Luke 532

-

Posts

2,931 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by Luke 532

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Jesus speaks out against mockery throughout the New Testament. Jesus uses truth to drive home his point all the time. He repeatedly "pulls rank" with those that mock him in the Bible ("I AM"). I'm using truth (the fact that patience is a pillar of successful investing) to drive home the point that it shouldn't be mocked. I'm "pulling rank" to provide an example that patience does work, and it works for an everyday Joe like myself. If you'd like to discuss further you already know my e-mail. Don't want to clog the board further with non-investing stuff. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

It's always fun when a non-millionaire mocks a group of millionaires on how patient they are being for a thesis to play out. Wow. Hey man. You tilted? Lol, I’ve made money on trading this. Lol. Tilted? Not even close. Glad to hear you've made money trading it, but my comment was based on my pet peeve of those with less success at something (whether it's investing, athletic ability, personal finance, etc.) mocking the very traits that have made those more successful than them, well, more successful. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

It's always fun when a non-millionaire mocks a group of millionaires on how patient they are being for a thesis to play out. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Seems to me that David Stevens is acting a bit desperate... Ten days ago... Four days ago... Today... https://www.insidemortgagefinance.com/imfnews/1_1379/daily/treasury-wants-to-reduce-fannie-freddie-footprint-1000046445-1.html?ET=imfpubs:e11034:73599a:&st=email&s=imfnews In a new opinion piece, Mortgage Bankers Association CEO and President Dave Stevens takes aim at the speculators who bought shares in Fannie and Freddie and the tactics they’ve taken to get the two released into the wild again (commonly known as “recap and release”). In a new blog posting, Stevens says since the moment the GSEs were put into conservatorship “a debate has raged over their future. The debate is complex, highly charged and at times, frankly nasty.” Then the soon-to-be retired trade group CEO notes: “Part of the reason for the tone of the debate is that various groups representing the interests of shareholders of the two companies have chosen to wage a bare-knuckles campaign to get the two companies re-privatized. If they were re-privatized, the increase in value of these stocks, currently trading below $2 per share, could produce a massive profit to their investors. Thus, a hodge-podge of players acting on behalf of shareholders has put significant capital behind a coordinated effort to increase the odds of their re-privatization, including contributing to sympathetic non-profits and other stakeholders who could be persuaded to share their views, hiring PR firms to plant beneficial op-eds and other stories in the press, and creating organizations intended to give the impression of grass roots support.” Wait. Planting stories in the press? Donating money to nonprofits? Sounds like a page out of the Fannie-Freddie lobbying book, pre-conservatorship… -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

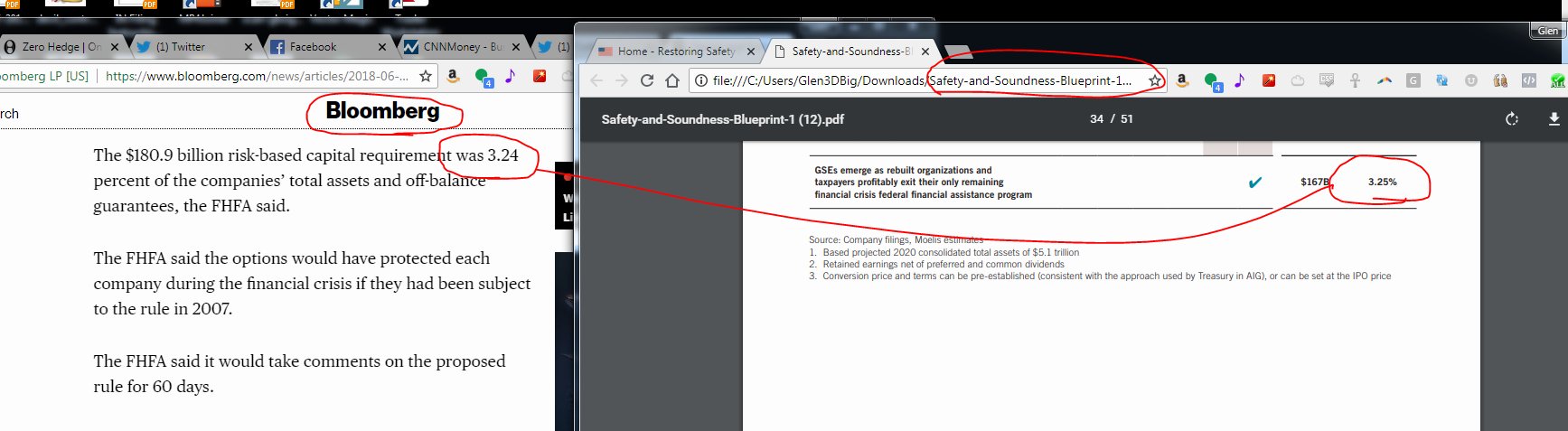

Tim Howard's comments on Rosner's paper... https://howardonmortgagefinance.com/2018/05/03/a-view-on-affordable-housing/comment-page-1/#comment-6828 I’m a little puzzled by this note from Josh. I generally agree with his overall assessment of the FHFA capital proposal—which he calls “a good start,” and “not being so onerous as to reduce the economic viability of their mandated mission to ensure liquidity to the primary mortgage market”—but he then spends the bulk of his piece objecting to the fact that “FHFA will not implement the capital requirements while the GSEs are in Conservatorship and will, instead, wait for Congress or the Administration to affirmatively act on GSE reform,” arguing that “Such a position is in direct opposition to the requirements of the HERA law and, again, ignores that Congress has acted and given it direction in the HERA law.” All of that is true. The problem is that Treasury and FHFA interpret HERA differently from how Josh does, and so far the Treasury/FHFA interpretation has prevailed in every court case decided to date. Fannie and Freddie cannot be recapitalized as long as the net worth sweep remains in force or until the conservatorship has ended, and FHFA cannot end either the sweep or the conservatorship without Treasury’s approval. For those reasons, I’ll take the half a loaf FHFA has given us: beginning a substantive dialogue about the right way to capitalize the companies post-conservatorship, if, whenever and however—i.e. legislatively or administratively—that happens. As I noted shortly after the FHFA capital proposal came out, I’m going to take my time going through and analyzing it before I write my comment letter (which I’ve got a couple of months to do). But I do have a preliminary reaction to it: it is extremely, and I would say unnecessarily, conservative. I’m going to withhold judgment as to whether the average 3.24 percent “estimated risk-based capital requirements as of September 31, 2017” for Fannie and Freddie shown in Table 1 of the summary document would make the companies “unviable” (I suspect not), but I will make arguments for how and why that number could be reduced without materially increasing taxpayer risk, and at the same time significantly lowering the cost and increasing the availability of mortgages to the large majority of homeowners Fannie and Freddie were chartered to serve. I recognize, of course, that there is a political dimension to the recapitalization of Fannie and Freddie, and that there will be some threshold capital percentage below which it will be very difficult to go, irrespective of the merits of the arguments for doing so. Building on the “Rule of Law Guy’s” observation, the range of dollar capital numbers for Fannie and Freddie as of September 2017 given in the FHFA summary table—from $154.1 billion without a deferred tax asset reserve to $180.9 billion with one—is virtually identical to the $155 to $180 capital range in the Moelis recapitalization plan released just over a year ago. I doubt this is coincidental, and it suggests we now are seeing some serious “fleshing out” of a pathway to administrative reform of the companies, if only for informational purposes. And it’s interesting that given the fundamentally high credit quality of the mortgages Fannie and Freddie finance, the only way to get to a 2.75 to 3.25 percent average capital number is to add a host of conservative buffers, a few of which are redundant. Hopefully some of those can be worked down as the discussion moves forward. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

+1 -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Rosner's paper on FHFA Capital Requirements... https://www.scribd.com/document/381737512/GF-Co-FHFA-s-Proposed-Capital-Rule PDF attached... 381737512-GF-Co-FHFA-s-Proposed-Capital-Rule.pdf -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Excellent point. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

love these guys... https://thenationalrealestatepost.com/11000-secret-fannie-mae-papers/ -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

the real Tim Howard... I’ve just now downloaded FHFA’s notice of proposed rule making (NPR) on Fannie and Freddie capital. I’m very glad they’ve done this. I’ll read it as soon as I can (it’s 368 pages), and definitely will submit a comment on it. https://howardonmortgagefinance.com/2018/05/03/a-view-on-affordable-housing/#comments -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

:-)

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Next up: Moelis... Note: attached image stolen from Twitter.

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

PDF only: https://www.fhfa.gov/SupervisionRegulation/Rules/RuleDocuments/E%20Capital%20to%20Fed%20Reg%20for%20Web.pdf -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Watt's Enterprise Capital Requirements released... https://www.fhfa.gov//SupervisionRegulation/Rules/Pages/Enterprise-Capital-Requirements.aspx -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

It appears David Stevens is no fan of Trump! I doubt he'd be publicly bashing POTUS at this juncture if he thought he was going to get his way with the GSE's. Similar to Corker bashing Trump awhile back when he realized his desires weren't going to materialize. https://www.housingwire.com/blogs/1-rewired/post/43640-monday-morning-cup-of-coffee-ben-carson-backtracks-on-plan-to-raise-rents-for-poor -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

I don't know anything about him, but Josh Rosner applauds the choice: -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Bob Broeksmit will be the new head of MBA, replacing David Stevens. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

In Multifamily Finance, Fannie and Freddie Are Still the Elephant in the Room https://commercialobserver.com/2018/06/fannie-freddie-conservatorship/ -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

New from the Milken Institute Housing Finance Program: Senior Fellows Michael Stegman and Phill Swagel begin a series of papers that focuses on the effectiveness of the affordable housing measures we have in place today. https://assets1c.milkeninstitute.org/assets/Publication/Viewpoint/PDF/WP-An-Affordable-Housing-Fee.pdf -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

David Stevens feels left out in the cold... https://www.insidemortgagefinance.com/imfnews/1_1371/daily/MBA-Wants-more-transparency-on-gse-activities-1000046308-1.html?ET=imfpubs:e10982:73599a:&st=email&s=imfnews -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

The narrative, slowly but surely, is shifting towards them being released from conservatorship. If it doesn't seem like they're in conservatorship (according to David Stevens' mouth piece IMF), then why keep them in that state? I know this isn't news to anyone that the conservatorship will end (Mnuchin has blatantly stated that), but those wanting to kill the GSE's are waking up to the fact that their desire won't happen, and it seems to me they are preparing themselves for that. No, I didn't derive all of that from one headline... but from what has transpired the past year or so. The GSEs in Conservatorship: Sure Doesn’t Seem Like It https://www.insidemortgagefinance.com/imfnews/1_1369/daily/gses-in-Conservatorship-Sure-Does-not-seem-Like-It-1000046264-1.html#Login -

Eric, I am so sorry to hear about the divorce you're going through. I know a lot of heartache, anger, confusion, etc. can come in a situation like this, especially when it's messy. I'm not sure if forgiveness and reconciliation is something that is possible or desired, but may I recommend the book As We Forgive: Stories of Reconciliation from Rwanda https://www.amazon.com/As-We-Forgive-Stories-Reconciliation/dp/0310287308/ref=sr_1_1?ie=UTF8&qid=1527132584&sr=8-1&keywords=as+we+forgive+stories+of+reconciliation+from+rwanda. My bride is the author and it speaks of very powerful instances where relationships are restored in the most dire of circumstances (victims forgiving the murderers of their loved ones). The stories are remarkable and I have benefited greatly from them in my own life with areas that have needed some level of forgiveness and/or reconciliation. If you, or anybody else reading this, would like a free signed copy send me a private message and I'll get it to you quickly. I pray for forgiveness and reconciliation between you and your bride, Eric, and general peace regardless of the outcome for you, her, and your children. I truly mean that.

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

I think many are going to be blindsided once Moelis gets implemented. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Indeed very interesting. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

I heard it too. It shouldn't be too surprising, right? It's just nice to hear "utility model" - as long as that keeps coming up that means Moelis is in play.