randallchsu

-

Posts

42 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Posts posted by randallchsu

-

-

Looks like we are trying to jump over a 7-foot bars

-

I think the allowed Perry claims largely only benefit the preferred. @cherzeca, correct me if I'm wrong.

The Takings claims, however, benefit both preferred and common. Considering that Ginsburg flipped a way I wasn't expecting, though, I think Bayes Theorem indicates that my analysis of the likelihood of success in the Takings case is probably worth bupkis.

I really don't 100% understand the reaction in the preferreds. Perhaps it's because many news articles indicate that the legal avenue is foreclosed, but that oddly leaves out the fact that the Perry case said both the breach of implied covenant & breach of contract cases can go forward.

Could it be because people are unsure how the class plaintiffs could be subdivided and lengthen the process that could take on?

From the opinion

"For those who purchased their shares after the enactment of the Recovery Act and the FHFA’s appointment as conservator, the analysis should consider, inter alia, (1) Section 4617(b)(2)(J)(ii) (authorizing the FHFA to act “in the best interests of the [Companies] or the Agency”), (2) Provision 5.1 of the Stock Agreements, J.A. 2451, 2465 (permitting the Companies to declare dividends and make other distributions only with Treasury’s consent), and (3) pertinent statements by the FHFA, e.g., J.A. 217 ¶8, referencing Statement of FHFA Director James B. Lockhart at News Conference Announcing Conservatorship of Fannie Mae and Freddie Mac (Sept. 7, 2008) (The “FHFA has placed Fannie Mae and Freddie Mac into conservatorship. That is a statutory process designed to stabilize a troubled institution with the objective of returning the entities to normal business operations. FHFA will act as the conservator to operate the Enterprises until they are stabilized.”)."

-

It seems like the original question bears similarity to "What is in Thomas Russo's portfolio?"

-

Looking to compile a list of businesses that can withstand time and continue to compound.

I will start with a few in China, looking for more inputs to complete a list of businesses around the globe that can run by idiots.

- Maotai, 600519.cn

- Golden Throat, 06896.hk

Edit: I added a spreadsheet based on replies.

https://docs.google.com/spreadsheets/d/1gVLx7tgbQjJOC8PdR90ve89Rnb8Xt49uK7wcMrBkAcM/edit#gid=0

-

What's the take on Mr. Carney's latest article?

-

Where is a complete list of funds under the category of select value manager holdings? I didn't find it in the prospectus.

-

Thank you for your reply. This question is not targeted for CSU, but is asking if this metric is a good way to apply to other asset light businesses. Accepting this approach seems like higher valuation can be justified, making the two birds in the bush that much more attractive than the one in hand.

So from what you are suggesting, this would be a pretty unique way to look at CSU and less so with other businesses?

-

From Constellation Software Inc. shareholder letter:

"Obviously, when you divide Adjusted Net Income by Invested Capital, you get a measure of the return on our shareholders’ investment (i.e. ROIC). If you add Organic Net Revenue Growth to ROIC, you get what we believe is a proxy for the annual increase in Shareholders’ value. In a capital intensive business you couldn’t just add Organic Net Revenue Growth to ROIC, because growing revenues would require incremental Invested Capital. In our businesses we can nearly always grow revenues organically without incremental capital."

Why adding organic net revenue growth to ROIC in an asset light business made sense? Also, how do you determine organic net revenue without management telling you the number?

-

What about buying put options on TIP related ETFs. However, the longest expiration date is usually less than one year.

http://blogs.wsj.com/wallet/2008/12/12/how-deflation-would-affect-tips-and-i-bonds/

-

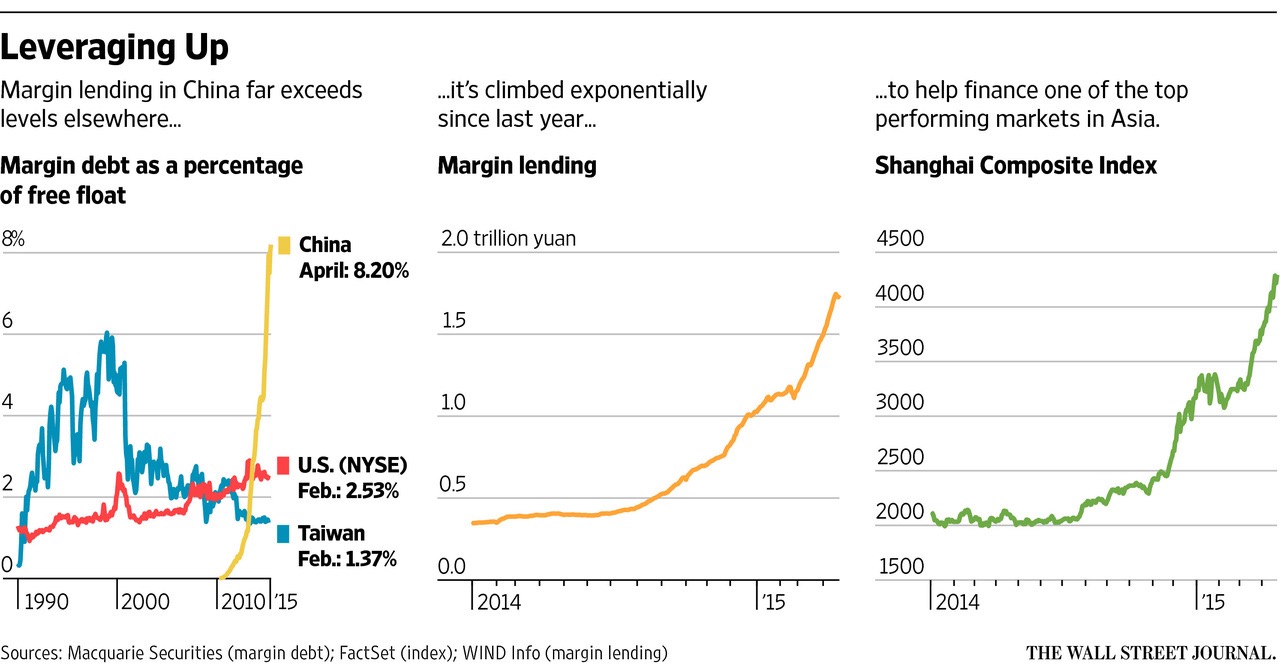

I think this gives a little bit explanation to the recent run ups in Chinese publicly traded stocks.

"Margin trading had been piloted in (China) in 2010 and then fully implemented in October 2011. Brokerages, sensing more revenue opportunities, were more than happy to provide margin-trading accounts. Investors, who had largely never experienced margin before, lapped it up as margin lending grew."

"Research by Macquarie Securities Group shows China’s margin-debt ratio at 8.2% of the free float. That easily exceeds the peak of 6% reached in the late 1990s in Taiwan, the second-highest level globally in recent years."

"Trading funded by margin loans accounts for 25% of daily volume on the ChiNext, the market in Shenzhen where Chinese startups trade, according to estimates from UBS AG."

http://si.wsj.net/public/resources/images/AM-BI665_CMARGI_16U_20150422053020.jpg

Link - http://www.wsj.com/articles/debt-builds-in-china-stock-rally-1429785899

Link - http://knowledge.insead.edu/blog/insead-blog/margin-call-on-overleveraged-china-3808

-

Touches on Munger's idea of lattice-work of models, spreadsheet vs. logic/reasoning, human decision making etc.

-

I complied a list of TARP warrants that got auctioned off by Treasury on Seeking Alpha last year, hope you find it useful.

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

in General Discussion

Posted

How big is John Paulson's position in fannie and freddie preferred shares?