TwoCitiesCapital

-

Posts

5,004 -

Joined

-

Last visited

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by TwoCitiesCapital

-

I don't mind them assuming the insurance biz is commoditized. We know it isn't true and that good underwriting is what makes this business model work, but we could give him that since it is for many others. But not paying any attention to the historical track record of the investment portfolio? Of the earnings it's managed to spit off during the 2-3 years this guy has been critical of them? Fairfax's market cap at the end of 2021 was somewhere in the ballpark of $10-12B. They've earned nearly $12B in headline earnings (not including balance sheet items and gains) over the last 4 fiscal years and much of that wasn't the insurance biz.

-

I have had the CFA charter for nearly a decade at this point and nearly ~15 years involved with the program if you consider the studying and time up to the requisite work experience. Professionally, it was a no brainer. I went to school in Mississippi and then moved to NYC. I'm 100% certain the only reason anyone even looked at me was having passed the 1st level. As a matter of fact, I didn't get a single call back for interviews UNTIL a few days after adding it to my resume when I got the results. If you don't go to a target school, CFA is probably one of the few ways to get noticed and distinguish yourself. That being said, none of the roles I had in NYC required it and I was often the only one with it. Nobody really cares about it beyond it getting my foot in the door. It was just something to give me pedigree that was lacking in my school choice. The MBA from a top school was the be-all end-all when I was in NYC ~7-10 years ago. Where I'm at now in the Midwest, nobody really cares about MBAs. The CFA is everything and several roles require it or progress towards it. Outside of introductions to more esoteric products like derivatives/futures/interest rates theories and etc, I don't think it's helped a ton in my personal money management. But professionally it was worthwhile and has given me opportunities and wages I wouldn't have otherwise been eligible for. I also enjoy the events put on my by my local society, it's been great for networking, and my employer pays my dues. So its really great from my perspective.

-

What a joke - the mental acrobats to avoid admitting he was wrong is insane. Earnings will normalize. There will be lower rates in the future and more catastrophes. And FFH will have fewer shares, more retained earnings, and additional growth through its associates to make up for it. Not to mention today's value is still probably fair in that environment even if it doesn't happen like that. If this man actually put a pen to paper, he could work this out for himself.

-

Hard to measure an ROI on something that basically has no upfront cost, but ongoing cash draws. In Fairfax case, it's basically infinite because it's only been up since they opened it.

-

The # of ADRs are fixed and the # of shares backing them are fixed so the ratio remains constant, but ADRs CAN trade at wide premiums or discounts to the underlying security of the issuing bank isn't engaging in the creation/redemption of the ADRs units so that the different can be arbitraged. I'm not 100% sure what drives whether the banks are engaged in issuing/destroying ADR units, but there are ADRs that do trade at premiums/discounts in periods where the sponsoring bank closes that ability to arbitrage. Please don't make me hate FFH with this thesis. Right? It finally seems like the stock is actually responsive to earnings announcements now! A few hundred million tacked onto Q4 earnings as a result a la the TRS. Brilliant! He might have been the one pushing it up today trying to exit? Though he should've exited as soon as it was clear his thesis on the aggressive accounting was bunk when Digit IPOd...

-

I feel similar watching Elon Musk over the last 18 months...definitely seems to be taking after his father. I suppose you have to have some eccentricities and a willingness/ability to be different to achieve the level of success these guys have...but when that starts bleeding out of business success and into personal turmoil it really is sad.

-

I didn't sell in the past few quarters, but sold a small portion of my position in 2023 to keep it below the position limits of 10% of networth that I set for myself. Now that Bitcoin, and other, names have performed fairly well in late-2023/2024, I have been able to hold onto shares this year and may actually be able to add in the next pullback. Isn't necessarily optimal - but the rules were set for a reason and am being diligent about following them.

-

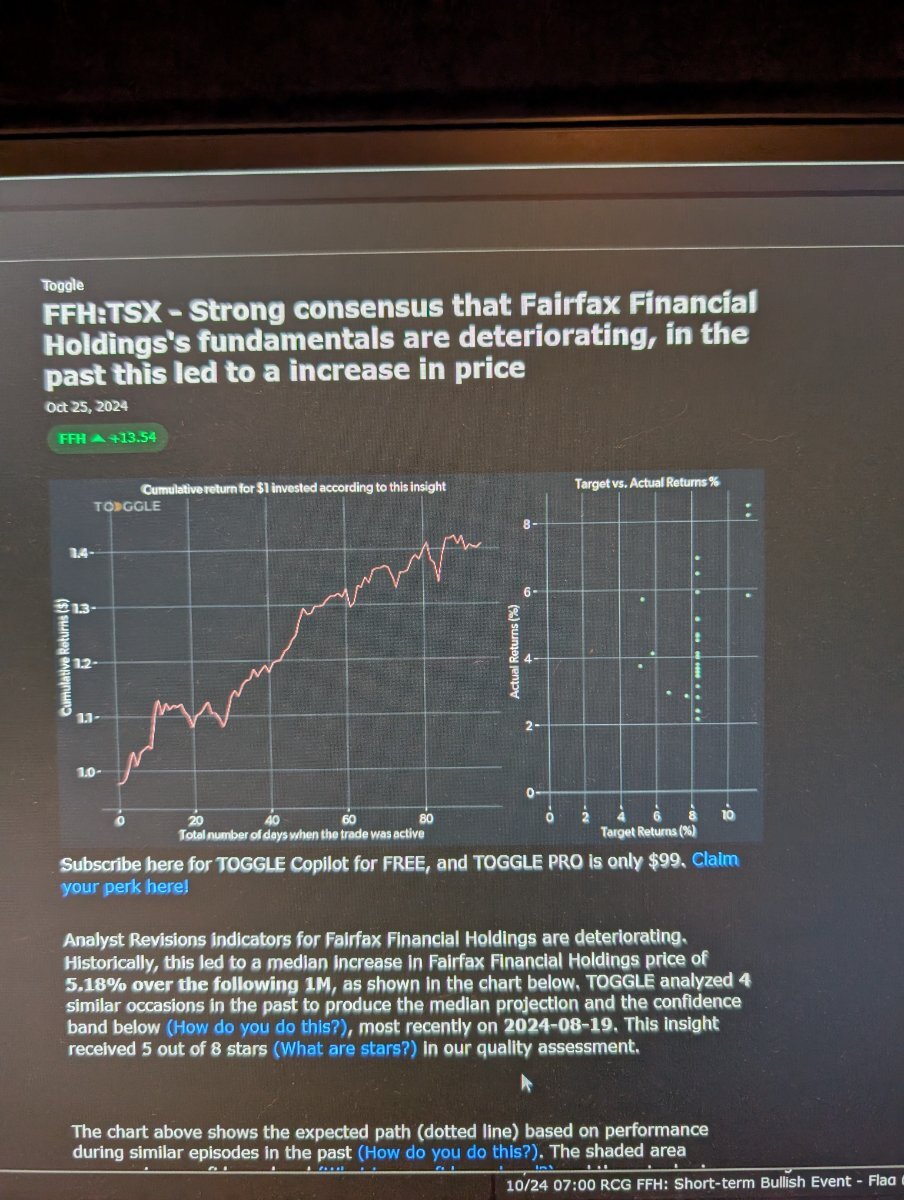

Lol Is it the deteriorating fundamentals OR Q3 earnings that is gonna propel this higher?

-

Also - I don't know exactly where my shift occurred - I used to view BTC as a p2p payments network and believed that for probably the first ~2-3 years I was buying it. My attempt at valuing it? Take the EV of Visa/MasterCard/AmEx/Paypal/Discover and dividend by 21 million coins (a figure in excess of $70k per coin today btw). Some where along the way, I think it clicked for me that it IS a payment network, but the real value is in its monetization as provably the hardest asset in existence by enforced scarcity. Then it started to make sense to me as a store of value as well. I still think its value is based on its p2p network size and capabilities - but there WILL be a monetary premium attached and the price of 1 BTC is probably going to a level that would be "silly" by any other means/method of valuation simply due to how arbitrary the price is when you can subdivide it into 100 million and it becomes the global money of choice after decades of politicians wrecking money globally.

-

Maybe I have misunderstood Gresham's law, but we can see in throughout history that when a society's money is soft and inflated, flows move OUT of the inflated money to a newer harder money. Lyn Alden covers many examples of historical monies being exploited for their lack of hardness, but ultimately this is how most societies eventually landed on gold through a trial and error process of monies being exploited and new alternatives tried. So how do countries that gravitate towards a gold standard accumulate gold when they have none to start with? Well, by saving any gold they can get their hands on and spending any other type of currency away. This is what I thought the application of Gresham's law was, but perhaps I am mistaken about its application and this is described by something else. Either way, when something is being adopted as a money, early adopters get rewarded as the monetary premium goes from negligible to enormous. No rational person would spend the money that has the growing monetary premium to hold onto the one with the falling monetary premium. I agree that at the moment - Bitcoin on-chain/self custody is probably beyond most people. I don't think that will matter much. Just as transportation of gold, and securing gold, were beyond most people which is why we started custodial banking relationships. Services will pop up to assist individuals in safely and securely managing their Bitcoin wallets and transactions. I expect that retail interaction with the base-chain to be limited in 5-10 years. Perhaps in buying a house or a car you'll touch it. Beyond that, I think it will largely be reserved for large settlements between banks, nations, and corporations and retail will largely exist on level 2 and level 3 arrangements above that much like we all use digital checking products and credit cards without ever having touched or seen the physical cash

-

Agreed - for now. Gresham's law is people spend bad money before they spend the good money. Most people acquiring BTC have no incentive to spend it when they have plenty of fiat to spend in its stead. Once BTC becomes the standard, that will no longer be the case

-

Despite diminishing BTC per block, the current value of the rewards being given is still quite large given that the price appreciation has more than kept up with the absolute block reduction. This will not ALWAYS be the case, but it doesn't appear to be stopping before we reach mainstream adoption/use which still seems to be 5-10 years out. As we get closer to that point, and through another halving or two, we can then make more educated guesses about the state of block rewards (are they still sufficient) or will fees have to be raised (also a possibility). Regardless - I still expect large counterparties to want absolute settlement and will pay fees to get it done - fees that are likely to still be quite a bit less than the current system with all of the intermediaries taking cuts to achieve an acceptable ROE for their owners. Will that be banks settling payments cross borders? Central Banks settling balances with their member banks? Card processors settling large blocks with retailers like Walmart/Target? Someone selling their house for 1 BTC? Any number of scenarios could exist where you would want final settlement on the blockchain AND would still be willing to pay $10 or $100 or $1000 to get it done in a manner that is more permanent and still cheaper than these methods exist today.

-

Agreed! I own it heavily (~20% of my net worth) and will keep DCA'ing regardless of who wins. It'd be nice to have political support, but I don't expect it and am actually skeptical of most politicians who are offering the olive branch as its decentralized nature seems to suggest that opposition is the default for those who seek to consolidate power and influence to themselves (i.e. politicians). But I just think it's shocking how many people are willing to ignore what Trump actually did his first 4 years to pretend his next 4 will look wildly different - for Bitcoin/the debt, for Fannie Freddie, for merger/arbs, etc.

-

I don't want to believe it, but would be consistent with my every experience within the legal system so far. The system is broken and only "works" because people believe it works - not because it actually does. The US government getting away with stealing these entities has to be an outcome assigned a fairly significant probability now that the courts have refused to enforce reasonable applications of property rights

-

https://www.wsj.com/finance/currencies/federal-investigators-probe-cryptocurrency-firm-tether-a13804e5?mod=hp_lead_pos2 Tether back under scrutiny.

-

Did they actively score against themselves, refuse to play, or give up on every snap while claiming to want to win? That would be a more apt comparison. Trump could have run a balanced budget or at least moved the budget in that direction. He didn't. He expanded spending and cut taxes to run the largest peace time, non-recession deficits we've ever seen. He is a self described "debt guy" who has presided over many personal/business bankruptcies himself and suddenly I'm supposed to believe this guy has found fiscal religion? As far as Fannie and Freddie - he did do stuff. He milked them for the 4 years he was in office and then he hamstrung his opponents from being able to do the same. He could have dropped the suits. He could have negotiated their release instead. He could have let them keep their profits during his 4-years. He didn't. He milked them and then continued the status quo all while calling his opponents criminals for doing the same. Actions speak 1000x louder than words. I find if you ignore what politicians say, and watch what they do, you probably have a better idea of what they're about. Because most things he says are patently false? Like many other politicians? He has DONE nothing to support this thesis. I don't care what he says - his ACTIONS have been the polar opposite. Anything he says right now is basically pandering for votes. Once he's in office, there is no reason to expect it will be any different than the last time he was there.

-

Perhaps. As mentioned, I don't really know what the reason is. Their preference for payment isn't my business and they didn't force me to pay cash. Just offered an incentive to do so. 20 years ago, paying in cash would have been the norm and internet banking weird. Now, internet banking is relatively normal and paying in cash is seen as weird or underhanded.

-

"Instant" bank transfer doesn't really exist. ACH still typically takes 2-3 business days to move and be credited while wires cost way more the $1.38 and take longer than 5 minutes. Is this ok in many instances? Sure. But for the times where 2-3 days is unacceptable, BTC is better and cheaper than a wire. As for why we couldn't do ACH, or wire, or personal check, or money order, or etc - my primary guess is because they don't want to declare it for income tax purposes. But I can't say for certain and there could be other reasons for their preference. Cash is legal tender. They're asking to be paid in cash. It shouldn't be difficult to do, but it is.

-

The first time around he was surrounded by Mnuchin, Paulson, Calabria, and many others who wanted to privatize Fannie. It didn't happen. I'm not saying it won't - I'm just saying you all seem to be giving him an awful lot of credit and holding onto a lot of hope for crypto and Fannie Mae for somebody who doesn't have a demonstrated history of really caring or doing anything about either.

-

I think his incentives are to do whatever is best for himself. He's said it before - he's a debt guy. I don't think he actually cares about the debt. His actions last time around support that thesis. What I'd need to see is something to support the idea that he's suddenly done a 180 on that. Maybe I do. I underestimated his ability to get elected the first time and under estimated his ability to push through tax cuts. But he also did little-to-nothing for Fannie Mae other than to hamstring the other party from pillaging them after he did for 4 years. I could be wrong - but simply looking at what he did the first time around SHOUDL give us a sense of what his policies/views/thoughts will be the second time around....unless if there's reason to believe he's changed.

-

This will surprise absolutely NONE of the BTC community, but another anecdote: My contractors doing framing/drywall in my condo offered a $4k deduction in price if I paid in cash. I bank w/ USAA so there are no branches meaning I have to use ATMs to get the cash. But most ATMs have daily withdrawal limits of $200 - $800 meaning it was going to be dozens of trips/transactions/ATM visits to get the $12k I needed for the downpayment. I walked all over my downtown area cataloguing ATM maximums and their fees (basically requires you to go through whole withdrawal process just to cancel at the end to get the info you need). It took hours to find an ATM with a maximum withdrawal above $1,000 and even then it had insufficient bills for me to reach its maximum when I tried to withdraw it. It took hours of effort to identify the best ATMs and 4 visits over multiple days along with $12-15 in fees to get the $12k I needed. I will have to do this again 2 more times as project milestones are passed and new monies are due. Anyone who banks online will have similar issues trying to get cash in excess of $2k for any reason. In the meantime, I just sent $10k of Bitcoin in less than 5 minutes for about $1.83 in transaction fees. Would be 1000% better if my contractors took Bitcoin instead of cash.

-

It seemed like your point was to suggest that Donald Trump is interested in supporting crypto in one way, shape, or form as a response to the growing debt? I simply pointed out there were many options he could've taken to address the debt when he was previously president - or did the exact opposite. Thus, I am skeptical Donald Trump cares about the debt at all and even more skeptical that he views BTC as a path towards a more sound money solution in addressing the debt.

-

What Trump could've done about the debt was to NOT provide massive tax exemptions for those who owned real estate or to run the largest peace time deficits we'd ever seen pre-Covid. Trump can pay lip service to doing something about the debt, but when he had the power to do something about it, all he managed was the status quo of making it worse. I wouldn't expect anything different from a second term.

-

Japan is absolutely having trouble. GDP growth has been minimal and its currency has dropped by 40-50% against the USD in the last 5-years. That is more akin to EM currency risk than a "flight to safety" asset that it has historically been characterized as.

-

Japan and Europe are both worse off and not THE reserve currency. Neither has really gone through a existential doom-loop yet. That isn't to say they wont, but I doubt the US goes first.