nafregnum

-

Posts

265 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by nafregnum

-

Around July 21-23 The Economist ran some articles and podcast episodes critical of ESG in its current form. (Special Report: A broken idea. ESG Investing) https://www.economist.com/special-report/2022-07-23 (Economist Money Talks podcast, July 20, 2022 - The backlash against ESG) https://overcast.fm/+JXrTTNtN0/0:35 A good quote: "E. and S. and G. independently, all have their merits. Where it goes wrong is when they're put together into one ugly acronym." Personally, I do care about all three letters. The problem is: you can't boil down measurements on all three of these domains and come up with a meaningful single score... I worry that ESG funds might be selling the feeling of moral purity and righteousness without really doing a whole lot -- which is a problem because (a) people who care may be lulled into a false sense of security/virtue, and (b) the vilification of O&G is leading to a kind of chronic undersupply. John Curtis (Republican US representative) has some great thoughts about the bigger picture -- he says U.S. natural gas burns 40% cleaner than Russian natural gas. The USA represents 14% of worldwide emissions. So even if USA got to zero, it wouldn't mean a whole lot on its own. If NG from North America is so much cleaner, and if it's more responsibly sourced (less methane leaks, more oversight, etc) then why wouldn't the USA want to celebrate its NG industry? There's just a lot of confusion in the thinking as we humans muddle our way toward a greener future. At a dinner in Scotland, the president of Scottish Power told him that they're 100% renewable, because they have so much wind that they can power the whole country with wind. Curtis asked him innocently: "What do you do when the wind doesn't blow?" And he said, "Oh, that's easy. We import Russian NG when the wind doesn't blow." Two minutes later he looks at Curtis and says "We are 100% renewable." having not made the connection that they were still very dependent on natural gas. ... One more example of confused thinking: https://www.inputmag.com/tech/gmc-hummer-ev-carbon-dioxide-emissions-electric-truck I'm sure there'll be plenty of EV Hummer owners with virtue signaling vanity plates, despite the fact that they're dirtier than ICE sedans (charging that huge battery with power from the U.S. grid causes more emissions than a gas engine sedan emits.)

-

Global food crisis coming? If so, how will it play out?

nafregnum replied to nafregnum's topic in General Discussion

https://www.bloomberg.com/news/articles/2022-08-02/europe-may-turn-to-manure-in-switch-away-from-russian-fertilizer Sounds like it'd take some years to transition to manure for some reason. If Nitrogen is so expensive to make with high NG prices in Europe and BASF isn't doing it there now, it seems like NG prices in USA will remain low enough for someone to build up a few nitrogen plants in America and export it over to Europe? -

I started listening to Peter Zeihan's recently published book "The End of the World is Just the Beginning" after watching these videos where he makes a bunch of bold predictions -- his presentation to the pork industry was packed with information, and very entertaining. A lot of the info was new to me since I don't follow agriculture very closely. (and part 2) Now I'm trying to chase down and verify a lot of this information... For example, just in the first 90 seconds he says Ukraine with 17% of global corn exports has already fallen off the map and is not coming back. Same with Brazil and soy exports (55%) which he says is falling off the market and won't be coming back either. He explains why: Nitrogen fertilizer inputs are too expensive now. China imports 59% of its soy, so their hog farming seems like it'll be pretty wrecked. He's was hired to make this presentation to the US pork producers industry, and his conclusion for them was that a lot of their competitors will be gone within 3 years and it'll be fat years for US pork producers. I'm not sure what I think. If we get a global food crisis, wouldn't humanity switch to eating the corn and soy directly rather than feed it to pork? If nitrogen fertilizer stays expensive, what crop yields suffer most, and where else does this cascade? The price of gasoline is already causing uprisings in parts of the world. Won't it be even worse if the price of bread skyrockets? Is there really a credible risk that Russian oil fields in the permafrost will get stopped and we'll lose 4-6mbd of Russian crude? If it happened, would losing that much supply just wreck the whole world? I'm interested to hear what anyone else thinks about this stuff...

-

Where Does the Global Economy Go From Here?

nafregnum replied to Viking's topic in General Discussion

This is definitely a factor, and seems to be an elephant in the room for the political parties. I don't think either party is brave enough to say we NEED immigrants. The Economist has a current article (the July 30 2022 issue) titled "Not coming to America" about recent declines in immigration. An estimated 1.8m working age foreign migrants are missing relative to the post-2010 trend (graph below) A lot of older migrant workers from Mexico have moved back, and the US hasn't been moving quickly enough to get through a huge backlog of H1B visa interviews. ...one quote: "The Pew Research Center calculates that without new arrivals America's labor force would decline to 163m in 2040 from 166m in 2020. If net immigration were to return to pre-pandemic levels, the labor force would instead grow to 178m by 2040." ...the conclusion paragraph: "There is no shortage of sensible ideas. Connecting migrants with employers before they reach America's southern border would reduce pressure on crossings and help businesses. Marianne Wanamaker, who served as an economic advisor in Mr Trump's White House, argues that getting rid of visa caps for specific occupations would also alleviate worker shortages. "We have tools available to us to resolved labor issues that we don't appear willing to use," she says. "That is the result of years and years of making immigration a third rail of American politics." The conclusion is a dismal one: the headaches of the past year from worker shortages, far from being temporary, will be a recurrent problem in an ageing America that has forgotten how immigrants made the country what it is." Add to this the demographics of China itself. https://www.reuters.com/world/china/chinas-population-expected-start-shrink-before-2025-2022-07-25/ Sam Harris recently interviewed Ian Bremmer about his new book, "The End of the World is Just the Beginning" ... he says China's one child policy had wrecked their demographics and undoing the policy was among the first changes Xi made when he came into power, but the demographic problem is unavoidable and will be impossible for them to fix without massive immigration (which isn't very common in China as far as I'm aware) https://www.samharris.org/podcasts/making-sense-episodes/288-the-end-of-global-order Here's a bit of the discussion where Ian mentions how the census data is worse than it appears, starting around 2m22s into it.

-

I think all time highs won't be back so soon either. 1) Interest rates are higher and we won't be back to ZIRP this year. 2) Ukraine war and European energy's spooky disharmonious conflict hell ride coming up this winter. 3) Oil, which won't get cheap unless national recessions kill demand because supply is constrained by green dogmas. Almost a year ago, in the thread "THE TOP is coming" there was the idea from an interview with Jeremy Grantham that referenced 'confidence termites' which would cause the risky stuff to start trending downward while money moved into safer places, until even the safest places would be sliding downward as well. Now I find myself wondering what sectors will bounce back first as confidence starts to build...

-

Interesting detail I heard this morning about inventory levels and discounting that's upcoming. Animal Spirits podcast today mentioned that some liquidator companies are picking up container deliveries directly instead of having those products flow through their intended retailers first -- that kind of seems like a bullish indicator for stores like TJ Maxx and Ross, but it also seems like there'll be some better than usual deals on appliances and such in another month or two, and Black Friday -- and that may push inflation down a little more as well.

-

The link between value investing and Stoicism.

nafregnum replied to Fundmanagerthrwawy's topic in General Discussion

I think learning about Stoicism is a huge benefit to investing mindset. We can't stop strong emotion from happening during an emergency moment, but we CAN recognize when everyone is losing their head and ask ourselves whether panicking is helping the situation. I think Marcus Aurelius was caught in a squall at sea and everyone was freaking out and he was the guy who got calm first and helped everyone else to do what was necessary to keep the boat from sinking. Buffett's Inner Scorecard analogy seems like a pretty stoic concept. The practice of negative visualization (imagining what could go wrong) seems similar to Charlie's "Invert, always invert!" Focusing on those things inside our own control and not worrying about things outside of control -- that sounds so much like the advice to stay in the circle of competence. I wouldn't be too surprised to find Stoic influences in the life of Ben Graham or his mentors. Ok, I just googled "Ben Graham stoicism" and found this nice essay: https://macroops.substack.com/p/a-value-investors-guide-to-stoicism (quote is from Graham's "The Intelligent Investor") If you've already read Meditations, my favorite book on Stoicism after that one is "How To Think Like A Roman Emperor" by Donald Robertson. The Audible version is great for me because I love listening to UK accents and he sounds Scottish. It's got a lot of biographical details about Marcus Aurelius' life that brought him more to life. Some very good stories in there. -

From where we are today, which sectors will benefit most if inflation cools off? Housing because of the return of low mortgage rates? Tech? Which will benefit most if inflation remains higher longer? Oil (think OXY) + financials (banks, due to higher rates)? To use Parsad's metaphor: Which springs are coiled tightest right now?

-

Thanks, by the way, to everyone in this thread as well as the energy sector thread and the inflation thread. I've gained a lot from your contributions and experiences.

-

I really like this question. I once read the market is priced for what people think conditions will be in 18 months. If that's true, I imagine we'd see a bottom after the first official readings show inflation cooling off. Mr Market will see a light at the end of the spooky Fed rates tunnel. @Ulti contributed this link in the other thread about inflation, with some evidence that we may already be past the inflation peak. https://ritholtz.com/2022/06/revisiting-peak-inflation/ Question is... will it be the real multi-year bottom, or a head fake? For example, there are 1M barrels of oil per day coming from the US strategic petroleum reserve until September 30. What happens to oil prices after that point? Will speculators pile back into oil and cause inflation fears to resurface? https://www.reuters.com/business/energy/us-sell-up-45-mln-bbls-oil-reserve-part-historic-release-2022-06-14/ I know I shouldn't enjoy thinking about the macro stuff this much. None of my thoughts are very original, but it's still pretty fun to dream up this big Rube Goldberg machine and imagine it in motion.

-

Movies and TV shows (general recommendation thread)

nafregnum replied to Liberty's topic in General Discussion

Thanks for that earlier recommendation, @Spekulatius! I've been watching Station Eleven this week (finished episodes 5 and 6 last night) ... I might need to review some Shakespeare plots just to appreciate it better. The show has really grabbed hold of me -- I keep thinking, "I sure do appreciate civilization and the internet." Just imagining the trauma for all the pre-pans is super heavy. -

I wish I knew a lot more about the oil hedging that airlines and oil producers do. About 12 months ago oil was $20 and now it's around $120. During the lows you'd hope all the airlines locked in some extremely cheap gas hedges. And now oil producers are going to to lock in at these highs. Is this the kind of wild volatility that ends up bankrupting the insurers (is this all done with derivatives?), or are these financiers making money hand over fist and loving every minute of it?

-

My hope for end-game is that they get to a cease fire before April. I can't predict much, but these two articles gave me some hope. This one made me want to go eat at McDonalds. I think they're doing a class-act kind of thing to not leave all those 62k workers high and dry. https://www.newsweek.com/mcdonalds-closing-restaurants-russia-will-keep-paying-62k-workers-1686052 This one gave me hope that they achieve a negotiated peace before the death count goes from under 10k to over 100k. https://www.jpost.com/international/article-700677 And this one's for Putin and all other Masters of War. (IMO the best Bob Dylan cover ever)

-

+1 for mental models This is also in the book "Influence" by Robert Cialdini - the book that Munger loved so much he gifted it to all his grandkids, and gave the author 1 share of BRKA worth about $73,000 at the time if memory serves. An example from the book was specifically about Russia: “This pattern offers a valuable lesson for would-be rulers: When it comes to freedoms, it is more dangerous to have given for a while than never to have given at all. The problem for a government that seeks to improve the political and economic status of a traditionally oppressed group is that, in so doing, it establishes freedoms for the group where none existed before. And should these now established freedoms become less available, there will be an especially hot variety of hell to pay. We can look to much more recent events in the former Soviet Union for evidence that this basic rule still holds. After decades of repression, Mikhail Gorbachev began granting the Soviet populace new liberties, privileges, and choices via the twin policies of glasnost and perestroika. Alarmed by the direction their nation was taking, a small group of government, military, and KGB officials staged a coup, placing Gorbachev under house arrest and announcing on August 19, 1991, that they had assumed power and were moving to reinstate the old order. Most of the world imagined that the Soviet people, known for their characteristic acquiescence to subjugation, would passively yield as they had always done. Time magazine editor Lance Morrow described his own reaction similarly: "At first the coup seemed to confirm the norm. The news administered a dark shock, followed immediately by a depressed sense of resignation: of course, of course, the Russians must revert to their essential selves, to their own history. Gorbachev and glasnost were an aberration; now we are back to fatal normality." But these were not to be normal times. For one thing, Gorbachev had not governed in the tradition of the czars or Stalin or any of the line of oppressive postwar rulers who had not allowed even a breath of freedom to the masses. He had ceded them certain rights and choices. And when these now-established freedoms were threatened, the people lashed out the way a dog would if someone tried taking a fresh bone from its mouth. Within hours of the junta's announcement, thousands were in the streets, erecting barricades, confronting armed troops, surrounding tanks, and defying curfews. The uprising was so swift, so massive, so unitary in its opposition to any retreat from the gains of glasnost that after only three riotous days, the astonished officials relented, surrendering their power and pleading for mercy from President Gorbachev. Had they been students of history—or of psychology—the failed plotters would not have been so surprised by the tidal wave of popular resistance that swallowed their coup. From the vantage point of either discipline, they could have learned an invariant lesson: Freedoms once granted will not be relinquished without a fight.” - Excerpt From: Robert B. Cialdini. “Influence: The Psychology of Persuasion.”

-

I think Shell came under some heavy criticism. I just read that they've announced all profits from that purchase will go to Ukraine aid. It feels like poetic justice for profits from Russian oil sales to be flowing into Ukraine. At a minimum, there's t $28.50/barrel in profits because of the way it was sold. At 7 barrels per metric ton, and 100,000 metric tons, that's 700,000 * 28.50 = $19,950,000 that Shell would need to pay out.

-

Clarification: It was $28.50 below benchmark Brent crude price, not $28.50 per barrel. https://www.wsj.com/livecoverage/russia-ukraine-latest-news-2022-03-04/card/shell-buys-russian-oil-at-bargain-price-2ZljvO2HQlmPm5d5aAgG Shell bought 100,000 metric tons of Russia’s flagship Urals crude on Friday, according to people familiar with the transaction. It paid $28.50 a barrel below the price of international benchmark Brent crude, the widest discount on record.

-

I've been stewing on this question and following threads like this with interest. Thanks to everyone for your thoughts here. Below I probably sound pretty bearish, but there's a big difference for me between feeling worried and feeling certain enough to take action. I'm currently at 9% cash... Whatever happens this year and next, I wish everyone here good success. Recently I listened to a very interesting book called "I am a Strange Loop" which focuses on feedback loops like when a microphone and speaker are too close to each other and they generate that horrible high pitch screech because the two are "feeding into" each other. Another feedback loop mentioned by the author is the idea of a best seller list for books. Many people buy books on the NYT Bestseller list simply because the book is on the list, which helps fuel the book to climb higher in the rankings. Publishers know this, and will spend a lot of upfront money to promote a promising title, hoping to get onto the list and ride the inevitable wave of popularity. Looking at the last few months and my own thinking, I'm finding reasons to worry ... just thinking about other things I've read by people like Buffett & Munger, Howard Marks (in The Most Important Thing), and Jason Zweig (his chapter commentaries in The Intelligent Investor) ... Buffett: "The future is never clear; you pay a very high price in the stock market for a cheery consensus." also "Be fearful when others are greedy, and greedy when others are fearful." https://money.cnn.com/data/fear-and-greed/ I keep telling myself I'll wait until people are feeling especially greedy to sell out of some of my most overvalued positions, but when they get up again I keep feeling too greedy, thinking "I'll wait until tomorrow or the next day to sell it." and then they move down 5% or more and I go back to "waiting" trying to catch a top that eludes me yet again... so my own behavior is starting to make me think I'm too optimistic. Marks said somewhere that if he could know just one thing about a stock before he buys it, he'd like to know precisely how much optimism is already priced into it. I can't find the sentence now, but a lot of similar sentiment is in this memo: https://www.oaktreecapital.com/docs/default-source/memos/2015-09-09-its-not-easy.pdf Chris Bloomstran just took a close look at the ARK fund's components: Jeremy Grantham gives interesting details about how some previous tops died, not like a balloon popping but like air leaking out of a balloon. He called it "confidence termites" in this recent podcast interview (from Aug 5th) https://moneyweek.com/investments/investment-strategy/603678/jeremy-grantham-podcast [ below is what I found interesting from Grantham -- he describes how the risky junk loses the most value first, and then you may see "confidence termites" eat away at sentiment like a feedback loop ] Grantham: The history books are pretty clear, there doesn’t have to be a pin. No one can tell you what the pin was in 1929. We’re not even certain in 2000. It’s more like air leaking out of a balloon. You get to a point of maximum confidence, of maximum leverage, maximum debt, and then the air begins to leak. And I like to say, the bubble doesn’t reach its maximum and then get frightened to death, what happens is the air starts to leak out slowly because tomorrow is a little less optimistic than yesterday. And gradually, people begin to pull back. And the process is very interesting, in that before the end of the great bubbles, and there’s only been a handful, so we can get carried away with over-analysis. But before the great bubbles ended in 1929, 1972, and in 2000 in the US, the three great events of the 20th century, there was a very strange period in which, on the upside, the super-risk, super-speculative stocks started to underperform. They never do that in between, ever. And then suddenly, it starts. So, you go back to 1928, the JACI Index, the low-price index, and the S&P were up 80% in 1928, and then the S&P was up, say, 40%. That’s what it’s meant to do. And then in 1929, the S&P went up another 40% before crashing. The low-price index started early in the year to go down. It couldn’t even get the sign right. It had a beta of about two, and started to go down, and the day before the crash it was down over 30%. Nothing like that happens again until 1972. And let me point out that 73/74 is still the biggest decline, adjusted for inflation, since the Great Depression. It was 62% in real terms. And in 1972, the last up year, the S&P outperformed the average Big Board stock by 35%, approximately plus and minus 17 points. The average stock was going down steadily all year, and the S&P was going up. Nothing like that happens again until 2000. In 2000, in March, the great TMT bubble starts to peak, and Pet.coms get taken out and shut. And then in April and May, the junior growth. May/June, the middle growth. June, July, August, the Ciscos. Cisco was the biggest company in the world for eight minutes, I like to say. And the whole TMT block, that was 30% of the market cap, was down about 50% by September. The S&P was unchanged. Unchanged. Which meant that the remaining 70% was up 17%. That is an amazing deviation. So, bang, bang, bang. It’s only happened three times. It happened leading into the great air leaking out. And finally in September, the confidence termites, as I like to think of them, reached the broad market, and the entire 70% rolled over like a giant iceberg, and down it went, 50% over two years. And so, where are we today? Those three deviations, by the way, 1929 was eight months, 1972 was 11 months, and 2000 was six or seven months. And on February 9th, the Russell 2000, which had had a crushingly good year, wiped out way ahead of the S&P from March of 2000 until February 9th, way ahead of the NASDAQ. And the S&P has continued on its merry way, having a nice bull market. Even after yesterday’s great rally, the Russell 2000 was decently down since February 9th, the NASDAQ is five points ahead of it, and the S&P is ten points ahead. This is getting to be a pretty good down payment. It’s February, March, April, May, June, July. It’s five months. I would say this is tracking quite nicely. And the confidence termites started, once again, exactly where you would expect, they started with my favourite biggest holding, personal holding, QuantumScape. QuantumScape, a solid-state lithium-ion battery company I bought into eight years ago, as a green venture capital. They came as a SPAC, came at ten, went to 130. At 130, it was 52 times my investment, which is pretty nice. It was also $55 billion, bigger than GM, bigger than Panasonic, if you want to think batteries. There’s nothing like that to compare to in 1929, by the way. The scale of that. They’re a brilliant research outfit, and I’m happy to still hold a quarter of my… But they don’t have a product for four years, and they have no trouble telling you that. So, here is a research lab that will have no profits, no revenue for almost four years, selling more than GM. $55 billion, give me a break. Anyway, that started down. It’s now down 80%. The SPAC Index is down 30%. The SPACs have started to dry up. Bitcoin, 62,000 to today’s, after a nice rally, 31,000, half price. Tesla, 900. Down to 650. This is the classic pattern of start with the most speculative, the most heroic, and work your way down carefully until finally you’ve reached the market. I would say it’s lasted longer than I thought. Why? Two reasons. One, the vaccine was simply bigger and better than anyone expected, and we produced it quicker, it was more effective, particularly Moderna, Pfizer, than anyone had ever hoped possible, really for any vaccine of that kind. And the other reason was the speed and size of President Biden’s stimulus package. He came in with such a roar, and bang, you’re suddenly talking trillions of dollars of stimulus. Those two things, of course, were bound to increase confidence, bound to increase the money in the hands of individuals. Individuals, because of Trump’s stimulus and because of Biden’s stimulus, have been dripping in resources, and they have bought into every setback. And they’re buying all the crazy stuff, the meme stocks that are just jokes, where they’re whipped up into a frenzy, and they’re buying them just for fun, it seems, ten times more than any underlying value. And, by the way, every indicator of that craziness, this is a record, this is more impressive even than 2000, and that was more impressive than anything that had preceded it. But the craziness that we have seen in the meme stock, companies being bought on no earnings potential, on no underlying reality, is just amazing.

-

Li Lu Book Documentary - Moving the Mountain - it is riveting

nafregnum replied to LongHaul's topic in General Discussion

I think I found the answer to your question about what Li Lu meant - there was a Q&A session afterwards where he says this: https://www.longriverinv.com/blog/qampa-with-li-lu Question 11. You said earlier that index investing can be a suitable choice for the average investor so long as the index reflects the overall economy. Assuming passive index investment funds continue to occupy a larger and larger share of the market, what consequences do you think this will have? Li Lu: This is a very interesting question, although perhaps less relevant in China because index funds do not yet comprise a large part of the market. The situation is also different in China and the US. In China, because we haven’t yet fully implemented [an effective system of corporate disclosure], nor do we have a strong policy for de-listing companies, our indices do not fully or fairly represent the underlying economy. I think that the regulators will address this in the coming years. We have transformed from a manufacturing- and export-led economy into a consumption-led economy. In this new era, the means of financing may move from indirect finance to direct finance. The role of the stock market will grow in importance, and this will require attracting more and more people to participate in it. But if we want more people to participate, we will have to better control the market’s gambling and excesses, and increase the part of it which focuses on investment. The best, fastest and biggest way to do the latter is through index investing, which means making indices better reflect the underlying economy. One possibility would be to develop a good ETF to do so. But there are many man-made factors involved which make this not the easiest course of action. The best approach is to therefore use a market-based solution [and enhance regulation] so that the existing indices become more representative. This is China’s challenge. -

As far as I can tell, it still doesn't really have the "alerting" type stuff I want -- the GuruFocus watch list will email when the price of something in the watch list changes by 5% or more in a day, or if trading is more than double the 30-day average volume. I'd love to see notifications of insider buys/sells, as well as buys/sells from 13F reports.

-

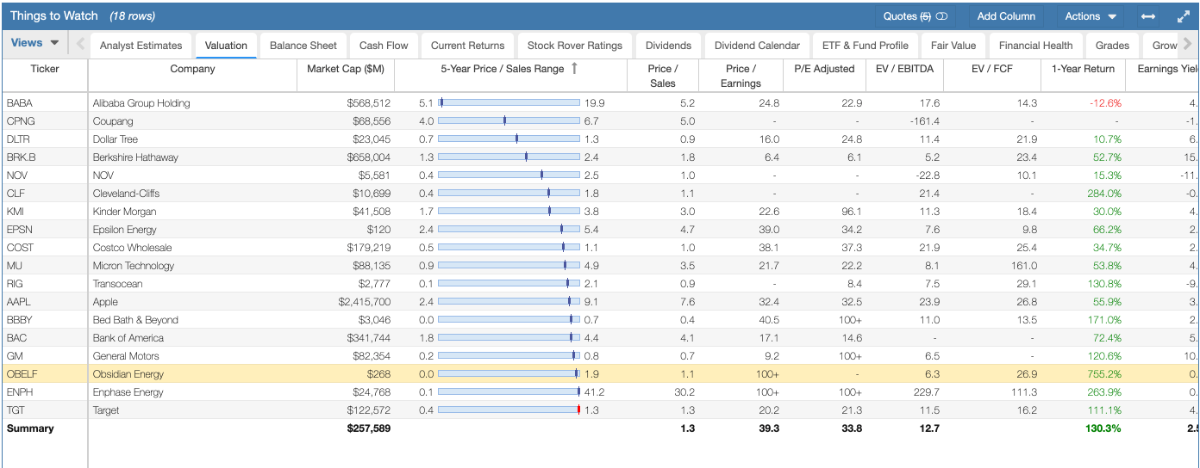

The best I've found in the last couple days has been stockrover.com -- in addition to some strong screener functionality, you can make watch lists and then see all kinds of comparable columns for the companies in the list - you can also chart all the stocks in a watchlist as a group. I really like being able to move columns around and sort by things like "5 year Price/Sales range" as in this screenshot.

-

https://www.forbes.com/sites/woodmackenzie/2021/06/17/how-high-can-oil-prices-go-in-2021/ Interesting tidbits, if I understand the article correctly: * The first half of the year used up 100 million barrels of the inventory buildup that happened in 2020. By the end of the 2021 the inventory will be reduced another 100 million barrels, under pre-pandemic storage levels. * "OPEC+ is currently revelling in higher prices and recouping some of the US$335 billion of revenue the group ‘lost’ last year when the market collapsed. A Brent price in line with our 2021 forecast of US$69.30 would lift OPEC’s revenues close to 2019 levels on 10% less volume." ... So, as it appears to me, back in Nov 2014 OPEC flooded the market in order to try to kill North American shale, but it only partly worked. OPEC was willing to push prices down when they were swimming in money and could deal with some short term pain. But now the incentives are different: after losing $335B in 2020 they actually NEED their oil to be more profitable in order to recuperate. Having OPEC "aligned" at least in the near term seems like a nice environment for unhedged producers like Obsidian Energy.

-

Is there a killer app in the "Watch List" category? I've heard investors say they build a list of all the companies that meet their criteria which they'd be happy to own at the right price. I'd love to do the same thing, but I'm doing too much of the tracking in my head. Here are things I wish I had: * I want to know when insiders are buying or selling companies in my watch list, like in an emailed report * Notifications of significant price or volume movements (gurufocus.com watch list currently satisfies) * Simulated "Morning Newspaper" view of recent news stories about any of my companies * Notifications of buys/sells by 13F "Super Investors" like the list of folks on dataroma.com * Notifications of dilution / buy backs.

-

I Haven't Been This Excited About Going Against The Herd in Years!

nafregnum replied to Parsad's topic in General Discussion

Thanks a lot to both of you for these other names to check out -- since my "bet" is for recovery in oil, then maybe stretching it across a basket of these names will be a little less risky than if I plow it all into Obsidian (already took a 3% position there) -

I Haven't Been This Excited About Going Against The Herd in Years!

nafregnum replied to Parsad's topic in General Discussion

Thanks a lot @Gregmal I've been thinking similarly about Oil. Good solid reasons demand should remain strong. I got unbelievably lucky about 4 years ago in buying a small position in Enphase (solar stuff) when I saw Dan Loeb had bought a chunk. It turned out to be my first (and probably only ever) 100+ bagger. Now I'm considering whether to sell and just put those winnings into Obsidian Energy because I think Enphase won't double from here within 12 months but I think I agree with @SharperDingaan that OBELF it has a fair chance of doubling from its current level. -

I Haven't Been This Excited About Going Against The Herd in Years!

nafregnum replied to Parsad's topic in General Discussion

Oh darn. This is something I wasn't very aware of -- is there another thread or someone I ought to read more of to get a good understanding of what might blow up in Energy? Do you mean a bubble in all energy, or just in "Green Energy"?