based mutual funds, to observe the professionals in action. I kept reading but didn't read the BRK letters yet. Something strange happened and I started worrying about my FB stock. I hadn't applied Value Investing principles and selected it more out of a "gut feel", what if I was wrong? So by April when I was almost sure FB didn't fit into Value Investing philosophy I immediately sold all the stock @$27. I told myself, wow, I got lucky with a 40% return in under 6 months, especially when I had no clue what I was doing.

I later made a lot of Value investing bets like AIG, MBI, MSFT etc where I made decent returns and i knew (at least i thought I knew) why I was making money. I met a bunch of big losers too like BBRY, CTCM, ARTW (this list is long). I did VRX too (made a bunch on way up and lost most of the gains on the way down, from about the same buy price point interestingly :)). All these losses though taught me something valuable about the risks I hadn't considered.(when you lose money, you gain experience as WEB recently said in his letter! that is indeed true for me).

What the early value investor in me had missed was taking into account melting ice cubes and giving secular growth enough credit. It is dangerous to your health to have half-assed knowledge and interpret the religious teachings narrowly, especially when you don't have the discipline of the great gurus. Percentage wise I think I lost more on VRX on the way down. But I still consider FB my worst mistake.

It is one of those things, not error of commission or omission, somewhere in between. Was lucky enough to buy it, didn't have the intellect to do nothing and hold it. As you guys know that particular stock is up 5x from my sell point and more than 6x from my buy point. I haven't had 5 baggers, but this could have been it.... in just 4 years! Alas... (also read as "a loss" which I haven't suffered in any other stock....yet)

Just wanted to share this after reading WEB's take on, a person with experience meeting a person with money, in his latest letter. Sometimes something looking good on paper might indeed be your biggest mistake as it could have been great! Never assume you understand any religion because you have read it once. Reading once again might give you a different insight, if you still have a teachable mind.

Would be interesting to hear the worst investing mistakes from others on the board and their learnings from it. (only one mistake could be your WORST!)

PS:

Recently after lot of gut wrenching, stomach churning and fighting my inner demons, I decided to atone for my past sin and made a purchase decision again on FB @$120. Yes this was a very tough decision. The market didn't give me the value it once gave, but there was a small sell off given growth uncertainty and I could convince the still alive market timer in me to go for it. The market might as well be right this time, but I am hoping to beat it by holding it for long and wearing it down! Might not be a 5 bagger anytime soon, just hoping for decent returns this time. Let see...

-

How about paying these rating agencies differently?

Why not pay them using the bonds they rate? And force them to hold those bonds until maturity or at least a fixed period of time.

That should align their incentives with the buyers right? They certainly would have been more careful with aaa ratings on some CDOs

-

Great thread, thanks.

My mistakes are too numerous and tedious to list.

One kind of mistake is when I make analytical errors. I think something will happen, but the opposite happens. To me these are honest mistakes. To be able to not make them tomorrow, I have to make them today, so I can reflect and learn. I will be forever making them, but hopefully less.

Another kind of mistake is I pretend to know something when I don't. This is where the gurus sometimes come in and trap me. I look at a potential investment, which looks appealing although I am not sure. But I will invest anyway because some gurus have it. Of course it's never the gurus' fault. It's 100% my own.

To ensure I only invest in something I think I understand, increasingly I feel my job is not to expand my circle of competence, but to narrow it. To know everything is just impossible.

+1

But it is enjoyable to try and expand the circle no?

-

Wow, where do I begin...

I will probably wait until everyone is done and just summarize... I think I have committed most of the above sins.

I just was lucky to avoid the oil and gas names because I felt lazy to study up and try to bring that industry into my "circle of competence".

I keep telling myself not to invest in anything but a simple layup, but keep getting attracted to complex(intelligent sounding?) situations. Need to keep working on this.

-

How valuable is this float with negative interest rates around the globe? Clearly Japan and Europe seem to want a float of their own ;)

-

I loved this rant, completely agree! Cash is king.

To pile on:

-We are putting a roof on a house we own. The contractor quoted us a check price and a cash price. The cash price was a few hundred dollars lower. Why? Because he could pay the truck driver and materials on the spot and doesn't need to rely on suppler credit. He said for the lack of hassle and cost savings he passes it straight on. I happily paid cash.

Or perhaps he simply prefers to have a few cash sales because there's no traceable documentation which could trip him up when he fails to report the revenue from that job to the IRS. It's a nice little boon to his financial situation to charge you $5k to do your roof, not report the revenue and then apply the $3k of costs (for which he will certainly have documentation) against the revenue that he must declare from the clients who do pay him by cheque.

But at least the explanation that he provided to you is less sleazy than the simpler alternative.

Seriously, this is the correct reason. Supplier credit? Give me a break, that's being naive. He's worked with that same truck driver for months/years. He says listen, I'll pay you when I get paid. Either do the job and get paid after I get paid, or don't do the job and don't get paid at all. The truck driver knows that. And he's buying materials out of pocket from Home Depot, whether you pay him by cash or check. He's giving you a break on cash because it causes him less of a headache with taxes and dealing with cash flow. This guy is a contractor who would rather be on his couch than your roof. He looks you over once, and figures really quickly how much of a break he needs to give u to cough up in cash. I'm guessing on a 5K job it's about $200 bucks. $300 if you endeared yourself to him and asked about his family and shared a cigarette and beer with him. Supplier credit? C'mon now.

+1 ;D

The only supplier credit he is sharing is a small portion of the taxes he is avoiding by getting paid in cash.

Most likely he hasn't even heard of the term "supplier credit"

-

IBKR - had been eyeing this for couple of years now, finally felt the price was in my zone.

-

Powerball: a progressive tax on ignorance; the more you have, the more you pay.

But the expected winnings of a $2 ticket is now greater than $2 right? It is therefore a rationale thing to play it tonight

No. Using the Kelly criterion, the optimal bet would have been 1.2 x 10^-8 % of your bankroll on the lottery ticket (without considering splitting). That would have been one $2 ticket if you're worth $17.5 Billion.

I actually read it as....if the pot is worth $17.5 billion then it makes sense to invest the $2. I will wait until the price is right... :)

-

I'm trying to expand my skillset from pure fundamental analysis, and have initiated a very small short position in the Euro to play around and see what I can learn.

I thought your results as an investor have been quite good until now… Why do you want to change something that has worked very well so far?

Cheers,

Gio

Maybe because macro forecasting is fun even when you are wrong. Everyone should be allowed some entertainment

-

3) Just a reminder: stocks got cheaper, not more expensive.

Oh, but noes, there's Elliot wave reversal and the core of the Earth stopped spinning ( http://www.imdb.com/title/tt0298814/?ref_=nv_sr_1 ) and there's an Arquillian Battle Cruiser ready to attack ( http://www.imdb.com/title/tt0119654/?ref_=nv_sr_3 ), gotta go, sell everything.

I am not selling. There is no Hindenburg omen or sighting of Halley's comet yet.

-

There are much higher returns in purchasing, owning, operating private businesses than investing in the stock market. The main surprise to me when attending Berkshire and Fairfax meetings is how many people just want to talk about stock market investing as opposed to owning and operating actual businesses outright.

Not sure if it is laziness, ignorance, hubris or fear but never understood why more value investors don't practice the value investing and management principles in investing and operating private businesses.

Easier to sit in front of a computer and buy/sell stocks and let others do the work for you...

Can I personally run a business like Malone can? Most definitely not...so I invest with him through a couple of clicks and then spend my time learning from what he does.

-

I would rather index the SP500 at the lowest cost possible if I feel I am unable to be mentally functional. I will be happy beating 90% of the managers over the long term doing nothing.

Problem with finding fund managers is even if you are able to spot the extremely good ones and even if they beat the market consistently, unless u can buy life insurance on them, there is no guarantee you would get what you hoped for.

Problem with investing in a fixed set of high quality stocks is, even if you are able to spot the really long term compounders with good moats, unless u can buy CDS on them, you can never be sure whether they will survive. You can never be too sure whether someday a good enough fool might run the business and destroy the moat.

SP500 will survive until we have a functioning stock market.

I guess this is why even WEB suggests this strategy for his estate plan.

-

As others will invariable line up for the Star Wars movie next week, I lined up to watch the first show of The Big Short in NYC today. ;). Luckily the line wasn't that big, in fact just a couple of guys ahead of me.

As is the case with such movies, I found the book more interesting, but the movie was not bad. They even managed to make it a bit funny.

I have special memories of this historic event because I was just starting my career and unbeknownst to me at the time, I had a very close ring side view as important events unfolded. I consider myself very fortunate to do a mini internship at the time with Greg Lippmann and his team. I observed the presentation (which is now being circulated) being put together, arguments between Lippmann and Eugene Xu - the Quant (This part is not in the book ). I remember being clueless at the desk as the lowly intern while the bosses left for the now infamous Las Vegas conference. So this book and the movie hold a special significance in my mind and it will be an experience I will never forget.

Now you know why I lined up for the movie on the first day.

Anyway after watching the movie, I started reading Dr. Burry's letters from the time again, here is an excerpt that I found interesting

While many see a commodities bubble, I see a federal mandate to inflate commodities

prices in dollar terms. The recent collapse in some commodities prices along with a

strengthening dollar does little to dampen my enthusiasm for the sector. I fully expect

such volatility along the way; that is the nature of the markets. In fact, the Funds

established direct commodity exposure through futures contracts during the recent

pullback. At recent prices, the total value of futures contracts amounted to less than 15%

of the Funds assets.

It is an entirely reasonable argument to note that as the world slows down, other countries

will start cutting rates, making the dollar relatively more appealing. As commodities have

been the prime beneficiaries of a weak dollar, this improving state of the dollar would

result in poor performance for commodities going forward. However, we must remember

that the United States is the largest economy by far, and it has the most leveraged

consumers by far. The primary cause of the rest of the world’s ills will be secondary

effects of the slowdown in the United States. Every other country will have some degree

of strength derived from domestic and other non-US sources. At the end of the day, the

credit crunch hurts the United States more than any other country. The sickest patient will

require the most aid, and I would expect that aid will come in the form of Federal policies

that hurt the dollar’s value over a longer time frame.

I just realized, he seems to have even predicted the emerging market contagion, dollar strengthening and related commodity complex collapse which we are currently seeing...he goes on to predict a follow up recession and further fed support (FWIW I didn't predict any of the above but I do believe QE4 is coming soon 8) )

I am now really in awe of this man's rational/logical thinking....it is a bit scary even to think, what it would be to think like him and know what he knew would be a reasonable probability back in 2008.

If I had a chance, I don't think I would like to talk to him. It is a bit like looking through the crystal ball and knowing your future. It takes all the fun out of living and investing!

beating the market - not what it used to be

in General Discussion

Posted

We need to differentiate a bit here between outcome and process:

Beating the market is an outcome.

This game is far more enjoyable if the focus is on efficient capital allocation i.e. if you enjoy understanding businesses, their competitive dynamics, the environments they operate in, how they generate revenue, how they spend and how they invest, it is far more fun in my own opinion. This is true irrespective of the market conditions and price where it is trading at.

As investors we are only serving as cogs in that wheel trying to move money to the best utilizers of capital given prevailing prices. If we keep doing it right, eventually we might beat the market, as good capital allocations must necessarily triumph over bad allocation. Hopefully we are not doing it only to beat the market, that would just make us keep staring at the scoreboard.

Agree with Schwab in that the game seems to be as hard as it ever was. The tools have changed, but everyone has access to similar tools.