Thrifty3000

-

Posts

637 -

Joined

-

Last visited

-

Days Won

5

Content Type

Profiles

Forums

Events

Everything posted by Thrifty3000

-

Busch league. It barely qualifies as a short thesis. Even if MW's claims are valid, what's the downside? A $20 million regulatory slap on the wrist, where FFH neither admits nor denies wrongdoing? One of the best investments I ever made was in Jefferies during their 2011 short attack. At least the Jefferies attack was existential. The MW attack on FFH is just toothless noise. A comparison to Jack Welch's GE (and GE Capital) is just silly. #buyingOpportunity

-

Pre-COVID I had about a third of my portfolio in an all-world (ex US) ETF. The only other ETF I’ve ever owned has been S&P 500. Currently, I don’t own a meaningful amount of ETFs or mutual funds. Right now I prefer individual equities and cash over broad indexes. I basically look at the S&P 500 index as risk free over the long term. I assume it will compound at 6 or 7%. So, since I consider it risk free I usually won’t invest in an individual company unless I’m confident the investment will outperform the S&P 500 by at LEAST double. In other words if I don’t think I can earn at least 14% on an individual company I’d prefer to own an index. (However, if cash is yielding 5% I’ll take the cash.) These days if I sell stock I’m parking proceeds in cash, which is about 10% of my portfolio.

-

That will be up to the board of directors, and will probably be based on overall performance against the S&P 500 over rolling five year periods. Greg has been reporting to Buffett and the board on company results and his initiatives for several years now. So the board should have a good level of confidence by now on his grasp of the overall machine. I have a hunch Todd is being groomed to succeed Greg. By the time he takes the reins I think he’ll be about as good of a fit as investors could hope for - sans the personality.

-

So, for this simple look through earnings spreadsheet the most important fields I track are: Ticker # of Shares I Own Per Share Cost Basis Normalized Earnings Estimate Per Share Normalized Dividend Per Share Total Cost Basis (Cost Basis Per Share X # of Shares Owned) Total Normalized Earnings (Normalized EPS X # of Shares Owned Total Normalized Dividend Current Share Price Current Value of Investment (Current Share Price X # Shares Owned) Normalized Earnings Yield Normalized Dividend Yield Price to Normalized Earnings Multiple 10 Yr Estimated Growth Rate Year 10 Normalized Earnings Forecast (Based on current normalized earnings and my estimated growth rate) % of Portfolio Allocation Unrealized Gains % Unrealized Gains Normalized earnings is the field I focus most on getting right. I don't have a one size fits all approach for this one, though. I'm mostly focused on understanding what free cash flow will look like through a full economic cycle. I also try to understand and adjust for key risks - like super cats. For some investments I have to adjust for things like big, temporary, expenses - like major litigation costs/settlements that will take a few years to burn through (think post-GFC Bank of America). With some investments that have highly reputable managements I've learned that management forecasts are plenty reliable. So, if I'm really comfortable with a manager, I'll start with their forecast, try to poke holes in it, and adjust accordingly if I come up with anything. As far as making adjustments, I review my estimates annually at a minimum. However, anytime I learn about a material change, or think of a material risk, whether from company updates, CoBF, or otherwise, I immediately update my estimate. I probably make a handful of small adjustments to the model every quarter. I rarely have to make major adjustments at this point. I may make 1 or 2 major adjustments to the model each year. Usually, I get to just bump up the earnings estimate for the next year, which is fun. Since I started maintaining this spreadsheet in 2019 I've been able to increase my total normalized look through earnings by six figures every year just by replacing lower yielding investments with higher yielding ones whenever clear opportunities arise.

-

Yes, earnings quality and growth are essential. (Ideally, you have a high quality present value estimate.)

-

In the 1960s the top marginal tax rate in America was 91%!! Apparently there were 24 tax brackets, of which 19 were higher than today's top marginal rate. That was some SERIOUS anti-capitalistic wealth redistribution. By the time Reagan took office, two decades later, the rate had been reduced to around 70%. And, during the 1980s the rate was reduced further to 50%. We've got it real good today by comparison. Just shows the tug of war between the greedy capitalists and the bleeding heart liberals swings back and forth pretty widely over time.

-

They can fire up the printers and inflate those debts away Weimar-style. Apparently China doesn't have much of a safety net for the elderly, and with real-estate imploding bigly, the current generation of retirees is already pretty screwed. I assume elderly will be working longer and their children (err child) will be tightening the bootstraps to help care for mom and dad. Consumer staples will be fine, but commodities, discretionaries, durables, etc need to downshift a good bit. If a third of China's $18 trillion GDP has been tied to housing (and infrastructure to support housing), and another third derives from government-run entities that are one seventh as productive as their US contemporaries (so not super cash flow positive), then there's not a whole lot of horsepower left in the economy to service the interest on $48 TRILLION worth of debt (slap a 5% interest rate on that and you have to wonder how they can possibly afford to fund the debt AND pay for a sprawling government). Could be a REALLY hard, deflationary, landing. Assets could get REALLY cheap, even from here (think GFC). Once the dust really starts settling on the economic deterioration a billion or so Chinese people may stop taking so kindly to ol' Xi (queue insurrection). Assuming China doesn't devolve into a failed state like Russia, a real doozy of a downturn could prove to be the opportunity of a lifetime for cash rich companies like Tencent to hoover up competitors and talent for pennies on the dollar, and emerge much larger and stronger than they are today (think Berkshire during the GFC). Lots of ifs. Will be fascinating to witness from afar.

-

I almost never buy or sell. I have a handful of core investments that I’ve owned and followed for years. I have about 3% of my portfolio in some tracking positions that I’ve held for over 2 years while getting to know them better. I have a watchlist of companies I’m either trying to learn more about or waiting for the right price to buy. I find it very hard to find companies that I like better than my core holdings. Though it does happen. I’ve exited 7 or 8 positions in the last 5 years. Half were core holdings and half were trackers. Looking at equity earnings like a salary makes me think much more like a business owner when I’m buying parts of the businesses that are paying my “salary.” Also, once you give yourself enough “raises” - via more and better investments - you’ll be able to replace your actual salary with your equity “salary.”

-

Don't forget about the big risks of doing business with strapped-for-cash commies: 1) Big bro takes the free cash from the company for the good of the many. 2) When there's no free cash left big bro takes control of the company and appoints his buddies to all the paying jobs. Eventually Atlas Shrugs and the capital either fights or flees.

-

Selling an asset to buy a cheaper asset is a perfectly logical thing to do (assuming you’ve rationally factored in taxes and relative risks). It sounds like you’re overly influenced by price, which will make investing very uncomfortable at times. I recommend focusing more attention on learning how to appraise the value of a business. The more confidently you can estimate how much a business is worth to a rational buyer the less emotionally-attached to prices you’ll become. A trick that has been incredibly helpful for me… I created a spreadsheet where I track MY portion of the look through earnings from my equity investments. So, for example, If I have 100 shares of Fairfax and I estimate the normal earnings to be $150 per share then in my spreadsheet I would show MY total Fairfax earnings as $15,000. If I have 1,000 shares of BRK and assume $25 per share of look through earnings then I would add $25,000 to my spreadsheet. With Fairfax and BRK combined I would have $40,000 of earnings. (I look at those earnings almost like my salary. I want my “salary” to be big, steady and growing over time.) Notice I haven’t mentioned stock price, because my number one priority is the quality and growth potential of MY earnings. With that mentality, if I can at anytime sell all my Fairfax and BRK shares to buy assets producing significantly more than that $40,000 of look through earnings then I am happy to do it. I treat that like getting a pay raise - which is fun and motivating. This approach helps ensure that the only way I can confidently sell one asset for another is if I’m confident in my analysis and able to transact at attractive prices.

-

I wouldn’t be surprised to see the share price increase 35% this year - barring any black swans.

-

Regarding the China real estate crisis I’ve recently read/heard fun facts along the lines of: - China has approximately 80 million vacant homes, which is MASSIVE relative to the country’s 450 million households. - building 80 million excess homes is by far the biggest overallocation of resources in modern history. - Over 90% of the Chinese population already owns one or more homes. - Only 7% of the population has investments in securities/financial assets. - 30% of China’s economy has been tied to real estate. - The vast majority of household wealth is tied up in real estate. - Due to fear of the consequences of housing price declines, the CCP has instituted price controls on vacant houses. - Because prices aren’t allowed to decline, retirees and others are unable to sell the properties to fund their retirements, etc. - When the prices eventually adjust, homes in key areas of China could be worth 70% less. (By comparison the GFC was a nothing burger). - Also, because prices are artificially high, hundreds of millions of people don't know how much life savings they have left. - And, the major state-run banks are loaded up with real estate loans. - Because of price controls and an imploding economy, a large and growing percentage of the population is increasingly disgruntled. So, that sucks.

-

Thanks @Viking . It looks to me like the top 5 holdings alone could generate look-through earnings in the ballpark of $1 billion. Since the top 5 holdings represent about half the equity portfolio, it seems like your $1.8 billion earnings estimate for the equity portfolio is perfectly reasonable. Once again, thanks to your work, I’ll have to upwardly adjust my financial model. I have been underestimating the earning power of the equity portfolio.

-

Regarding the dividend, if memory serves, I believe one of FFH’s largest and most loyal shareholders has routinely been popping up on quarterly calls and politely asking Prem to consider a dividend increase. I like that Prem is setting an example here of how to be fair and friendly to long term investors. I also think there is psychological managerial benefit to being on the hook for paying your investors a dividend. It helps make managements more financially responsible. My hunch is managements that don’t pay a dividend are more apt to spend money on nap pods, trophy office spaces and moonshot bets. I assume the intangible benefits of investor goodwill and cultural discipline will ultimately offset the added tax burden.

-

In roughly 2010 I did 2 internet searches that led to my initial investment in FFH. First, I googled the phrase “Warren Buffet of [insert country name]” for a number of countries like Canada, England, Australia, etc. That was probably the first time I learned about Prem Watsa - the “Warren Buffett of Canada.” Second, I searched for “value investor message boards” which, of course, led me to COBF. Additionally, I remember reading one of the Berkshire annual meeting transcripts - around the time of the GFC - where Buffett had mentioned a Canadian insurer that almost perfectly timed the housing market crash with credit default swaps. I quickly learned it was FFH. Somewhere around 2010, after learning Prem and Fairfax were approaching legendary investor status I bought a few thousand dollars worth of shares. Maybe $50k. After following them for a decade, in 2020 I figured FFH was nearly certain to earn $28 to $35 per share. I really liked what I knew about Prem and the company, so when the shares hit $250 during the Covid crisis I bought 10 times more shares. After 2020 I monitored the discussions on this board very closely, and thanks to @Viking and others I realized I was vastly underestimating FFH’s true earning power, so I continued doubling down until I had over a third of my net worth invested (at somewhere around $400 per share). So far so good. I haven’t sold yet, since I still consider the shares undervalued, and since I’m still plenty happy with the management and culture.

-

I think Greg is the operations guy - following Dave Sokol’s hard core manage by objectives playbook. Basically, Greg is responsible for holding under-performers accountable for getting back on track. Todd is one of the best business analysts on the planet. So he gets to review - and reject - hundreds of deal opportunities a year. And Ajit is the insurance god. I think we’re in good hands.

-

I voted no, but mostly because $2,000 would require a slightly more optimistic outlook than I’m comfortable with. I’m assuming BV will be around $1,500 per share by the end of 2027, and I believe 1.2x BV ($1,800) is a reasonably conservative multiple for FFH. Now, with that said, given how unpredictable Mr. Market is, and how well FFH has been managing capital in recent years, I do think there’s maybe a 50/50 chance the share price could at least touch the $2,000 per share mark by the end of 2027. So, I’m not a hard no. I just don’t want to set myself up for disappointment.

-

You would have to chart a few more things to be able to answer your questions. Just looking at per share BV growth, CR and Portfolio return doesn’t tell you enough. For example, you would need to know the share count at the beginning and end of the period. During some periods FFH issues lots of new shares, while other times FFH buys back shares. This impacts per share BV growth. Additionally you would need to chart the premiums written per share and the value of the portfolio per share. The amount of premiums written per share fluctuates widely depending on the underwriting environment. During soft markets FFH will reduce premium volumes to 1x BV or less. But, during hard markets FFH ramps up premium volume to 1.5x BV. So, CR needs to be viewed in relation to the amount of premiums per share during a given time period.

-

YES. I was just about to say the same thing about return of capital. With so much cash flooding in the door it will be very interesting to watch where they park it. If the stock price continues hovering around book value then if they aren't using excess cash to buy back shares it means they must have REALLY juicy alternatives. I assume the only reason they would park excess cash into ultra-low yielding bonds rather than return capital would be if those bonds allowed them to underwrite additional insurance at extremely favorable rates.

-

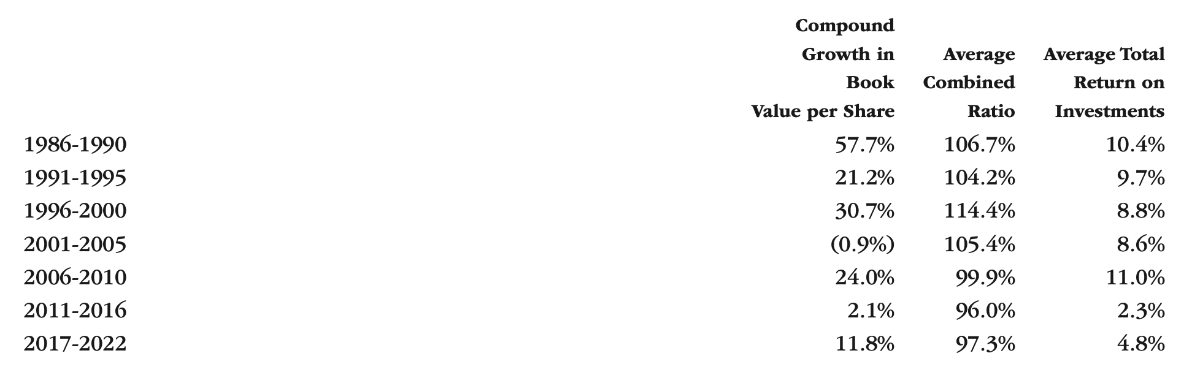

From 2011-2016 5-year treasuries yielded around 1.5%, and the portfolio only yielded 2.3% because of the equity hedges. From 2017-2022 5-year treasuries were extremely volatile, but appear to have averaged around a 1.75% yield. However, the portfolio returned 4.8% thanks to the equities, etc. I think the last decade shows us that a 4.5%+ portfolio return is reasonably achievable even in an environment with sub 2% treasury yields. Therefore, $100+ per share portfolio earnings (after taxes/expenses) seems plenty reasonable 4 years from now and beyond.

-

Here is a historical chart showing average portfolio returns:

-

If you want a doomsday scenario where cash and bonds collectively earn less than 1%, and the rest of the portfolio earns less than 8%, you're looking at EPS in the neighborhood of $90 pre-tax. After taxes and overhead/expenses would put it around $40 EPS. Add or subtract what you want for insurance earnings. I'd expect at least $25 to $50 EPS in that type of rate environment.

-

The investment portfolio will probably be closing in on $70 bil in 3 years. Bonds and cash will probably make up 60% of the portfolio. A blended 4.5% return, or $3.2 bil, should net around $100 per share. If the bonds are only earning 2% then the rest of the portfolio has to earn 8% to maintain the $100 per share bogey. I don’t think that’s too big of a hurdle for the investment team. I also think if interest rates are 2% that it’s not far-fetched to assume sub-100 combined ratios, which should help FFH stay in the neighborhood of $150 EPS through the cycle.

-

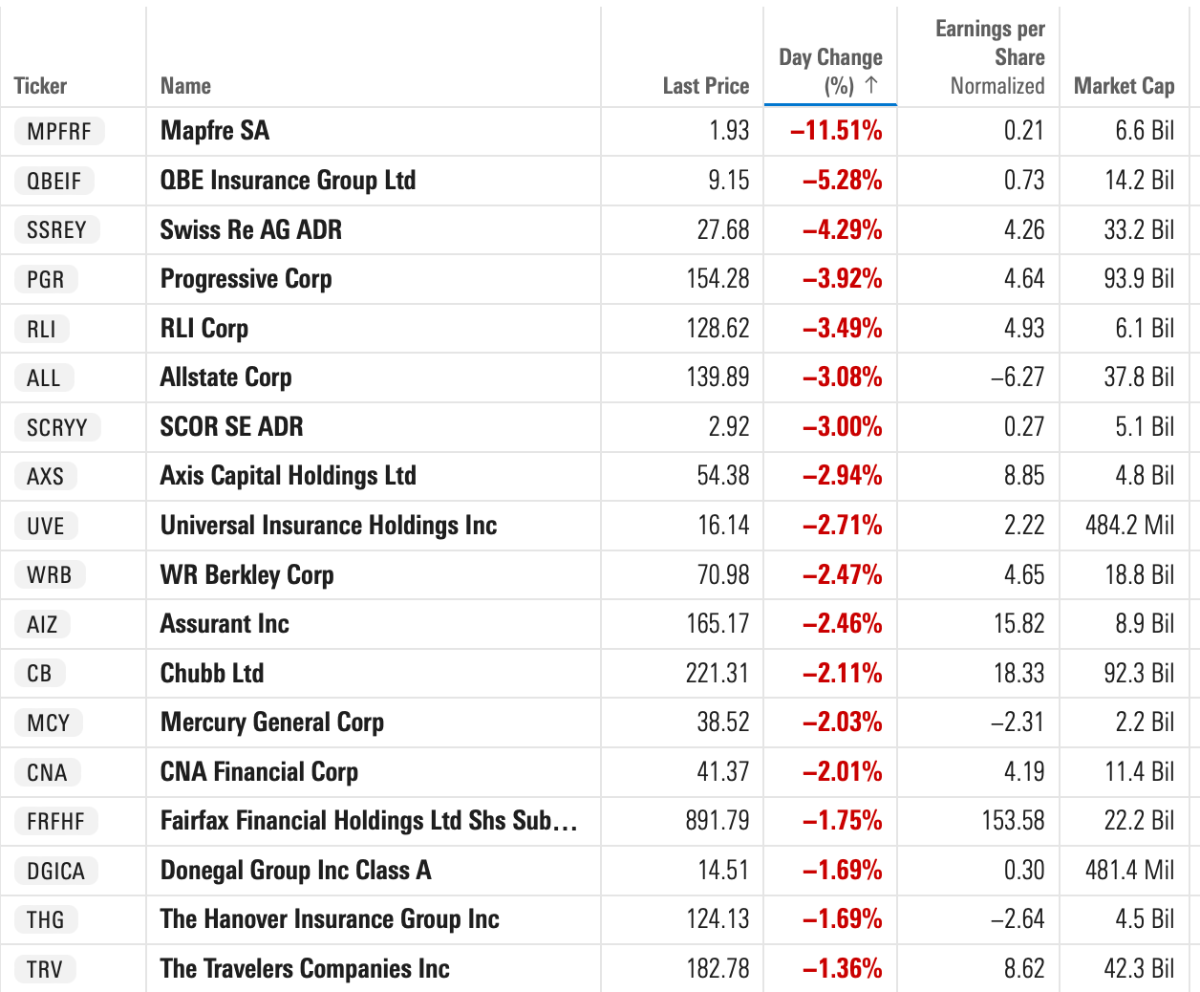

Industrywide beatdown:

-

If we assume BV grows by $150 per share annually for the next 3 years then depending on which year P/BV hits 1.2x your compound annual return from today's price would be as follows: If P/BV is 1.2x on Dec 31 2024: approx 40% CAGR! If P/BV is 1.2x on Dec 31 2025: approx 26% CAGR If P/BV is 1.2x on Dec 31 2026: approx 21% CAGR Of course, if P/BV is still a sad and lowly 1x BV by Dec 31 2026: approx 14% CAGR And, if P/BV reverts to the 2020 level you're looking at a Dec 31 2026 CAGR of approx 2% (buying opportunity!)